A Better Abacus for China

Preview of the upcoming major study RHG has undertaken over the past two years to review and build an understanding of China's system of national accounts.

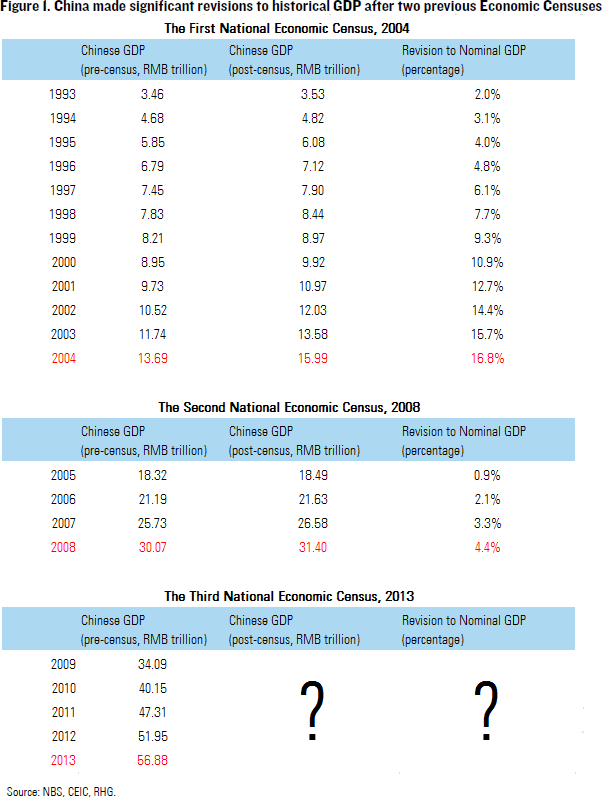

Beijing is entering a critical one month period of announcements about its gross domestic product (GDP) – the broadest measure of its economic size – and GDP growth that will partly re-frame our understanding of China’s economy. By the end of December the National Bureau of Statistics (NBS) is expected to unveil revised economic census headline numbers for 2013 – the latest in a line of economic reassessments that occur every five years. Past revisions have announced that China was 5, 10, or even 17% bigger (2004) than previously thought because “missing” activity was identified. A couple weeks after that, around January 20th, 2015, officials will issue a first reading for 2014 GDP growth. This will finally tell us how far below the stated 7.5% 2014 target the nation came out. Despite the significance of these big releases, long-standing qualms about the reliability of Chinese data undermine their potential to illuminate the outlook.

With that cynicism in mind, Rhodium Group has been working in partnership with CSIS since mid-2013 to review China’s system of national accounts and develop a revised assessment of China’s real GDP. This note previews our results, which will be published in final form early in 2015. There are three takeaways from the study that are worth sharing now to help observers interpret the coming news. First, China is using an upgraded methodology and the results should be taken seriously. Beijing is counting activity previously underestimated, and converging toward international best practice: President Xi is locking China into greater statistical transparency – by choice – with implications for how the $10 trillion economy operates. Second, we re-estimate China’s 2008 nominal GDP – the most recent year which available data permit us to dissect properly, to have been 13 – 16% bigger than official figures previously showed. Finally, Beijing is using something similar to the revised methods we applied to 2008 for better gauging 2013 and 2014 and years to come: extrapolating from our experience therefore, China – and hence the world economy – is likely to be seen as perhaps $1 trillion bigger a month from now than expected today. This presents a number of implications, including fewer years – all things being equal – before China passes the US as the world’s largest economy.

ECONOMIC CENSUS AND NBS REVISIONS

It is obvious that China has grown rapidly, but few are comfortable with the data describing that journey. On the eve of the People’s Republic’s 65th anniversary this year, National Bureau of Statistics (NBS) head Ma Jiantang wrote in the People’s Daily that China delivered average annual growth of 8.2% from 1953 to 2013, reaching RMB 57 trillion in 2013, 12.3% of total global output. This, he noted, was a “miracle” achieved by the Chinese people through diligence, perseverance, and wisdom. However, these statistics carry an asterisk, and stand under a cloud of public misgivings due to enduring inconsistencies, such as the sum of provincial gross output surpassing national aggregates year after year, at ever-expanding margins.

Beijing is committed to making improvements. At the end of 2012, just days before President Xi Jinping was elected General Secretary of the Communist Party, Beijing kicked off its third national economic census with 2013 as the measurement year. China’s two previous economic censuses, in 2004 and 2008, significantly revised past GDP figures and changed how the economy was measured. This time the changes will also be remarkable (Figure 1).

The 2013 economic census is not just about better data compilation under the existing framework. In parallel to the census – the initial results of which are expected later this month – Beijing has been upgrading its whole system of national accounts. With international standards rising and China’s own economic mix changing in ways that are poorly captured by existing measures, Beijing had no choice. China’s current GDP framework, the Chinese System of National Accounts 2002 (2002 CSNA), was built from a now outdated global standard, the System of National Accounts 1993 (1993 SNA), run by five organizations led by the United Nations. That system was revised to the 2008 SNA half a decade ago and countries have been making the conversion since, including Australia, Canada, the United States, European Union member states, South Korea, and the United Kingdom.

