Critical Mineral Chokepoints Extend Far Beyond Mining and Refining

China dominates manufacturing of intermediate goods that use critical materials as inputs, creating an additional layer of chokepoints, which Beijing is targeting in its most recent export controls—including outside of China.

Beijing’s export controls have focused global attention on its dominance of raw and refined critical minerals. These upstream sectors logically became the focus of the recent sprint to develop new capacity and stockpiles, but China’s leverage over critical mineral supply chains extends far beyond raw materials and refined products. China dominates manufacturing of intermediate goods that use critical materials as inputs, such as silicon wafers, rare earth permanent magnets, LEDs, and battery materials. These intermediate manufacturing sectors create an additional layer of chokepoints, which Beijing is targeting in most recent export controls—including outside of China.

Recent state-backed investments by the United States, Japan, Canada, Australia, France, and Germany, in upstream mining and refining capacity are a step toward easing this severe dependence. But China spent a decade using its control of upstream minerals to expand its market share in downstream manufacturing. If advanced economies hope to break free of critical mineral chokepoints, they need a comprehensive approach that ties upstream investments to downstream applications. Plans that overemphasize mining and refining—or even raise costs for downstream sectors, such as the US proposal for price floors—could inadvertently exacerbate overall dependence on China.

China poised to weaponize downstream chokepoints

Raw and refined minerals are the tip of the iceberg

China spent the last decade consolidating its dominance of rare earths and other critical minerals. Beijing then leveraged its control over upstream supplies—and ability to depress prices through subsidies and regulatory interventions—to increase China’s market share in higher value-added downstream manufacturing. These products, such as magnets, wafers, LEDs, and battery materials, are essential inputs for advanced manufacturing, from clean energy to defense technologies (Table 1). China’s recent export controls have primarily targeted upstream materials (the dark blue items in left three columns in Figure 1), but Beijing’s leverage is equally strong in the intermediate manufactured products (righthand column) that were the focus of industrial policy for the last decade. Any advanced economy effort to eliminate supply chain vulnerabilities must also address these downstream manufactured goods that incorporate critical minerals.

