Pathways to Build Back Better: Investing in Transportation Decarbonization

As Washington considers different proposals for investing in transportation infrastructure, we assess the energy system and emissions impacts of potential new, long-term federal investments in on-road decarbonization.

Washington is revving up its engines in a push to step up investments in transportation infrastructure. While it’s unclear just what will make it into a final package, the Biden administration’s American Jobs Plan and leading members of Congress are making transportation electrification a priority. Transportation is currently the largest emitting sector in the US. Unlike the electric power sector, there are no easy options for quickly swapping out fossil fuels with clean energy.

In this note, we assess the energy system and emissions impacts of potential new, long-term federal investments in on-road decarbonization and how investments might interact with potential new vehicle regulations. We find that federal investment in the form of long-term extensions of current tax credits coupled with a build-out of charging infrastructure can catapult electric vehicles (EVs) from 2% of all light-duty vehicle (LDV) sales in 2020 to as high as 52% of all LDV sales in 2031. Targeted public spending on medium- and heavy-duty vehicles, transit buses, and school buses can make even more decarbonization progress, while also cutting harmful air pollution. The combined impact of all investments we consider in this analysis, along with potential EPA regulations that put EVs on a path to 100% of light-duty sales in 2035, achieves CO2 emission reductions of nearly 180 million tons in 2031, roughly equal to 11% of 2020 sector emissions. These outcomes can be achieved with no net increase in total costs for many consumers.

The long road to a decarbonized transportation sector

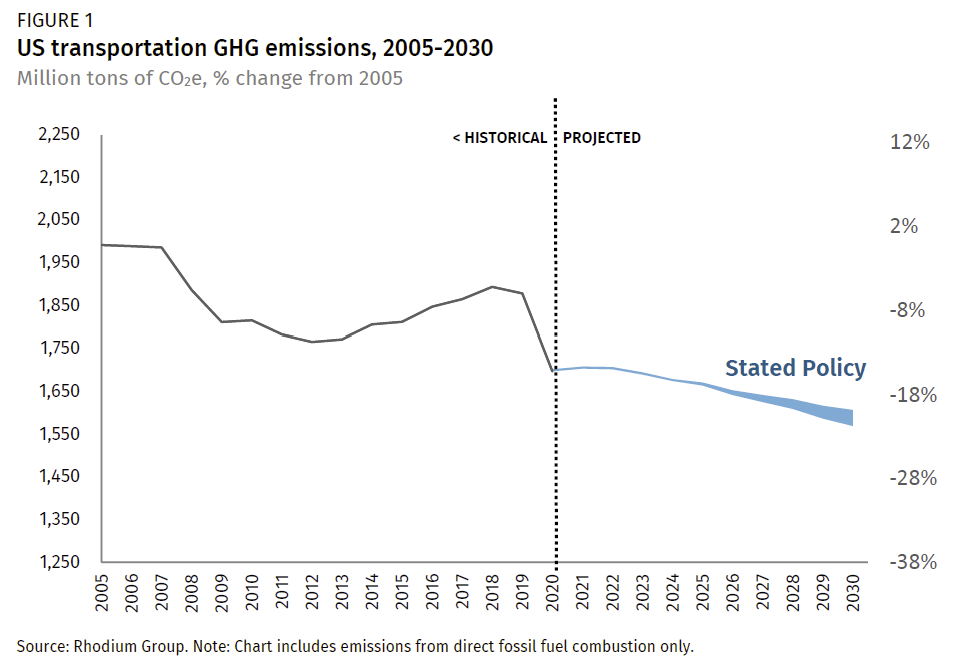

In 2017 the transportation sector overtook electric power as the leading source of greenhouse gas emissions (GHGs) in the US and now represents 31% of total net GHG emissions. The COVID-19 lockdowns and recession hit transportation emissions harder than any other sector in 2020. We estimate that fewer people flying and commuting cut emissions in the sector by 15% compared to 2019 levels. As more Americans get vaccinated and the economy recovers, transportation emissions will likely recover too. At best, emissions will be flat in the early 2020s and then decline slowly through 2030 as new vehicles get marginally more efficient and EVs become a meaningful part of the market (Figure 1). To accelerate progress, new action to deploy zero-emitting vehicles and enabling infrastructure will be necessary.

