Irrational Expectations: Long-Term Challenges of Diversification Away from China

Firms are actively diversifying investment and sourcing away from China, but it won't necessarily reduce reliance on Chinese inputs and suppliers in the near term.

In the first half of 2023, Mexico overtook China as the main trading partner of the United States—the first time since 2005 that China did not hold the top spot. Some observers seized upon this development as proof that diversification away from China was well underway. Others cautioned against jumping to conclusions, pointing out that Mexican imports continue to rely heavily on Chinese inputs. For the diversification skeptics, global value chains are simply too integrated to untangle and the Biden administration’s de-risking policies are unlikely to succeed.

Which camp is right? There is almost as much data to support the idea that firms are diversifying away from China as there is showing that they are doubling down on the Chinese market. Reaching a verdict is further complicated by the fact that there is no consensus on how to define diversification—a concept that encompasses not only trade and investment but also supply chains and tougher-to-measure concepts like knowledge-sharing. Still, as companies around the world reassess their links to the Chinese market in response to an increasingly challenging business environment in China and rising geopolitical tensions, business leaders need to get a clearer sense of whether diversification is happening and what form it is taking. This note explores these issues using a wide range of available data points. We find that:

- Firms—foreign and Chinese—are actively diversifying investment and sourcing away from China, in sensitive as well as less sensitive sectors. Because channeling new investments to new markets is easier than finding alternative suppliers, particularly for intermediate inputs, the trend is most visible in the FDI realm.

- Because global value chains are so entangled with China, diversification will not necessarily result in a reduced reliance on Chinese inputs and suppliers in the short- to medium-term. A more comprehensive relocation of global supply chains is likely to unfold eventually, especially in sectors like EVs where co-localization is key, but this will happen over an extended period of time.

- Because China’s manufacturing clout is so significant, even substantial shifts in production to alternative destinations may only result in small declines in China’s share of global exports, manufacturing or supply chains. These moves, however, can trigger major economic, industrial, and logistical impacts on new destination countries, given their much smaller sizes.

- These realities mean that it will take years for advanced economies to achieve the objectives behind their “de-risking” policies—namely limiting trade, investment and supply chain exposure to China in a subset of critical areas. This does not mean that the broader diversification objective is misguided. But policymakers will need to adjust their expectations about the timeframe needed to substantially reduce dependencies. If they do not accept that diversification is a complex, long-term challenge, there is a risk that calls for bolder policy measures to reduce dependencies on China grow.

Diversification is well underway

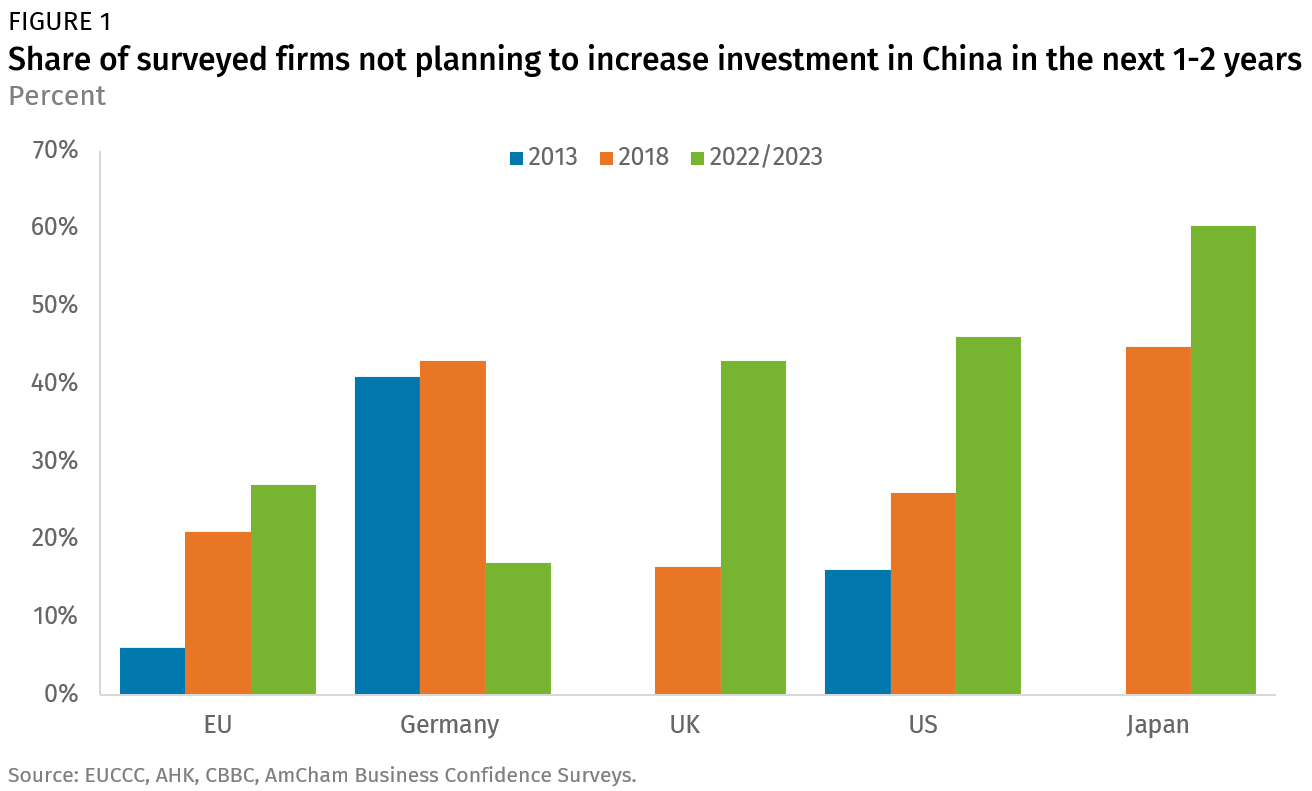

A wealth of anecdotal evidence on investment, trade and supply chain patterns suggests that some degree of diversification from China is already underway. Business association surveys—early indicators of shifting sentiment—show that the appetite for making new investments in China is waning. They suggest that a growing share of EU, UK, US, and Japanese firms do not plan to increase investment in the country over the coming years (with German firms a notable exception, see Figure 1). One in five German and UK firms, and one in ten US firms, now say that they plan to decrease investment in China. And a growing number of firms from advanced economies say they are relocating or intend to move manufacturing or sourcing outside of China, most often to ASEAN (especially Vietnam) and near-shore destinations (Central and Eastern Europe for EU firms, Mexico for US ones).

