The Mountain is High, the Lead Investor is Far Away

The allocation of capital for China's industrial policy—be it direct grants, credit, or PE-VC investment—does not necessarily follow the objectives announced in Beijing policies.

At the Third Plenum in July this year, the Chinese Communist Party pledged to increase support for strategic and emerging industries, reaffirming its commitment to innovation-led economic growth. But the financial resources underpinning Beijing’s industrial policy are heavily constrained by China’s economic slowdown. Beijing is striving to better allocate the fewer resources it has to make its industrial policy more efficient.

In this note, we comb through available data on China’s industrial policy funding to analyze the outlook for industrial policy financial support. The allocation of capital—be it direct grants, credit, or PE-VC investment—does not necessarily follow the objectives announced in Beijing policies. Decades of misdirected investment make it hard for financial actors to now channel their resources to more productive sectors and firms, creating tension between central government wishes and the needs of the financial sector. Beijing wants them to allocate more capital to small companies and emerging technologies, but they need to play it safe by funding large, established players and delaying losses in sectors affected by high overcapacity.

Limited direct grants channeled to fewer champions

Financial support is not the sole mechanism of Chinese industrial policy, but it plays a crucial role in innovation outcomes. In addition to companies’ revenues, the main pillars of China’s innovation financing ecosystem include fiscal funding (such as direct grants to companies), bank credit, and private equity and venture capital (PE-VC) investment. Last year, we argued each of these sources is heavily affected by slower growth, and a tighter fiscal environment in China will likely force the government to channel funding more strategically (See “Spread Thin: China’s Science and Technology Spending in an Economic Slowdown”).

So has that strategic channeling happened? The most recent data on all three sources suggests not. In fact, instead of pushing financial actors to allocate funding more effectively, capital continues to flow into “safe” areas: Industry giants, SOEs, and industries where China already holds a dominant global position, such as batteries and solar.

Some of these “safe bets” are established players, such as BYD, that attract funding because they are perceived as lower risk with predictable returns. But much of the favored allocation results from local government incentives to preserve unprofitable actors—especially SOEs and heavy industries such as steel—that are inefficient and already suffer from overcapacity. Consequently, the financial system is now hindering China’s short-term and long-term growth by weakening future productivity growth rather than supporting it.

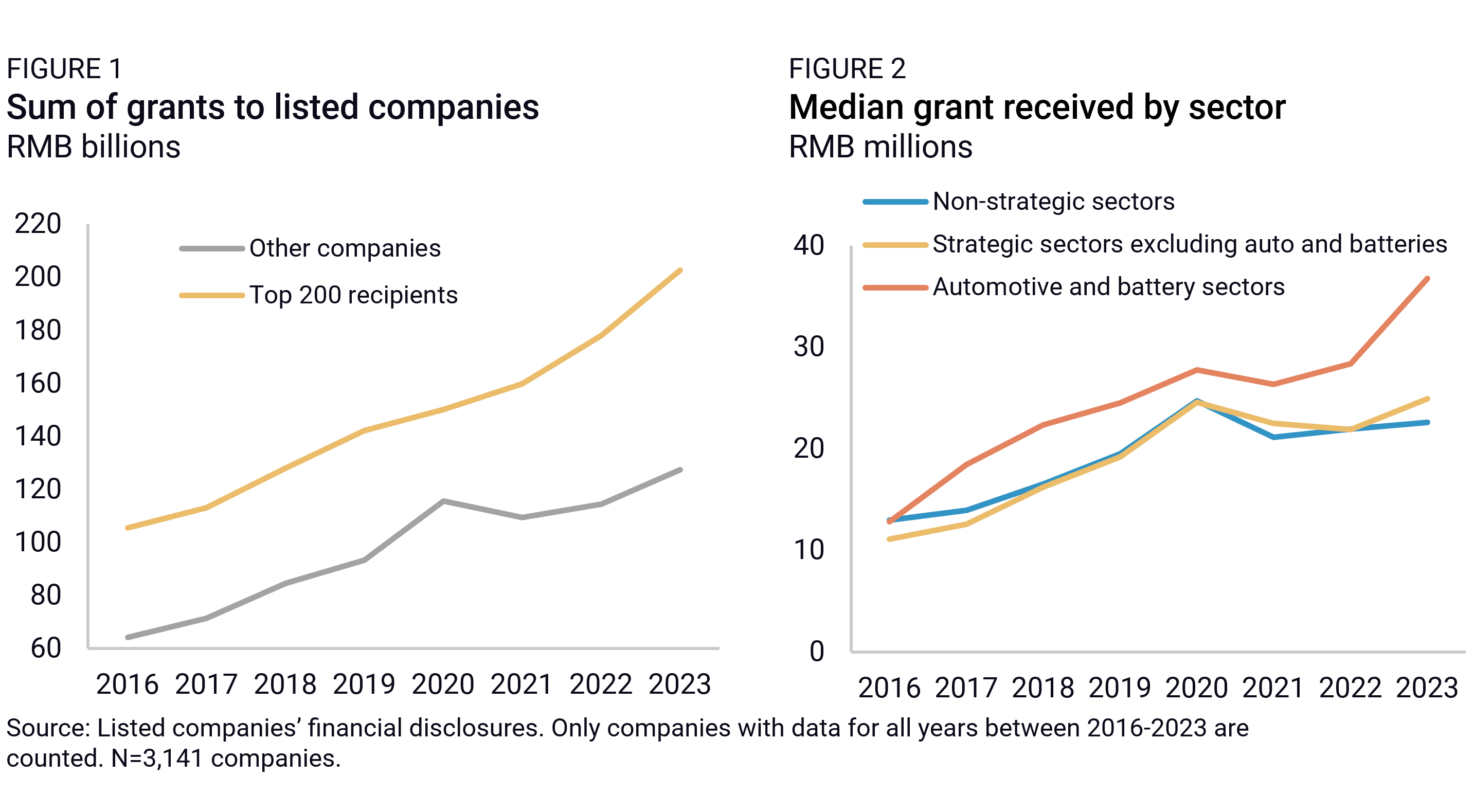

Take government grants to listed companies.1 While the 200 largest recipients continued to receive rapidly increasing amounts, grants to the other 2,941 companies grew at much slower levels than before COVID-19 (Figure 1). Strategic industries targeted in policy documents did not receive more grants than non-strategic industries, on average—with some exceptions like batteries and autos (Figure 2). In fact, even sectors considered highly strategic, like semiconductors and pharmaceuticals, have seen stagnating levels of median government grants over the past three years.

