Nuclear Energy Renaissance: Are We There Yet?

We discuss why now may be the best time in decades for new nuclear energy in the US and what needs to happen for nuclear power to really take off.

Excitement about nuclear energy in the United States is soaring amid increasing energy demand and data center buildout, bipartisan congressional support, and a strong appetite from the Trump administration. Nuclear power is a potentially multitrillion-dollar market opportunity, which has stutter-stepped before. In this note, we discuss why now may be the best time in decades for new nuclear energy and what needs to happen for nuclear power to really take off in the US.

Recent restarts of nuclear plants that were shut down for economic reasons are an early indicator of potential new power plant development. But more needs to happen to fully realize a nuclear renaissance in the US. We identify actions that can support momentum for nuclear scale-up, including developing a book of orders for a single power plant design. This can lower costs through repetition as supply chains ramp up. In addition, there are policy mechanisms that can help mitigate risk for the first wave of power plants, including siting and permitting reform, expanding domestic market opportunities for nuclear energy, narrowing the field of reactor options, and developing a pathway for the diffusion of US nuclear technology abroad.

Is this the new moment for nuclear energy?

Recent news and company press releases have been filled with announcements about developing new nuclear power plants. The Trump administration has announced a slew of investment pledges from other countries, notably up to $550 billion from Japan, with some of this potentially earmarked to pay for the US government’s recent $80 billion partnership with companies to build new reactors. The Trump administration also set a goal of quadrupling nuclear capacity from roughly 100 GW today to 400 GW by 2050, and to have ten new large reactors with complete designs (as opposed to incomplete designs before construction, which often lead to delays) under construction by 2030.

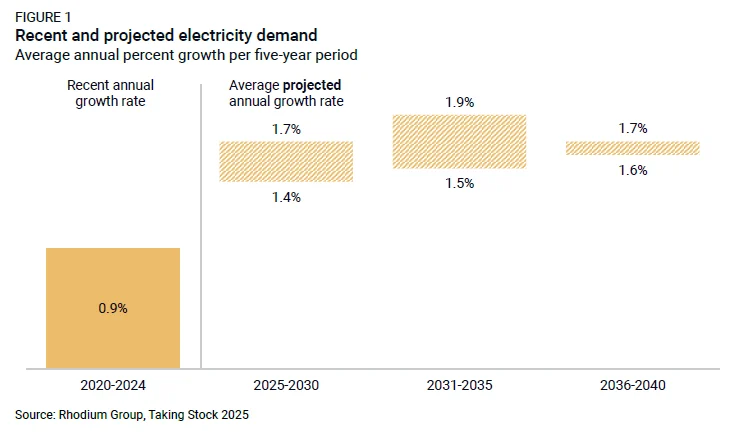

At the same time, US electricity demand is projected to grow rapidly for the first time in decades (Figure 1), partially due to data centers. As multi-billion-dollar deals for AI infrastructure buildouts proliferate against a backdrop of intensifying US-China AI competition, speculation is growing about whether the US has the capacity to power the ~80 GW of peak demand from data center growth planned for 2030. The US will need more electricity from as many categories of supply as possible to meet this demand. This provides an entry point for new nuclear, but building new nuclear plants in the US is currently very expensive. Is it enough to spark a wave of new development? We think more actions are needed to see new nuclear reactors built at scale in the US. Still, several current indicators, such as increasing electricity demand, are similar to the environment in which the first wave of nuclear power took off in the US.

