The Chosen Few: A Fresh Look at European FDI in China

European direct investment in China is increasingly dominated by a handful of large companies, many of them German.

After decades in which China felt like a one way bet for European firms, market conditions have become far more challenging due to restrictive COVID-19 policies, slowing economic growth and rising geopolitical tensions. Against this increasingly uncertain backdrop, we have taken a close look at European (EU+UK) FDI in China to assess the current state of investment on the ground, and shed light on how it has evolved over the past decade. Our key finding is that European investment has grown much more concentrated, both in terms of the companies that are investing there, the countries they come from, and the sectors in which they operate. While a handful of large firms, many of them German, continue to pour money into their China operations, many other firms with a presence in China are withholding new investment. At the same time, virtually no new European firms have chosen to enter the Chinese market in recent years. And acquisitions of Chinese firms have stalled, with greenfield investments increasingly dominating the FDI landscape.

Our findings point to a widening gap in how European firms perceive the balance of risks and opportunities in the Chinese market. They also suggest that a more nuanced perspective on the issue of European corporate dependencies is needed. From a direct investment point of view, it is wrong to talk about a broad-based dependence of European, or even German, companies on the Chinese market. As policymakers in Berlin and other European capitals consider measures to reduce economic dependence on China, they would be wise to take the growing concentration of corporate risks into account.

