Two-Way Street – US-China Investment Trends – 2020 Update

The US-China Investment Project clarifies trends and patterns in two-way investment flows between the world’s two largest economies.

The US-China Investment Project clarifies trends and patterns in two-way investment flows between the world’s two largest economies. This report updates the picture with full year 2019 data and describes the 2020 outlook in light of a complex tangle of new developments including January’s Phase One US-China “Economic and Trade Agreement”, the COVID-19 global pandemic and the start of a US presidential election year.

The key findings of the report are:

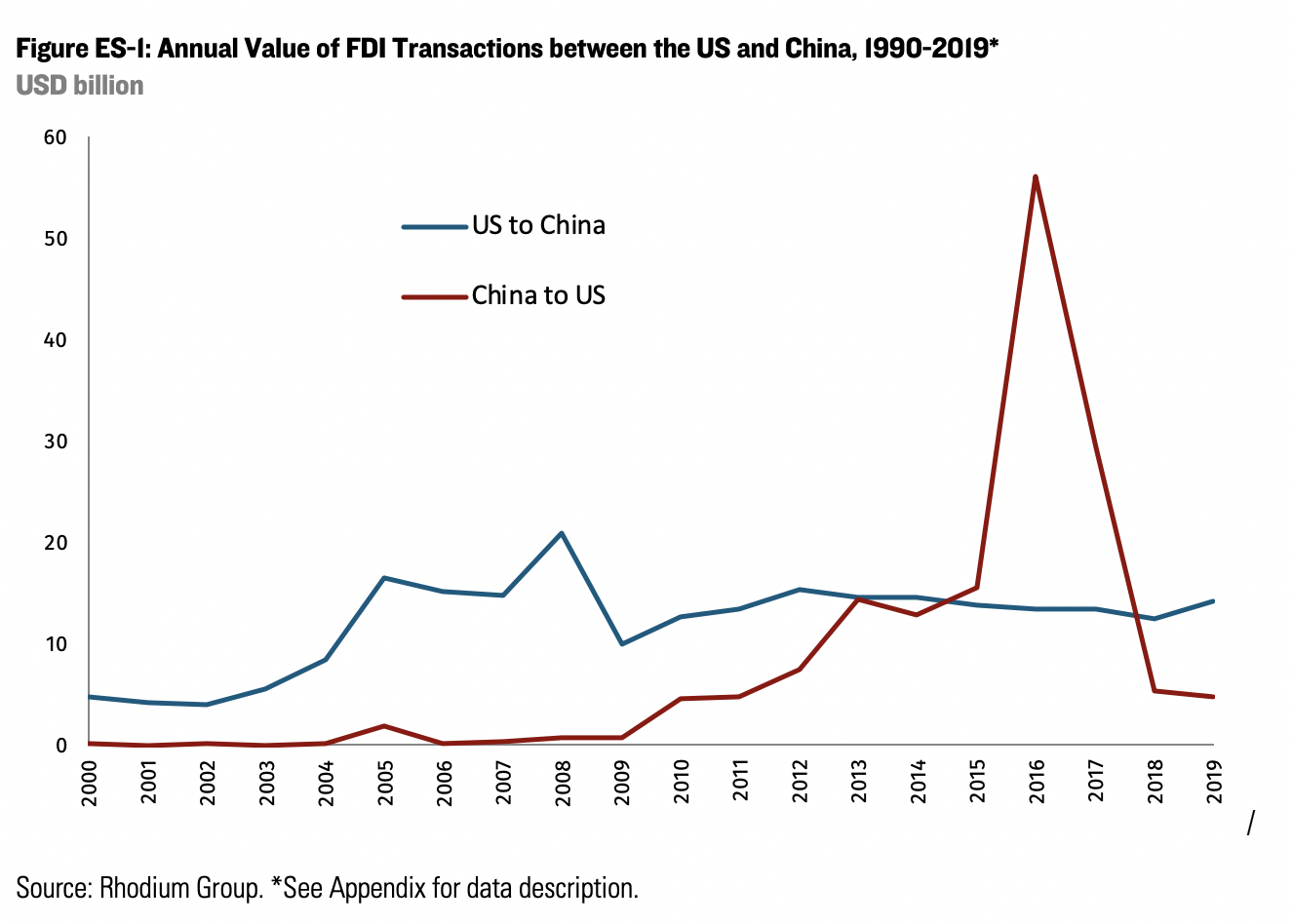

After big declines in 2017 and 2018, two-way FDI flows between China and the US flattened out in 2019 as the bilateral relationship continued to sour:

- Chinese FDI in the US dropped to $5 billion – a level not seen since the global financial crisis in 2009 – as Beijing’s outbound policies, US regulatory scrutiny and an uncertain outlook for US-China relations continued to weigh on investor risk appetite. The drop affected acquisitions and greenfield projects alike and was felt broadly across industries. Sectors with low political and regulatory risk – consumer products and services and automotive – have been the most resilient.

