A stretch of the South-Central and Southwest United States, from Louisiana and Texas to Arizona and Colorado, is already experiencing rapid changes to its energy system and economy, and those changes are poised to continue. Rapidly increasing electricity demand from large load sources like data centers and record installations of new electricity generators look to sustain this transformation. States in this region can strengthen their grids and their economies by transforming it into a hotspot of next-generation geothermal power deployment and manufacturing. Next-generation geothermal provides a clean, firm complement to increasing amounts of variable energy generation projected to come online in this region, and a combination of promising subsurface geology, a robust workforce rooted in the region’s oil and gas backbone, and strengths in manufacturing make this cluster of states particularly well-suited to seize the opportunity.

Targeted, well-designed, ambitious policies enacted by states can leverage the immense changes and investment opportunities on the horizon to drive deployment of geothermal on the grid, which can scale from basically zero today to providing as much as 4% of total regional power generation by 2035. The region is also well-positioned to manufacture Organic Rankine Cycle (ORC) turbines, a key current bottleneck in large-scale geothermal deployment. The effects stretch beyond this corner of the country, with the region becoming a supplier of these turbines to geothermal facilities elsewhere in the US, and the learning that comes from drilling and installing new geothermal plants driving down costs everywhere. The result: the region can drive $5-12 billion of the coming investment wave into the next-generation geothermal industry by 2035 and support tens of thousands of job-years, positioning these states as a geothermal powerhouse for the next decade and beyond.

Leveraging the electro-industrial transition

A concentrated wave of investment has been building in the United States over the past few years, focused on growth of electricity-intensive industries like data centers and clean manufacturing alongside with the electric infrastructure needed to power these quickly expanding fields. These trends are poised to continue, driving rapid increases in demand for electricity and linking US economic fortunes to its ability to serve electric load quickly, reliably, and cheaply. In this note, we continue our analysis of the ability of states to meet the moment in this transition to a new electro-industrial era.

Our first note on this topic, Unlocking Electro-industrial Growth to Meet Surging Electricity Demand in the Southeast, describes the basics of this electro-industrial growth and demonstrates how states in the Southeastern United States can enact smart, targeted policy to meet fast-rising electricity demand while building a sustainable regional economic engine with substantial private investment and job growth. In that first note, we show how state policy can act as an accelerant for trends that are already strongly established in a region.

We continue our work on the electro-industrial economic transition by answering a different question in this note: how can states scale a much more nascent but critical industry, creating a regional powerhouse of deployment and manufacturing? As we’ll unpack later, this means we take a different approach to discussing results in this analysis as compared to the first electro-industrial cluster, focusing on the growth of clean resources over the next ten years.

In this note, we first identify next-generation geothermal power generation as an early-stage but promising technology and explain how it can play a critical role in this transition. Then, we zoom in on our study region, portions of the South-Central and Southwestern US, and demonstrate how this region is particularly well-suited to drive momentum for new geothermal deployment and manufacturing. We outline key policies that states can enact to seize this momentum and then quantify the energy systems and economic results of putting these policies in place.

The role for next-generation geothermal in the electro-industrial future

The case for an electro-industrial future is predicated on continued—and expanded—availability of low-cost, efficient sources of electricity (on the supply side) and low-cost, efficient processes to convert these electrons into valuable economic outputs (on the demand side). The lowest-cost source of electricity in most parts of the country today is some combination of solar, wind, and battery storage. These technologies have the added benefit of avoiding conversion losses inherent to fossil fuel consumption.

These commercially available technologies can provide much of the electricity generation needed to power the electro-industrial era—an average of 57% in 2035 in the National Lab of the Rockies’ 2024 Standard Scenarios main cases and as much as 80% of generation across all scenarios in 2050. There are lots of ways to manage these sources’ intrinsic variability, including demand flexibility and a robust transmission network build-out. But firm generating capacity (generators that are available when called on rather than relying on variable inputs like wind and sun) plays a critical role even in these high renewable futures, and a robust portfolio of grid resources can maximize reliability while minimizing cost.

Next-generation geothermal power generation has numerous advantages in meeting this demand for firm power. Today, effectively all of the 4 gigawatts of installed geothermal capacity in the US use conventional hydrothermal technologies, which rely on naturally permeable subsurface reservoirs that are limited in their geographic availability. By contrast, next-generation geothermal approaches, including enhanced geothermal systems (EGS), closed loop geothermal systems (CLGS), and superhot geothermal, do not rely on these specialized formations and can be built in a much wider range of locations. Some of these systems can also operate flexibly, further enhancing their value to the grid. Much more information on these different types of geothermal technologies can be found in the Department of Energy’s Pathways to Commercial Liftoff: Next-Generation Geothermal Power report.

Recent advances in geothermal drilling techniques have substantially driven down the cost of drilling the wells needed for these next-generation systems. Geothermal drilling also leverages a large, skilled workforce focused on oil and gas production, as we unpack in greater detail below. As a result, we’ve previously found that EGS in select locations has a levelized cost of electricity that can be cost-competitive with natural gas plants—the most widely available firm technology today. Geothermal costs are also locked in once constructed, while the cost of gas generation is subject to considerable volatility in fuel costs. Finally, geothermal is one of a handful of technologies that will continue to benefit from federal support through the early 2030s in the form of a federal clean electricity tax credit, helping to further drive down costs to utilities and consumers and bring federal dollars to the region.

