China’s Interbank Squeeze: Understanding the 2013 Drama and Anticipating 2014

This note assesses recent developments in China's inter-bank market and puts them in context with the Chinese reform outlook.

In mid-December 2013, as in June, China’s benchmark money market rates shot up as the People’s Bank of China (PBOC, or “the Bank”) declined to inject liquidity to satisfy business as usual growth in credit among banks. These two end-of-quarter incidents were dubbed “cash crunches” by most observers, but to us that term mischaracterizes what’s going on and glosses over the important differences between these two episodes.

The year 2014 has started off with additional drama over credit markets in China, and concerns that rising costs could lead to defaults for some risky financial products and end up spilling over to a broader financial crisis in China. In this note we explore the current situation and the recent changes in money market structure. We also consider the common view that the central bank is not in control, and whether its intervention can steer reform for the coming year. As we held throughout 2013, we believe the Bank knows what it’s doing, is being as rational as it can be in the context of China’s unique political crosswinds, and will play a decisive role in shaping 2014 outcomes.

PBOC’s death is wholly exaggerated: Many pundits have been writing that the Bank has lost control of monetary conditions in China and is flailing about making policy mistakes. The opposite is true: in 2013, the Bank demonstrated that it is precipitating corrections, not reacting to them, and can apply differentiated tools in the face of different pressures.

Higher rates boost foreign opportunities: Since the Bank is acting decisively, and not reacting to something it can’t manage, the higher borrowing costs it has engineered are likely to stick through 2014. At this elevated level, they will start to change business patterns in the real economy. Resulting stress for both Chinese financials and real economy firms will, in our view, widen opportunities for their foreign cousins.

High stakes, but no meltdown: Continued business-as-usual debt creation would lead to national insolvency in a few years at the current rate of growth, but the aggressive measures being taken to avoid that won’t seize-up the system in China, since government controls both sides of the ledger. In fact China has had far fewer defaults – which are a normal reality in a market economy where investors must take responsibility for their risk/return choices – than it should for its size, and this is part of growing up and getting stronger.

BREAKING DOWN THE MONETARY BASE

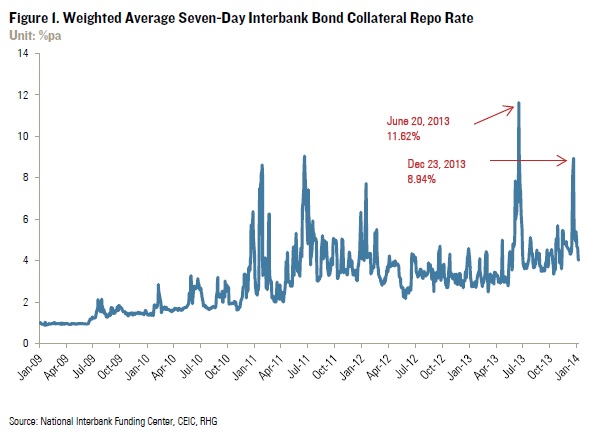

Ask any trader in China what the most critical dates in 2013 were and chances are they will say June 20 and December 23. On those two days interbank borrowing costs spiked severely, sending traders and banks scrambling for money to cover their positions until the last minute of market closing. Rumors of bank and wealth management product defaults cascaded, and the PBOC seemed to fuel panic by remaining on the sidelines and declining to supplement liquidity as was normally expected [Figure 1].

In late June 2013, as major media were flashing “cash crunch” headlines and seven-day interbank repo rates soared to 11.62% (almost triple current rates as of this writing), the PBOC issued a notice observing that “total liquidity isn’t in shortage”. Indeed, on June 21 financial institutions’ total excess reserves at the central bank were about 1.5 trillion RMB, more than twice necessary levels (according to the PBOC), in addition to about 18 trillion RMB of required reserves. During the December cash crunch, the PBOC used an unusual platform – the Twitter-like Weibo – to note that excess reserves remained around 1.5 trillion RMB, at a “relatively high historical level”. With so much excess reserves in central bank vaults, why were the banks still short of cash?