- US FDI in China edged up slightly compared to previous years to $14 billion as US firms continued to bet on Chinese consumer demand and seized opportunities from an easing of restrictions on foreign ownership in some sectors, including automotive and finance. Much of the stability of US investment into China was due to large multi-year greenfield projects geared towards meeting local demand in areas such as automotive and entertainment. At the same time, newly announced greenfield projects dropped, foreshadowing a slowdown in 2020 that was underway even before the COVID-19 pandemic disrupted the outlook.

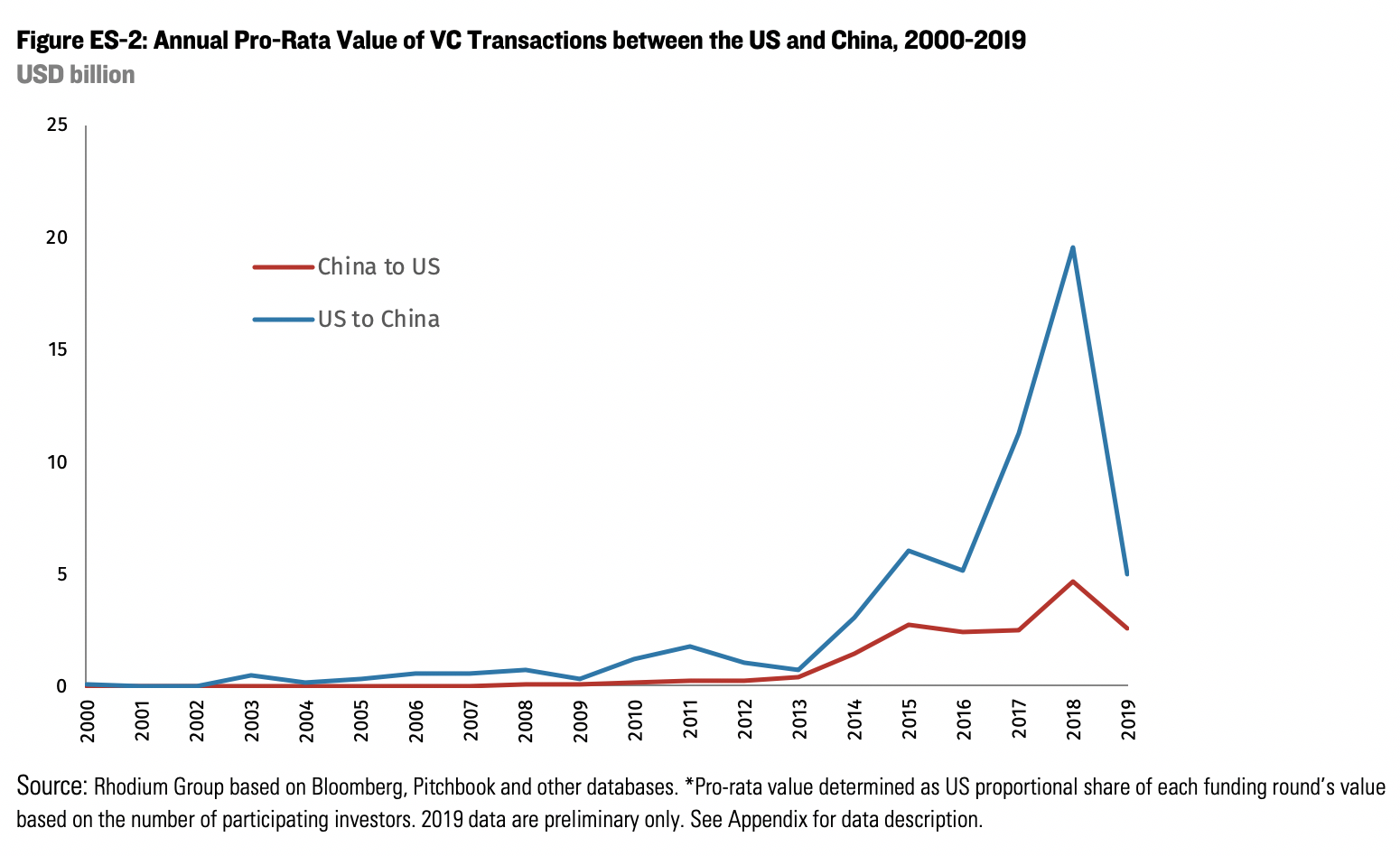

Two-way venture capital saw a steep drop in 2019 as China’s overheated technology market corrected sharply and US regulators got a mandate to scrutinize early-stage high tech deals:

- Chinese venture capital investment (VC) in the US fell to $2.6 billion in 2019, after an uptick of $4.7 billion in 2018. This downturn partly reflects technology market turbulence in China, which required local investors to scale back overseas ambitions. US-China political tensions and regulatory moves, including the passage of FIRRMA and ECRA, were also important factors. The contraction in 2019 affected all fundraising stages, target industries and investor types.

- In 2019, US-owned venture firms invested an estimated $5 billion in Chinese startups, a dramatic drop from the record $19.6 billion in 2018. The 2017-2018 boom in US venture capital investment into China was in line with a broader expansion and growth of the Chinese technology market and especially later-stage technology firms. In 2019, there was a slowdown in the Chinese VC market as investors became more selective in the face of increasing economic uncertainty and the view took hold that parts of China’s tech ecosystem had become overheated after years of rapid growth.

Visit the US-China Investment Hub

After dropping to a seven-year low in 2019, the US-China “Phase One” agreement set the scene for a positive 2020 outlook for bilateral capital flows but the global COVID-19 outbreak has changed the near-term outlook and could set in motion dynamics that alter the long-term picture:

- The immediate measures to contain the spread of the virus are impacting deal making: The global pandemic is bringing local economies to a halt, including in deal making. As a result of these real economy closures and physical restrictions on mobility, China’s outbound FDI to the US came to an almost complete stop in 1Q 2020. A recovery is likely in the second half of the year but full-year numbers will show the impact of the virus.