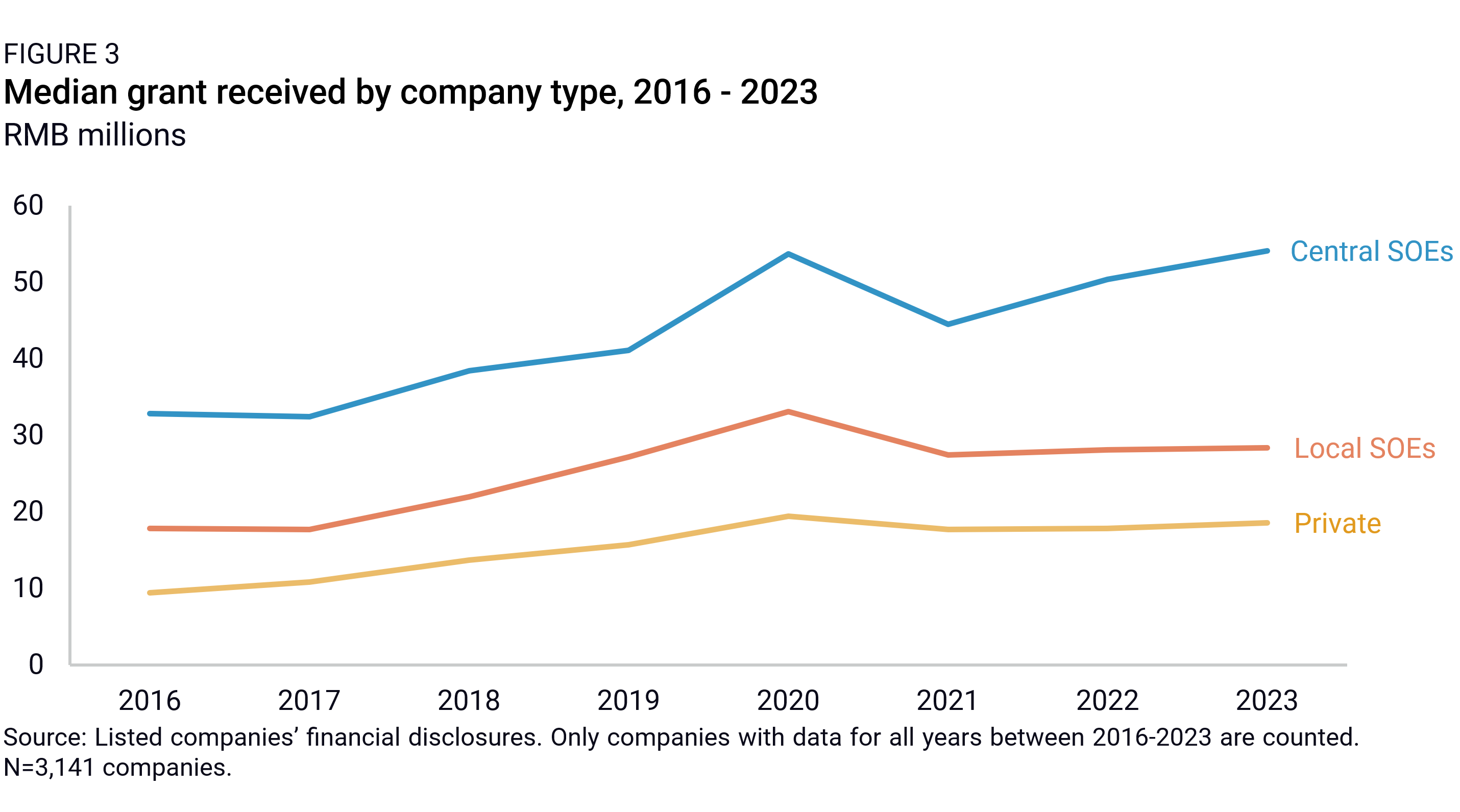

On the contrary, much of the increase in government grants to listed companies between 2022 and 2023 was concentrated in China’s struggling industrial and logistics behemoths, including China’s airlines and logistics sector, as well as mining, metallurgy, and other heavy industry companies. As Beijing has placed renewed emphasis on the role of SOEs in driving economic growth, they have also been receiving growing grants, while median grant amounts for private firms stagnated after 2020 (Figure 3).

This widening gap should be concerning to Beijing. The Chinese government has repeatedly emphasized the need for more inclusive industrial policy funding and sought to strengthen fiscal support for smaller companies, which are often the primary drivers of creativity and technological advancement. In recent years, new programs targeting smaller firms, like the “Little Giants,” marked the emergence of an “accelerator state” strategy linking the success of smaller, innovation-driving firms to economic growth. But the reality of grant allocation goes against that high-level strategy.

Two likely connected factors are driving this growing concentration of grants in large companies, SOEs, and a few sectors like electric vehicle (EV) batteries. First, local governments may be increasingly risk-averse when disbursing grants. As their budgets become more tightly constrained, they feel pressure to “bet on the right horses” and make safer choices as a result. Second, as China’s economy slows down, local governments may feel the need to support the biggest employers and drivers of local growth, which often are large companies and SOEs.