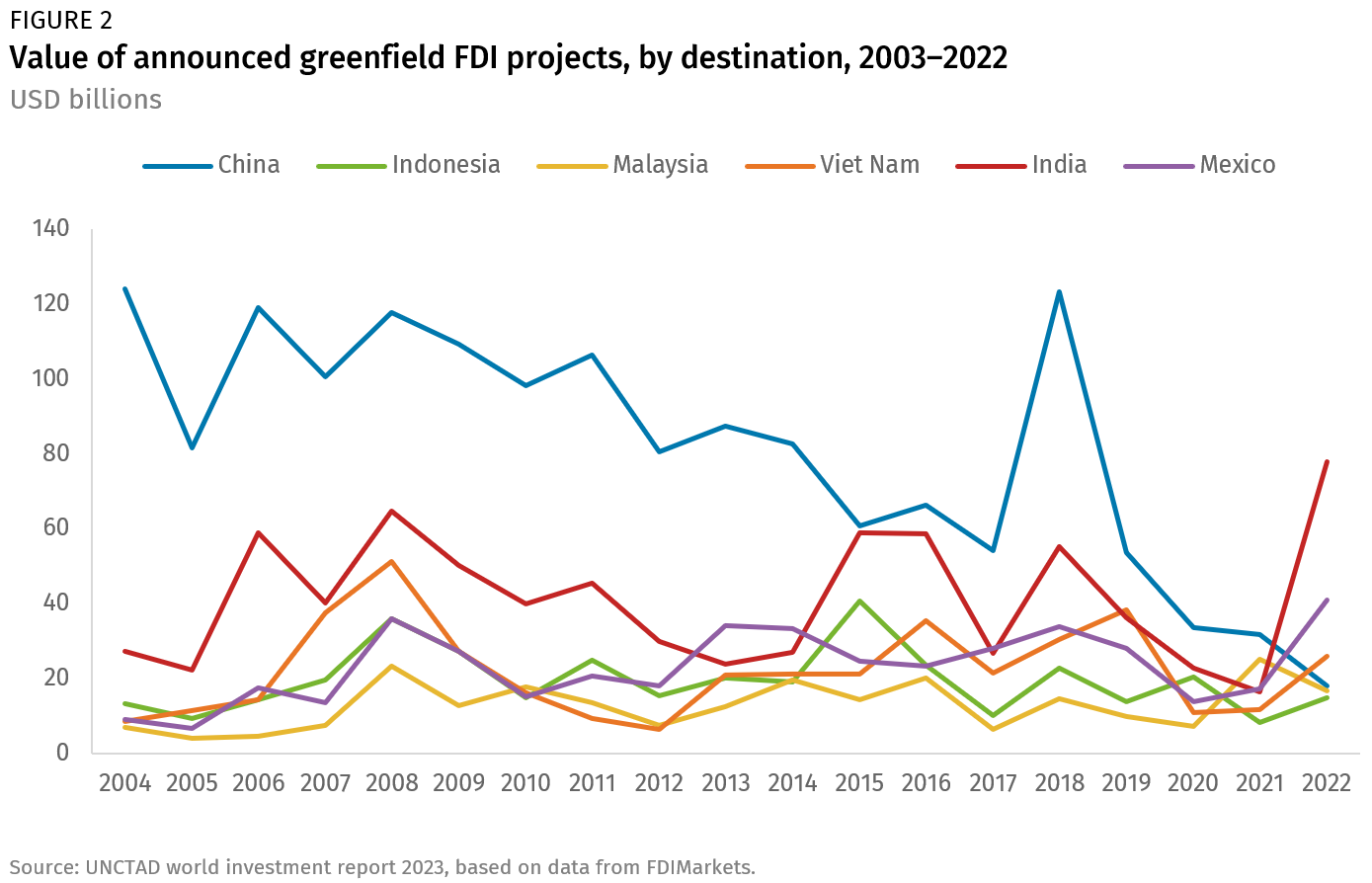

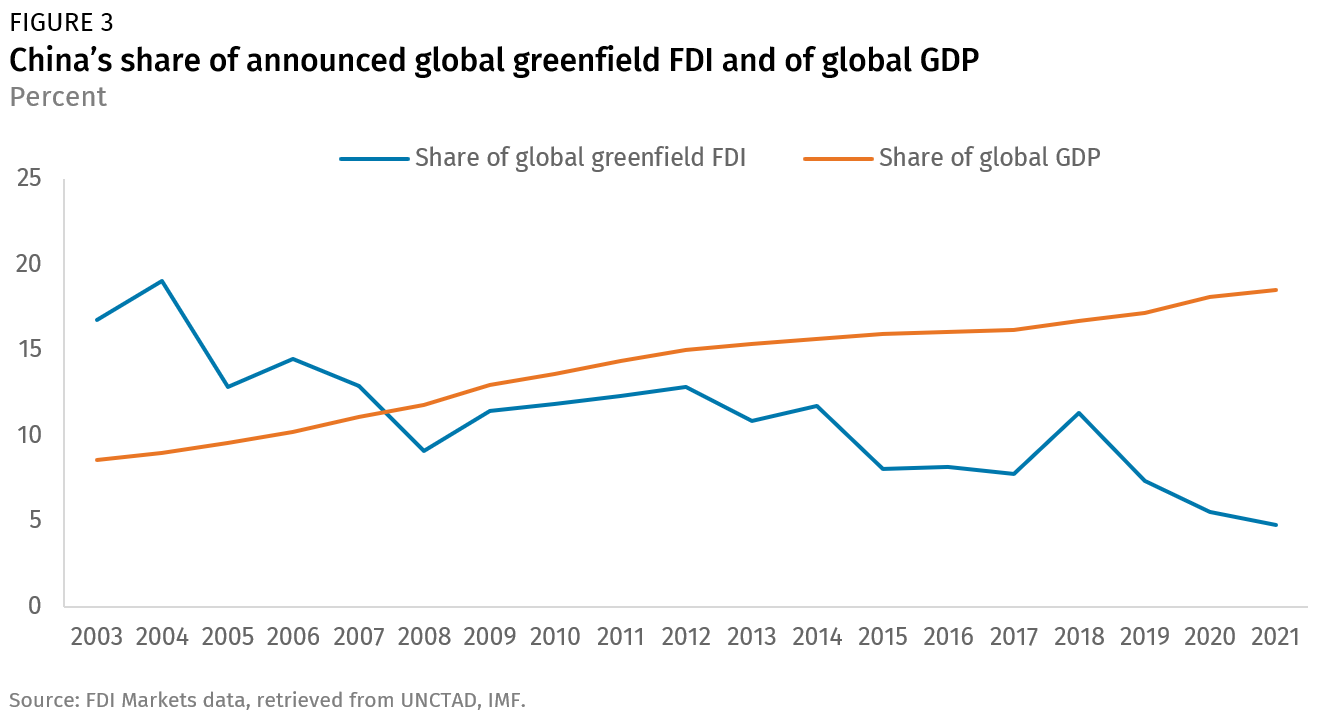

The shift in corporate intentions toward China, evident in recent surveys, can also be seen in investment data. Our tracking of US and EU FDI into China shows that the number of FDI transactions in China by EU and US firms is trending down, and is now roughly half of levels seen a decade ago.1 Annual investment values are well below the levels seen in the early 2010s (see “Big Strides in a Small Yard” August 11, 2023). This compares with robust (and fast-growing in 2022) greenfield FDI to alternative destinations like Vietnam, Malaysia, Mexico, and especially India (Figure 2). These trends have resulted in a decline in China’s share of global greenfield FDI since 2004, a trend that has accelerated over the past five years, with that share declining from 11% in 2018 to just below 5% in 2021. This occurred despite the fact that China’s share of global GDP increased over this period, reaching 19% in 2022 (Figure 3).