The Chosen Few

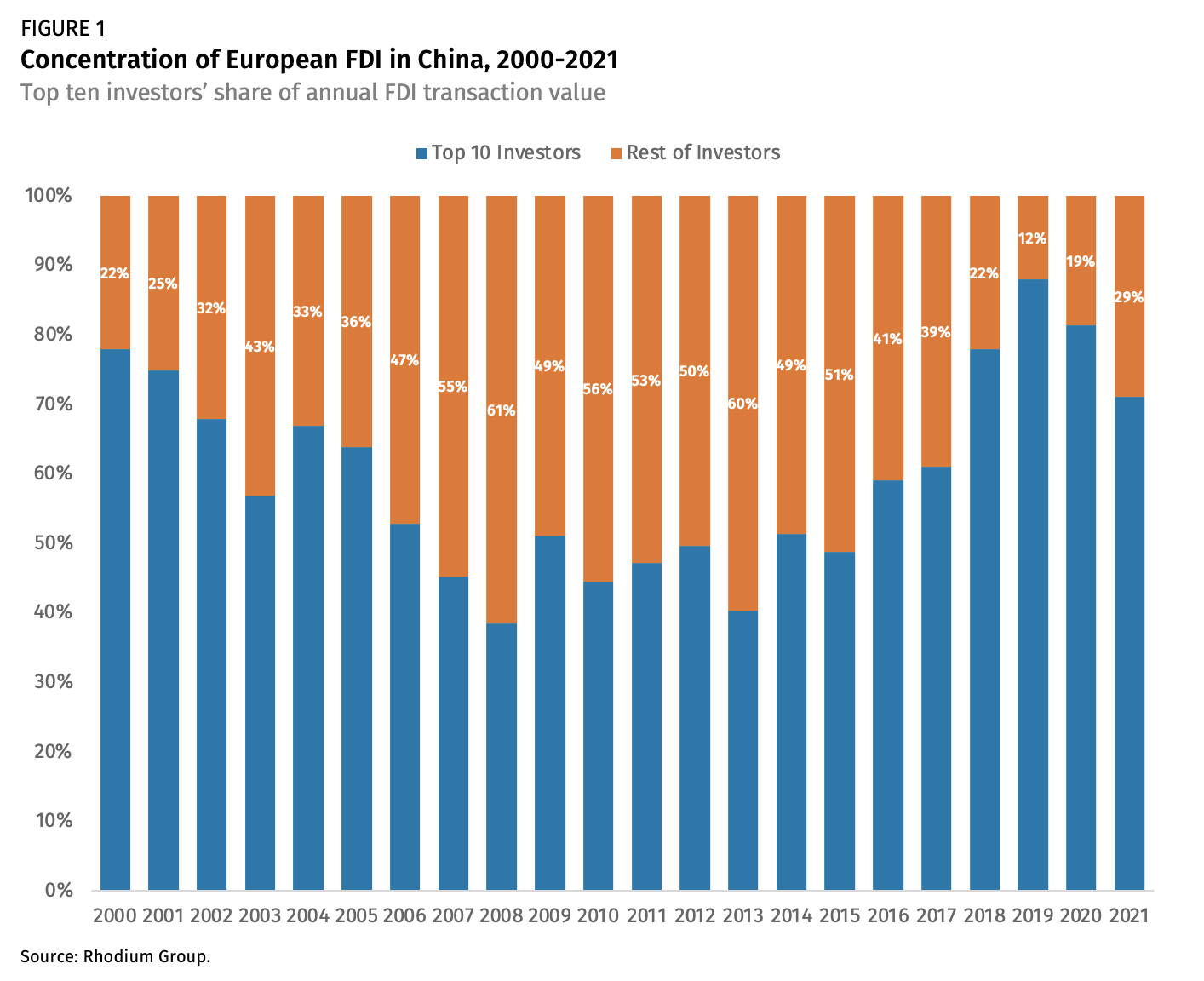

Our review of core trends in European FDI to China over the past decade has yielded one especially striking finding: today, the overwhelming majority of European investment in the country comes from just a handful of companies. We find, for example, that the top 10 European investors in China in each of the past four years made up nearly 80%, on average, of total European direct investment in the country. In 2019, the trend toward greater concentration was especially marked, with the top 10 investors representing 88% of all European FDI (see Figure 1). In comparison, over the previous decade (2008-2017), the top 10 European investors in China made up just 49%, on average, of the total European investment value.

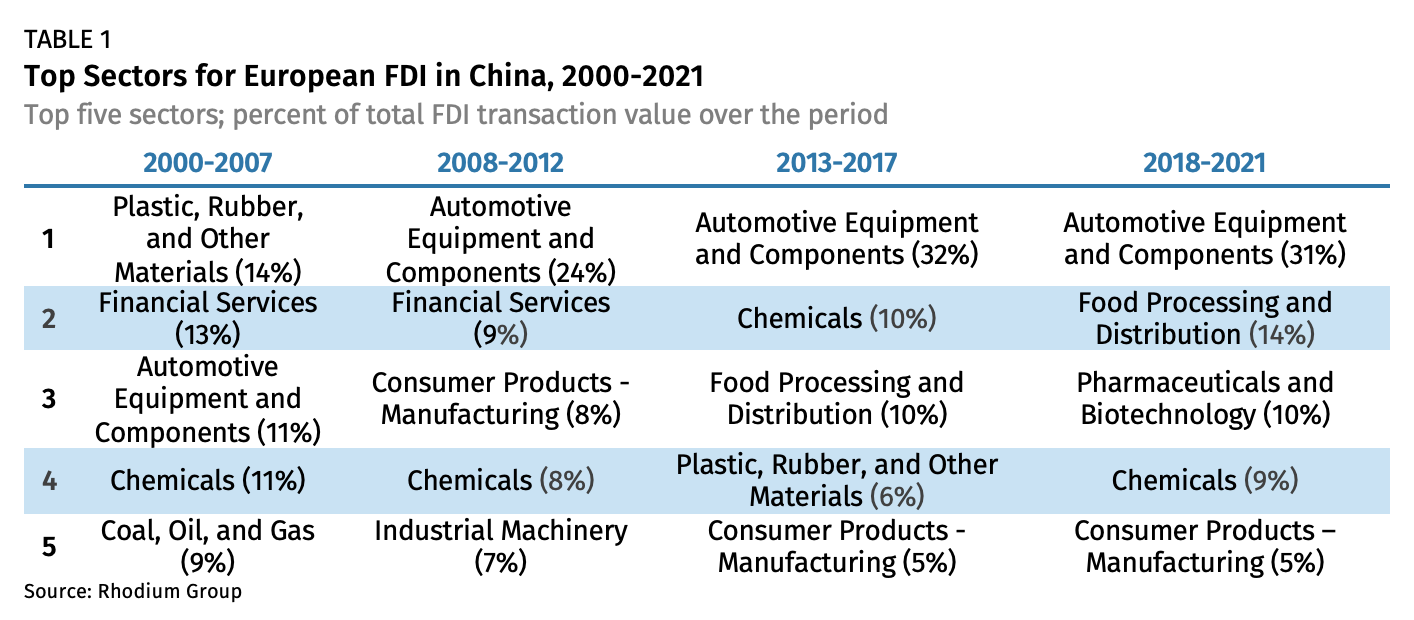

European investment has also become more concentrated in terms of sectors. Five sectors—autos, food processing, pharma/biotech, chemicals and consumer products manufacturing—now make up nearly 70% of all FDI, compared to 57% in 2008-2012 and 65% in 2013-2017 (see Table 1). Among them, the auto sector stands out. It now consistently represents about a third of all European direct investment in China. This proportion was even higher in H1 2022 as German carmaker BMW increased its stake in its China JV from 50% to 75% and other European automakers poured money into new facilities to build electric vehicles.