Clean firm resources more broadly—firm sources of electricity that emit few if any greenhouse gases—are particularly of interest to governments and companies that have clean energy or climate targets. Next-generation geothermal has been a leading source of new deals to provide clean firm capacity to corporate buyers, with large data center companies like Google and Meta lining up behind new-build geothermal projects.

The turbine bottleneck

Scaling geothermal deployments to achieve their promise will also require scaling the supply chains of the components required to drill geothermal wells and produce power. Our partners at RMI conducted a review of the current state of play and found that the need to build out this supply chain will not only enable faster geothermal growth on the grid but can also be a major economic opportunity.

For this work, we focus on one key link in the supply chain that RMI identified: the turbines that turn the heat that geothermal wells produce from the subsurface into electrons. Geothermal power plants use three primary turbine types: dry steam, flash steam, and binary cycle. Dry steam and flash steam turbines are typically used in higher temperature geothermal reservoirs, whereas binary turbines can generate power from lower reservoir temperatures, making them well-suited for most EGS projects. Today, most geothermal turbine manufacturing occurs outside of the US, with production concentrated in countries such as Israel and Italy. Lead times for turbines delivered to the US typically range from 12-18 months, with roughly 3-5 months of this attributable to international shipping alone. Expanding domestic manufacturing capacity could meaningfully reduce these lead times and accelerate project deployment, an increasingly important consideration given the emphasis on quickly bringing new capacity online. A more robust domestic turbine manufacturing base would also help protect geothermal development from global supply chain disruptions, such as shipping lane disturbances from geopolitical conflicts, tariffs, and export controls. The US has some existing binary turbine manufacturing capacity; however, it is primarily for small-scale turbines used in waste heat recovery applications rather than larger turbines required for utility-scale geothermal power deployment.

Before the shale boom in the late 2000s reshaped energy markets, high oil and gas prices led to a wave of excitement around geothermal as an energy source. In turn, we saw an uptick in domestic investments in geothermal turbine manufacturing at this time. In the years since, the geothermal sector’s boom-and-bust cycles have made investors wary of committing capital to domestic manufacturing facilities, given the risk of stranded assets.

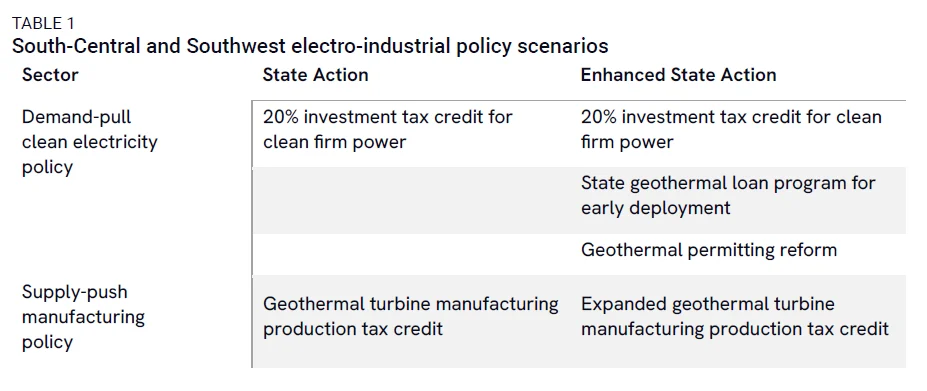

Reversing this trend will require a coordinated policy approach: supply-side incentives to encourage in-region turbine manufacturing, paired with demand-side measures to accelerate geothermal deployment. Together, these strategies can not only restore domestic manufacturing capacity but also position the South-Central and Southwestern US as a leading hub for geothermal turbine production.

The South-Central and Southwestern US can scale up geothermal

Our study region for this work consists of seven states across the South-Central and Southwest US: Arizona, Arkansas, Colorado, Louisiana, New Mexico, Oklahoma, and Texas. This region has already experienced meaningful changes to its grid and economy and, as we unpack in the sections that follow, these changes are likely to continue. Between continued expectations of rapid load growth, high-quality subsurface geothermal resources, a huge concentration of skilled workers in the oil and gas industry, and a history of turbine manufacturing, the region is a perfect place for state policymakers to make investments to develop a strong geothermal industry.

First, there is a growing need in the region for firm, reliable power. For at least the last 15 years, this region has experienced mostly steady annual electricity demand growth while national demand fluctuated from year to year. Because of these trends, regional electricity demand increased by 33% from 2010 to 2025 while national demand grew by only 8% over the same time frame. National demand growth trends have recently shifted: demand has increased consistently since 2024, and all signs point to sustained growth into the future. Yet, the South-Central and Southwest US region continues to see higher levels of demand growth than the national average. These states drove 27% of national electricity demand growth over the last two years, and we expect that they will account for about 30% of national demand growth from 2026 to 2035. This demand growth is largely driven by data centers (especially in Texas), the electrification of oil and gas production in the Permian Basin, growth in manufacturing of semiconductors and clean energy technologies, and population growth. Data centers in particular need constant access to reliable power, while both data centers and oil and gas operations require low-cost electricity. Meeting this growing power demand is critical to sustaining economic growth in the region.

The seven states in focus pair rising demand with ample geothermal resources. Unlike the neighboring states of Nevada, Utah, and California, these states have seen little geothermal growth to date (apart from a single conventional hydrothermal plant in New Mexico). However, the availability of next-generation geothermal technologies like EGS opens up much more of the country to geothermal development. Recent estimates from the Department of Energy find hundreds of gigawatts of potentially developable resources in states across the region (Figure 1).