Bank credit, too, is concentrated in fewer actors

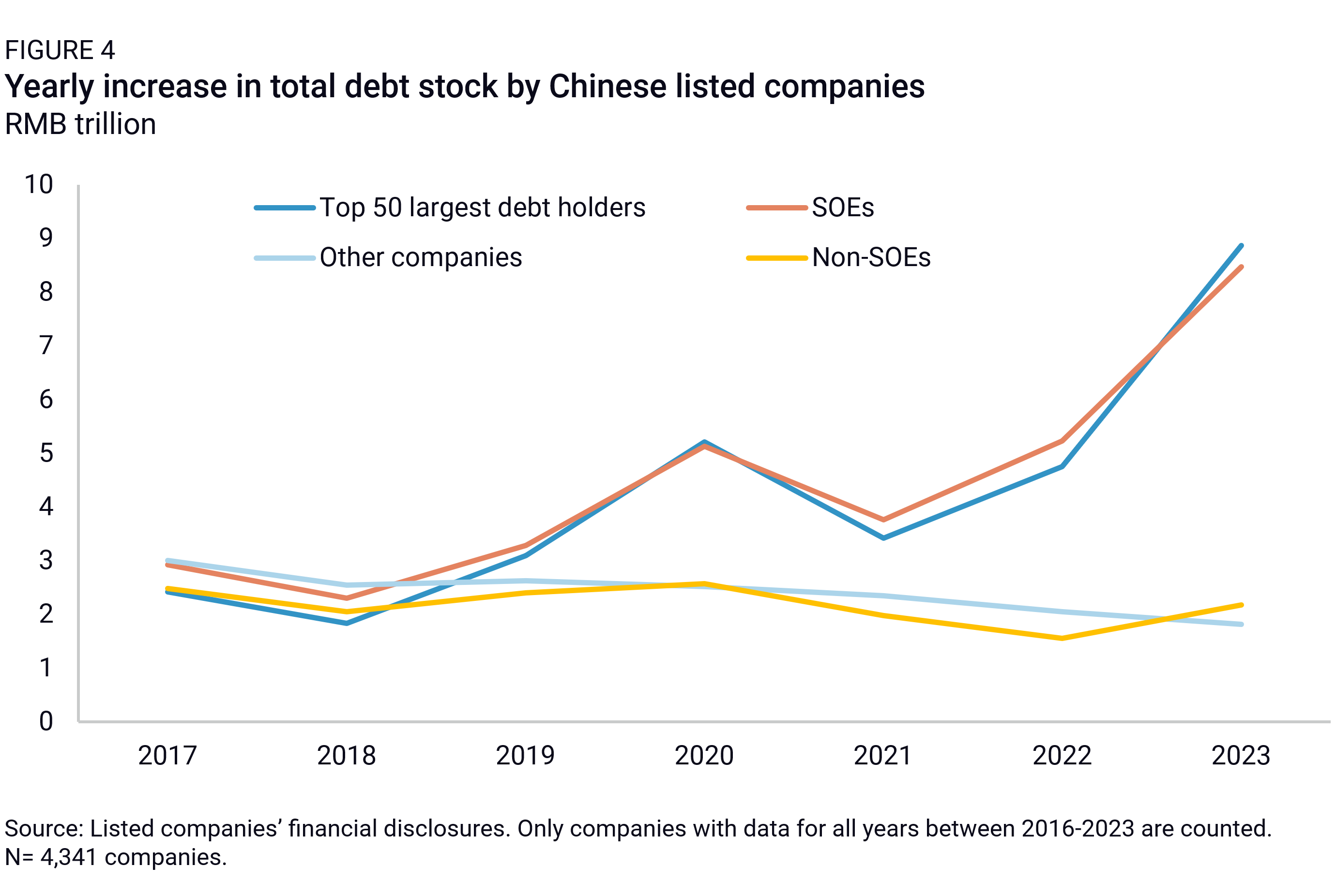

Faced with growing fiscal constraints, governments are asking banks to step up their role in funding China’s industrial policy. Beijing needs banks to lend to sectors and firms that can more efficiently fuel innovation and economic growth than the industries that were prioritized in the past. But decades of misallocation—with credit flowing mostly to legacy industries and SOEs—make changing patterns of lending difficult, particularly in a context of slower economic growth. Our data shows that while total amounts continued to grow, banks chose to pile in on the largest borrowers—often SOEs—rather than allocate credit more efficiently (Figure 4).

This is likely because as interest rates trend lower to encourage more lending to companies, bank profits are squeezed. In this environment, they prefer to lend to lower-risk borrowers so as not to increase their share of non-performing loans. This has led them to double down on the top debt holders while sustaining or decreasing lending to most others. As we explained in another note (See “The End of China’s Magical Credit Machine”), declaring losses, cutting off non-performing companies and projects, and writing off loans would reduce banking system profits, which are the only consistent source of capital for the banks and key channels of financing for investment in China’s economy. It is far easier to simply roll over the loans and keep local companies operating, even if that means credit continues flowing to low-productivity industries.