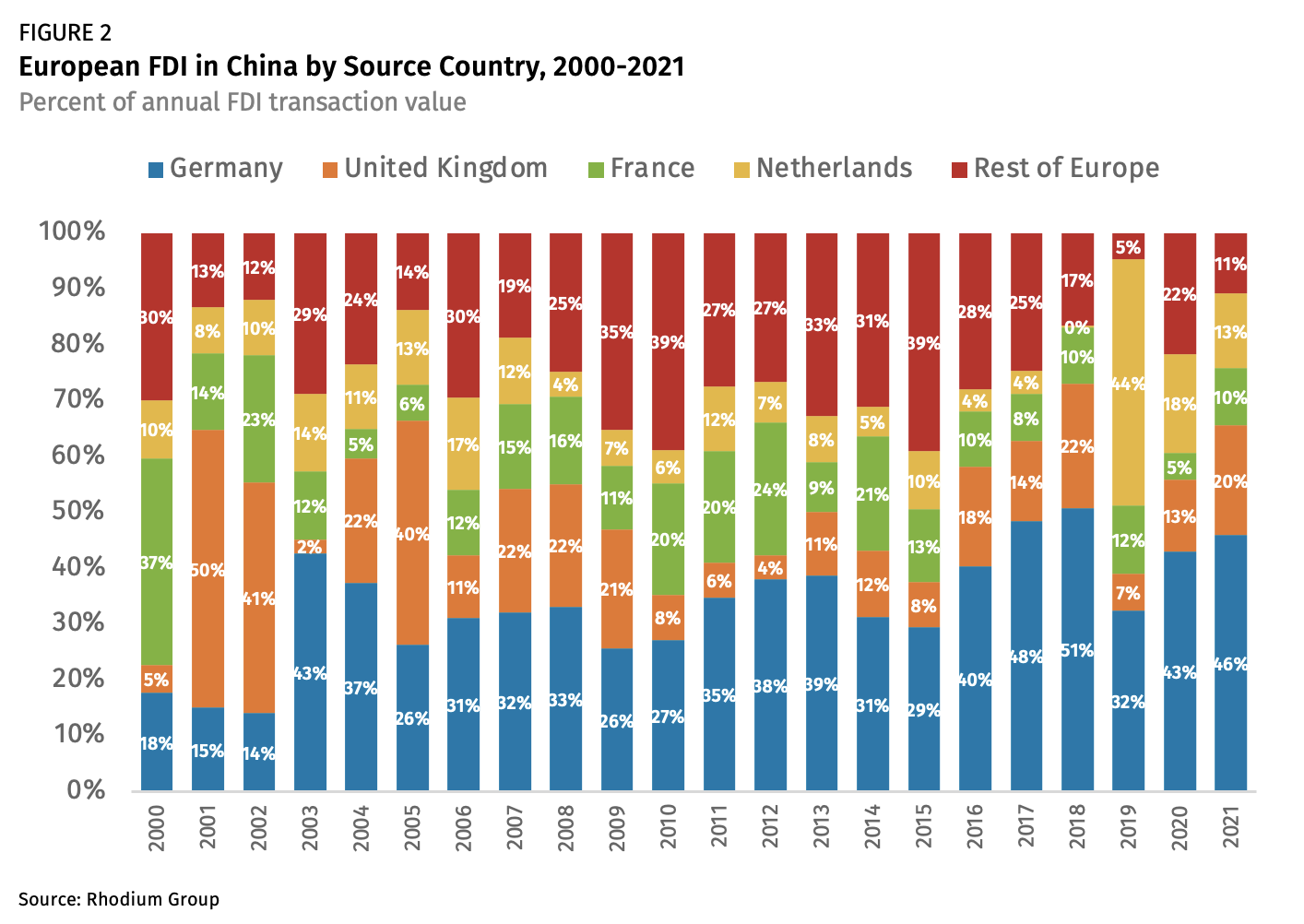

Finally, European FDI in China has become more concentrated in terms of countries of origin. Four countries—Germany, the Netherlands, the UK and France—made up 87% of the total investment value, on average, over the past four years, compared to 69% in the previous ten years (see Figure 2). Among them, Germany stands out as the top investor by far, making up 43% of the total, on average, over the past four years, compared to 34% in the previous 10 years. In 2018, German firms accounted for more than half of all European investment in China. This trend is driven by a number of factors: German companies were early entrants to the Chinese market and their presence there was actively encouraged and aided over decades by the country’s political establishment; they are typically in capital-intensive manufacturing and engineering industries, meaning large fixed investments; and they are present in sectors that have seen strong growth in China over the past decade.