- The crisis is changing the outlook both for certain sectors and for economic growth as a whole, reducing investor risk appetite: China’s GDP growth will be close to zero this year compared to an average of 7.6% for the previous decade, and that slowdown is even more pronounced in certain sectors (for example, automotive). Company capital expenditures, including for foreign firms, are expected to fall, and the weight of China’s economy in global investment allocation models is under review. The short-term outlook for the US economy is similarly gloomy (with 2020 US GDP projected to see a contraction) and many sectors targeted by Chinese investors in the past could see heavy contractions, including tourism, energy and commercial real estate.

- COVID-19 will spur debate about global supply chain reorganization: The scramble around medical supplies has further inflamed concerns around the globe about dependence on foreign supplies of certain materials and triggered a serious debate about re-shoring and risk diversification. China is at the center of that debate, and supply chain diversification could lead US companies to move more manufacturing capacity out of China. At the same time, pressure to de-globalize supply chains could also mean higher levels of FDI going forward as multinationals are forced to localize operations and source from a greater number of suppliers.

- Crisis creates opportunity: Equity and credit markets have lost value due to the pandemic, which could generate buying opportunities. In the US, Chinese investors could look at brands and consumer-related assets in entertainment, food or other impacted areas. In China, the deflation of the technology sector bubble has already piqued the interest of foreign investors. Since stimulus options are limited, letting markets pull in distressed asset buyers is even more important.

- The trajectory of broader bilateral relations remains important: Coming off the “Phase One” agreement, the COVID-19 crisis presented an opportunity for the US and China to work together on crisis mitigation and scientific solutions to end the virus spread. However, intensifying economic competition and a systemic battle of political systems continue to weigh on the relationship as governments engage in blame games. That has further soured the views of businesspeople on both sides of the Pacific. The start of the US presidential campaign cycle could further amplify these risks in coming months.

The full report is available here: Two-Way Street 2020

To receive future updates, visit the US-China Investment Hub and subscribe. Follow @USChinaCapital on Twitter.