Note

Clean Investment Monitor: US Q3 2023 Update

Investment in clean technologies is continuing at record levels in the US, as demonstrated by new data from the Clean Investment Monitor.

New analysis from the Clean Investment Monitor compares on-the-ground clean investment progress with projections of the Inflation Reduction Act.

A year and a half has passed since the Inflation Reduction Act was signed into law, and more than two years since the enactment of the Infrastructure Investment and Jobs Act. These two pieces of legislation represent the largest public investment in clean energy and transportation in US history, designed to incentivize far larger private investment. The Clean Investment Monitor (CIM), launched in September 2023, tracks public and private investment in technologies covered by those bills on a quarterly basis, to provide policymakers and stakeholders with timely information on the state of clean energy and transportation manufacturing and deployment in the United States.

The CIM can also be used to compare on-the-ground progress on clean energy deployment and GHG emissions reductions with projections of the impacts of the IRA and IIJA, developed shortly after their adoption. In this report, we take stock of progress in two key areas: the construction of new utility-scale clean electricity generation and storage capacity, and the sale of battery electric vehicles, plug-in hybrid vehicles, and fuel cell vehicles (referred to collectively as “zero emission vehicles” or ZEVs).

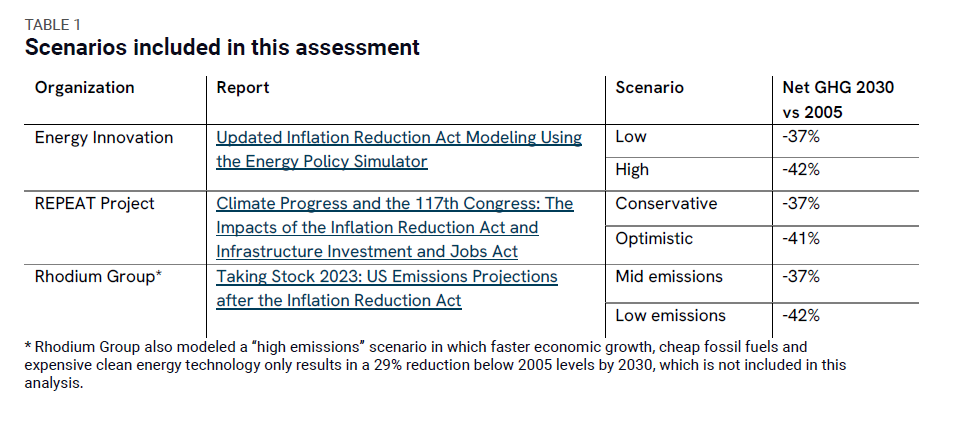

We compare actual progress in 2022 and 2023 in the CIM database to projections from three organizations whose assessments of the potential impact of the IRA and IIJA are widely used by policymakers and stakeholders: Energy Innovation (EI), the REPEAT Project at Princeton University, and Rhodium Group. All three groups modeled scenarios for IRA/IIJA implementation that found the possibility of a 37-42% reduction in US net GHG emissions by 2030 relative to 2005 levels (Table 1). This is broadly in line with the authors of the IRA’s stated objective of achieving a 40% reduction in emissions by 2030.

