New Data on the “Debt Trap” Question

We reviewed 40 cases of China’s external debt renegotiations to understand the broad patterns of outcomes.

The Belt and Road Forum took place last week, in a context of mounting pushback against Beijing’s signature foreign policy initiative. Debt sustainability concerns are at the center of current criticism, with the Sri Lankan example—where China assumed control of the Hambantota port—serving as a cautionary tale of the risks of reliance upon Chinese financing for infrastructure projects. We reviewed 40 cases of China’s external debt renegotiations to understand the broad patterns of outcomes, and to explore whether asset seizures as occurred in Sri Lanka are typical or exceptional. Key findings include:

- Debt renegotiations and distress among borrowing countries are common. The sheer volume of debt renegotiations points to legitimate concerns about the sustainability of China’s outbound lending. More cases of distress are likely in a few years as many Chinese projects were launched from 2013 to 2016, along with the loans to finance them.

- Asset seizures are a rare occurrence. Debt renegotiations usually involve a more balanced outcome between lender and borrower, ranging from extensions of loan terms and repayment deadlines to explicit refinancing, or partial or even total debt forgiveness (the most common outcome).

- Despite its economic weight, China’s leverage in negotiations is limited. Many of the cases reviewed involved an outcome in the favor of the borrower, and especially so when host countries had access to alternative financing sources or relied on an external event (such as a change in leadership) to demand different terms.

On April 25, the second Belt and Road Forum opened in Beijing, promoting Beijing’s flagship foreign policy plan, the Belt and Road Initiative (BRI). This second forum takes place in a very different setting than its previous edition in May 2017. Since that time, criticism has grown around Xi Jinping’s signature initiative, with a series of host countries delaying, renegotiating or even shelving projects with China, due to concerns around their sustainability. Japan, the EU, and the US have also formulated strong condemnations of the potential economic consequences of China’s external investment push, and are developing their own alternatives to Beijing’s plan.

Central to such criticism and to the recent pushback are concerns around debt sustainability within recipient countries. Most of China’s BRI projects are financed through China-sourced loans from policy banks, which some target countries can find difficult to repay, in some cases because of suspected inflation of project budgets or sub-optimal project planning. Sri Lanka’s decision in December 2017 to grant a 99-year concession to China on the Hambantota Port, and to agree to China Merchant Port Holdings acquiring 70 percent of the port’s operating company, serves as a cautionary tale of the dangers attached to countries’ overreliance upon Chinese financing. A slew of recent renegotiations of BRI projects highlights the fact that concerns about these excessive debt burdens are legitimate. This realization among recipient countries will likely constrain the growth of BRI-related loans in the future; acceleration of growth in Chinese outbound lending for BRI-related projects is probably off the table.

Until a more sustainable model for project financing is advanced by Beijing, key political and economic questions surround China’s handling of bad debt renegotiations, both now and in the future. Is the Sri Lanka case representative or an outlier? And what does the evidence show us for how China usually manages souring external loans?

Assessing Patterns in China’s Debt Renegotiations

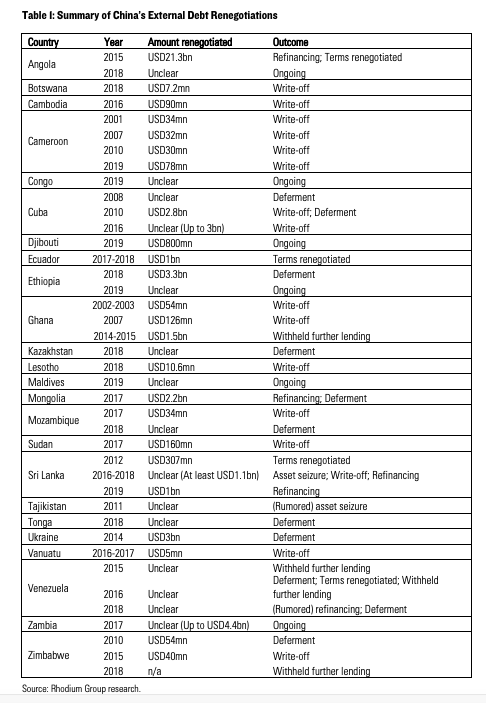

To answer these questions, we compiled the first available database of cases of Chinese external debt renegotiations. We focused on cases for which information was available through open sources. So far, we have found 40 instances of debt renegotiations across 24 countries, although this database is still preliminary, and we expect to discover more cases in the future. Most of these have occurred since 2007, but we also found a few cases from previous years. Altogether, these represent around USD50bn of renegotiated debt. For each of these instances, we sought to understand the events that triggered renegotiation, as well as to map the outcome of the process (deferment, forgiveness, refinancing, or another outcome). Results are summarized in Table 1 below:

Notable here is that we only cataloged loan renegotiations. We did not include within our analysis project term renegotiations, as have recently occurred between Beijing and Kuala Lumpur surrounding the East Coast Railway project. We also did not cover private loans. Instead, we focused on loans that involved a host government directly (either because it was extended to the government itself, or because it involved a government guarantee). In doing so, we uncovered a wide variety of loan types, including loans for specific projects (a railway in Ethiopia), credit lines extended for unspecified projects (a CDB credit line to Ghana), loans to national companies (Angola’s Sonangol), loans for budgetary items (as in Zimbabwe), and one foreign exchange swap line (in Mongolia).