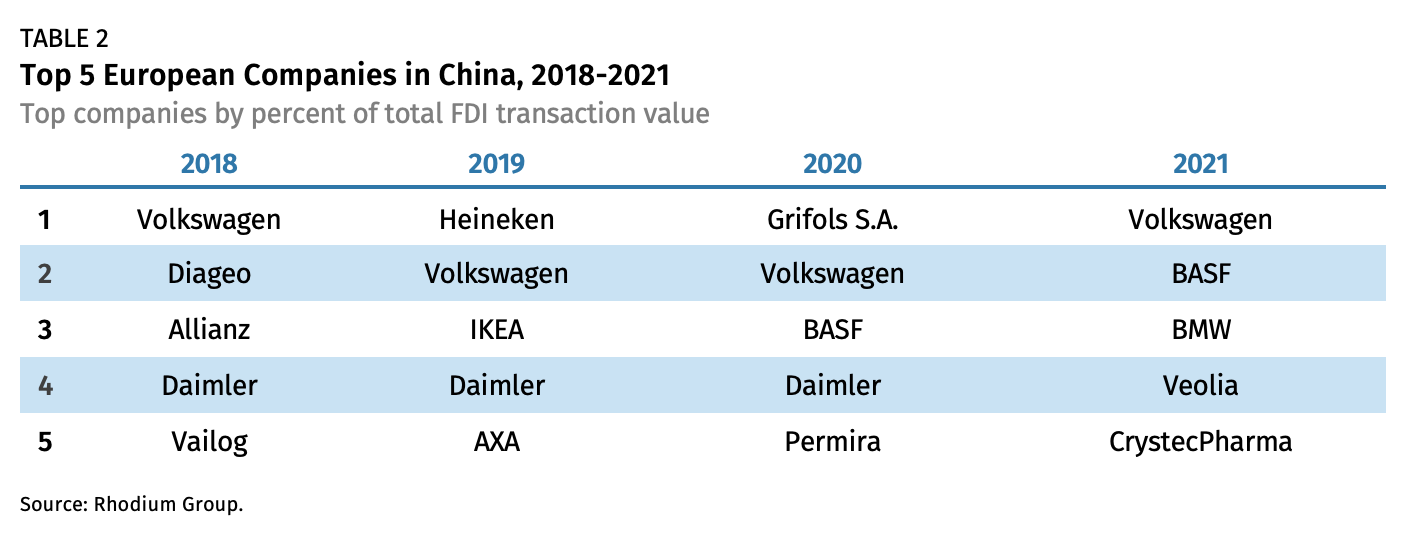

Among German firms, the three big automakers (Volkswagen, BMW and Daimler[1]) and chemicals group BASF have led the way in China. These four firms alone contributed 34% of all European FDI into China by value from 2018 to 2021.

The biggest European investors in China have maintained steady investment flowing into large greenfield projects due to three main considerations: First, they have generated significant profits in China and believe the market will continue to be lucrative despite the economic and geopolitical headwinds. Second, these companies feel they must continue to invest and develop products in China in order to safeguard the value of past investments and remain competitive with increasingly innovative domestic rivals, for example in sectors like electric vehicles. Third, they are trying to insulate their China operations from rising global risks through greater localization—an approach that is also being actively encouraged by Chinese authorities. In this respect, recent FDI in China looks quite different than it did a decade ago. It has become more defensive, in a reflection of a more risky environment, in China and globally.

The Others

The concentration around a few major German players is notable, but it does not mean that companies from other European countries are showing no interest in the Chinese market. Firms from France, the UK and the Netherlands consistently rank among the top ten investors as well, with non-trivial FDI in the automotive, chemicals, pharmaceutical, insurance and consumer goods sectors. Among them, Ikea, Diageo or AXA stand out as companies that have continued to make new, sizeable investments in China.

A closer look at transaction count, rather than investment value, points to continued engagement from firms in other European countries as well—including Italy, Sweden, Finland, Belgium, Denmark, Spain, and Austria. Together, these countries’ firms made up a stable 20-30% of all FDI transactions in China over the past decade. Still, the profile of these companies is slightly different from that of the “chosen few”. Generally speaking, their investments are more sporadic, and although they are typically active in the same industries, they tend to specialize in more specific niches like automotive components or green energy supply chains. Smaller firms, particularly from Germany, Sweden, and Finland, are also prominent in lower capex industries like industrial machinery and equipment, which represented 11% of deals but just 3% of transaction value between 2018 and 2021.