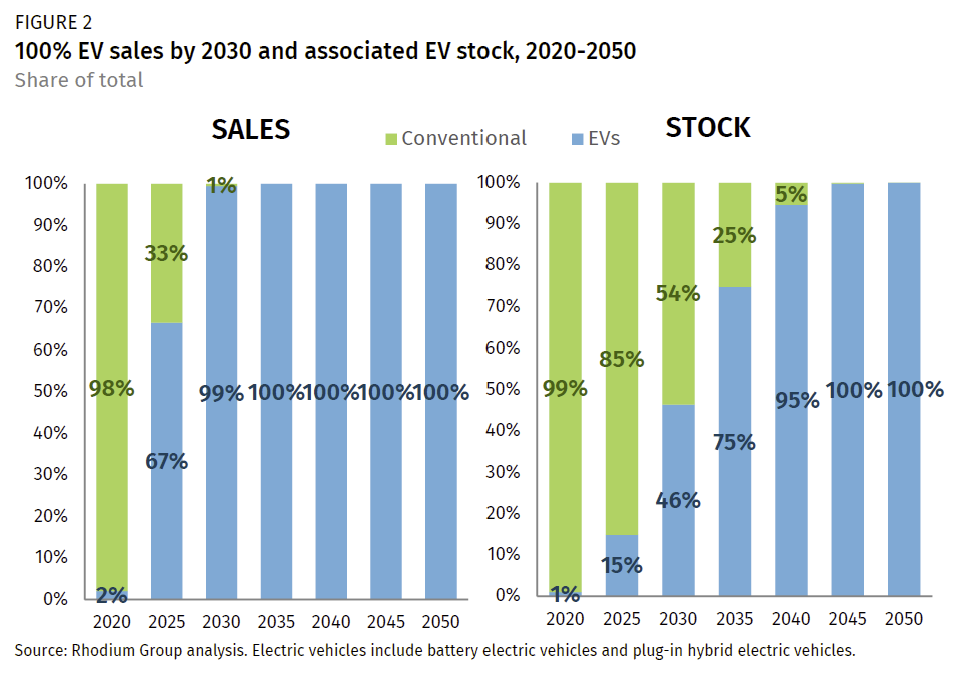

Any action to decarbonize transportation through electrification will require ambitious and sustained effort to accelerate deployment of electric vehicles as quickly as possible. Why the urgency? Unlike the electric power sector where a hard pivot from fossil energy to clean energy is entirely doable, it will take decades to replace all of the conventional gasoline and diesel vehicles on the road today with electric models. For example, even if the US can meet a 100% EV sales target in 2030, one of the most aggressive goals on the table, conventional fossil fuel vehicles won’t be completely off of America’s highways until 2045 (Figure 2). In any given year, only a small portion of cars on the road are brand new. It takes time for existing stock to turnover. Going forward, every vehicle sale matters in the race to electrify and decarbonize transportation.

Investment in electric vehicles is trending

It’s spring in Washington, DC, and, like the azaleas and cherry blossoms, policy proposals for infrastructure investment and decarbonization are coming out in full force. The White House released its American Jobs Plan at the end of March, which includes a wide range of policies intended to build infrastructure, create jobs, and address GHG emissions in all parts of the transportation sector. Senate Finance Chair Ron Wyden’s Clean Energy for America Act, cosponsored by 24 Democratic colleagues in the Senate, includes tax credits for electric vehicles and clean transportation fuels. Other proposals from last Congress are still very much in the conversation as well, including Senate Majority Leader Chuck Schumer’s Clean Cars for America proposal as well as the Driving America Forward Act to expand the current tax credit for electric vehicles proposed by Michigan Senators Debbie Stabenow and Gary Peters and Representative Dan Kildee. House Ways and Means Subcommittee Chair Mike Thompson’s Growing Renewable Energy and Efficiency Now (GREEN) Act also includes the Driving America Forward Act proposals. Other members of Congress have introduced more targeted bills, including support for electric vehicle charging infrastructure and a clean energy manufacturing tax credit that will likely support manufacturing of electric vehicles, batteries and other components manufacturing.

We combine elements from many of these proposals to estimate the energy system impacts of a package of policies that invest in transportation decarbonization. This illustrative package is by no means the only investment pathway to decarbonize transportation, but it does start to draw down emissions in several of the largest emitting transportation subsectors. Specifically, the package we model includes the following provisions available from 2022-2031:

- Light-duty vehicle (LDV) purchase incentives: Consumers can receive up to $7,500 for the purchase of a battery-electric (BEV) or plug-in hybrid (PHEV) vehicle. The credit is available for all new electric vehicle purchases, without a cap on the number of credits available for a given manufacturer.

