The Impacts of Rising Electricity Demand from Data Centers on US Energy and Emissions

As the pace of data center buildout in the US rapidly evolves, we examine the energy and emissions impacts of a future where data center electricity demand grows at a faster rate than we've previously considered.

The pace of data center buildout in the US is rapidly evolving, as improved chip design leads to efficiency gains, while geopolitical and economic competition in the AI race push for maximizing total compute and, therefore, electricity use. In Taking Stock 2025, our energy outlook under current policy, we included a middle-of-the-road estimate for data center energy demand. In this note, we examine a future where data center demand grows at a 30% faster rate through 2030 and 25% faster rate through 2035 than we previously considered, given data center momentum.

Supply chain bottlenecks, orderbook backlogs, jammed interconnection queues, and onerous siting and permitting processes all pose headwinds to adding large amounts of new supply to the grid. In our higher data center demand scenario, these headwinds prevent substantial new power generation from coming online by 2030 to meet this increased demand—instead, existing gas and coal generation are used more. With more time for new generating capacity to come online, the grid response in 2035 varies depending on market conditions. With favorable market conditions for decarbonization, solar and wind account for the lion’s share of capacity additions in 2035. With less favorable market conditions—cheap natural gas and higher prices for clean generating resources—gas additions dominate, and emissions increase relative to our baseline; although, corporate clean energy commitments may offset some of these emissions. This note also looks at the impacts of higher data center demand on electricity costs, finding the costs to run the electric grid also increase with more demand.

Higher data center demand

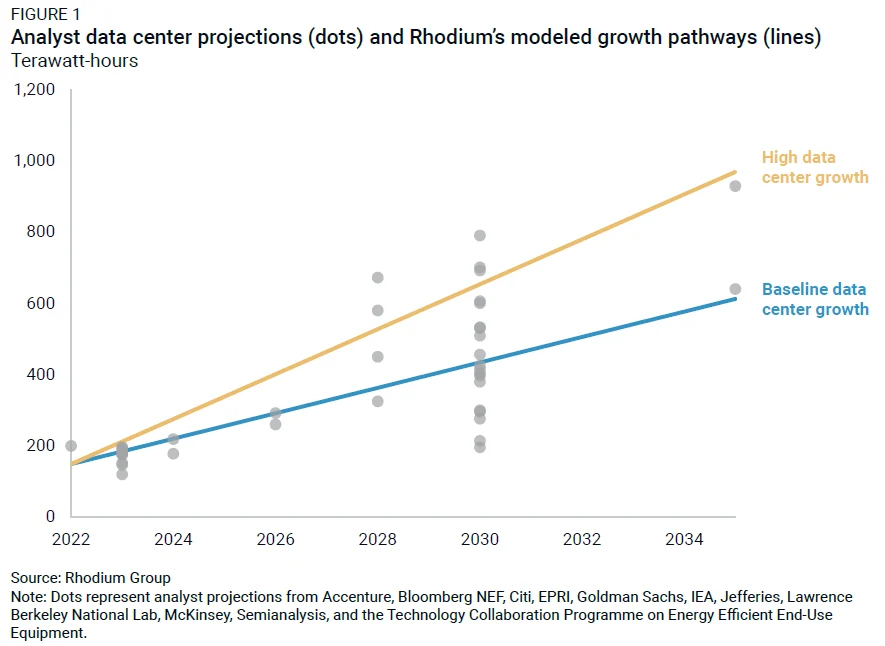

Just how high electric demand from new data centers might get in the near future is one of the most important questions for investors, grid operators, equipment manufacturers, and policymakers. For now, the answer is highly uncertain, and estimates are all over the map (Figure 1). The spread between the lowest and highest analyst expectations for data center demand in 2030 is more than the combined current electricity demand of the states of California and Florida. In addition to being a dynamic space, differences in the underlying methods for estimating data center electric demand (for example, using interconnection requests, which leads to an overestimate, versus hardware shipments) contribute to this large range. More recent estimates tend to be higher than older ones. For example, recently, the Electric Power Research Institute increased its 2030 data center electricity load by 55-65% relative to its 2024 estimates.