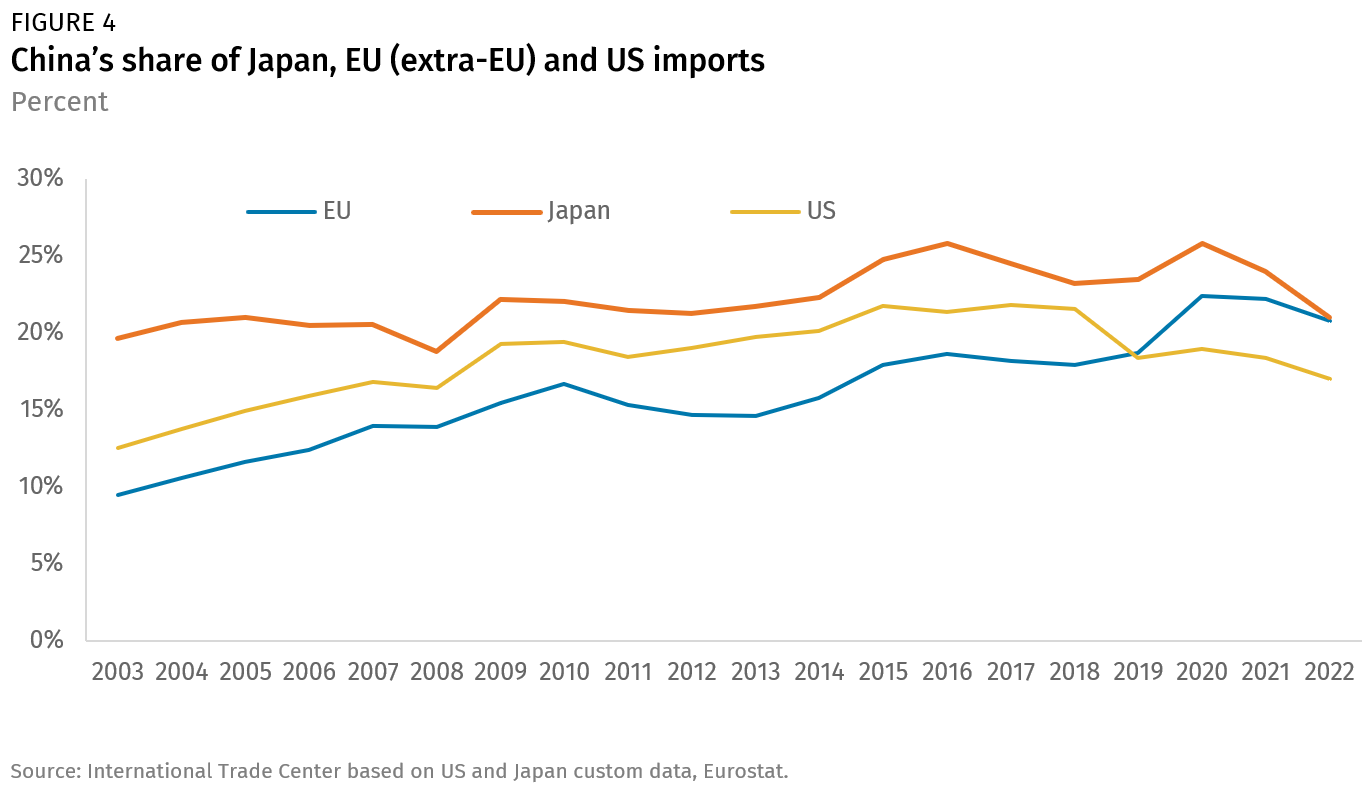

Diversification in firms’ investment decisions alone is not necessarily enough to impact trade patterns, given that a majority of China-world trade today is driven by Chinese rather than foreign firms (72% of China’s exports as of March 2023). This is clear when looking at EU-China trade ties, which have deepened in the past three years, despite EU firms showing waning interest in China investment. But where policies have raised the costs of bilateral trade, MNCs have also started to seek alternative sourcing locations, especially for assembled goods, with a much more visible impact on trade patterns (Figure 4). Such policies have led to a clear diversification trend in US-China trade, with China’s share of US imports declining from 22% in 2018 to about 17% in 2022—much of it linked to reciprocal US-China tariffs imposed under the Trump administration.2 Japan, an early mover in implementing policies to encourage supply chain diversification, has also achieved marked change in its trade relationship with China. Apart from a short rebound during the pandemic, China’s share of Japanese imports dropped from 26% in 2016 to 21% in 2022.

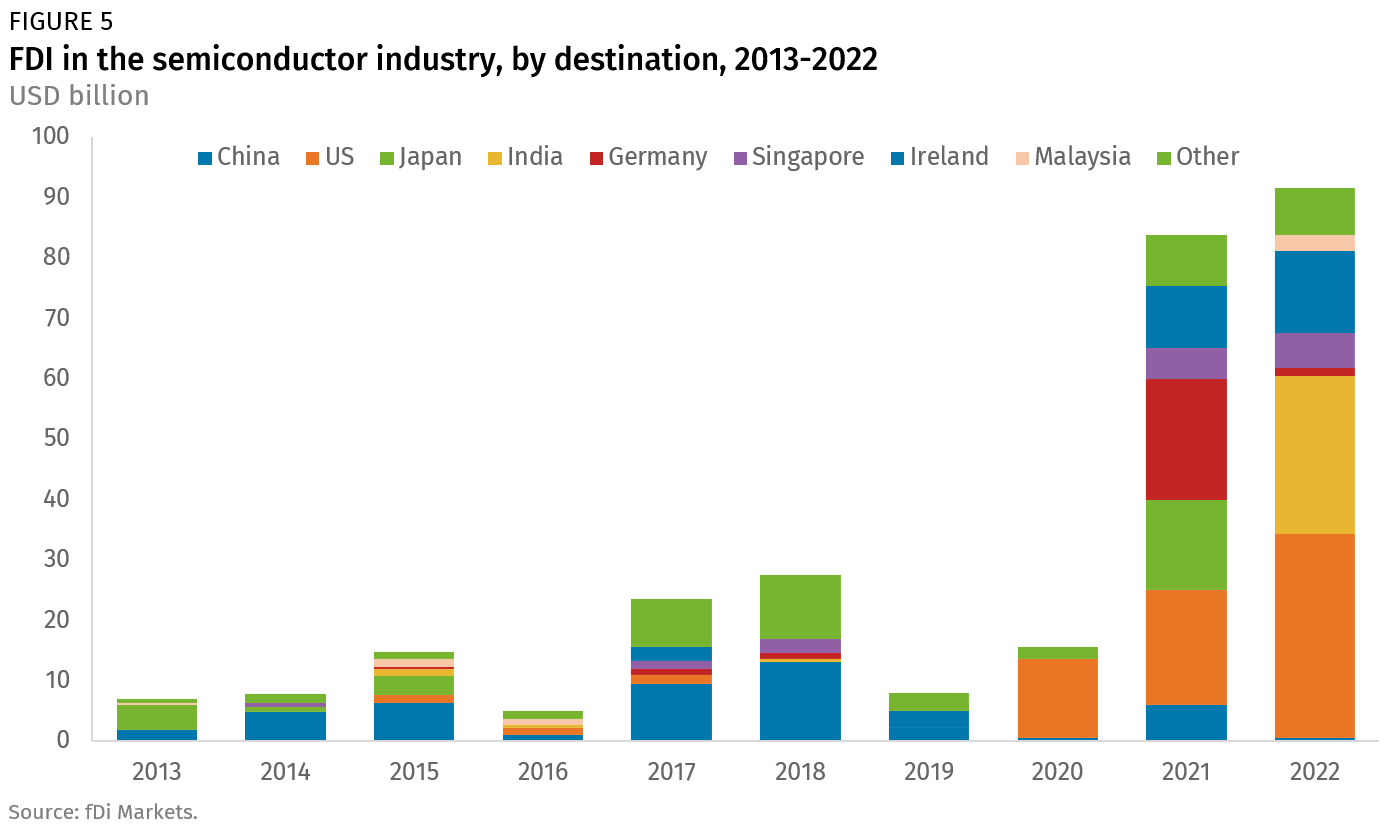

Geopolitical dynamics have played a key role in influencing corporate sentiment toward China in recent years, with tariffs, export controls and other politically motivated restrictions on economic activity raising the costs associated with investment and trade in a range of sectors. Geopolitics has also influenced the debate in corporate boardrooms, raising the hurdles to capital expenditure plans in China and bolstering the attractiveness of alternative locations. Diversification is therefore most evident in geopolitically sensitive sectors. Annual investments in the information communications technology (ICT) sector in China by US firms plummeted from over $4 billion in 2016 to just over $2 billion in 2019, and to a couple hundred million dollars in 2020. As scrutiny of the semiconductor sector grew, chipmakers announced plans for major investments in the US and Europe, as well as alternative locations like India. As a result, China’s share of global inbound FDI in semiconductors plummeted to 1 percent in 2022, from 48 percent in 2018. Meanwhile, the US share rose to 37 percent from zero percent over the same period, and the combined share of India, Singapore, and Malaysia rose to 38 percent from 10 percent (Figure 5). Electric vehicle (EV) and battery investment intentions in the US, finally, have spiked in the wake of the Inflation Reduction Act (IRA), with $52 billion in related FDI announced within the first nine months of the legislation’s publication.