- Public LDV charging grants: State and local governments and the private sector receive funding to build out a national EV charging network required for the expanded LDV EV fleet on the road.

- Medium-duty (MDV) and heavy-duty (HDV) vehicle purchase incentives: Purchasers of all-electric MDVs and HDVs receive a 10% investment tax credit (ITC). Purchasers of electric HDVs are exempted from the 12% federal excise tax on heavy-duty trucks.

- Electric bus incentives: Federal grant programs pay the incremental cost of battery-electric transit and school buses and associated charging infrastructure and upgrades.

We model these policies in RHG-NEMS, a version of the Energy Information Administration’s National Energy Modeling System modified and maintained by Rhodium Group. For the purposes of this note, we use our Taking Stock 2020 V-shaped macroeconomic recovery baseline, which includes current federal and state policy on the books through May 2020. Notably for a discussion of the transportation sector, this includes modeling state zero-emission vehicles (ZEV) mandates and low-carbon fuel standards (LCFS).

We make several modifications to the Taking Stock 2020 baseline. First, we include a second, lower lithium-ion battery price pathway based on forecasts from Bloomberg New Energy Finance. Second, the Biden administration is reviewing the Safer Affordable Fuel-Efficient Vehicles (SAFE) rule, which is the current LDV fuel economy and greenhouse gas emissions standards established by the Trump administration. That review is still under way, but in order to not overstate the impacts of an investment package relative to baseline, we assume the Biden administration replaces the SAFE rule with standards that achieve targets first implemented by the Obama administration, with a one-year delay. We also assume such new standards follow similar annual improvements in fuel economy from 2026 through 2031. As we discuss in a later section of this note, the Biden administration could choose to adopt still-more-stringent standards than the Obama-era standards.

Finally, we pair our transportation investment pathway results with carbon intensity of electricity outputs from the investment pathway in our recent power sector investment note, resulting in lower GHG emissions per kilowatt-hour for electricity relative to current policy.

