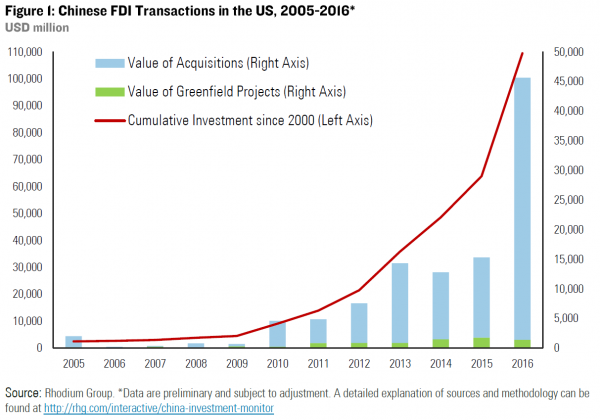

Record Deal Making in 2016 Pushes Cumulative Chinese FDI in the US above $100 billion

The United States became the largest recipient of booming Chinese outbound FDI in 2016, with $45.6 billion worth of completed acquisitions and greenfield investments. Cumulative Chinese direct investment in the US economy since 2000 now exceeds $100 billion. This update reviews Chinese investment patterns in the US in the past 12 months and provides an outlook for 2017. Rhodium Group’s interactive China Investment Monitor was also updated with full year 2016 data.

Chinese FDI in the US Tripled in 2016 to $46 billion

Chinese companies invested a record $45.6 billion in the US economy in 2016. This is triple the amount we recorded for 2015 and a tenfold increase of annual investment just five years ago. Acquisitions account for the majority of total investment ($44 billion). Chinese companies also continued to expand organically through greenfield projects but their scale remained small compared to acquisitions. The record level of investment in 2016 pushed cumulative Chinese FDI in the US economy since 2000 to $109 billion.

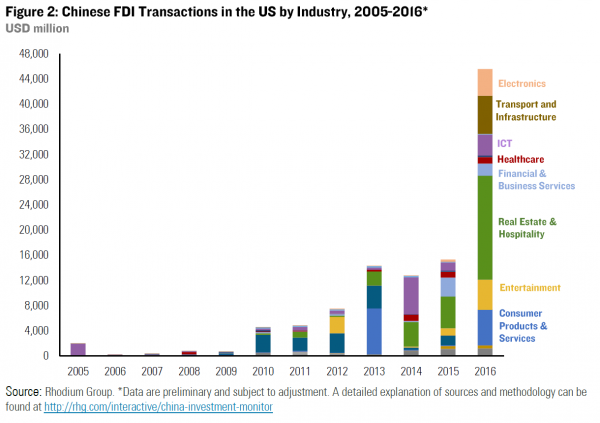

Corporate China’s US Portfolio is Broadening

The mix of industries targeted by Chinese investors also expanded remarkably in 2016. In contrast to the dominance of fossil fuel investments before 2013, more than 90% of Chinese FDI in 2016 was targeting US services and advanced manufacturing sectors. Real estate and hospitality (Strategic Hotels, Carlson Hotels and numerous commercial real estate investments in New York, California and Hawaii), information and communications technology (Omnivision), entertainment (Legendary Entertainment), and financial services (AssetMark) continued to attract the interest of Chinese investors. Sectors that saw a big increase of Chinese interest from previous years include logistics (Ingram Micro), consumer products (GE Appliances) and electronics (Lexmark).

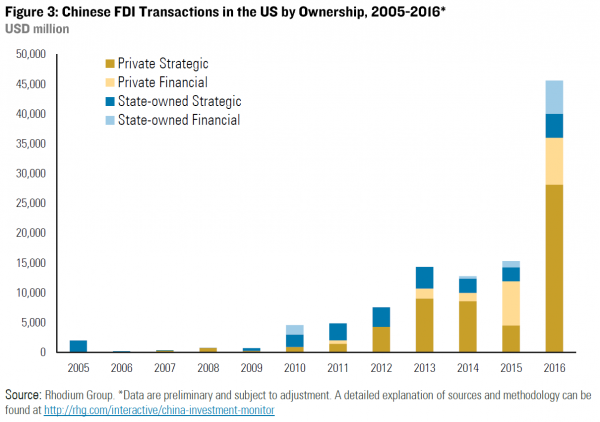

China’s Private Sector Continues to Dominate US Expansion

In line with previous years, private sector companies continued to drive the growth of Chinese FDI in the US. Privately owned companies accounted for 79% of total investment in 2016, about the same level as in 2015. One important deviation from 2015 patterns is the smaller share of financial investments in total FDI. Transactions primarily motivated by financial returns accounted for more than half of total investment value last year, but their share dropped to 30% in 2016. Strategic investments (FDI in the traditional sense of real economy firms investing in their principal areas of business) were back in the driver’s seat this year.

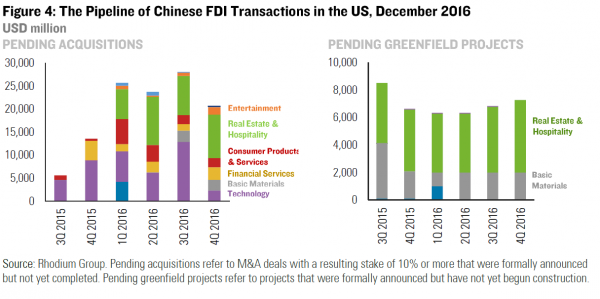

Outlook: Rich Pipeline But Political Uncertainty

Economic fundamentals suggest further expansion of Chinese FDI in the US in coming years: The Chinese economy is slowing and companies are keen to diversify; pressure on Chinese companies to upgrade technology and build out brands and local consumer presence is only increasing; the US growth outlook is brighter than in Europe and other advanced economies; and anticipation of further US dollar appreciation against the Chinese Yuan further increases the rationale for adding US assets.

The pipeline of Chinese deals reflects those realities: Chinese companies are currently waiting to finalize regulatory approvals or financing for $21 billion worth of US acquisitions. They have also committed to more than $7 billion of capital expenditures related to announced greenfield projects that have not yet started construction.

While the economic fundamentals and the deal pipeline suggest that 2017 will be another boom year for Chinese investment in the US, the political realities on both sides pose a major downside risk to both pending transactions and new deal flow in coming months.

China is wrestling with another period of heavy capital outflows and resulting downward pressure on the Chinese currency. Net outflows under the non-reserve financial account totaled $379 billion in the first three quarters of 2016 (and real outflows were significantly higher if one accounts for hidden interventions by China’s central bank), and the recent change in US monetary policy will put additional pressure on China’s balance of payments. While Beijing continues to pledge its support for legitimate outbound FDI, it has recently tightened administrative controls on certain types of transactions, singling out some of the biggest sectors receiving Chinese capital in the US (such as real estate and entertainment). Those changes and uncertainty about implementation of new rules could impact pending transactions as well as the pace of newly announced investments in coming months.

Chinese investors also face greater uncertainty and political deal risk in the United States in the aftermath of the Presidential election. Recent appointments by President-elect Trump suggest a more confrontational approach to trade and investment policy toward China. One important question for Chinese deal making is how foreign investment reviews under the Committee on Foreign Investment in the US (CFIUS) will change under the incoming administration. Another medium-term risk for Chinese investors is growing Congressional wariness of potential security and economic risks related to Chinese investment. In addition to a surge in letters opposing individual Chinese acquisitions in 2016, there seem to be serious efforts underway on Capitol Hill to prepare legislation that would expand the mandates of CFIUS to review Chinese and other foreign transactions.