Private equity and venture capital grows risk-averse

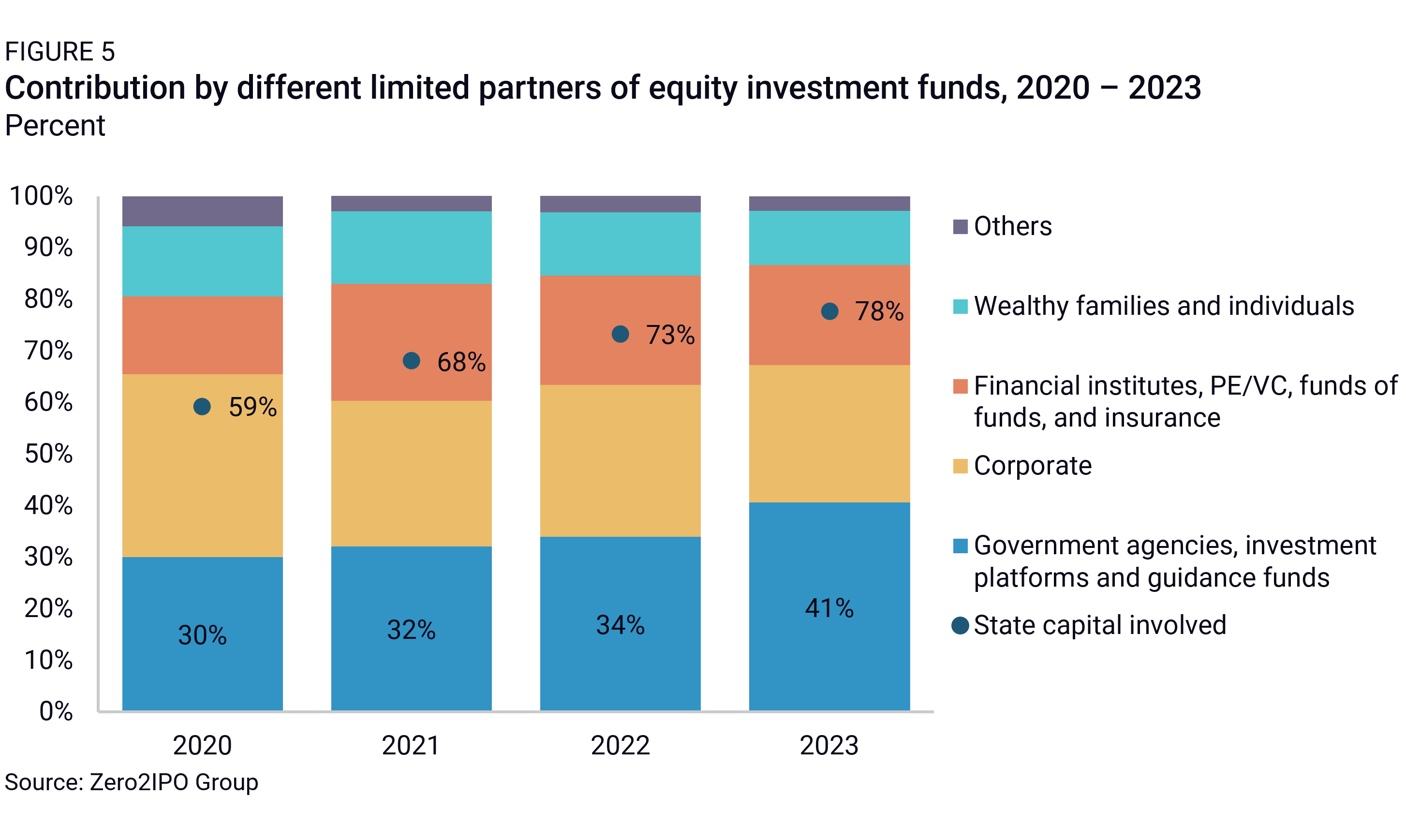

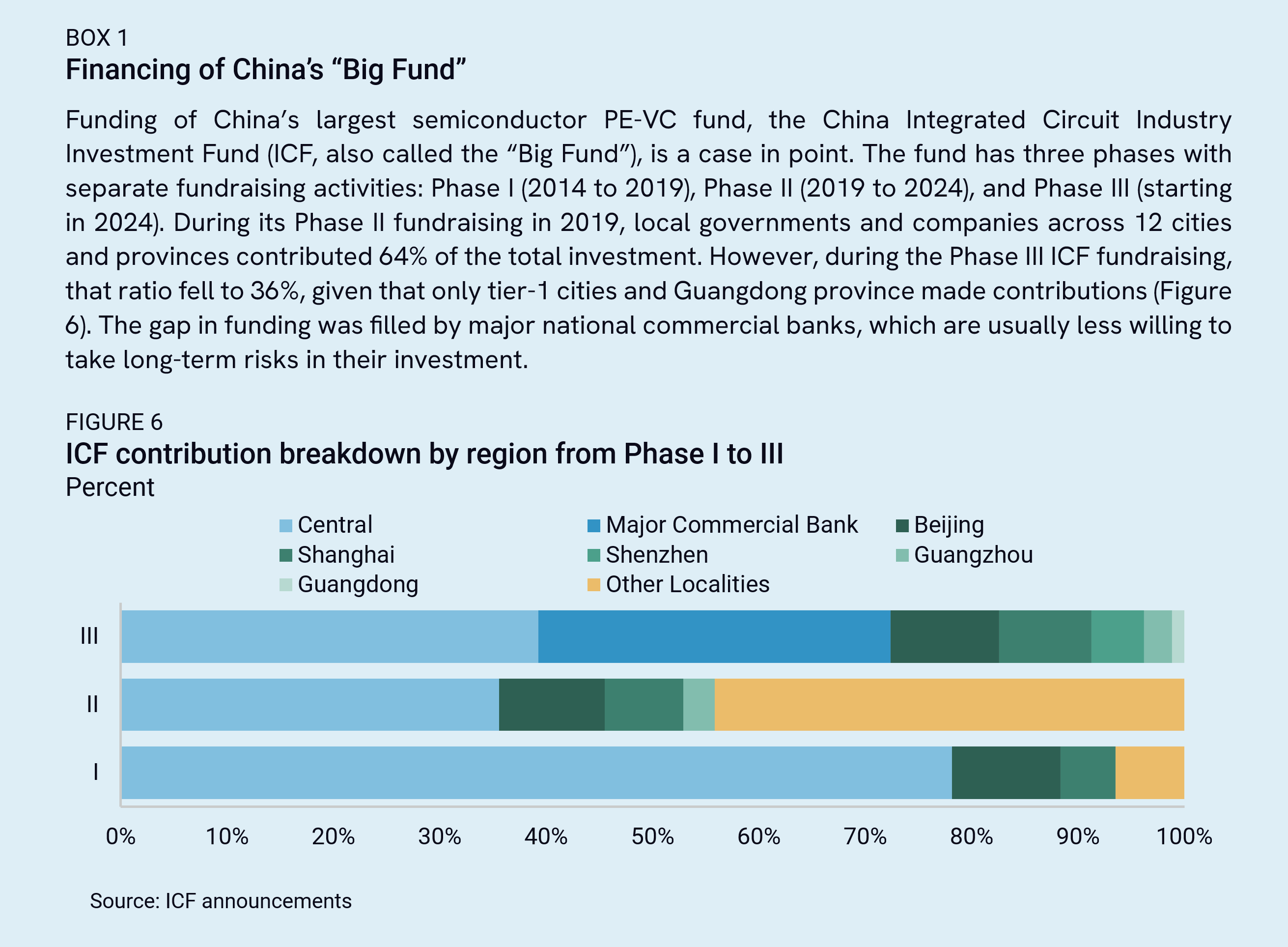

Beijing also needs PE-VC investment flowing to emerging industries and innovative start-ups. But the private PE-VC sector has collapsed since 2021, leaving only state-backed investors to partially fill the gap. Government-led funds contributed 41% of fund capital as limited partners in 2023, up from 30% in 2020. When accounting for investments made by SOEs, the ratio surges to 78% in 2023 (Figure 5). There are also indications that Beijing is increasingly leveraging bank capital into investment funds to compensate for declining direct government funding (Box 1).

Beijing’s ability to channel state resources succeeded in preventing early-stage investment from plunging along with late-stage investment. But this shift toward more public capital leaves the PE-VC sector more risk-averse and less able to make the kind of risky, long-term bets that China’s technological financing requires. State