But geopolitics is not the only driver of diversification choices, and behaviors are changing across a much broader set of sectors. A deteriorating business environment has also driven firms in highly restricted sectors, from digital services to energy, to downgrade their expansion plans and refocus resources on other geographies. Rising competitive pressures have had an additional effect, with companies such as Samsung Electronics, LG, and Stellantis exiting the Chinese market amid declining market shares, and announcing large investment projects in India, Vietnam, Mexico, and other destinations. Slowing economic growth and rising production costs in China are increasingly important factors for companies as well, as they reassess their presence in the Chinese market. Rising costs were tolerable when China was delivering GDP growth rates in the high single digits and the business environment was relatively stable. They are harder to ignore when growth is in the low single digits and the market is highly politicized. All in all, these data points paint a picture of global MNCs actively diversifying away from China, due to a combination of geopolitical and commercial considerations.

A slow and China-linked diversification

Then why is there such an intense debate about whether or not diversification is happening? The reason is that, while individual companies are reassessing their approach to China, the country remains a vital hub for global manufacturing value chains. Diversification, especially of sourcing activities, will unfold gradually. Barring an acute geopolitical crisis, a clear decline in China exposure will take years. It would not be surprising to see China’s overall share of global exports, manufacturing and supply chains continue to rise, even as diversification away from China accelerates.

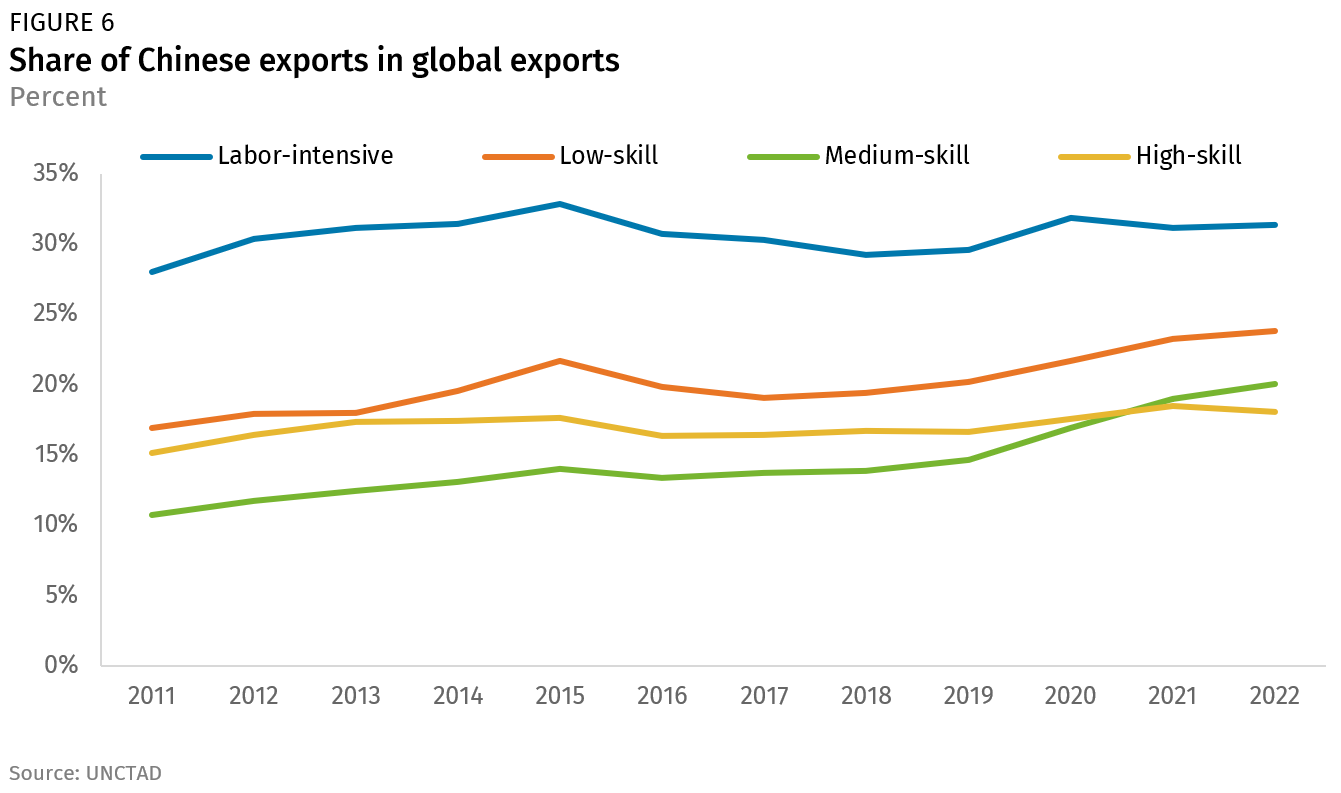

The evolution of labor-intensive industries, early movers out of China, illustrates this counterintuitive dynamic. Diversification has been taking place for years in these industries, but it has been obscured by a concomitant expansion of manufacturing value chains in China. Textiles, for example, were an important driver of Chinese export growth for years. Over the past decade, however, the share of Chinese textiles in US and Japanese imports has fallen sharply (by 15 and 20 percentage points respectively), replaced by alternative countries of origin like Vietnam or Bangladesh. At the same time, FDI in China’s textile sector has also fallen rapidly, from $1.2 billion in 2012 to less than half a billion in 2019, according to MOFCOM data. Yet these shifts are barely visible in the aggregate, with China’s share of global labor-intensive manufacturing exports holding steady at around 30% (Figure 6).

