China’s Subsidies Are Fueling “Involutionary” Competition in the Auto Sector

Setting subsidies at fixed, nominal levels pushes consumers to buy lower-priced cars to get a bigger implied discount, which is pushing the industry toward intense competition at lower price points.

China’s highly publicized auto subsidies may be contributing to price wars and entrenching “involutionary competition” within the industry. Setting subsidies at fixed nominal levels encourages buyers to choose lower-priced cars to maximize discounts. The persistence and expansion of these subsidies has shifted the whole industry toward competition among models at lower price levels. These auto subsidies will be very costly in 2025, estimated at 3% of total central government fiscal revenue and equivalent to 7% of auto retail sales. We expect auto subsidies to extend at least into 2026 to avoid a sharp decline in sales. Given that the NEV purchase tax exemption will be halved in 2026 and 2027, sales are still likely to slow in the years ahead without additional measures to bolster the impact of subsidies.

Race to the bottom

“Involutionary competition” has become a key focus of China’s official rhetoric over the past few months. In the auto sector, talk has focused on combating deflation by limiting price wars and consolidating firms. In June, the Ministry of Industry and Information Technology (MIIT) summoned original equipment manufacturers (OEMs) to Beijing and told them to stop price wars and reduce timeframes for payables to their suppliers. MIIT also reportedly took measures to prevent OEMs reporting “zero mileage” (e.g., brand new) cars as used car sales to inflate total sales levels. A July State Council meeting pledged to regulate irrational competition in the auto sector and strengthen product quality inspections.

The irony here is that the subsidies powering auto sales are themselves probably incentivizing “involutionary competition” among automakers and falling sales prices across the sector. To see if this is the case, we examined indicators of prices, market structure, and market exits to see how subsidies changed sales patterns. We also compared the effects of subsidies in the auto sector to those in home appliances and consumer electronics.

Scrappage (where cars must be scrapped to qualify) and trade-in subsidies in the auto sector are usually set at a fixed level, rather than a percentage, encouraging buyers to choose lower-priced cars for higher implied discount rates. In addition, the subsidies have likely slowed progress toward consolidation of the auto sector, as they have kept more OEMs afloat while also dragging them into fierce competition in lower price ranges (Figure 1).

Estimated auto purchase subsidies from the central government will reach a record high of 342 billion yuan in 2025, including 150 billion yuan in scrappage and trade-in subsidies and 192 billion yuan in auto purchase tax exemptions for new energy vehicles (NEVs). This is equivalent to 3% of estimated central government fiscal revenues and 7% of passenger car retail sales this year.

Despite the high costs and the “involutionary” nature of these subsidies, the ongoing slowdown in household income growth and consumption will likely force policymakers to extend them through at least 2026 and maybe even further to 2027, according to our model anticipating auto sales over the next few years. Given that NEV tax exemptions will be halved in 2026 and 2027, auto sales may fall off a cliff if the scrappage and trade-in subsidies are phased out at the same time. This highlights the significance of improving the incentive mechanism and eligibility criteria for the subsidies to enhance multiplier effects and to reduce the negative impact on prices.

Strong growth in volumes, tiny growth in revenues

The current round of auto sector stimulus started in April 2024 with the announcement of new scrappage subsidies (Figure 2). Owners scrapping eligible older vehicles would be rewarded with a 7,000 yuan subsidy if they purchased new cars with internal combustion engines (ICE) or with a 10,000 yuan subsidy for purchases of new NEVs.

However, these initial subsidies did little to encourage new sales. Most owners of older cars bought them at low prices from the secondary market and therefore may not have found the subsidies attractive relative to the prices of new vehicles. Subsidies were then doubled in August 2024 to 15,000 yuan and 20,000 yuan for purchases of eligible ICE cars and NEVs respectively, after existing cars were scrapped. In addition, local governments initiated trade-in subsidy programs to further spur replacement demand. The central government’s coverage of these subsidies also increased from 60% to 90%, alleviating some of the fiscal burden for local governments. This supported 2024 passenger car retail sales, which expanded by 5% to 23 million units in 2024, with around 29% of sales subsidized.