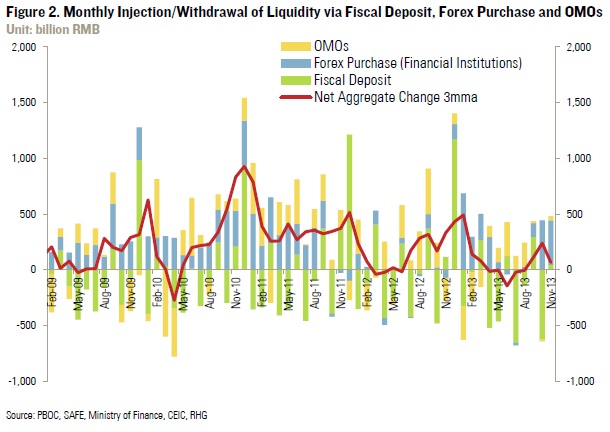

The problem isn’t aggregate funds and obligations, but the structure of specific indebtedness and also the PBOC’s capacity to manage market expectations. Let’s first take a look at the three major sources of state influence over China’s monetary base: fiscal deposit injections, forex purchases, and PBOC open market operations (OMOs). These are the regular channels through which the Bank provides liquidity to the market, and then banks leverage this high-powered money up through various lending activities. To make sense of the battle being fought in Beijing, it’s necessary to look more closely at these three channels [Figure 2].

- Fiscal deposit flows: Fiscal deposits are money placed with the PBOC by various levels of government through banks. Placement of fiscal deposits at the PBOC by government offices withdraws liquidity from the market, and injection of fiscal deposits means government expenditures occur, drawing money from PBOC accounts back to the banking system, increasing liquidity. Fiscal deposit flows are highly seasonal, often increasing liquidity at the end of the quarter as government spends money to meet budgetary objectives, and withdrawing liquidity over the rest of the quarter. For the last two months of the year traders can generally estimate the volume of fiscal deposit injections based on flows over the first ten months and the central government budget published at the beginning of the year, and execute trades accordingly. Fiscal deposit data is released monthly by the PBOC in its “Summary of Sources and Uses of Credit Funds of Financial Institutions (RMB)” (“Summary”) – financial institutions in the table include the PBOC, other banks, trust companies, financial lease companies and auto financing companies. A decrease in “fiscal deposits” means increased liquidity in the economy. In November 2013, the latest month data available, the injection of fiscal deposits was 43.5 billion RMB, and in June, it was 122 billion RMB.

- Forex purchases: Foreign exchange (forex) purchases involve local currency (renminbi) injected into the economy in exchange for foreign currency-denominated assets bought by the banking system. The PBOC can only impact forex inflows partially because forex transactions are hard to track and voluminous nowadays, and include both legal trades and hot money inflows. When Beijing launched a crackdown on export over-invoicing and hot money inflows in the spring of 2013, forex purchases fell sharply from 294 billion RMB in April to 67 billion RMB in May, before turning negative in June. To smooth the volatility caused by forex inflows, the PBOC conducts offsetting operations; when it fails to do so the mismatch of market expectations creates problems. In the Summary, increasing forex purchases mean more liquidity in the market (which can be countered by sterilization operations). In November 2013, total purchases of forex added 398 billion RMB to liquidity, while in June they withdrew 41 billion RMB. PBOC sterilization operations were conducted with reserve requirements, OMOS (see below) such as bill issuance (which are transparent but haven’t been employed lately) and other liquidity tools which are non-transparent (see below), leaving the net effect on liquidity somewhat unclear. Some analysts use the monthly increase of excess reserves at the central bank and other public data such as fiscal deposits and currency in circulation to estimate the net sterilization effect, but PBOC doesn’t provide an exact number.

- Open market operations: OMOs are another monetary policy option the Bank can deploy to influence market liquidity. Regular OMOs include central bank bill issuance, repurchase agreements, and reverse repurchase agreements. These instruments carry a maturity period ranging from a few days to three years, and when they mature they impact market liquidity in the opposite way to their initial effect. Data on OMOs is released by the PBOC as they are carried out, with publication on the Bank’s website, and at the CEIC, Bloomberg and Wind databases.