Putting the electric vehicle pedal to the metal

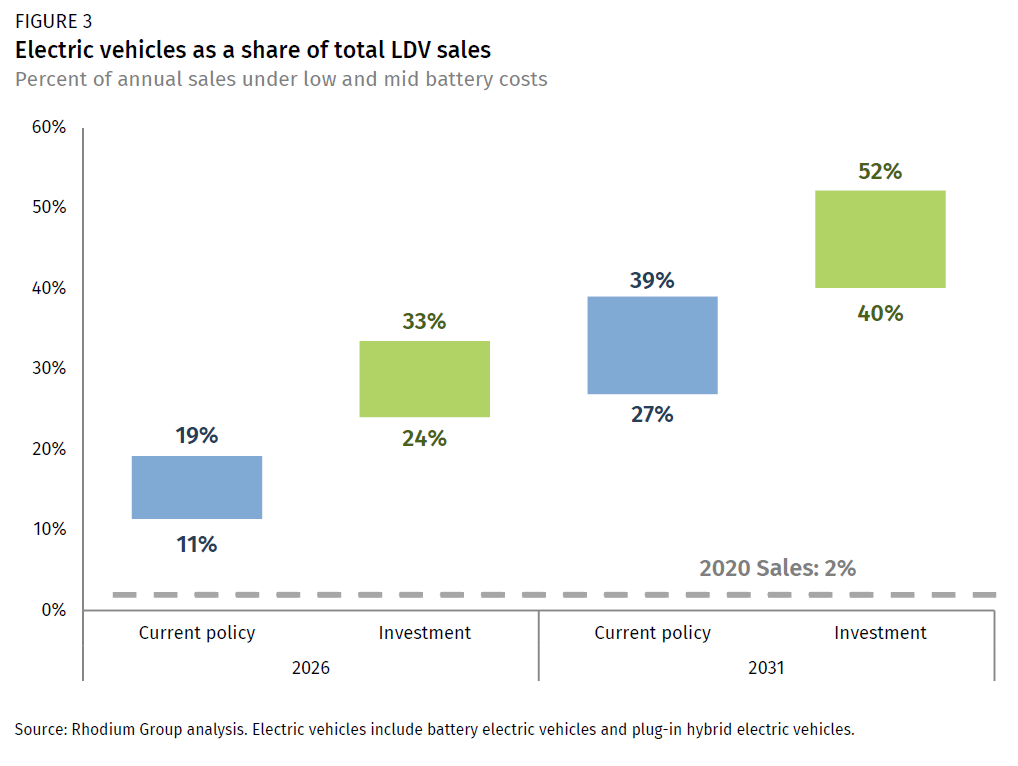

Looking at cars and light-duty trucks, we find that federal investment can meaningfully accelerate the transition to an electric LDV fleet. Under the investment package, in 2031, 40-52% of all sales of LDVs are electric, compared to 27-39% under current policy (Figure 3). The result is a cumulative 39-50 million electric LDVs sold by 2031, comprising 15-20% of all LDVs on the road.

Sparking a revolution in public charging

A large build-out of public charging infrastructure will be required to support tens of millions of new EVs on the road. The number of chargers required for a given fleet and the required investment are heavily dependent on assumptions about charging behaviors and the types of chargers that are deployed. The American Jobs Plan proposes building out 500,000 chargers nationally. Using the charging infrastructure assumptions underlying the National Renewable Energy Laboratory’s (NREL) Electrification Futures Study (EFS), a major analysis examining multiple electrification pathways economywide, we estimate that 430,000-600,000 public chargers will be required to support the number of EVs on the road by 2031 in the investment scenario under our mid and low battery cost cases. Most of these chargers are level 2 chargers, which can add 10-20 miles of range for every hour of charging. Others find that fewer chargers may be needed if the share of DC fast chargers (DCFC) is higher, though costs may be higher.

Amping up EV sales even further

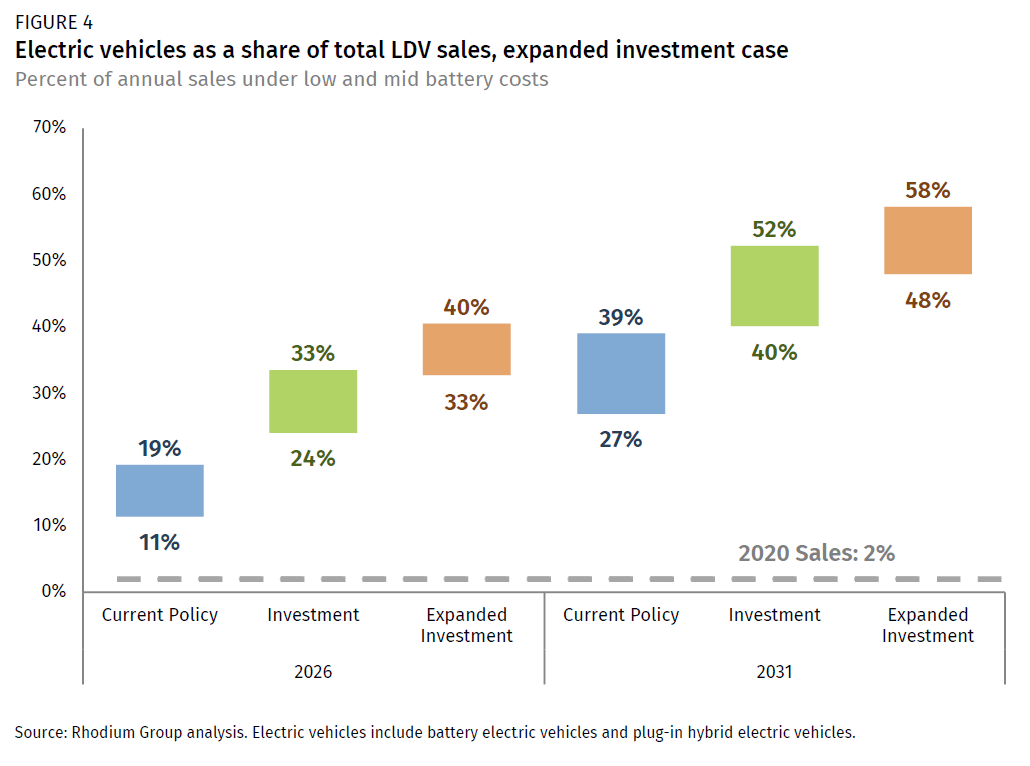

Some policymakers are considering incentives beyond the $7,500-per-car level to achieve specific policy goals. For instance, the Schumer Clean Cars for America proposal includes additional incentives for low-income families, for vehicles made at facilities with strong labor standards, and for vehicles made with at least 50% domestic content and a US-manufactured battery. Modeling the specifics of any individual proposal is beyond the scope of this note. But to provide an order-of-magnitude estimate, we estimated the effects of increasing the average purchase incentive available for LDVs to $11,250, or 50% above the $7,500 level in our main investment scenario. We find that larger incentives can accelerate EV deployment even further. Under this expanded investment case, the share of electric vehicles further increases, to 48-58% of all new LDV sales in 2031 (Figure 4).