We released Taking Stock 2025 in September 2025, which contained a middle-of-the-road estimate for data center electricity demand growth, nearly doubling by 2030 and more than tripling in 2040 relative to 2024 levels (Figure 1, blue line). With recent demand estimates exceeding the largest estimates from a year ago, we wanted to understand the potential implications of what even more data center demand could mean for the grid, businesses, and households. To do this, we assess a high data center growth scenario based on a 30% faster compound annual growth rate (CAGR) for data center demand through 2030 and 25% faster CAGR through 2035. This leads to data center demand equivalent to 14% of total US power generation in 2030 and 18% of total US power generation in 2035, relative to 10% in 2030 and 12% in 2035 in the baseline data center case.

We assess the impacts of this additional demand across the three emissions scenarios we modeled in our Taking Stock 2025 outlook (more details on scenario design are available in the technical appendix). Our low-emissions scenario offers the most favorable conditions for clean electricity deployment: rapid declines in clean technology costs, paired with relatively high fossil fuel prices. Our high-emissions scenario is the inverse, with much slower declines in clean tech costs and rock-bottom fossil prices; our mid-emissions scenario splits the difference.

What more demand means for the electricity grid

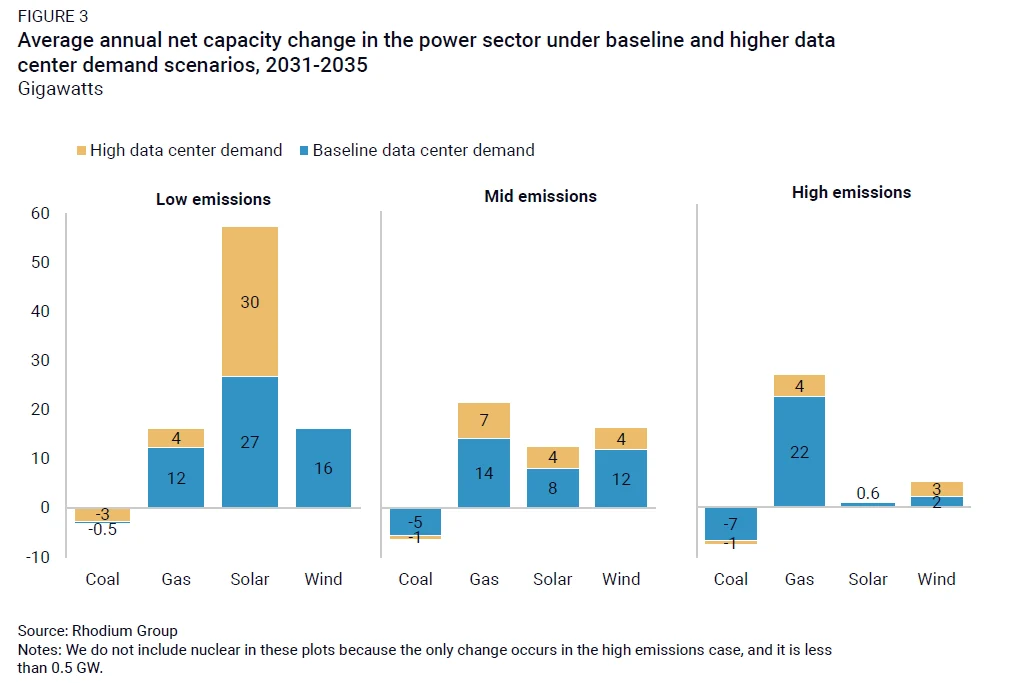

Across different scenarios, we find higher data center energy demand driving very little power capacity change on the grid through 2030 compared to the baseline. That changes as the 2030s progress. Our modeling accounts for current policy and the sector state of play, including tax credits, interconnection backlogs, and lack of available gas turbines. The pipeline for electricity generators through 2030 is mostly clean; as a result, output from new clean generators meets all new demand for electricity through 2030 and also backfills for a large share of retiring coal capacity under our baseline data center demand.