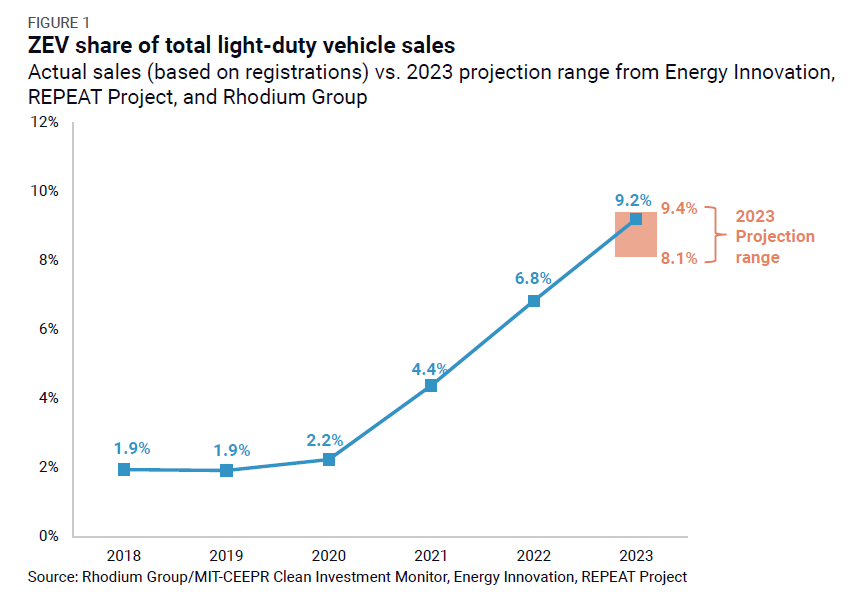

Over the past several months, there have been a number of news stories suggesting the US is experiencing a slow-down in electric vehicle sales, but sales in 2023 came in at the top end of the range of post-IRA projections. Based on preliminary 2023 CIM data, we estimate that 1.43 million ZEVs were sold in the US in 2023, the vast majority of which were battery electric vehicles. These sales account for 9.2% of total light-duty vehicle sales last year, up from 6.8% in 2022 and 2.2% in 2020 (Figure 1). Post-IRA analysis from EI, REPEAT, and Rhodium projected an 8.1% to 9.4% ZEV sales share in 2023. While actual sales came in at the top end of the range of post-IRA projections, they dramatically exceeded projections from a few years ago. In 2020, for example, the Energy Information Administration projected 580,000 ZEV sales in 2023—a little more than one-third of the actual total last year.

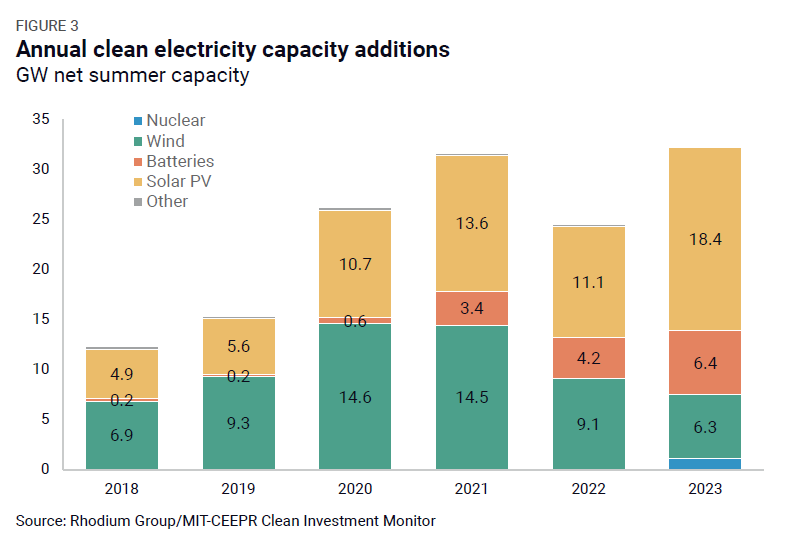

While ZEV sales exceeded post-IRA projections in 2023, utility-scale clean electricity expansion is falling short. There was a record 32.3 GW of zero-carbon electricity generation and storage capacity added to the grid in 2023, up 32% from 2022 and topping the previous high of 31.6 GW in 2021 (Figure 3). The majority of new capacity was solar PV at 18.4 GW, followed by battery storage at 6.4 GW and wind at 6.3 GW.