Because our database of EU FDI in China only includes transactions over EUR 1 million, we may not be capturing some smaller scale investments in services, less capital-intensive industries, or R&D activities. Additionally, in focusing on FDI, we are not accounting for other forms of economic engagement with (and dependence on) China. French and Italian luxury brands, for example, rely heavily on trade with China but are not deploying the vast amounts of capital that we see in the above-mentioned industrial sectors.

The Missing

Finally, our analysis reveals another noteworthy category of European investors—those that are missing from the picture. Given the size and growth of the Chinese economy in recent decades, one would have expected the country to attract a much broader range of foreign firms. But three types of investors are conspicuously absent in our review of recent trends.

First among them are investors in the services sector. Our data shows that between 2018 and 2021, business services made up less than 2% of the value and just 7% of the total deal count, while software & IT services made up 0.5% of the value and 3% of the deal count. This is despite the fact that, as of 2020, services made up 53% of China’s GDP (compared to 65% in the EU and 72% in the UK)[2] and despite the strong competitive advantage that European firms enjoy in those industries. Explanations for this include continued market access problems and the belated opening of the Chinese market to European players.

Second, we are seeing far fewer European companies looking to acquire Chinese firms. Greenfield investment makes up the lion’s share of European investment in China, representing two-thirds of the total over the past five years. Its share of total investment has been steadily increasing since 2019. By contrast, the value of European acquisitions in China hit a four-year low in 2021. As an economy matures, one would expect acquisitions to become a more common investment channel. That hasn’t happened in China, as European firms remain wary of buying Chinese companies given formal restrictions, high valuations and a lack of transparency around financial accounts and other liabilities. COVID-19 travel restrictions have amplified the M&A downtrend.

Third, China is seeing fewer and fewer new entrants on its market. Since the outbreak of the pandemic in early 2020, for example, stakeholders on the ground say that virtually no European investors that were not already present in the country have made direct investments. It’s true that many globally-minded European companies are already in China, and have been for some time. Still, one would expect new European players to be showing interest given the size and growth potential of China’s economy. This may be a temporary phenomenon, related to the pandemic and China’s zero-COVID response. However, conversations with stakeholders suggest that a longer-term dynamic may be at work, with smaller European companies reluctant to accept the growing risks of investing in China.

The absence of new players has contributed to the greater concentration of European FDI around a few big players. Incumbents have a distinct advantage in an increasingly politicized market where foreign firms face high barriers to access, an uneven competitive playing field vis à vis local players, and a less-than-transparent compliance landscape. This explains why fewer small and medium-sized enterprises (SMEs) are venturing into the country, and why in sectors like financial services, which have been opened to foreign investment in recent years, only a handful of big European players have made the leap, despite the growth opportunities.

Outlook

We have established that European investment in China is now increasingly dominated by a small number of big players, predominantly German companies, and their top suppliers. What is less clear is how this dynamic will play out in the years to come. China’s highly-restrictive zero-COVID policies will presumably be phased out over the coming years. This could encourage new firms to enter the Chinese market, reversing the concentration trend we have seen in recent years. However it is also possible, perhaps even probable, that the concentration of European investment in China around a small number of well established European firms whose presence is welcomed by the Chinese authorities becomes more entrenched.

As China’s economic slowdown accelerates, amid a real estate crisis and crackdown on private enterprise, and as policymakers in Berlin and other capitals press ahead with a resilience and diversification agenda, the proportion of China skeptics in European corporate boardrooms may continue to grow. We believe it is likely that the gap between the “chosen few” and the broader swathe of European companies that are reducing their China exposure, either by paring back their footprint on the ground or putting future investments into other markets, could become more pronounced in the years to come. What does the future hold for those firms that remain fully committed? We are already seeing what might best be described as an “internal decoupling” dynamic taking hold within some of these companies—as staff, supply chains and data flows are increasingly localized and ringfenced. This “in China for China” push risks opening up a greater divide between the headquarters of European firms and their China operations, a dynamic that poses long-term challenges for the companies concerned—reputational, cultural and financial (due to smaller economies of scale). Corporate boardrooms and policymakers will have to consider these risks as they weigh up their future relationship with China.

[1] The transaction value attributed to Daimler includes FDI by both Mercedes-Benz and Daimler Truck, which was spun off in December 2021.

[2] World Bank and OECD.