While as extensive as possible, this effort is preliminary and we fully acknowledge its limitations: We are most likely still missing several cases of debt renegotiations, especially when these are less publicized within public statements or media (if not kept explicitly secret). We suspect we are missing at least two dozen cases of debt forgiveness, especially to African countries – as alternate studies, as well as official statements from Chinese leaders, mention many more cases than what we could triangulate through open sources.[1] This discrepancy is mitigated by the fact that these cases of debt forgiveness most often represent small amounts, as detailed below. We also had to account for poor or incomplete reporting through open sources, although we confirmed the data to the extent possible with additional research.

Preliminary Findings

Though still incomplete, this initial assessment of China’s external debt renegotiation outcomes highlights a series of illuminating findings:

First and foremost is the realization that actual asset seizures are a very rare occurrence. Apart from Sri Lanka, the only other example we could find of an outright asset seizure was in Tajikistan, where the government reportedly ceded 1,158 square km of land to China in 2011. However, the limited information available, and the opacity of the process makes it difficult to determine whether this specific land transfer case was in exchange for Chinese debt forgiveness, or (as some observers argue) part of a historical dispute settlement between the two countries. Another caveat is that we are not considering cases such as loans to Kenya or Montenegro where port and land collateral are rumored to be explicitly part of bilateral loan contracts.

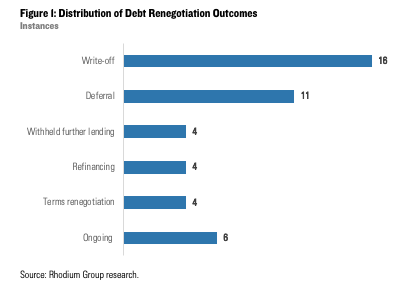

Instead, we find those debt renegotiations usually involve a more balanced outcome between lender and borrower, ranging from extensions of loan terms and repayment deadlines to explicit refinancing, or partial or even total debt forgiveness (see Figure 1). Among these outcomes, we find that write-offs are the most common outcome (16 cases), followed by deferments (11 cases), and refinancing, term renegotiations, and denials of additional financing (4 cases each). Six of the renegotiation processes covered by our data were still ongoing, with no specific outcome yet available.

Although the most common renegotiation outcome, explicit write-offs of debts usually involve very limited amounts. Besides the case in Cuba, where China wrote off between USD5.0 and USD 5.8bn of debt, forgiveness cases range from USD5mn (Vanuatu) to USD160mn (Sudan) and usually represent a mere fraction of the total amount due to China. For Sudan for example, the forgiven USD160mn in 2017 represented only 2.5% of the country’s estimated USD6.5bn owed to China, according to data made available by Johns Hopkins, China Africa Research Initiative.[2] In addition, most of these debt forgiveness cases were accompanied by additional lending in significant volumes. For example, when Beijing wrote off USD7mn of Botswana’s debt at the Forum on China-Africa Cooperation last year, Chinese leaders allegedly offered as much as USD1bn in new infrastructure financing to the country. This means that cases of forgiveness rarely serve to reduce a country’s indebtedness to China.

Interestingly, write-offs are often conceded by Beijing without a formal renegotiation process. Instead, Beijing usually unilaterally agrees to cancel part of a borrowing country’s debt, even when there are few signs of financial stress on the part of the borrower. Such cases of debt forgiveness are therefore probably used to signal support to the recipient countries, and improve bilateral relations.

Yet a few write-offs were also conceded in cases of acute financial distress within the host country: USD2.6bn of Cuba’s debt in 2010, about USD40mn of Zimbabwean loans in 2015, and an undisclosed part of Sri Lanka’s debt to China in 2017-2018 (which also included control passed to China for to the Hambantota port). Forced or constrained, these write-offs were often accompanied by a decision on the part of Beijing to withhold further lending. This was notably the case in Zimbabwe, where Beijing rejected Harare’s calls in 2014-2015 to finance a USD1.5bn rescue package. This also constituted part of Beijing’s response to Venezuela’s recent economic woes.

Negotiation outcomes are more diverse where financial stress proves more manageable. Beijing has repeatedly agreed to a mix of repayment deferments and some degree of refinancing (as in Mongolia in 2017), although often under harsher terms (as in Angola in 2015, or Sri Lanka in 2012). And where external events such as changes in leadership, or large movements in commodity prices, prompted renegotiations, Beijing was often compelled to agree to term renegotiations, usually to borrowing countries’ advantage (Ecuador in 2017-2018, Ghana in 2014-2015).