Both subsidies were extended into 2025 after a short pause in January, while Beijing also expanded the eligibility criteria for scrappage subsidies. Trade-in subsidies determined by local governments were capped at 15,000 yuan for new NEV purchases and 13,000 yuan for new ICE car purchases to avoid localities competing with one another to offer higher subsidies. Because the program started early this year, the proportion of subsidized sales volumes is now even higher, at 47% through May.

Data for June auto subsidy applications was not disclosed as several provinces had already used up the first two batches of funding for these incentives. The central government has already allocated 54% of the 300 billion yuan in trade-in subsidy funding to autos, home appliances, and electronic sales in the first half of the year. The third batch of 69 billion yuan in funding was allocated in July, with another 69 billion yuan to be allocated in October. But there is a risk that the funds may dry up before or during the peak sales season in Q4, while base effects may weaken retail sales growth at that time.

Despite concerns about the availability of subsidies in H2 2025, auto subsidies have fueled 11% growth in passenger car retail sales to 11 million units in H1. However, these surging sales volumes only generated 0.8% growth in total values of auto retail sales, according to the NBS. This would imply a 10% y/y decline in average car prices, worse than a 4% implied drop in average prices in H1 2024. But auto discount rates and CPI for the sector suggested smaller year-on-year price cuts in 2025 than 2024 (Figure 3). The CPI for ICE cars improved from a 6% fall last June to -3.4% this June and the same indicator for NEVs narrowed its drop from 7.4% to 2.5%.

The data points to an interesting set of conclusions. Prices of individual autos are still falling, but at slower rates than last year. But for the sector as a whole, average prices are down by wider margins. This likely points to a change in the overall market structure in which cheaper models are now a larger proportion of the market, especially for NEVs, which made up more than 50% of total sales in H1.

Other pricing data points to the same conclusion. We calculated market share proportions for NEV passenger car retail sales by price range from August 2024 to June 2025, after the scrappage subsidies were doubled and subsidized sales surged. We then compared the distribution of sales from August 2023 to June 2024 (Figure 1). The market share of NEVs priced above 150,000 yuan has dwindled by 8 percentage points, with premium models in the 300,000 to 400,000 yuan price range performing the worst. NEVs in price ranges of 100,000 to 150,000 yuan and below 50,000 yuan benefited the most from the subsidies, gaining 4 and 3 percentage points of market share respectively.

Entrenching “involutionary competition”

Multiple factors have contributed to the downward structural shift in prices across China’s economy, including slower income growth among high-income families and lower raw materials prices. “Consumption downgrading” dynamics have also impacted sales of other products eligible for trade-in subsidies, such as home appliances and electronics. But for those products, the trade-in program lifted average sales prices (Figure 4). This suggests that the key factor leading to falling average auto prices is probably not specifically linked to lower income growth or weaker consumption activity.

The devil is in the details for trade-in programs. Scrappage and trade-in subsidies for autos are usually set at constant levels,1 while subsidies for home appliances and electronics are set as a discount rate of 15-20% with a cap for the maximum subsidy offered. As a result, auto buyers will prefer lower-priced cars for higher implied discount rates. The maximum NEV subsidy is 20,000 yuan per unit, and to achieve a minimum 15% discount rate (comparable to that of home appliances and electronics), a buyer would only consider cars under 133,333 yuan. This is consistent with the shift in the market structure of sales to NEVs priced below 150,000 yuan.

Another difference in the settings for trade-in programs concerns requirements for product quality. Most NEV models2 and ICE cars with engine displacement up to 2 liters meet eligibility criteria for the subsidies, while those for home appliances and personal computers are only offered on products meeting energy or water efficiency standards of grade II or above. Higher subsidies for more expensive products encourage consumer upgrading.