In January 2013 the PBOC introduced two new tools to adjust liquidity more swiftly and accurately. One is Short-term Liquidity Operations (SLO), in which the PBOC provides credit to designated large banks for no more than seven days, with details not published until one month later. The other is a Standing Lending Facility (SLF). Compared to SLO, SLF has a different maturity period –previously one to three months but in January 2014 for just a few weeks to get past Chinese New Year – and it is also different in that announcements on the PBOC website don’t follow a regular schedule. The next release, of Q4 operations, will probably be in PBOC’s Q42013 monetary policy report in the coming month.

In addition to these interventions, several other factors affect the monetary base from the supply side, including central treasury cash auctions, forex flows not purchased by the banks, changes in the required reserve ratio (RRR), and unpublished and irregular injections and withdrawals of credit by the central bank such as by forcing the big banks’ hands in holding forex privately. However, unlike the three formal channels defined above, these are not considered regular PBOC interventions and data on some of them is lacking.

THE CRUNCHES: MISMATCHED EXPECTATIONS AND PBOC STERILIZATION

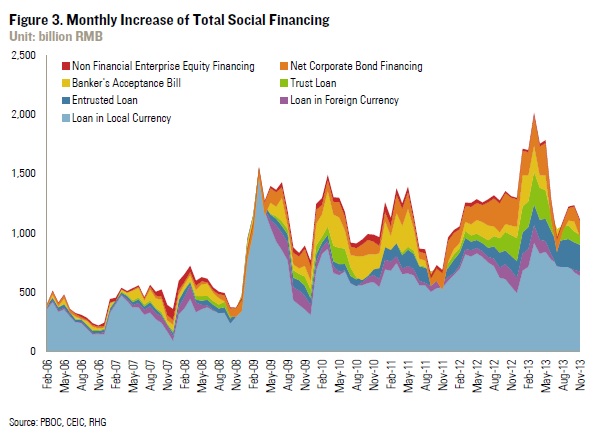

Many assumed the November-December 2013 liquidity squeeze was a repeat of June, but details were different in important ways. Starting in May, a Beijing crackdown on hot money inflows – partly out of determination to arrest the shadow banking sector getting out of control – choked down on forex inflows. The central bank not only refused to provide extra liquidity to offset the crunch, it kept conducting repurchases until June 9, thus continuing to withdraw renminbi from the market as well. PBOC also issued 92 billion RMB of central bank bill in May and 22 billion RMB more in June to further tighten credit. The Bank’s stance, and the evident lack of opposition to it from the nation’s paramount leaders Xi Jinping and Premier Li Keqiang, was a stark reversal from 1Q13, when total social financing (TSF, the broadest measure of new credit in China) rose to levels not seen since the financial crisis stimulus program in 2009 [Figure 3].

The Bank’s abrupt switch in stance caught the large state banks off guard. They had (dangerously) refused to believe that the Xi-Li Administration meant to break with business as usual up to this point; nor had they bet on American tapering so early – Bernanke signaled the end of QE on June 19 – given their poor read on US fundamentals (they had little presence in the US and senior leaders were preoccupied with Chinese conditions). The market began speculating that an unusual meeting of the Politburo Standing Committee at the end of April 2013 might have made a 180-degree turn in monetary policy. The large banks flipped to cash hoarding mode in the first weeks of June, and though they had roughly 1.5 trillion RMB of excess reserves with the PBOC they refused to deploy this cash to help midsized counterparts make up for the PBOC’s absence from the interbank market.

With the end of the 2Q13 looming, smaller shareholding banks were at risk of disaster within days. Their predicament dated to the second half of 2010, when Beijing faced up to the need to discipline the liquidity explosion echoing from the 4 trillion RMB 2008-2009 stimulus program. With trillions tied up in long-term infrastructure and property projects years from generating cash flow, but with mismatched short-term debt repayment obligations and reported liquidity growth that had to be staunched, the smaller banks used to finance the local stimulus projects were told to go to these interbank markets (which are generally off balance sheet and not subject to lending/deposit ratio regulations) to stay solvent and avoid disorderly defaults. As a result, by 2013 the scale of the credit created by the interbank market was second only to proper RMB loans, as the PBOC’s 3Q2013 monetary policy report makes clear.