This can be explained by China’s size and manufacturing clout. Today, the country represents 31% of global manufacturing value-added. As a result, even seemingly significant FDI flows to Vietnam and Bangladesh end up shifting only small fractions of China’s output and export capacity offshore. Vietnam’s population, after all, is only about 7% of China’s, and its manufacturing sector is a mere 2%. In addition, while the shift in textiles has been clear-cut, countless other labor-intensive sectors, from toys to light consumer electronics, have remained in China thanks to its infrastructure, logistics, and scale advantages, a relatively stable business environment, low outbound shipping costs, and low-cost inland provinces, where foreign investment more than tripled between 2012 and 2021. Finally, much of the decline in foreign investment in China was compensated for by Chinese firms growing manufacturing capacity and market share.

This counterintuitive dynamic is likely to play out in other sectors as well. Firms in the electronics, ICT, autos, or machinery sectors—both foreign and Chinese—may have started the process of diversifying away from China, but it will take years for this trend to be clearly visible in aggregate data and produce a clear decrease in micro- and macro-level exposure to China.

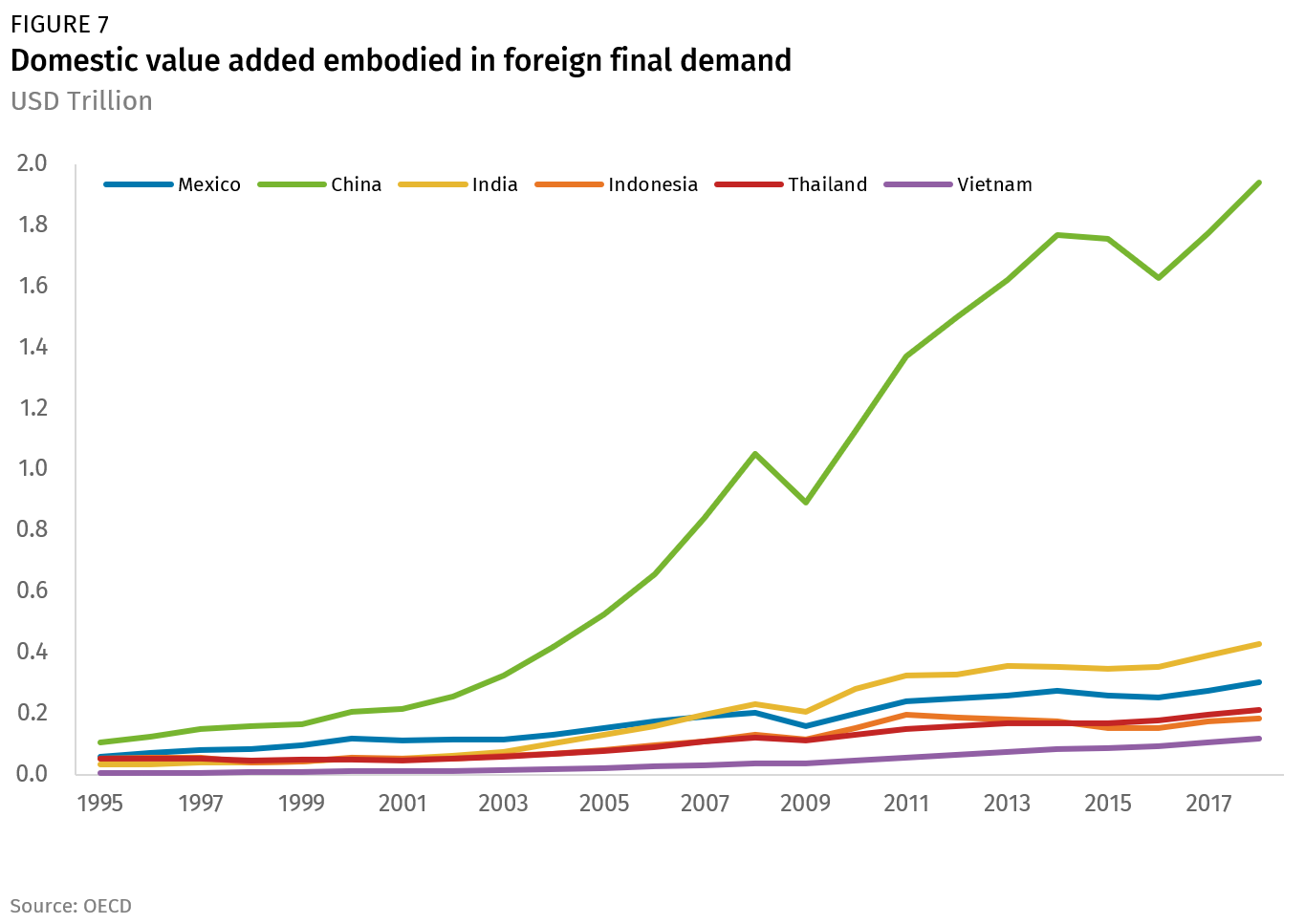

A second reason why diversification is unlikely to result in a rapid decline in exposure to China is that increased investments in, or trade with, alternative countries are often accompanied by a deepening of economic ties between these destinations and China. Over the past 20 years, China has onshored not just final assembly capacity, but also the deep value chains attached to them (Figure 7). Replicating these outside of China, or finding alternative supply sources, takes time, comes at a high cost, and is hindered by a lack of alternatives. Those MNCs that have sought to reduce their China presence or rebalance their global footprint have therefore done so in a piecemeal manner, shifting out single supply chain segments—often final assembly—to alternative destinations, while diversifying suppliers for a subset of the most critical inputs.