The first wave of US nuclear followed surging electric demand

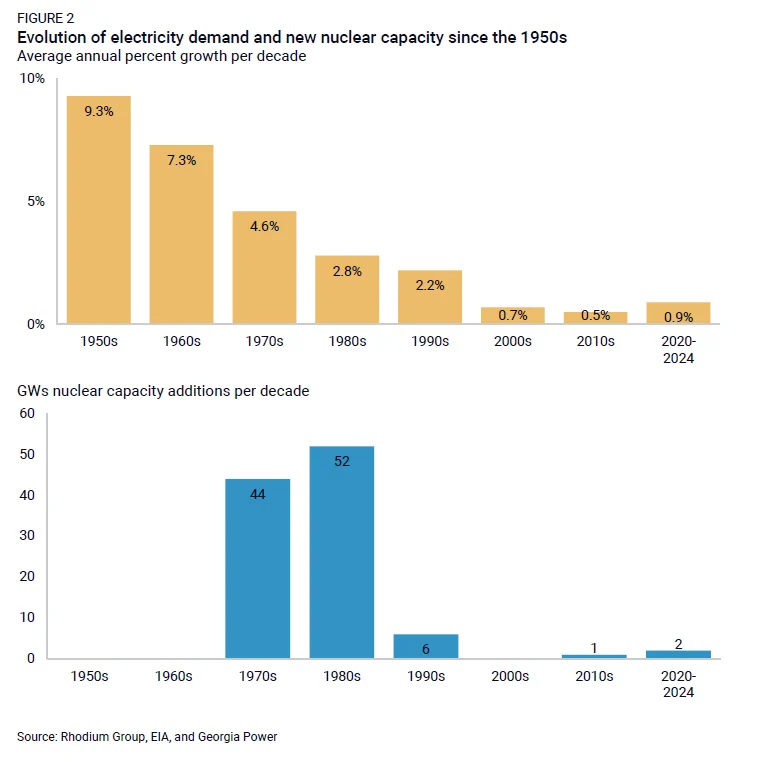

Following World War II and President Eisenhower’s “Atoms for Peace” speech in 1953, US national labs and the private sector rapidly scaled up civil nuclear energy. In the 1960s, the US nuclear power industry experienced rapid growth, as utilities viewed nuclear electricity generation as economical, clean, and safe. However, deployment and innovation started to sputter in the mid-1970s as electricity demand growth slowed (Figure 2), coinciding with the emergence of reactor safety and waste disposal issues. While there were no detectable health effects on plant workers or the public, the 1979 partial meltdown of one reactor at the Three Mile Island (TMI) plant exacerbated concerns.

New nuclear orders dried up in the following years, with no new plants built until the 2010s. Accidents at Chernobyl in 1986 and Fukushima in 2011 piled on to concerns. Lessons learned from these accidents and technical advancements improved safety in the next generation of designs, including the Generation 3+ utility-scale AP1000, which received its original design certification in 2006. Additionally, in response to these accidents, the US Nuclear Regulatory Commission (NRC) expanded its licensing requirements—one of many factors contributing to the increasing economic costs of building new reactors in recent decades.

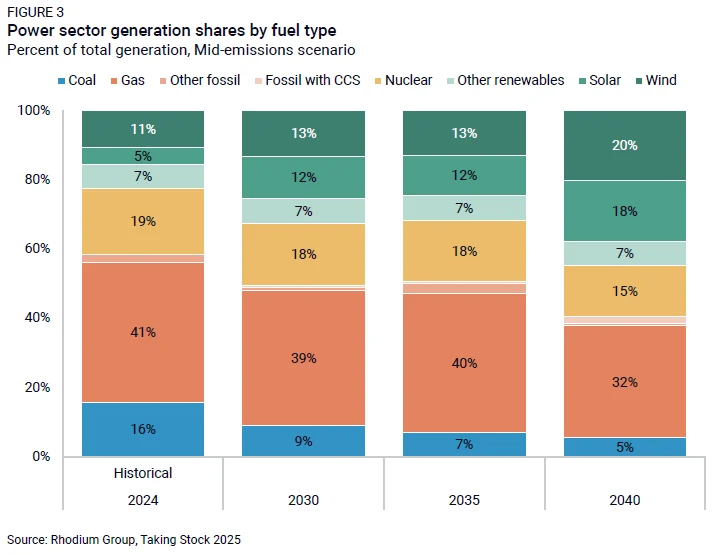

While the US currently has 94 operating reactors (representing ~19% of US electricity generation), their average age is over 40 years, and retirements loom, putting nuclear generation capacity at risk. Previous Rhodium modeling shows nuclear’s share of total generation falling in 2040 compared to both 2024 and 2030 (Figure 3). This is due to both market conditions (cheap natural gas) and the expiration of the zero-emission nuclear power credit after 2032—problems that new nuclear will also face and that Rhodium has pointed out for nearly a decade.