The big question in June was whether the PBOC anticipated these consequences of clamping down on interbank credit creation and higher borrowing costs, and whether they were in control both before and after US Fed tapering signals poured gasoline on the fire. To our minds, the addition of a new, special column introducing the SLO and SLF tools in the Bank’s Q1 monetary policy report published May 9 (just after the April 26 Politburo Standing Committee meeting), to be used “when multiple liquidity determinants reinforce each other or when market expectations change, [and when we are] likely to see short-term liquidity shortages that cannot be timely eased by money market financing”, makes clear this was an anticipated war of choice. This short sentence closely described what happened six weeks later. Why didn’t the Bank advertise its intentions more broadly then? Our belief is that doing so would have invited a maelstrom of preemptive criticism of the Bank from still powerful vested interests wanting growth at all costs. Remember, the vast majority of elite Chinese and foreign economists and political scientists still believed Xi Jinping would be a compromised, compromising leader at this juncture. The PBOC was doing its best to steer between preventing a systemic collapse and imposing capital discipline to deliver Xi’s reform commitment, and doing a pretty good job of it. And then on June 19 Ben Bernanke signaled (prematurely it turned out) the end of quantitative easing and the beginning of a taper, and that turned a managed squeeze of forex hot money out of Chinese markets into a more alarming rush. These external impacts, combined with murky expectations between regulators and banks, leavened by the end of the Bernanke put (guarantee of copious quantitative easing of liquidity), sent interbank rates to a dizzying June 20 peak.

To get the saddle back on market expectations the Bank published a special note on June 25 with three messages. First, the PBOC could see 1.5 trillion RMB in excess reserves — more than enough to meet settlement needs – through the crunch, so they knew the liquidity shortage was not aggregate. And they had the ability to compel those in surplus to lend, which they did (picking up the phone and telling them to get to it). Second, to deleverage and reduce off-balance sheet lending risks, the central government would henceforth remain tighter, while actively using shorter-term tools such as re-discounting, SLO and SLF to manage (not eliminate) tensions (eliminating risk for some borrowers was precisely the problem that got China into its current debt mess!). And third, while large banks could ultimately count on the PBOC to provide liquidity, they were expected to be market stabilizers, channeling money to smaller banks when necessary. The implicit message was that these squeezes would happen again, and big banks should prepare, and smaller banks should adjust their balance sheet and asset structures. While Beijing leaned toward more accommodation to offset downside anxieties in a fiscal and liquidity injection from late July 2013, this was tactical, and not an alteration in the overall level of seriousness about draining the shadow banking swamps.

After the June 25 note was released, confusion over the central bank’s stance was largely resolved – or should have been. Anxiety in November and December was therefore not a repeat of June, but rather a different story. As Figure 2 makes clear, the financial system’s forex purchases (injecting RMB into the market) resumed in August and continued through November, and are likely to have continued in end of year data. Probably 75% of this was sterilized. Washing most of the remaining forex purchase liquidity out was the lack of a year-end ramp up in fiscal deposit injection in November. Compared to an average of 234 billion RMB in government budget funds released to check-writing bureaucracies in the previous three Novembers, the 2013 figure was only 43.5 billion RMB, a reflection of the central anti-corruption campaign and seriousness about ending wasteful infrastructure and overcapacity industry projects. For instance the new 2014 railway fixed investment target was just publicly set to shrink from 2013, a surprise to market expectations. This is the reality: if you are serious about rebalancing and big bang economic reforms, then you have to put your money where your mouth is and reduce investment growth. December is the biggest month for fiscal injections, and it will be much bigger than November, but the trend seems to be much smaller than expected.