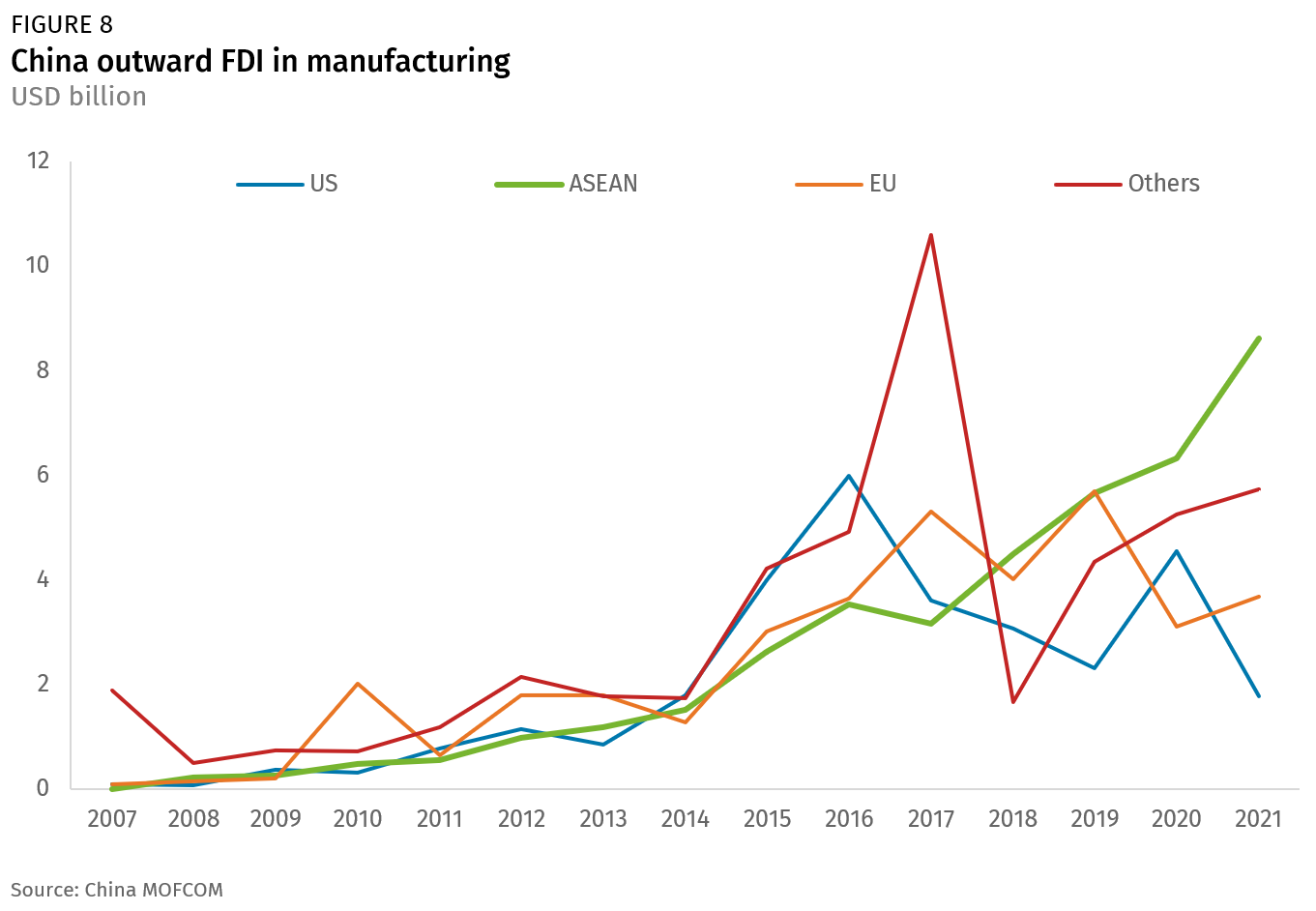

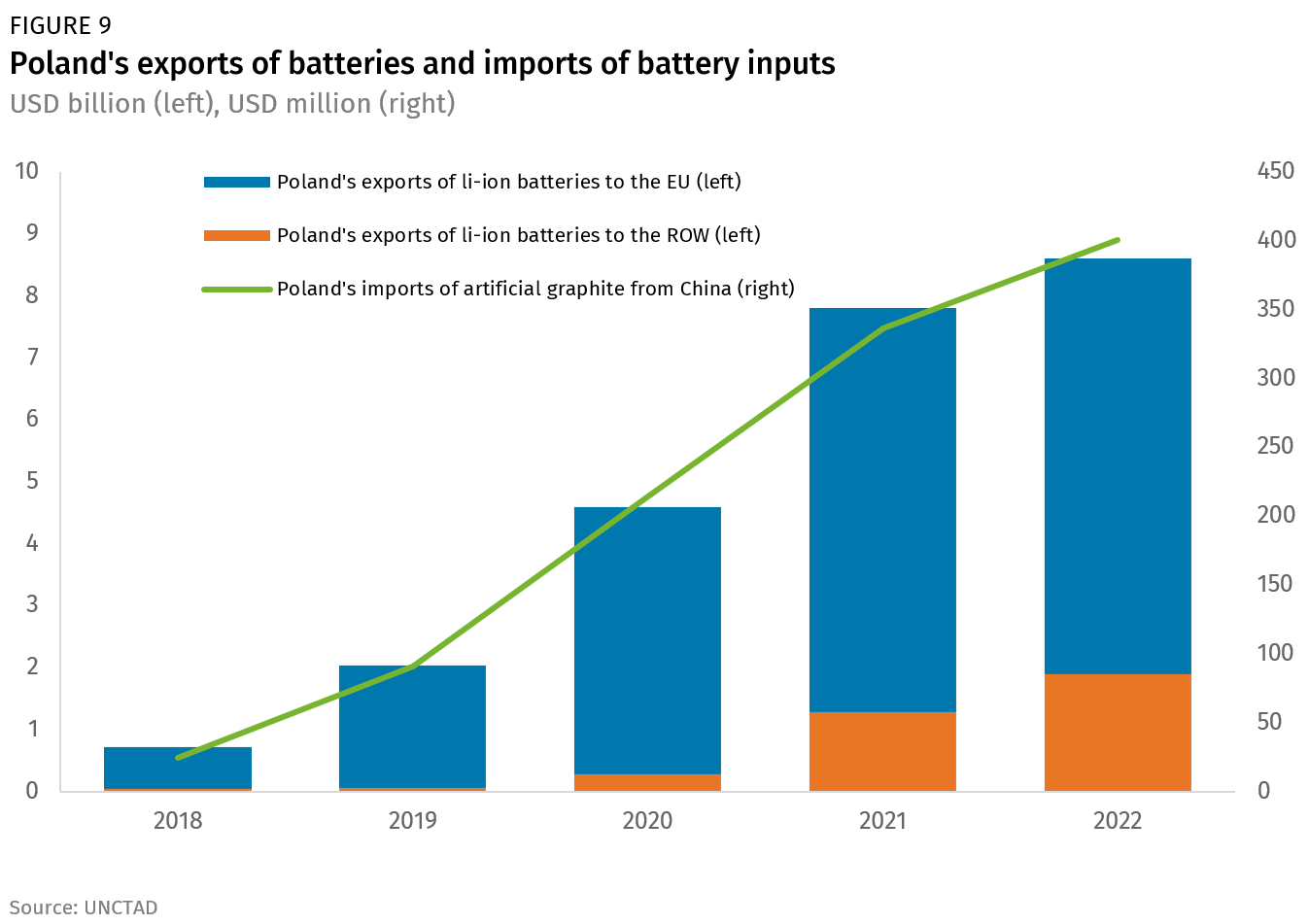

As such, diversification away from China does not always result in a meaningful reduction in firms’ reliance on China or Chinese firms—especially in the short-term. There are numerous examples of MNCs following Chinese suppliers to other markets or encouraging them to relocate outside of China. Many continue to source from China suppliers with whom they have developed close, long-term relationships even as they set up new plants in ASEAN or Mexico. In fact, Chinese outbound manufacturing patterns indicate that Chinese firms have been at the forefront of the global diversification wave (Figure 8). No wonder then that rising US imports from Mexico and Vietnam over the past 5-7 years were matched extremely closely by an increase in Chinese exports to these markets. This stickiness in relation to Chinese inputs is also visible at the sectoral level, where the relocation of electronics value chains to India or the transfer of electric vehicle (EV) production to Poland have been accompanied by a surge in China-sourced inputs (Figure 9).

This does not mean that diversification is not happening. However, it does mean that some of the objectives behind “de-risking” policies in advanced economies are unlikely to be met for many years. China’s centrality in global manufacturing supply chains, and unmatched capacity in critical sectors like electronics, EV or solar, means diversification will remain China-linked for years to come. Manufacturers will need to rebuild their local supplier networks over time—relying on relocated Chinese firms in many cases—and countries will need to rebuild local capacities and skills if they want to absorb manufacturing activity. This takes time, and significant investment.

Diversification, continued

Given these patterns, what should we expect in the future? We have developed five main hypotheses about the outlook for diversification away from China:

First, because diversification is driven by a wide range of factors which are likely to endure, from rising geopolitical competition to a deteriorating economic and policy environment in China, MNCs will continue to look for alternative manufacturing bases and supply sources for their most critical products and inputs. This does not mean that diversification cannot be accelerated or arrested by shifts in policy or by major geopolitical events, but we expect it to continue, and most likely deepen, over a period of years, if not decades.

Second, diversification will be characterized by greater investment by global MNCs in Asia, with Vietnam and India topping the list, and Thailand, Bangladesh, and Malaysia playing a role for specific sectors like EVs, textiles, or chips, in which these countries (respectively) already benefit from adequate skills and manufacturing capacity. Mexico will attract significant additional US MNC investment and sourcing interest across a broad range of sectors, as will Central and Eastern Europe (especially Poland and Hungary) from European MNCs. Chinese firms will deploy in ASEAN (rather than India), but also opportunistically to European, North African or North American destinations, as they seek to serve the EU and US markets. Even if slow and partial, these movements out of China will trigger significant economic, industrial, and logistical impacts on these countries, given their much smaller sizes.