What’s different now?

Several dynamics have shifted in recent years, which, when taken together, may mean this is the best time in decades for nuclear energy in the US.

Project delivery learning: The last two nuclear plants to enter commercial operation in the US, Vogtle 3 and 4 in Georgia, went into operation in 2023 and 2024, coming in more than $16 billion over estimate and seven years late. These astronomical costs and schedule overruns rattled investors. To date, they represent the first and only US deployments of the AP1000 design. First-of-a-kind projects almost always cost more than initially planned. That said, the construction timeline was cut by 50% between units 3 and 4, demonstrating project delivery improvement and workforce development from volume that could benefit new projects.

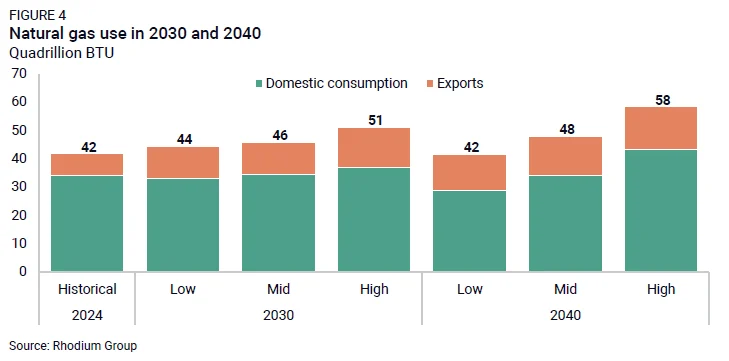

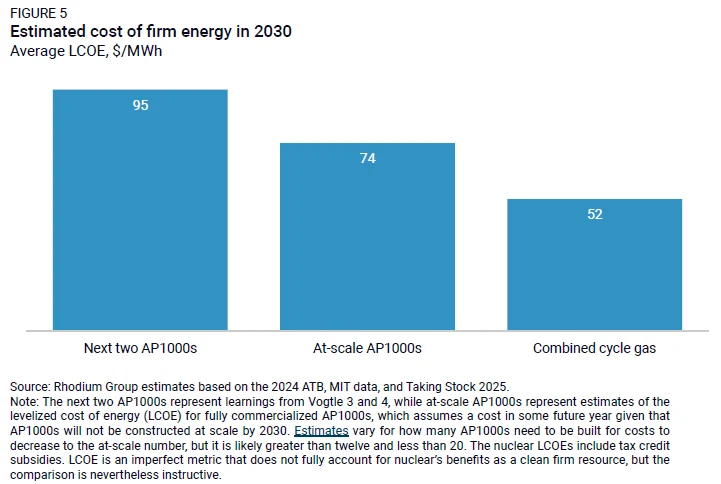

More favorable market conditions for nuclear: Several additional indicators are creating tailwinds for the deployment of nuclear power at scale. Energy demand is increasing at a rate not seen in decades, driven by a combination of electrification, data center expansion, and manufacturing needs (Figure 1). Access to electric power is one headwind for building data centers and is a reason why hyperscalers are becoming increasingly interested in the energy grid. Reduced subsidies or increased costs for competing technologies are also creating more favorable conditions for nuclear power. The One Big Beautiful Bill Act, passed this summer, removes tax credits for wind and solar over the next couple of years, while nuclear retains its tax benefits through 2032. Natural gas generation costs are likely to become more volatile due to increasing LNG exports (Figure 4) and order backlogs for gas turbines. By 2030 (the very earliest for any new large-scale nuclear to connect to the grid), the cost of AP1000s has the potential to be competitive with other firm power. We also acknowledge the potential for nuclear costs to decline if deployment ramps up in the following decade, perhaps approaching the cost of combined cycle gas (Figure 5).