There have been three other rounds of stimulus for auto sales as counter-cyclical subsidies to offset growth shocks: during the global financial crisis (2009-2010), deleveraging and supply side reform (October 2015-2017), and COVID-19 lockdowns (in the second half of 2022). Compared to these previous rounds of subsidies, the current scrappage and trade-in subsidies probably have the most “involutionary” incentive mechanism to reduce aggregate price levels. Auto purchase tax incentives are a de facto discount rate with a capped level of subsidy. They do not disproportionately discourage premium auto sales and are also available to first-time buyers. Promotion subsidies for NEVs are set at different levels for models of different driving ranges and powertrains (battery vs. hybrid), encouraging consumption upgrades by setting higher standards over time.

In contrast, scrappage and trade-in subsidies incentivize consumption downgrades, spurring growth in sales volumes and consequently keeping more OEMs afloat. The number of auto sector companies defaulting on their commercial paper and corporate acceptances, a proxy for market exits, has decelerated since mid-year 2024 (Figure 5). The combination of these two features has set back consolidation in the auto sector.

Concentration rates for NEV sales across firms had stabilized in H1 2024 from the fall in 2023. But the trend of rising concentration of market share reversed from August 2024 when scrappage subsidies were doubled and trade-in subsidy programs were introduced (Figure 6). Even BYD’s market share started to fall from last October, losing share to newly launched Geely Xingyuan and Wuling Hongguang MINI models below 100,000 yuan as well as the Geely Galaxy Starship 7 and Xpeng Mona M03 models below 150,000 yuan. Consolidation of the upstream battery sector also stalled, with the market share of the top three power battery producers declining from 80% last May to 73% in May 2025.

Similar consequences emerged when the home appliance subsidy program for rural areas was active from 2008 to 2013. Eligibility for the subsidies was limited to home appliances below a price cap, which helped low-end manufacturers regain market share and aggravated overcapacity within these industries. By 2012, major manufacturers including Haier, Midea, and Gree all opposed the MIIT extending these subsidy programs.

The home appliance trade-in subsidy program has improved, but the auto sector might now be facing similar consequences. Auto subsidies likely entrenched “involutionary competition” by dragging OEMs into competition at lower price ranges and hindering sector consolidation and market exits. Operating profit margins of the auto sector have fallen from 5.1% in the first five months last year to 4.2% this year through May.

When will policymakers exit these costly subsidies?

We estimate passenger car purchase subsidies from the central government will reach a record high of 342 billion yuan in 2025, including 150 billion yuan in scrappage and trade-in subsidies and 192 billion yuan in auto purchase tax exemptions for NEVs. This is equivalent to around 3% of total estimated central government fiscal revenues and 7% of passenger car retail sales this year (Figure 7). This round of subsidies is much more costly than similar programs in the past.

We adopted a Gompertz model3 based on the real wage index4 to predict auto ownership growth, and a survival curve model5 to predict scrappage rates. The idea is to compare actual subsidized sales with theoretical sales without subsidies to evaluate the efficacy of auto purchase subsidies in boosting overall auto sales in volume terms (Figure 8).

Growth of the real wage index slowed sharply from 5.4% in 2019 to 2.1% in 2024, even using the official NBS data on wages and incomes. We set real wage growth at 3% in 2025, then expect it to weaken to 2.7% in 2026 after front-loading of trading activity ends, and then to climb back to 3% in 2029-2030. These are fairly conservative assumptions in our view, based on the idea that a rapid acceleration of wage growth in the years ahead is still very unlikely (See July 2024, “No Quick Fixes: China’s Long-Term Consumption Growth”).