So much for fiscal behavior at year-end; on the monetary side the PBOC again took no action to offset the shortfall – instead amplifying them by suspending reverse repos entirely for two weeks, further draining capital. In its 3Q2013 monetary policy report the Bank once more spelled out its intention to address interbank off-balance sheet lending and credit product maturity mismatches. In addition, if leading market traders are to be believed there was additional unannounced capital withdrawal in the first half of November caused by SLF maturity; as noted above, SLF interventions and their reversal are not always reported by the Bank. If this was the case, it may be discernable in the Bank’s 4Q2013 report released in late January or early February (before or after Chinese New Year). Taken together, the evidence is clear that the PBOC worked to drain cash from the banking system over the past three quarters since April 2013, driving up money market rates and reducing the rewards of risky lending and credit product creation. This is not just the flavor of the moment, but serves the Standing Committee’s top level priority of reducing systematic risks and forcing banks to strengthen liquidity controls and reduce funding to overheated sectors through under-regulated channels that circumvent controls.

THE NEW NORMAL?

By our estimate average 2013 money market rates were 150% of the previous ten years’ average. For 2014 the Bank has pledged a prudent monetary policy stance, and in light of interest rate liberalization signals such as the restart of certificate of deposits, markets are expecting interbank rates to float in the current range (currently just over 4% for seven-day repos, down from the December 23 high of 8.94% but still four times January 2009 levels). So what implications does this have for the money market and the real economy in 2014? We have two working conclusions.

First, shareholding banks and other financial institutions that were fed on off-balance sheet lending in the past three years will go through painful restructuring in 2014. They need to adjust their asset structures and bring their gray-area banking activity back to the balance sheet. During this process we believe there will be recurring trust product defaults, though without any real risk of a banking system collapse. The PBOC foresees these problems and has an actively adjusted opinion about the degree of resilience in the system – a much clearer view of that than anyone outside the Bank in fact, by an order of magnitude. That is not hubris on the Bank’s part. This is not Soros against the Bank of England; Beijing has sacrificed the benefits of open financial markets prone to speculation in exchange for retaining control over the institutions with access to its credit system: the PBOC is not independent, but it has asymmetric dominance in terms of systemic liquidity information.

When “cash crunches” like last June happen, or when the Bank makes them happen, the Bank has tools with which to manage short-term liquidity without abandoning the goal of long-term deleveraging – the political system of China is finally backing them up and moving institutions, incentives and expectations in the right direction. In January 2014 they demonstrated this again, lest anyone think 2014 would be more placid: the usual pre-Chinese New Year cash demands and the unusual appetite for cash to fund stock buying accounts for newly relaunched IPO markets sent interbank markets right back up for short-term funds. The Bank let them rise, even while rumors of high-return but risky wealth management product (WMPs) defaults swirled, before injecting the cash the market needed, at high rates, for short durations. The risk is not from the Bank’s gaming the market to impose a new, more conservative set of credit expectations; rather, it is that leverage continues to build up too quickly, and in non-transparent ways, and due to undisciplined political fiat such as ruled the Ministry of Railways in recent years. That is an acute medium-term risk, though for the moment Xi is making progress convincing skeptics that he really is going to shift the patterns of investment.

Second, in 2014 rising borrowing costs will mean repercussions for the real economy: industries that used to rely on cheap capital, especially those in overcapacity, such as steel, cement, glass, and even rail, face strong headwinds in financing. As mentioned above, the just -concluded national railway network conference (a senior-level central affair for this “strategic” sector) announced that the fixed asset investment goal for rail in 2014 was 630 billion RMB, 30 billion RMB less than what was spent last year. Targeting lower growth in 2014 was well beneath market expectations, given how important rail investment was in anchoring Chinese growth targets over the past five years. With falling rail FAI and steel sector consolidation, rising export surpluses thanks to a strong US will not be enough to get China to the rumored 2014 7.5% growth target (we still bet that high a target will not be announced). In response to the financial crisis huge industrial and property investment kept China sailing relatively smoothly, underwritten by largely unregulated shadow bank lending. Off-balance sheet activity and over-investment in China are two sides of the same coin, and if Beijing is determined to tackle either of them then the either side will be affected too. The most productive real economy firms in China – the ones that have to pay the bills and create the sustainable jobs going forward – are completely tangled up in this legacy. Cutting through this in 2014 is going to be messy. Ultimately, this year, we see no alternative for Beijing other than letting capable, productive private businesses off their leash so they can help pull the economy out of the ditch.