Demand for more energy options: Meeting surging electric demand in the US should be easier with more options for supply—not just more of what’s off the shelf (wind, solar, natural gas). That’s one reason why large electric buyers are exploring advanced nuclear, geothermal, next-generation storage, and even fusion technologies to generate power at scale. Advanced nuclear is particularly attractive because it is a highly energy and land-dense option, meaning it generates outsize power relative to its fuel and land requirements. Diversifying supply chains with nuclear power is also crucial in the face of increased geopolitical risk (e.g., China cornering the solar market) and order backlogs for specific components. At the same time, while nuclear waste can be mostly managed in interim storage at nuclear facilities, a long-term geologic repository for waste will be important if and when nuclear power scales up.

AI innovations: AI innovations could also accelerate nuclear deployment by helping to analyze the vast amount of information generated by nuclear operations for regulatory compliance, fuel cycle optimization, and safety enhancement. This is already in action at a nuclear plant in California. The NRC could use AI to digitize some of its records and streamline processes. Both nuclear developers and operators can utilize AI to reduce costs and extend plant lifetimes by refining reactor designs, predicting performance, and adjusting power output in real-time to optimize efficiency.

Shifting political and public support: Public support for nuclear is also on the rise. Six-in-ten US adults support nuclear power, according to a recent survey—a major shift since 2020, when there was greater opposition than support. In Congress, the ADVANCE Act was passed in 2024 with overwhelming bipartisan support (88-2 in the Senate and 393-13) to modernize nuclear licensing and regulation at the NRC. The Trump administration is quite bullish on nuclear energy, with an Executive Order calling for a quadrupling of nuclear energy capacity by 2050. That equates to an additional 15 GW per year every year from 2030 to 2050 or nearly triple the fastest annual deployment pace the US achieved during the 1980s. Recent comments from Secretary Wright emphasize that, during the Trump administration, the Department of Energy’s Loan Programs Office (LPO) will predominantly fund nuclear power. During his first term, the only time President Trump used LPO authority was to finance the Vogtle 3 and 4 reactors.

Despite all these promising signs, there are still formidable barriers to scaling up nuclear energy. We discuss below the current state of play for nuclear power in the US—both some positive initial actions and the challenges that remain.

A huge market opportunity, but where are we currently?

Quadrupling US nuclear capacity by 2050 could represent a one- to two-trillion dollar opportunity. Large-scale reactors, such as the AP1000, are expected to remain central to this strategy, particularly as large loads like data centers continue to drive growth in demand.

The same headwinds mentioned above for new nuclear have been pushing existing nuclear out of the market over the last decade: low natural gas prices, slack demand (Figure 1), and subsidized renewable energy. However, some of these factors have now changed, and some plants are being resurrected. Hyperscalers have recently inked deals to resurrect 1.5 GW of closed plants. In addition, the restart of the Palisades (805 MW) plant in Michigan is nearing completion and is on track to be the first US nuclear plant to come back from retirement, despite a last-minute lawsuit from environmental groups. Negotiations are also underway to restart construction of two abandoned AP1000s at the VC Summer site.

However, there are few, if any, additional opportunities for more power from existing nuclear plants beyond these restarts. Increasing electricity output from existing plants through uprating upgrades could bring ~3 GW of new capacity online by the mid-2030s. Beyond restarts and upgrading existing plants, there’s a third option for adding capacity that hasn’t gotten as much attention until recently: the possibility of building new AP1000s and small modular reactors (SMRs). The most significant development on this front is the US government’s announcement of an $80 billion partnership with companies to build up to ~8-10 GWs of new AP1000s, as mentioned earlier, with investment from Japan possible.