funds, and even more so banks, have been notorious for their strict scrutiny and risk-averse investment patterns. Prevention of losses, instead of high returns, is their top priority since any loss of investment could become a loss of state capital and proof of corruption. Officials tend to consider equity investment as loans, demanding small volatility in valuation and guaranteed payback of principal.

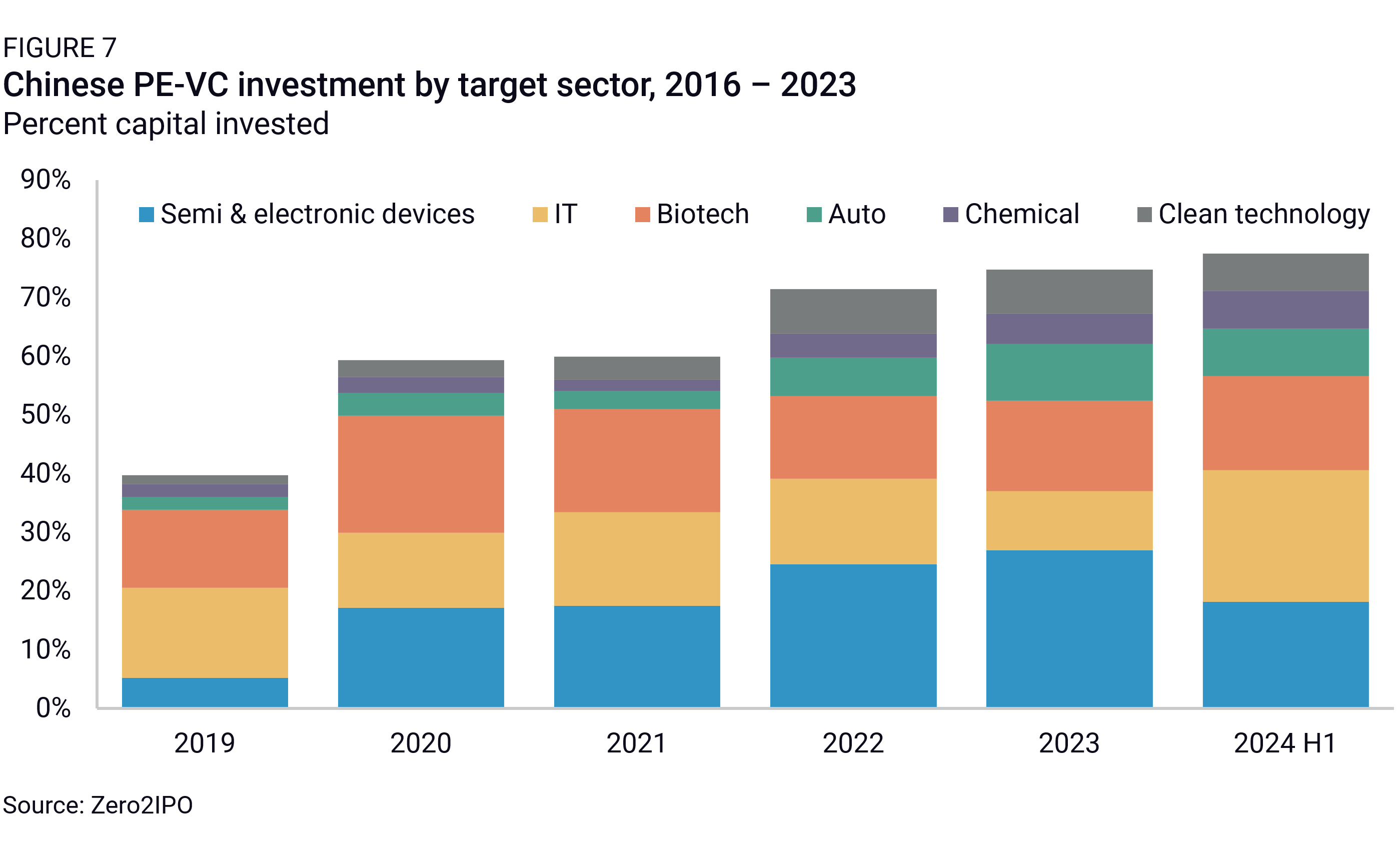

The risk-averse attitude of state-backed VC is reflected, notably, in the narrowing sectoral distribution of investments, concentrating on a few sectors considered safer bets given their relevance to Beijing’s strategic goals (Figure 7). The semiconductor, IT, biotech, automotive, chemical, and clean technology sectors collectively accounted for 77% of PE-VC investment value in H1 2024, up from 40% in 2019. This rise as a share of investment did not, however, prevent the absolute value from halving in recent years, from RMB 1.4 trillion in 2021 to RMB 700 billion in 2023.