What drives different outcomes in debt renegotiations?

The multiplicity of outcomes raises questions about the key determinants of negotiation leverage and decisions, particularly given the wide variety of settlement conditions, from asset grabs (possibly the least favorable outcome for the borrower) to constrained write-offs and deferments (possibly the most favorable outcomes).

Several factors appear to influence renegotiation outcomes. First and most important is the availability of alternative financing sources. In renegotiations in Ghana, Mongolia or Zambia, alternative channels of financing such as the IMF or international capital markets (Eurobonds) were available, which likely created more leverage among borrowers for renegotiation of terms with China. In comparison, Sri Lanka’s indebtedness was so high in 2016-2017 that this likely prevented the government from turning to other financing partners for relief. This might explain why renegotiations produced more favorable outcomes for borrowers in the first three cases.

Another key factor seems to be the leverage generated by leadership changes in borrowing countries, which allows incoming governments to start renegotiations with stronger negotiating influence, and hence a real ability to demand a change in terms. In the case of Ecuador, the new government demanded and obtained a renegotiation of lending terms, arguing that its predecessors had agreed to unfair conditions that were no longer tolerable. The current negotiation with Angola might see similar negotiating power accumulating in Luanda.

In addition, we find that resource-backed loans are not an element of leverage for Beijing, and in fact do not necessarily represent a strong guarantee against repayment problems. The case of Venezuela is an obvious illustration of the limited guarantees provided by oil-backed financing. But the lesser-known Ukrainian case is also telling in that respect. Though its loan was backed by grain shipments, Beijing had to ultimately turn to international arbitration to resolve its dispute with Kiev, who consistently failed to provide the required volume of annual grain shipments to repay its loan. Beijing has no means to seize these grain shipments by force. In addition, the Ukraine case shows that despite China’s size and growing international economic clout, its leverage in some of these cases remains quite limited, even in disputes with much smaller countries.

Past Performance Not Indicative of Future Results

While these are the first findings from this bottom-up catalog of 40 cases of China’s external debt renegotiations, and they do suggest meaningful patterns in the risks from China’s outbound lending, additional caveats are appropriate.

First, it remains unclear whether these patterns will persist in the future. As China’s global economic clout expands, one possibility is that external loans will involve stricter conditions for borrowers. Or, on the contrary, in the wake of international criticism, Beijing may prove less inclined to demand repayment terms involving asset seizures or unsustainable mitigating conditions.

Second, it is probable that borrowers will notice one another’s renegotiation outcomes, and start pushing back on Beijing more forcefully for similar favorable conditions, or avoiding costly termination clauses (as in the recent Malaysian case). If anything, the Sri Lankan case serves as a cautionary tale of the danger of borrowing too much from China. This is also one of the arguments advanced by countries such as Zambia, Myanmar or Sierra Leone in their efforts to cancel or at least scale down Chinese projects.

Third, beyond asset seizures, Beijing could still use loan renegotiations to advance foreign and domestic policy objectives. Vanuatu’s debt renegotiation was surrounded by rumors about the island being encouraged to embrace Beijing’s South China Sea stance, and Tajikistan’s debt woes in 2011 were in fact followed by a wave of infrastructure and energy contracts attributed to Chinese companies in the country. These unspoken or indirect outcomes of renegotiations are much harder to trace and properly assign but may be a critical part of political agreements between Beijing and borrowing countries.

Finally, many more renegotiations should emerge in the near future. Many Chinese projects started recently, along with the loans to finance them. As a result, many more projects and bilateral loans may face distress in a few years. Key cases to watch include loans to Pakistan, Turkmenistan, Djibouti, Montenegro or Kenya, among others, which we would expect to start renegotiations soon. In addition, the high and growing levels of indebtedness among African recipients is paving the way for a new round of renegotiations. Such cases will have to be monitored closely.

At the very least, the large number of debt renegotiations seen so far will likely serve as a brake on the narrative of accelerating Chinese outbound lending along the Belt and Road. Beijing itself may grow skittish about lending additional sums to distressed borrowers. Recipient countries may borrow more, but only after existing debt burdens are resolved more favorably. More fundamentally, Chinese external lending will probably slow from current levels rather than accelerate, given the financial stress highlighted by this pattern of Chinese debt renegotiations.

Notes

[1] Chinese premier Wen Jiabao said in his 2010 UN Millennium Challenge speech that China canceled debt owed by 50 heavily indebted poor countries (HIPCs) and least developed countries (LDCs) worth 25.6 billion yuan as of 2009, and would cancel more in 2010. However, we do not know what countries were involved in this debt forgiveness plan. Similarly, in 2018 Xi said China would write off some interest-free loans to Africa’s poorest nations during the Forum on China-Africa Cooperation, but the full list was not made available.

[2] Johns Hopkins School of Advanced International Studies, China Africa Research Initiative, http://www.sais-cari.org/data.