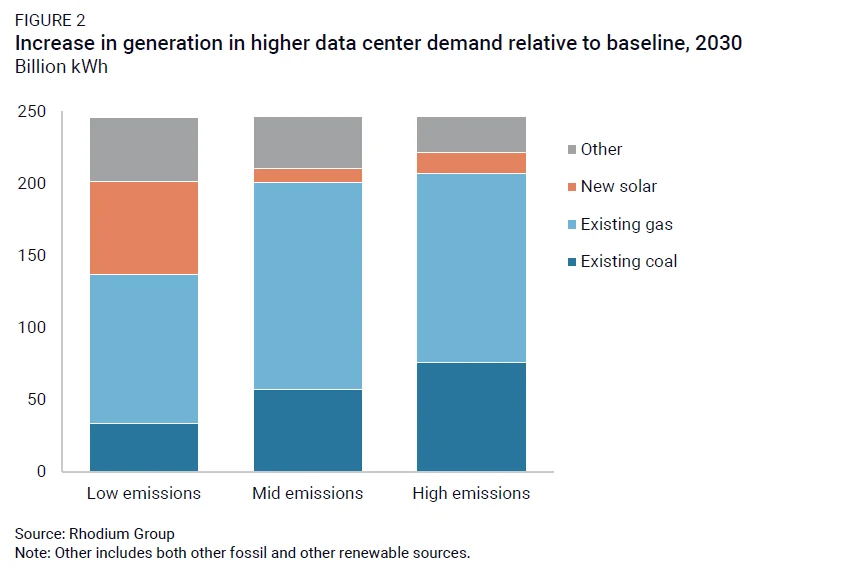

These same factors lead to capacity additions that are largely the same in our increased data center demand scenarios through 2030. Since not much new capacity can be added in the near term, we instead see existing gas and coal plants running at higher capacity factors and meeting 55-85% increased demand relative to baseline data center demand growth (Figure 2).

However, the story changes when there’s more time to add additional capacity to the grid in response to higher demand growth from data centers in 2035. With favorable market conditions for clean electricity generators in the low emissions scenario, solar and wind contribute the lion’s share of new capacity to the grid through 2035 under baseline data center demand (Figure 3, blue bars). Higher electricity demand from data centers dials up this trend, with new solar additions more than doubling relative to baseline (yellow bars). With more favorable conditions for fossil generators in the high emissions scenario, gas dominates additions through 2035 while renewables struggle to compete, and higher new data center demand pushes further in the direction of gas.