Investment conditions are also stricter with state investors. They sometimes request an early exit from the investment once the target firm faces financial headwinds. State-backed investors are also more likely to use safeguard mechanisms like buy-back clauses, which stipulate that the target firm or the firm’s founder will need to pay back a certain amount of initial investment if the anticipated IPO fails. Such clauses are challenging for small innovative companies and may discourage them from raising funds.

This risk aversion is contrary to Beijing’s objectives. The State Council recently sought to lift state capital’s risk appetite with a circular called Policy Measures to Promote the High-Quality Development of Venture Capital in June 2024. The document pledged to reform the fund performance assessment system so that the preservation of state capital would not be the main indicator of performance. However, challenges in fiscal resources and local debt may hamper these efforts to make state capital more willing to take long-term risks. Besides, even as the central government pledged to relax state capital supervision, the fear of anti-corruption investigations and accusations of mishandling state capital will make local officials reluctant to invest in risky sectors or companies. In the long term, it is unlikely that state capital’s risk appetite can compensate for the decline in private capital.

Piling up on overcapacity-hit sectors

Amid a general slowdown and increasing concentration of funding—be it government grants, loans, or equity investment—firms in sectors already affected by high overcapacity still appear to be safe havens for the allocation of state and commercial funding. In particular, while the growth of government grants for most other industries is stagnating, grants for the “New Three” sectors—EVs, lithium-ion batteries, and solar photovoltaic products—have continued to grow, supporting continued investment in production build-out.