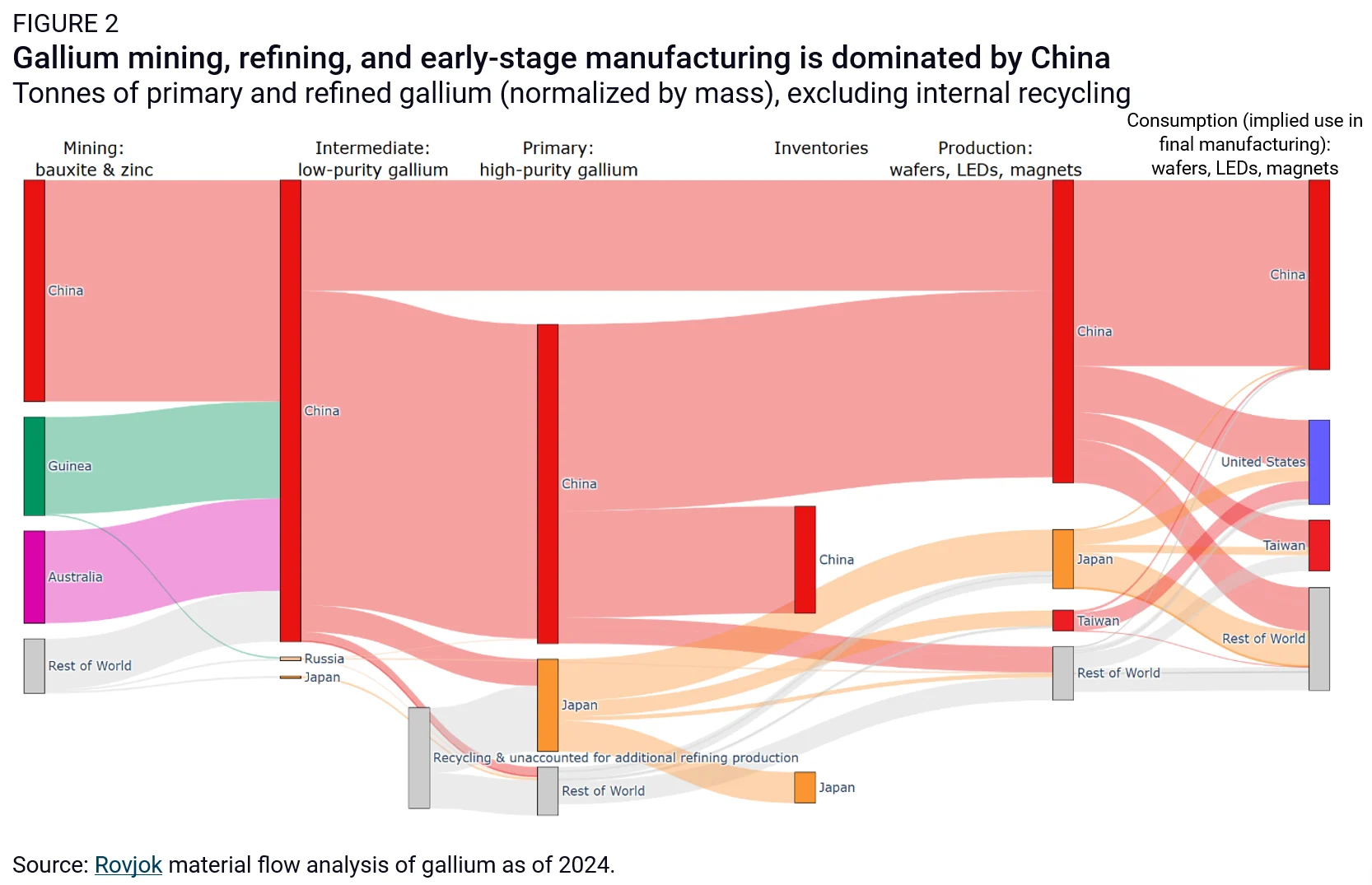

Mineral supply chains vary widely, but the structure of gallium flows (Figure 2) illustrates the risks of China’s manufacturing dominance. While production of raw materials (“mining”) and final manufacturing downstream (“consumption”) are more diversified, China dominates refining stages and the manufacture of intermediate manufactured products (“Production: wafers, LEDs, magnets”). When the vertical integration and global footprint of Chinese suppliers is factored in, China’s market concentration is even larger.

As a result, while direct global dependence on China for raw and refined materials is severe, global dependence on China for minerals embedded in finished products is just as significant—if not even more so. Figure 3 compares the world’s imported mineral raw materials (ores, chemical forms, processed forms, etc.) from China to mineral content embedded in intermediate products imported from China, such as wafers, magnets, and li-ion batteries. The volume of critical minerals embedded in these manufactured goods generally exceeds the volume imported directly, and when final goods like EVs, solar panels, and wind turbines are included, the dependence is even more severe.

China is expanding the scope of its export control regime

China is expanding its export control regime to exert end-user restrictions and target downstream products with embedded mineral content. In October 2025, Beijing released new export controls that included provisions for extra-territorial enforcement. Though these controls were temporarily suspended, they threatened to curtail sales of rare earth elements to foreign magnet and semiconductor manufacturers that did not comply with China’s end-user requirements. Even more concerning, MOFCOM’s February 24, 2026 export controls prohibited dual-use exports to 20 Japanese firms, including restrictions on foreign entities’ ability to sell products to the Japanese companies. This extended Beijing’s controls to countries that process or manufacture midstream items out of Chinese critical minerals, dramatically expanding the reach of China’s leverage.

The application of these measures has so far been limited because Beijing faced bureaucratic constraints to implementing end-use checks—including lack of qualified MOFCOM personnel abroad. But Beijing is actively resolving these constraints so it can extend the reach of its export controls to third countries.