China established a team to prepare for the switch, led by NBS Deputy Chief Xu Xianchun, who oversaw the evolution of China’s statistical work over the last two decades. In November 2013, Xu announced that China would employ the 2008 SNA and that the transition would accompany the 2013 economic census, with a new 2014 CSNA published in 2015. According to our interactions with the NBS, restatement of China’s 2009-2013 GDP (starting in the first year after China’s 2008 census) and the new 2014 figures will be based on this new Chinese framework. In a nutshell, the new methodology will focus on three changes. First, it will adopt many of the major changes in the 2008 SNA, such as treating research and development (R&D) expenditures as fixed asset investment; R&D was previously counted as intermediate inputs by most entities and therefore not part of GDP. Second, it will improve the counting of fast-growing intangible activities and services to better reflect the true economy. For instance, Beijing will recalculate “imputed rent” that home owner-occupiers “pay” to themselves based on market rent rather than construction cost data. Third, the new system will rationalize and streamline the relationship between central and local statistical authorities and between different divisions within the same bureaucracies (including the NBS), making distortion less pervasive.

Data published by different Chinese authorities can sometimes be contradictory, or at least inconsistent. There are anomalies and inconsistencies in advanced economies too, but not to the same extent. For example, in Japan, which employs a central-local GDP accounting structure similar to China’s, the sum of all Japanese prefectures’ GDP surpassed the national aggregate by 5% in 2011, while in China the discrepancy was nearly 10%. Beijing, which increasingly needs to steer policy based on standard employment, inflation, and production gap signals rather than big project campaigns, is aware of this discrepancy, and is acting as the principle advocate for improvement. The new census and transition to the 2014 CSNA are important moves on this front. China’s growth through 2017 (which is expected to fall significantly from the double-digit levels of the past to perhaps 6-7% per year in the medium-term) depends on strengthening service sectors and promoting small and medium businesses, areas where statistical coverage has historically been at its weakest.

Modern policymakers rely on data to make decisions. Despite his affection for ancient Chinese learning, President Xi knows that archaic statistical notions – like councilor Guan Zhong’s admonition to Duke Huan of Qi in China’s Spring and Autumn period 2700 years ago that, If one does not keep statistics secret, those below will control the government on high¹– would be ruinous for the modern, market economy he seeks to build. Xi is pivoting a $10 trillion economy away from heavy industry, and toward more services, higher value-added industrial products, and intellectual work, but he lacks good data with which to make choices. Former chairman of the banking regulatory commission Liu Mingkang publicly complained about the lack of sound data that keeps Beijing in the dark. Enhancing data quality is an institutional need for China’s leaders if they are to implement stated reforms. Good data will allow for better allocation of resources, efficient counter-cyclical stimulus, and the monitoring of financial risks.

Many 2014 CSNA changes will have no aggregate impact. While some affect headline GDP or its composition, some are just conceptual. But among the dozens of changes the NBS is contemplating, two are going to have a heavy impact on headline GDP in the 2013 census results. One is the inclusion of R&D expenditures in GDP as fixed asset investment instead of as intermediate inputs (which are not counted). The other is the recalculation of home owner-occupiers’ imputed rent based on market rent rather than on construction costs.

A BETTER ABACUS, A BIGGER ECONOMY

In early 2013 we began reevaluating China’s economic size and its implications, in partnership with colleagues at CSIS who shared our concern about the global importance of China’s national accounts. China is widely projected to overtake the US as the world’s largest economy in the not so distant future. Based on a purchasing power parity (PPP) approach, the International Monetary Fund (IMF) says that has already happened in 2014. Despite China’s status as the first economic peer competitor to the US in more than a century, its national accounts data – the sources, the concepts, the methodology – are poorly understood. By nature, the work of national accounts is arcane and that reality is compounded by China’s political opacity. Policymakers – as well as business leaders and other stakeholders worldwide – are left reacting to China using suspect information.

Our research has taken us into the nitty-gritty of China’s GDP accounting system, with the goal of clarifying concepts and methods to compile a new set of nominal GDP numbers. Now in the final stage, our dissection of China’s full GDP regime will be published in partnership with CSIS as Broken Abacus, early next year. The report provides a historical review of GDP accounting, a discussion of China’s statistical systems and the legitimacy of its critics, a full recalculation of the most recent assessable year (2008), and an analysis of the implications for the policy and business community, today and going forward. We build out our results not from just a handful of proxies such as electricity data, but from the same source data used by the NBS, reinterpreted in a variety of ways to comport with best practices in national GDP accounting. Where bottom-up data are unusable, we draw comparisons with similar economies or employ alternative Chinese data, such as tax numbers. We use publicly available data to estimate the imputed rent and value-added derived from R&D expenditures – two items largely understated in extant 2008 figures – which we suspect Beijing will publish separately for 2013.