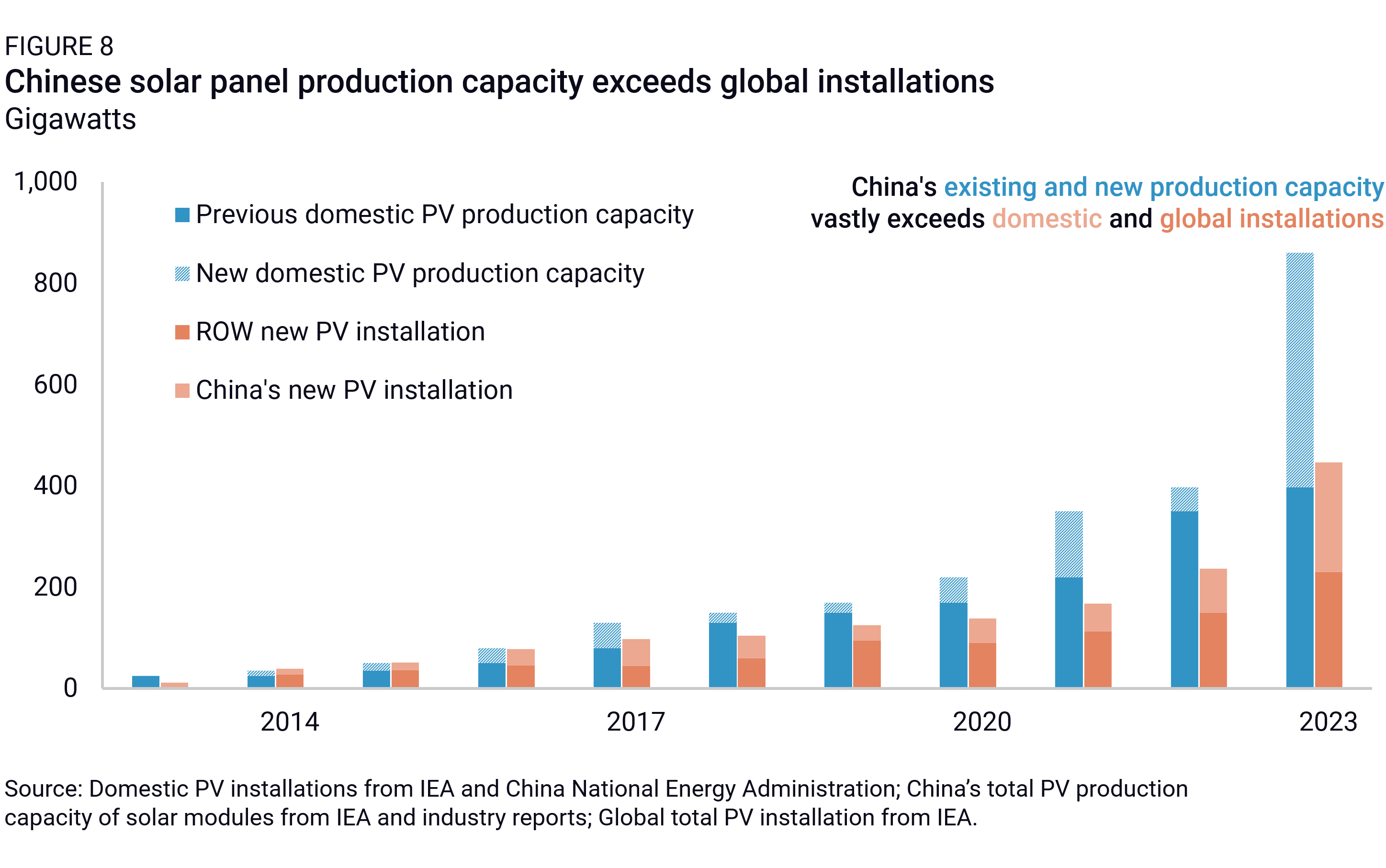

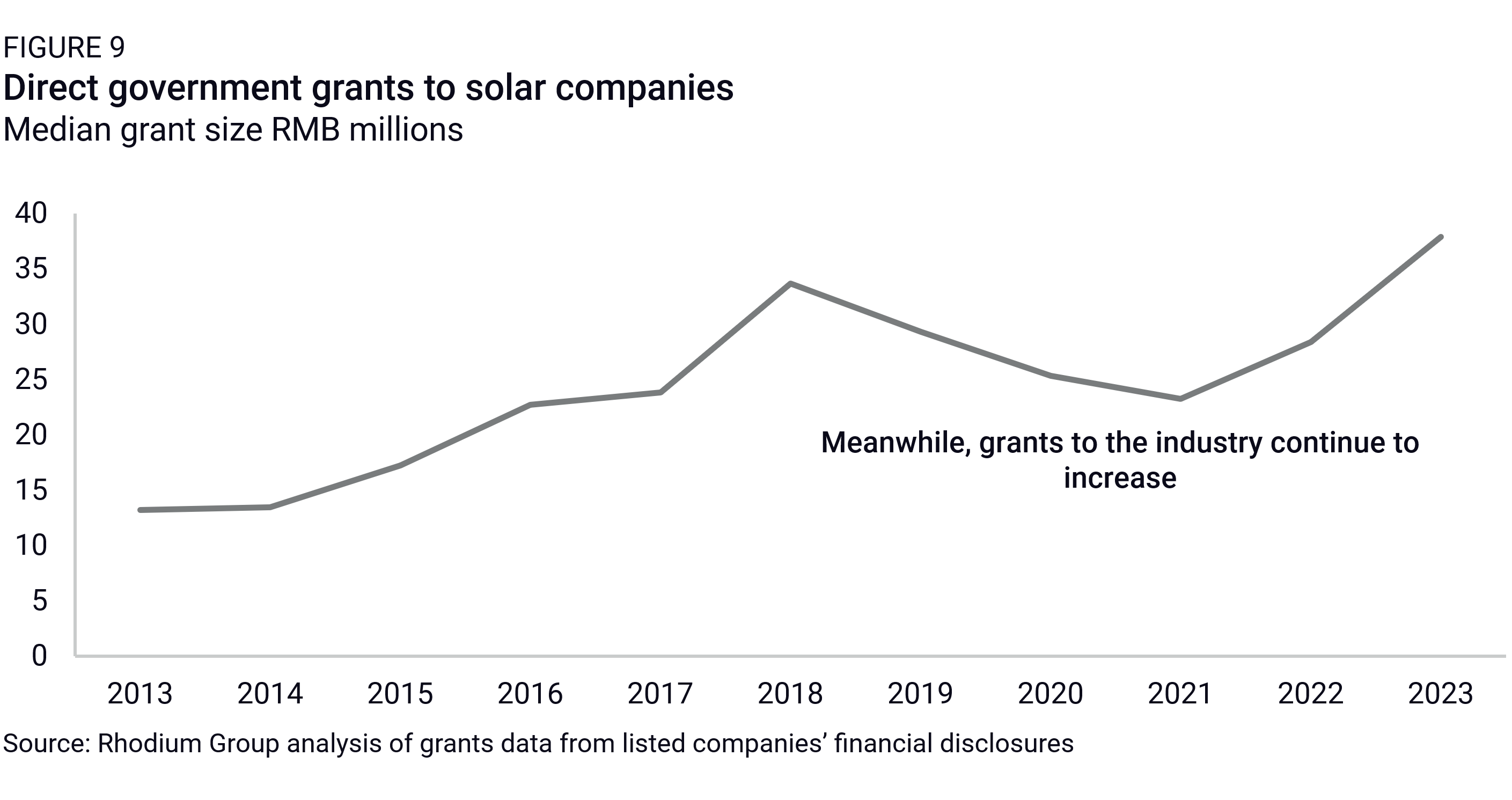

Take solar. In 2023, direct grants to solar equipment firms grew by a third year-on-year, while China added 861 gigawatts of solar panel production capacity, more than double the global total of new solar module installations (Figure 8). Government support and production growth are directly related, as local governments usually sign a contract with the producer, requiring a certain amount of production or capacity to be reached before a certain date. If the requirement is not fulfilled, then the producer must repay the subsidies. As a result, according to data from the Chinese consultancy PV Infolink, China’s solar module manufacturers reported an average capacity utilization rate of 23% in February 2024, down from an average of around 57% in the first half of 2023.