There is also a risk that Beijing will use its enhanced export control regime to thwart foreign de-risking efforts, including in downstream intermediate and final products. In the most recent spat with Japan—ostensibly in response to Prime Minister Sanae Takaichi’s comments about Taiwan—Beijing targeted TDK Corporation, a major Japanese manufacturer of rare earth magnets. This raises the prospect that Beijing might try to undermine foreign efforts to reduce their exposure to China’s dominance of intermediate manufactured products. China has already restricted the export of several types of mineral extraction and processing equipment, as well as battery manufacturing technology. It is also reportedly considering restricting the export of more technologies needed to support de-risking efforts downstream, including, for example, solar panel manufacturing equipment.

A downstream strategy needs coordinated planning

Advanced economy competition makes downstream cooperation harder

Resolving chokepoints in downstream manufactured goods is a daunting challenge. Intermediate products like wafers, LEDs, and battery materials are low-margin businesses that require an experienced labor force, specialized supply chains, and a deep bench of technical know-how. Few countries can support a resurgence in ex-China manufacturing in these sectors, and fewer still can compete in the face of China’s economies of scale, state subsidies, deflationary pressure, and control over key production technologies. Supply-side subsidies and other state support that work (reasonably well) in mining and refining would struggle to sustain manufacturing across hundreds of differentiated intermediate products.

Advanced economies must work together to create sustainable demand for new supply chains to loosen China’s market concentration in midstream and downstream manufacturing sectors. To foster investments in risky manufacturing sectors, ex-China producers will need privileged access to large, predictable consumer markets. Yet cooperation will be difficult in downstream markets.

Interests have been (relatively) aligned across producer and consumer countries seeking to diversify upstream supply chains, which has helped facilitate coordinated support for mining and refining investments. However, advanced economies compete in downstream sectors like automobiles, machinery, electronics, clean energy, and defense, which makes cooperation more difficult. As advanced economies use subsidies, trade barriers, and local content requirements to bolster these sectors, they could trigger beggar-thy-neighbor competition and trade tensions. Trade friction among advanced economies could eat away at the scale of market demand for ex-China producers, increasing costs for everyone, and undermining incentives to invest in new capacity.

Upstream support measures can harm downstream producers

On February 4, Washington hosted the Critical Minerals Ministerial that sought to establish a price floor for critical minerals with 54 countries. USTR’s February 26 request for comment on a plurilateral agreement suggests Washington may be moving forward, even though many large economies appear wary of the tariff-based price floor. There is a logic to price floors under certain conditions, as protecting revenue is important to incentivize private investment in mining and refining. This kind of mechanism could also protect against market volatility, including price shocks from China, which have undercut global markets more than once.

However, the bigger problem is the unintended consequences downstream: Higher prices for minerals will increase costs for mineral-intensive downstream manufacturers who compete in price-sensitive global markets. Manufacturing value chains will quickly realign so that dependencies (and imports) move further downstream to finished or semi-finished products if foreign manufacturers out-compete firms producing at higher costs inside the price floor coalition. For example, European automakers manufacturing EVs with higher-cost minerals produced within a coalition may face even steeper competition from Chinese-made EVs in export markets. Policymakers inside a price floor regime will quickly face pressure to protect successive stages of the value chain. Tariffs on rare earths may expand to magnets, then motors, then turbines as competitive pressures move downstream. The resulting web of tariffs—potentially between advanced economies that are all seeking to de-risk supply chains—could create immense complexity and uncertainty about which products (and which countries’ goods) face tariff protection. Even without trade tensions, companies producing inside a price floor coalition will struggle in third export markets where higher input costs cannot be offset through domestic tariffs.

This is not a theoretical concern. Efforts to protect upstream supply chains have a history of reducing output in downstream sectors. Japan’s decade-long struggle to reduce dependence on Chinese rare earths appears to have accelerated the migration of downstream magnet producers to other countries, where they were free to use Chinese inputs. There is a risk that US policy does the same: focuses too much on upstream suppliers while inadvertently hurting domestic manufacturers—reshuffling vulnerabilities, not reducing them. To avoid this, it will be essential to introduce support for demand or rebate mechanisms for producers that face higher input costs. A successful de-risking strategy will require a comprehensive approach to value chains that works in service of downstream manufacturing—as Beijing has done for more than a decade.