Subsidies from 2009 to 2010, 2016 to 2017, 2022, and 2024 to 2025 generated additional sales from theoretical baseline levels by 31%, 27%, 10%, and 54%, with subsidies equivalent to 0.6%, 1.2%, 1.5%, and 2.4% of central government fiscal revenues. Subsidies from 2009 to 2010 were the most efficient in boosting sales while subsidies in 2022 were the least effective, likely due to limited travel under COVID-19 lockdowns. The cost of the 2024 to 2025 subsidies was higher because of weaker income growth.

Temporary subsidies do not create new demand, but rather pull future demand forward. The shortfall of actual sales from theoretical sales can be observed from 2011 to 2013 after the subsidies offered in 2009 and 2010. However, such shortfalls were negligible after the subsidies in 2016 to 2017 and 2022, as they were presumably offset by price discounts offered by dealers and automakers as well as local government subsidies.

If auto subsidies are cut off before theoretical sales recover sufficiently, price wars and additional local government subsidies could return. This would of course be contrary to leadership’s intention to combat “involutionary competition.” The model predicts that theoretical sales should further rebound from 2027 and increase back to the 20 million unit level in 2028, when replacement demand picks up, given the scrappage of cars sold in previous years.6 This trajectory implies that subsidies need to be extended through at least 2026 and possibly through 2027.

However, central government fiscal revenues have plateaued around 12 trillion yuan since 2022 (see March 24, “China’s Harsh Fiscal Winter”), given the decline in tax revenues driven by investment-led growth. Beijing is also facing a dilemma as approximately 65% of scrappage and trade-in subsidies are extended for NEV purchases, while these cars are exempt from the 10% auto purchase tax, the consumption tax based on ICE displacement, and vehicle and vessel taxes paid to local governments. This situation is unsustainable from a tax revenue perspective, and it’s been announced that NEV purchase tax exemptions will be halved in 2026 and 2027. The Ministry of Finance and the State Taxation Administration (STA) also announced that purchases of luxury NEVs priced above 900,000 yuan will require consumption tax payments from July 20, adding to downward pressure on prices in this limited market segment.