Cost overrun risk challenges new utility-scale nuclear builds

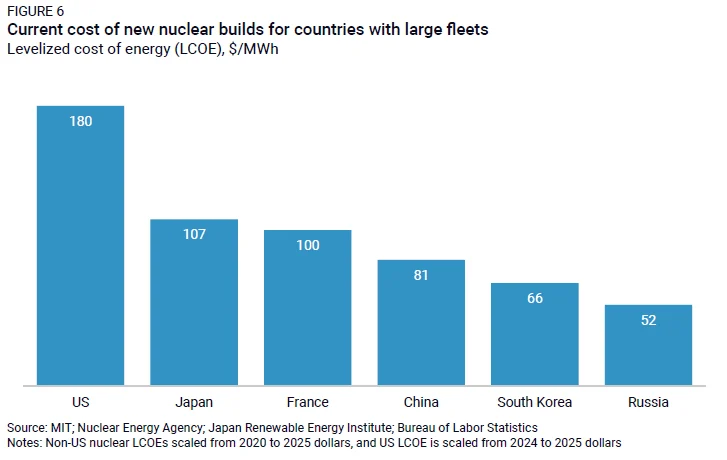

However, building new utility-scale nuclear plants is currently very expensive. The levelized cost of energy (LCOE) for new nuclear energy in the US is higher than in other countries (Figure 6). While developers of large loads like data centers may be willing to pay a premium for firm generation, utilities are generally unwilling and unable to put this type of financial risk on their balance sheets. Other countries with cheaper nuclear have driven down costs through tighter project delivery (a Korean team built four units on time and on schedule in the UAE) and sufficiently large orderbooks (repeated builds of the same reactor type lowering costs).

Big power buyers and utilities also have other supply options that are currently cheaper than new nuclear. As discussed above, if AP1000s continue down the cost curve, they could be cost-competitive with other clean firm power in the 2030s and potentially approach higher-end estimates of natural gas combined cycle (Figure 5) towards the end of the decade. But as things currently stand, the economics of building new large-scale nuclear over other energy options doesn’t pencil out in the US as it does in other countries, without additional policy support and project delivery improvements.

Expanding the solution set with small modular nuclear reactors (SMRs)

While cost challenges exist for building large-scale reactors in the US, not every new demand need requires a 1 GW AP1000. Innovators are expanding the nuclear solution set through the development of SMRs. SMRs of 75-350 MW per unit are generating significant enthusiasm. While first-of-a-kind costs will be high for any SMR, estimated capital costs overall are lower than for an AP1000, and revenue from early units can start to come in while subsequent units are built. SMRs also use fourth-generation nuclear technology, which is safer and more efficient. However, none are yet commercially deployed in the US, and only four are worldwide. As a new technology, SMRs have less developed supply chains. Most rely on a different fuel than what the traditional nuclear fleet uses, which adds to these supply chain challenges. Nonetheless, SMRs are another option for expanding nuclear capacity and are generating substantial enthusiasm in the private sector and for military applications but are not yet commercial in the US.

What needs to be true for nuclear energy to scale up?

The Department of Energy estimates that nuclear reactors will need to cost about $3,600/kW to be built quickly and scaled around the country, while the two units at Vogtle came in around $11,000/kW, three times that amount. Currently, the financial risk associated with new nuclear builds is too significant for most investors’ and utilities’ appetites and balance sheets. Assuming US electric demand continues to climb, structural changes to nuclear procurement, policy, and regulation, as well as shifts in energy markets, have the potential to get new nuclear on track for scale up. In this section, we outline some of these changes.

Building a US orderbook

Real concrete deals for orderbooks (repeated builds of the same reactor type) at scale are essential to justify supply chain ramp-up and drive costs down. Orderbooks need not come from only one project sponsor, and indeed likely won’t, to better share risk. This could involve demand aggregation at the regional level, aligning hyperscaler energy needs, political will, and utility realities to form demand signals that unlock additional private capital. The Northwest/Intermountain West or Southeast regions of the US are promising possible early movers.