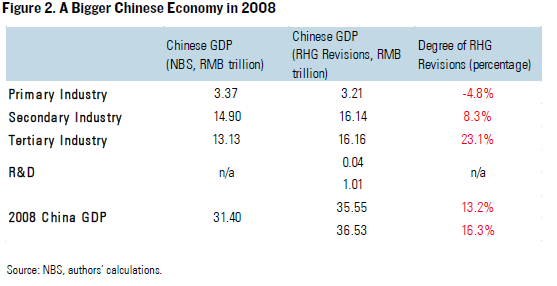

The table below presents our working re-estimates of China’s 2008 nominal GDP by industry. R&D expenditures are treated as a separate sector because China’s data does not permit us to attribute them by sector. The bottom line from our re-estimate is that China’s actual nominal GDP in 2008 exceeded the officially reported figure by 13.2% – 16.3% (Figure 2). This is a conservative range: the estimations we chose to set aside due to methodological concerns are almost all on the high side of this range. In value terms, a higher estimate for imputed rent is the biggest contributor to the upward restatement, followed by higher estimates for industry and construction activity, for traditional service activity, and for R&D expenditure. Our restatement for the agricultural industry is a slight downward adjustment.

Combining our better assessment (with hindsight) of 2008 and an understanding of the methodological changes we expect Beijing to make for 2013 GDP, we are in a position to offer a perspective on the soon-to-be-released results and their credibility. If the need for upward restatement we identified for 2008 holds constant for 2013, NBS’s plan to upgrade methodology should increase how large we believed China to be that year by perhaps 14.5%; but it is likely that NBS will argue it had already partially closed that gap after 2008, and therefore an upward revision of 5-10% is more likely. A 10% augmentation of the current official 2013 figure means $918 billion in new-found money – or upward revision – for last year. Projections of the 2014 full year result would be increased accordingly.

CHINA’S GDP IN THE BROADER CONTEXT

By the end of December 2014, the NBS will likely unveil its 2013 revisions. By about January 20th, 2015, they are scheduled to release a first reading for 2014 GDP. As the property and infrastructure sectors are weighing down the economy, Beijing is expected to announce a 2014 growth result that misses its stated 7.5% goal, and analysts are watching for signs of a lower than 7.5% target for 2015.

With a revised base GDP number, the political context in which we analyze China’s growth dynamics has fundamentally changed. A base nominal GDP figure 10-15% above current official numbers, plus growth holding up in the 6-7% range through 2020, would mean tens of trillions in additional RMB economic output through the decade. That will strengthen the need for accelerated reforms in China if Beijing does not wish to fall out of that growth range down the road. The old-line growth model with diminishing returns looks all the more wasteful in light of the renewed GDP figures, so we expect the current debate about trade-offs between reform and growth will largely disappear over the coming years. In China’s new reality, securing economic growth is no longer a valid excuse for stalling on reform; growth can only be achieved through deeper restructuring and liberalization.

Upwardly revising GDP also presents tremendous implications for policy targets and expenditures that are benchmarked against nominal GDP. The revised numbers will partly reshape the picture where expenditures on items such as military equipment, education, and social security are expressed as a share of GDP. And of course, if keeping a certain expenditure item – such as healthcare, or R&D – above a certain level as a percent of GDP is an enshrined policy commitment already, then the GDP revision will have fiscal and budgeting implications for those line items.

For the United States, there are several implications. First, the probability assigned to the possibility that China’s GDP is actually smaller than thought, rather than larger, should be reduced. Second, the statistical methodology upgrading and commitment to greater transparency, evidenced by President Xi’s announcement of China’s intention to subscribe to the IMF’s Special Data Dissemination Standard with higher public reporting requirements, support the hypothesis that a broad-based economic reform impulse underpins China’s current leadership, who will find it more difficult to deny data anomalies. Third, the revised growth picture demonstrates how important and dynamic the burgeoning services sectors are to China’s performance. These are manned by a different set of special interests, executives and stakeholders than the industrial giants most in favor for their contributions to GDP in the past. Fourth, as has been noted above, for expenditure components often viewed as a percentage of GDP, for instance military spending, an augmentation for China’s GDP may change their ratios against the total economy, if their values are not revised proportionally. A similar implication applies to the line items decreed to keep pace as a share of GDP – such as healthcare spending – for which expenditure commitments will need to be stepped up accordingly. Finally, all things being equal, with a 10% larger GDP base, China would be expected to reach parity with the United States in nominal terms sooner. That assumes, of course, that in the process of upwardly revising current GDP, China’s statisticians are not compelled to conclude that the era of “moderate-to-high-speed growth” is already further behind the nation than originally thought.

Notes

¹ Guanzi, Volume Two, p. 390, § 71.2. W. Allyn Rickett. Princeton University Press: 1998.

· Special thanks to Yaqi Wang and Qi Dai for their contributions.

· Correction: An earlier version of this note misstated the basis China relies on to compute imputed rent. It is current construction costs, rather than historical construction costs (which is used for several other purposes). The China National Bureau of Statistics contemplates transitioning to using market rents, rather than construction costs, to evaluate home owner-occupiers’ imputed rent. The correction was made on December 17, 2014.