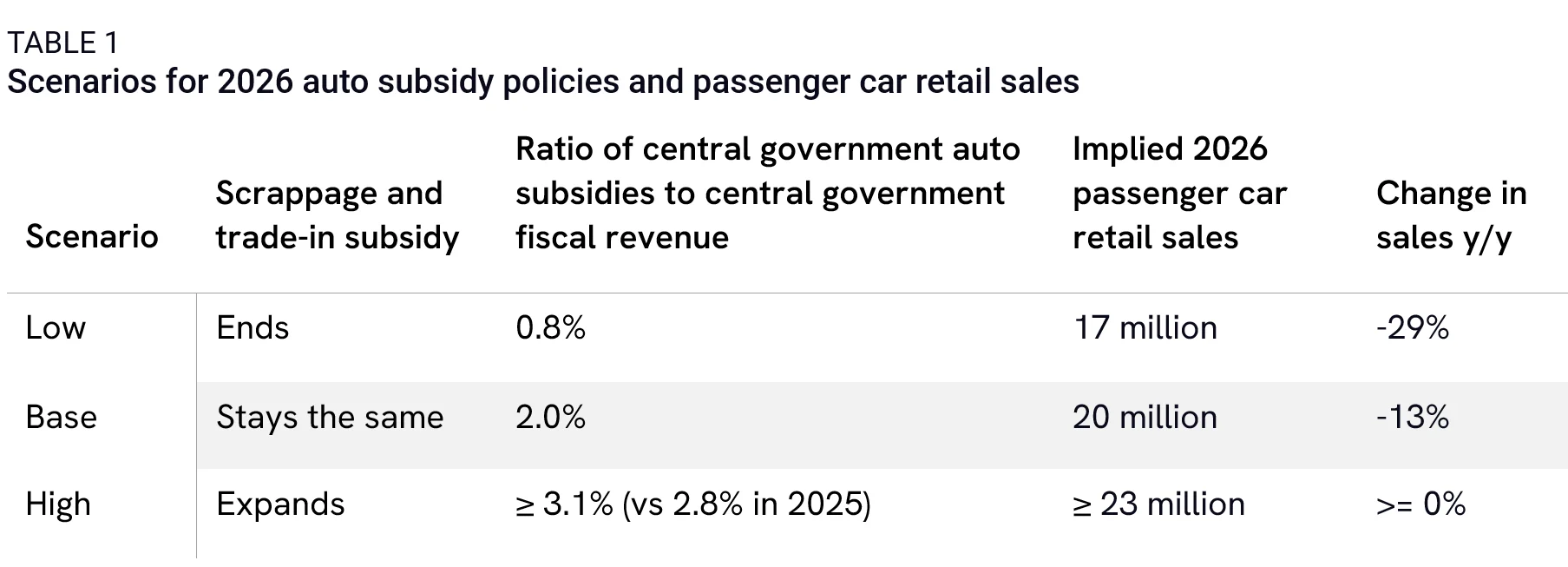

Halving NEV purchase tax exemptions could reduce total subsidies by around 100 billion yuan. Based on the implied efficacy of subsidies this year, passenger car retail sales volumes could report double-digit declines next year if scrappage and trade-in subsidies are also phased out at the same time (Table 1). It is therefore more likely in the context of China’s weakening economic growth that these subsidy programs will be expanded to levels between the “base” and “high” cases to offset part of the negative impact on sales from cutting tax exemptions in half.

However, this also suggests even weaker average price levels in the industry, as scrappage and trade-in subsidies will continue to incentivize lower-priced cars. Lower profit margins at home will also motivate OEMs to expand more aggressively in overseas markets.

Measures to improve the subsidy program’s incentive mechanism and the multiplier effect are thus crucial to mitigate the “involutionary” consequences from the subsidies and to boost sales. Potential measures include:

- Setting subsidies as a standard discount rate with a capped maximum level, similar to trade-in subsidies for home appliances and electronics;

- Setting higher subsidies on higher quality autos with greater energy efficiency, or technological features such as more advanced self-driving systems;

- Expanding eligibility criteria to include first-time buyers. The China Passenger Car Association estimated that the proportion of first-time purchases within total auto sales dropped to 35% in H1 2024 from 70% in 2016. First-time buyers will not benefit from scrappage or trade-in subsidies, but do represent an important source of demand;

- Providing special subsidies to migrant workers and rural families. 31% of migrant workers and 35% of rural families have cars, lower than the 42% national average in the 2020 census. This suggests greater potential growth in sales in rural areas once there is demand. These measures will be more effective if combined with transfers to migrant workers to improve their healthcare and pension benefits.

Footnotes

Trade-in subsidy policies vary by province. Some provinces provide higher subsidies for higher-priced new cars. For instance, Beijing offers 15,000 yuan subsidies to new purchases of NEVs priced at or above 200,000 yuan and offers a 13,000 yuan subsidy to new purchases of NEVs below 200,000 yuan. But it’s generally not a discount rate.

Scrappage subsidy requires newly purchased auto models to be listed within MIIT’s catalogue of NEVs eligible for auto purchase tax exemption, which include all models with a driving range exceeding 200 km and battery energy density greater than 125 Wh/kg. Trade-in subsidy eligibility varies by province and can be more expansive than scrappage subsidies.

The Gompertz model is a type of S-shaped curve to describe a growth process that starts slowly, accelerates, and then slows down to saturation levels. This feature makes it useful to model auto ownership based on income growth.

Real wage index is simulated using private and non-private urban wage and employment data, then deflated by CPI. Private urban wages prior to 2008 are estimated as 60% of non-private urban wages.

The survival curve model predicts the probability that a vehicle remains on the road at a given age.

The scrappage subsidy showed limited efficacy compared to trade-in subsidy. We do not expect the scrappage subsidy to draw scrappage replacement demand forward from theoretical levels significantly.