What more demand means for greenhouse gas emissions

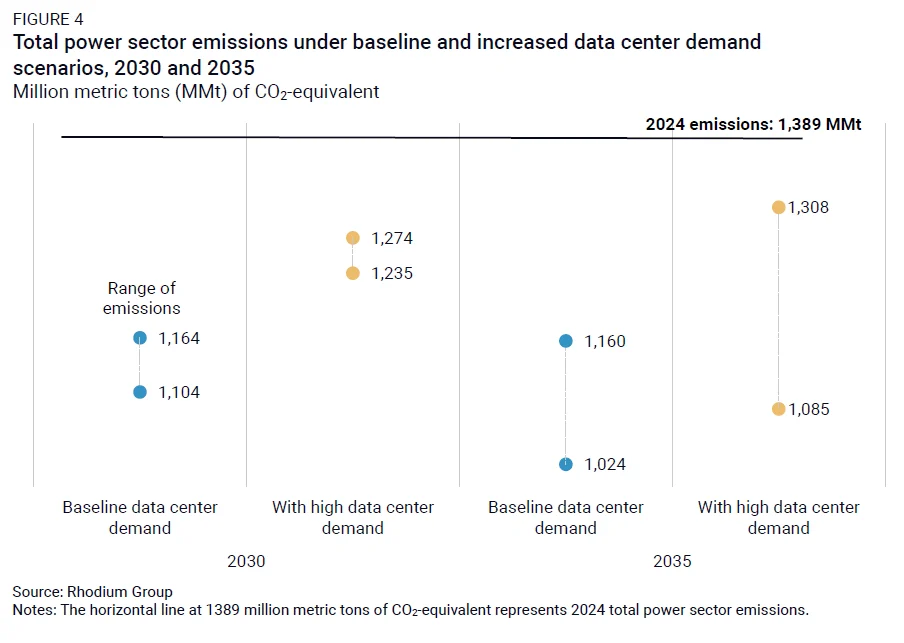

These power generation changes are accompanied by changes in greenhouse gas emissions, which could be partially offset by corporate clean energy commitments. In Taking Stock 2025, our annual outlook for US energy and emissions under current policy, we project that total power sector emissions generally decrease through the rest of this decade, reaching 17-21% below 2024 levels in 2030. Emission trajectories diverge in the 2030s: declines continue in our low and mid emissions scenarios, which achieve a 25-27% below 2024 levels in 2035, while emissions stay effectively flat in our high emissions scenario at 17% below 2024 levels. These projections include our baseline modeling for surging data center electricity demand under a middle-of-the-road data center buildout.

In our higher data center demand modeling, total power sector emissions are 6-13% higher in 2035 than in our baseline case (Figure 4). This still represents an emissions decline, but by less—a 6-22% decline in 2035 relative to 2024. Despite a generally unfavorable policy environment for clean technologies, the power sector is directionally getting less carbon-intensive as clean technologies get cheaper and more competitive with incumbent fossil technologies.

Most hyperscalers have commitments to procure clean electricity for their operations. The Corporate Energy Buyers Association reports that around 130 GW of clean electricity was procured by corporate buyers from all sectors from 2014 through 2025, representing at least 4% of total US electric generation. Some of the clean energy capacity we project to come online over the next decade is likely a direct result of data center companies procuring clean electricity. If most of the increase in data center electricity demand is coming from these same large data center companies (Lawrence Berkeley National Lab reckons around half of data center growth through 2028 will come from hyperscalers) and they sustain this commitment to building cleanly, these emissions increases could be mitigated.

Hyperscaler investments in bringing advanced nuclear, geothermal, carbon capture and sequestration, and other clean technologies to commercial scale also play an important role in system-wide decarbonization, but their impact is harder to quantify and will likely show up further in the future. Our estimates rely on normal market and policy conditions for power developers, which have not been the case recently with trade policy turbulence and attempts by the Trump administration to slow wind and solar development.

What more demand means for electricity prices

Because increased energy demand requires more generation, the total cost to run the energy grid increases. Total system costs increase by 13-15% in 2035 under higher data center demand relative to our baseline scenario. This higher cost is spread across more electricity sales, so average national electricity rates across all sectors are held effectively flat. However, this is not evenly borne across rate classes. We estimate that national average commercial electricity rates decrease by ~3% in 2035 because higher system costs are spread over more sales from data centers (their denominator increases), while residential rates go up by ~2% in the same period because the total system cost increases while residential sales remain relatively stable. This increase comes on top of retail rates that are already increasing faster than the pace of inflation for the first time since the early 2000s, driven by disaster recovery costs, inflationary pressure on grid components, and anticipated new demand.

There is certainly room for data center developers to pay their own way, but this analysis reflects the current reality, which does not yet include such pledges flowing through the system. Several policy proposals, such as PJM’s proposal to have data centers pay 100% of the energy costs for their new builds, could help shield ratepayers. If companies follow through on the Trump administration’s Rate Payer Protection Pledge, the cost of new supply and grid upgrades for data centers would be paid for by data center developers. That could help cushion price impacts for everyday consumers. Still, demand for new electric generating capacity and grid equipment from data centers will lead to inflated costs for all grid improvements and supply additions, regardless of whether they are supporting data centers. Without a major expansion of supply through siting and permitting reforms, interconnection acceleration, and more manufacturing capacity, increased demand from data centers will elevate costs for most players in the electric power system.