In addition to the high-level trade deals recently announced, actual investments from Japan, Saudi Arabia, or others with deep pockets and nuclear ambitions would send a clear signal about building real orderbooks of nuclear power plants. Combining this with partnerships with companies that have extensive expertise in nuclear energy project delivery would provide a stronger indication of systemic change, especially since, during the first Trump administration, significant announcements about reshoring manufacturing through investments did not materialize.

The US currently lacks a domestic supply chain for the fuel type that many fourth-generation SMRs rely on. Orderbooks of AP1000s and SMRs that use more conventional fuel could accelerate the initial deployment of new nuclear power at scale.

Cutting risk for the first wave of projects in the orderbook

Cost overrun backstops provided by the government for the first or first few projects would help minimize private sector risk, promote learning, and maintain developer skin in the game through a cost-sharing agreement. Senator Risch’s Accelerating Reliable Capacity Act from the last Congress provides one framework for doing this, albeit with limited funds. Other proposals could be used in tandem, such as one that reduces interest rates through credit subsidies when project milestones are achieved on time.

Another possible model is that the US government builds, owns, and transfers completed plants to buyers to mitigate risk, a strategy that other countries have successfully employed to expand their nuclear fleets. The $80 billion announced partnership could lead in this direction. A government power purchase agreement backstop could also provide revenue certainty and leverage existing demand for nuclear power.

Siting and permitting reform

Both Democrats and Republicans agree that a reform push to accelerate the siting and permitting of energy infrastructure is essential, but differences in their priorities have historically derailed these conversations and could do so again. Absent a major permitting change and transmission grid build-out, an emphasis on existing or retired coal plant sites for new nuclear builds would streamline the siting and interconnection process.

Expand the map of where nuclear is welcome

Historically, many states have prohibited the development of new nuclear plants. That appears to be changing with states lifting moratoria and implementing new policies to attract nuclear. For example, in October, Illinois lifted its moratorium on new nuclear builds—we’ll be watching for more states to do the same (eleven states still have restrictions against the construction of new nuclear facilities on the books). The New York Power Authority has also recently launched a new initiative to develop 1 GW of advanced nuclear energy there.

Narrow the field of designs

There are currently over 125 different SMR designs plus the AP1000 design. Nuclear power plants are similar to airplanes: the market has space for a few different models for different use cases (like Boeing versus Airbus and a couple of smaller-scale options). The current proliferation of reactor models dilutes available public and private funding and focus. It is also hard to scale up supply chains for more than a handful of designs. The recent announcements focusing on AP1000s are promising for narrowing down the field of commercial reactor design types towards a few that the Department of Energy and private sector can coalesce their resources around.

Set the stage for global diffusion of US nuclear

US nuclear technology can further scale through deployment to markets around the world. This will require federal support. Both the Development Finance Corporation and the Export-Import Bank are up for congressional reauthorization in the next year, and fine-tuning these organizations and others like the Millennium Challenge Corporation can better support nuclear energy. One possibility is extending the EXIM loan length to better match the lifetime of nuclear plants (15–22-year current loan lengths versus at least 30 years, given that nuclear plants can operate for 60-80 years).

Other legislation making its way through Congress, such as the International Nuclear Energy Act, which is included in this year’s national defense bill, would promote the development of a nuclear export strategy. While key details are still emerging, the recently announced civil nuclear energy cooperation declaration between the US and Saudi Arabia is useful for countering Russian dominance in the global nuclear export market. It simultaneously raises geopolitical questions in the Middle East, including whether this paves the way for Saudi Arabia to develop a nuclear weapon and whether this will prod Iran into completing its nuclear weapons capability.

Who would benefit from a true nuclear renaissance?

With the deployment of utility-scale nuclear energy, hyperscalers, industrial users, and other large load customers would benefit from a realized nuclear energy renaissance. Long-term, clean, firm, and reasonably priced nuclear power, driven by cost reductions from project repetition, could contribute to providing reliable and affordable electricity across the US and potentially overseas. However, while many things are going right for nuclear, more needs to happen to achieve a true nuclear renaissance.