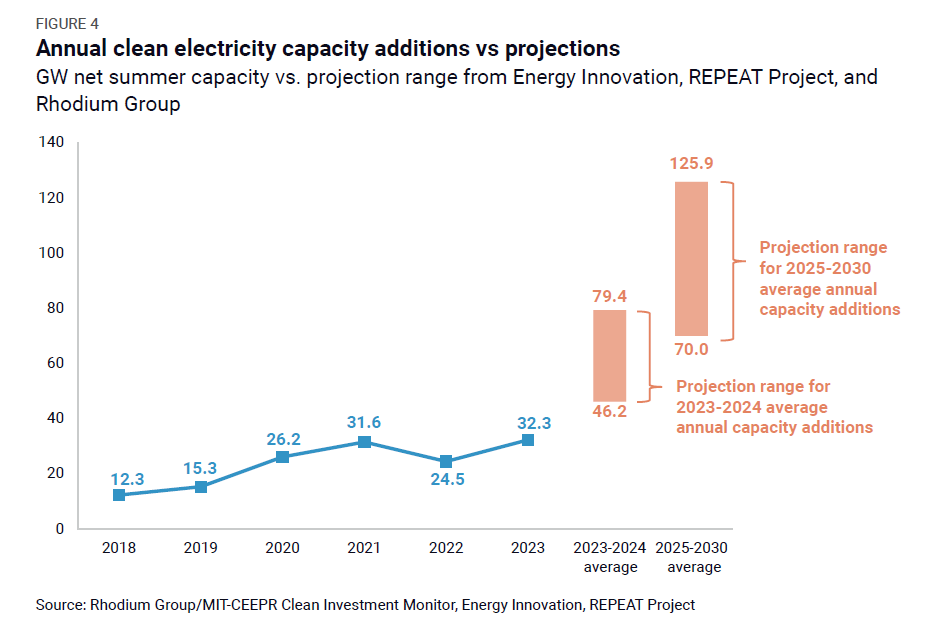

While impressive, this pace of additions is lagging EI, REPEAT and Rhodium projections of electricity system pathways consistent with a 40% reduction in net GHG emissions by 2030 (let alone the US pledge under the Paris Agreement of a 50-52% reduction). Solar is performing largely as expected in the REPEAT and EI projections while falling short of the Rhodium projections. Wind and storage are falling short of the REPEAT and EI projections (and down considerably in absolute terms since 2021) but are broadly in line with the Rhodium projections.

Projected average annual capacity additions in 2023-2024 from these three groups’ post-IRA modeling range from 46 to 79 GW (Figure 4). Given that 2023 capacity additions were only 32.3 GW, that leaves 60 to 127 GW of capacity that needs to be added in 2024 to stay on track with these projections. There is currently 60 GW of capacity under development with a scheduled start date in 2024—just reaching the bottom end of that range. But projected start dates at this time of the year have a tendency to slip, making it likely that the full year 2024 number for capacity additions will end up coming in considerably below 60 GW.

Beyond 2024, the pace of annual capacity additions consistent with modeled pathways to a 40% reduction in net GHG emissions by 2030 only increases. Post-IRA projections from the three organizations included in this survey have average annual capacity additions between 2025 and 2030 ranging from 70 GW to 126 GW.

A year and a half after the passage of the IRA, progress in two key areas of clean energy and transportation deployment—electric vehicles and clean electricity—is mixed. For electric vehicles, sales came in at the top of the range of post-IRA projections last year. ZEV deployment can remain on a track consistent with the IRA’s 40% emissions reduction objective, even if annual sales growth slows in 2024 —provided it stays in the 30-40% range. On the other hand, even though investment in utility-scale clean electricity generation and storage capacity reached record levels in 2023, it is at risk of falling behind post-IRA projections. The IRA has made renewable electricity cost-competitive with coal and natural gas (short-term cost inflation in 2022/2023 and a lag in issuing guidance on some tax credit provisions notwithstanding). The biggest barriers to deployment between now and 2030 are non-cost in nature—like siting and permitting delays, backlogged grid interconnect queues, and supply chain challenges. Tackling these non-cost barriers will be critical for the IRA to achieve its full clean energy deployment and emissions reduction potential.

Tracking public and private investments in climate technologies in the US

Explore the Clean Investment MonitorNote

Investment in clean technologies is continuing at record levels in the US, as demonstrated by new data from the Clean Investment Monitor.

Note

Using the Clean Investment Monitor, we assess how much investment is flowing to disadvantaged, low-income, and energy communities in the US.

Report

The newly launched Clean Investment Monitor provides comprehensive tracking of all public and private investments in decarbonization technologies in the US.