Third, diversification will happen much faster in sensitive sectors (semiconductors, EVs, ICT but also healthcare industries and green technologies). In less sensitive sectors that require skills and advanced equipment, the persistent attractiveness of China as a manufacturing hub will remain a drag on diversification efforts. Across sectors, we expect stronger diversification impulses in cost-sensitive manufacturing—especially for final assembly activities—and in sectors where shipping costs per unit are lower and manufacturing capacity and skills exist outside of China.

Fourth, China’s role in global value chains, and therefore in “diversified” trade and investment, will endure. China’s share of global manufacturing value-added and exports could remain at a high level or even grow further in the years ahead (once COVID effects on China’s export levels wane in 2023). Yet we also expect a slow but gradual onshoring of value chain segments in alternative other countries, motivated by economic benefits from agglomeration. All else equal, agglomeration should happen faster in sectors like electric vehicles or solar panels, where co-location of supply chains is a key element of competitiveness, than in electronics, where value chains have been global for decades. All this could happen while Chinese companies continue to increase global market shares, as these firms pick up manufacturing and export activities vacated by MNCs in China, gain competitive footing in higher value-added sectors and manufacturing segments in China, and gain ground in alternative destinations.

Fifth, the slow pace of diversification could trigger calls in the US (and possibly other G7 countries) for a more aggressive approach to de-risking. Policymakers will need to adjust their expectations about what diversification can achieve in a short period of time. There is a risk, if they do not view this as a long-term challenge, that demands for bolder policy measures (in the form of both incentives and barriers to trade and investment) grow in the years ahead.

1. Our databasing of EU and US FDI into China only covers transactions over USD 1 million and would therefore not capture a rise in smaller transactions, should it have happened over the same period. We doubt however that this is the case given smaller firms are the ones that have most reduced their FDI into China in recent years.

2. On average, US imports of goods affected by tariffs are about 20% below pre-trade war levels, according to PIIE research. Note that the real drop might be slightly milder, however, as China-based exporters sought workarounds in response to US-China tariffs—breaking down orders into smaller parcels that are not covered by tariffs, or shipping goods through third countries. But there is no question that the US has been progressively diversifying its trade over the past five years, at the expense of China.