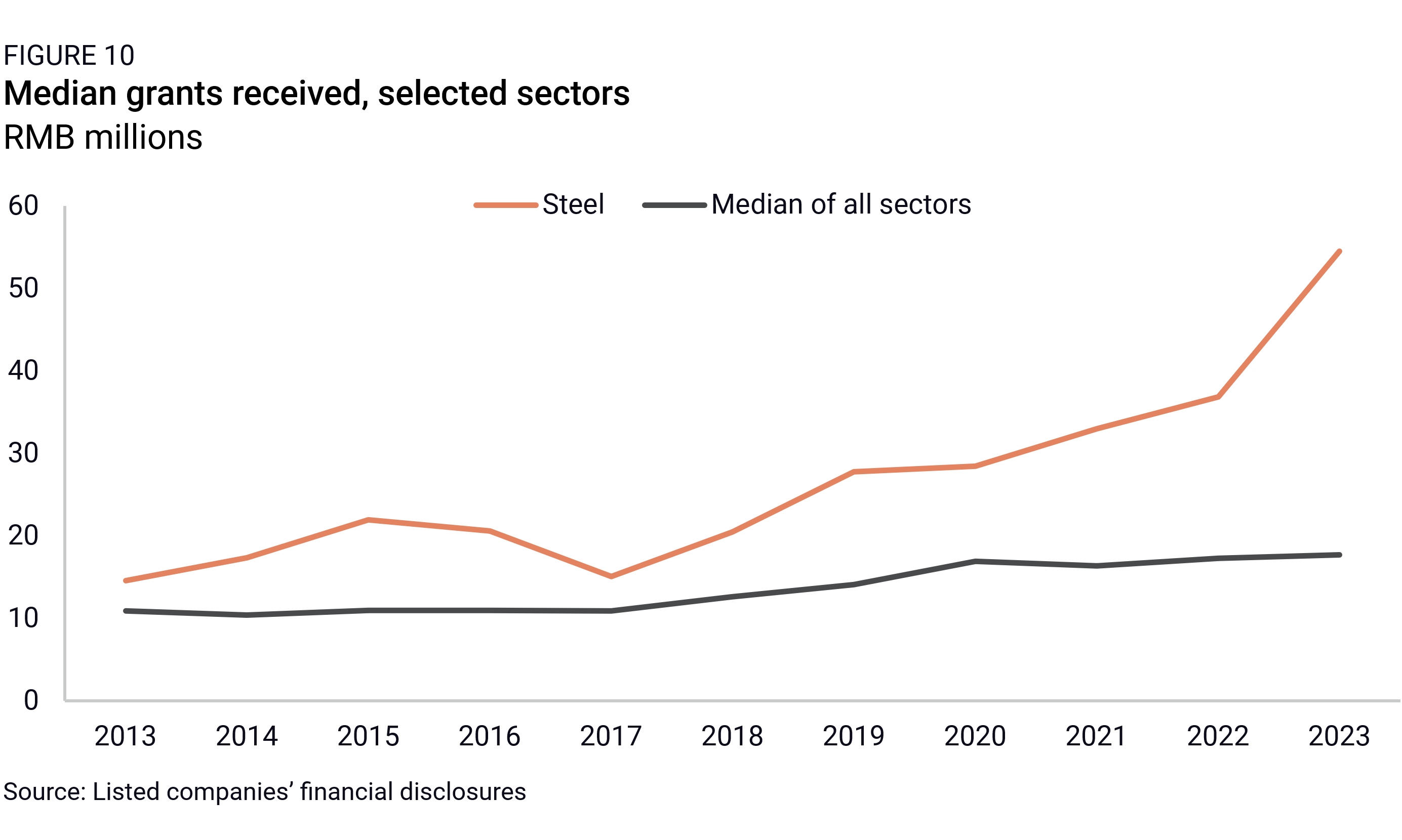

A similar pattern can be observed in the steel sector. During the last wave of overcapacity in 2015-2016, steel companies received large grants and cheap lending when excess capacity became rampant, thwarting progress in reducing capacity. Now, as the steel industry suffers from high overcapacity again and steel firms’ profits have declined to 2015 levels, government grants for the industry are rising fast, driven by support to local government-owned SOEs in the steel sector. Grants are being used to support the continued installation of new capacity, contributing to reduced export prices, along with the expansion of capacity abroad.

Outlook

Although the Chinese government has denied overcapacity is a problem, it mentioned the issue under the indirect name of “vicious involutional competition” during the July Politburo meeting. Ending the price war and making the new sector’s growth more sustainable is a key goal of Chinese policymaking. However, the data in this note reveals that the allocation of capital—whether through direct grants, credit, or PE-VC investment—often diverges from the objectives outlined in Beijing’s policies. The political and economic forces governing resource distribution are heavily influenced by the incentives of local governments and banks. Years of misallocated investment have made it challenging for these entities to redirect their resources toward more productive sectors and companies. Instead of channeling capital to small businesses and emerging technologies, as Beijing wants, financial actors are compelled to play it safe by supporting large, established firms and postponing losses in sectors burdened by significant overcapacity.

For small companies in emerging industries that cannot yet mobilize significant funding through reinvested profits, there are few other significant sources of funding to fuel innovation besides the three sources discussed in this note. The provision of industrial land and infrastructure through industrial parks, an important channel of state support to companies, largely boosts legacy industries. In 2022, newly built industrial parks mostly targeted industries such as chemicals, textiles, energy, construction materials, and metals—together accounting for more than 75% of the investment value of industrial parks disclosing their sectoral specialization.2 IPOs, historically an important source of additional funding for innovative companies, have become more difficult as Beijing slowed down the approval process to stabilize the stock market. By the end of July, 359 and 119 companies were waiting for approval to get listed in onshore and offshore markets, respectively, and funds raised through IPOs sank by 79% and 40% year-over-year in 2023 and the first half of 2024.

There are certainly other non-financial ways Beijing can influence the outcomes of innovation and industrial activity. Supply-side reforms of incentives for local governments and banks would be a key step. But this would likely require large-scale recapitalization from central government funds, which Beijing has shown little appetite for. Another obvious non-financial measure the government could take would be demand-side policies encouraging the consumption of innovative products. Without robust demand, the potential of innovative output remains constrained, as is the case in the artificial intelligence-generated content sector, where Chinese firms struggle to find sufficient domestic customers willing to pay for their AI services. But Beijing has been notoriously ineffectual at incentivizing consumer demand (See “No Quick Fixes: China’s Long-Term Consumption Growth”), and the manufacturing sector on its own is not enough to drive demand-led economic growth.

The slowdown in financial support for China’s accelerator state, as well as the absence of meaningful demand-side policies, will create challenges for Beijing’s innovation strategy and its long-term growth prospects. Large firms are key innovation drivers, but a high-performing innovation environment also requires a vibrant ecosystem of smaller, less established firms and a dynamic market willing to absorb new innovative products. If the expansion of capital is increasingly going to industries with existing overcapacity or otherwise inefficient investors, the drop in credit efficiency will also worsen existing structural problems associated with investment-led growth and accentuate trade tensions linked to rising Chinese exports.

Footnotes

We use the accounting category “other income” (其他收益), which, in Chinese listed firms’ financial reports, typically includes different forms of grants, including government grants related to assets, government grants related to income, tax write-offs, reduced prices on inputs, traditional subsidies from a variety of sources, etc.

Rhodium Group compilation, based on bonds disclosures and covering eight provinces: Guangdong, Shandong, Zhejiang, Jiangsu, Sichuan, Yunnan, Guizhou, and Xinjiang. The sectoral allocation only covers part of the total investment as most projects do not disclose the sectors they target.