Beyond light-duty vehicles, electrification is a heavier lift

The medium- and heavy-duty vehicle (MDV and HDV) subsectors represent a diverse array of vehicle types and uses, from delivery vans and garbage trucks to utility vehicles and semis. Electrification is a more cost-effective option for decarbonization for some MDVs and HDVs, while other approaches, like low-carbon hydrogen, biofuels, or electrofuels, may be better suited for other applications. The scope of this note is limited to a discussion of electrification.

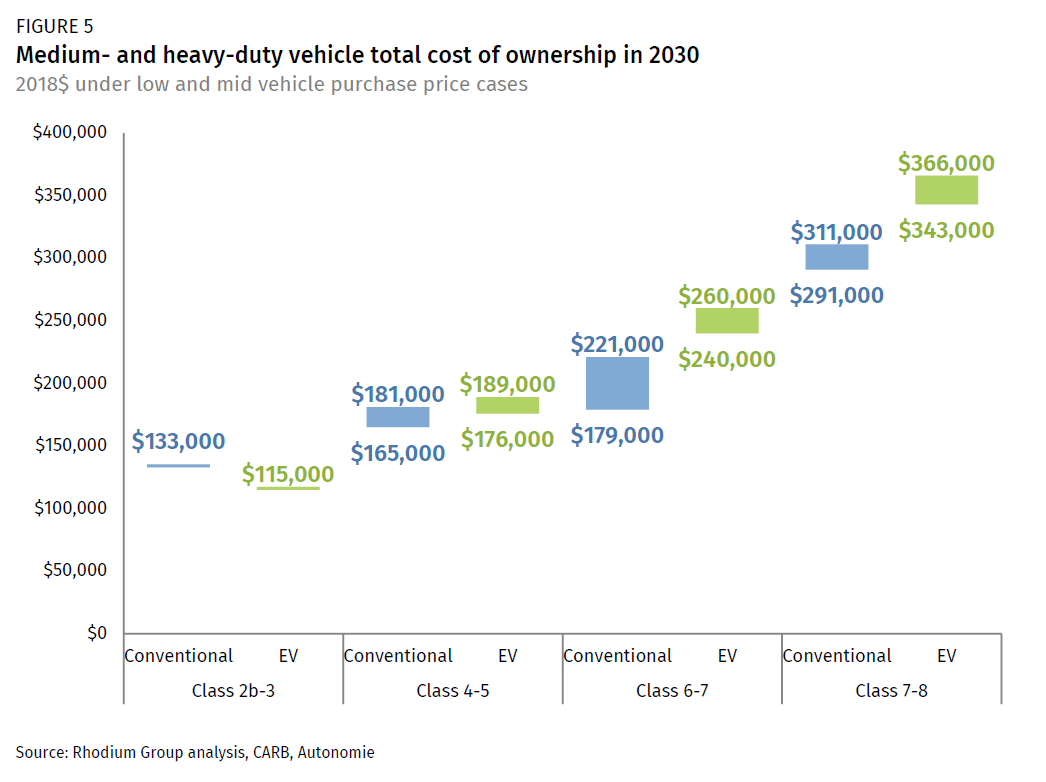

To estimate the effects of the potential investment package for electric MDVs and HDVs described above, we first estimate the impact the policy has on the total cost of ownership (TCO) of an electric vehicle relative to a conventional fuel (i.e., diesel or gasoline) vehicle.[1] By 2030, our modeled incentives—a 10% ITC for MDVs and HDVs and HDVs and an excise tax exemption for HDVs—can drive EVs to or below TCO parity with conventional vehicles in some smaller vehicle classes and reduce the gap in others (Figure 5). Particularly for larger vehicles (Class 6-8), a BEV is still more expensive on a lifetime basis. This is a function of range and weight with higher class vehicles needing larger, more expensive batteries.

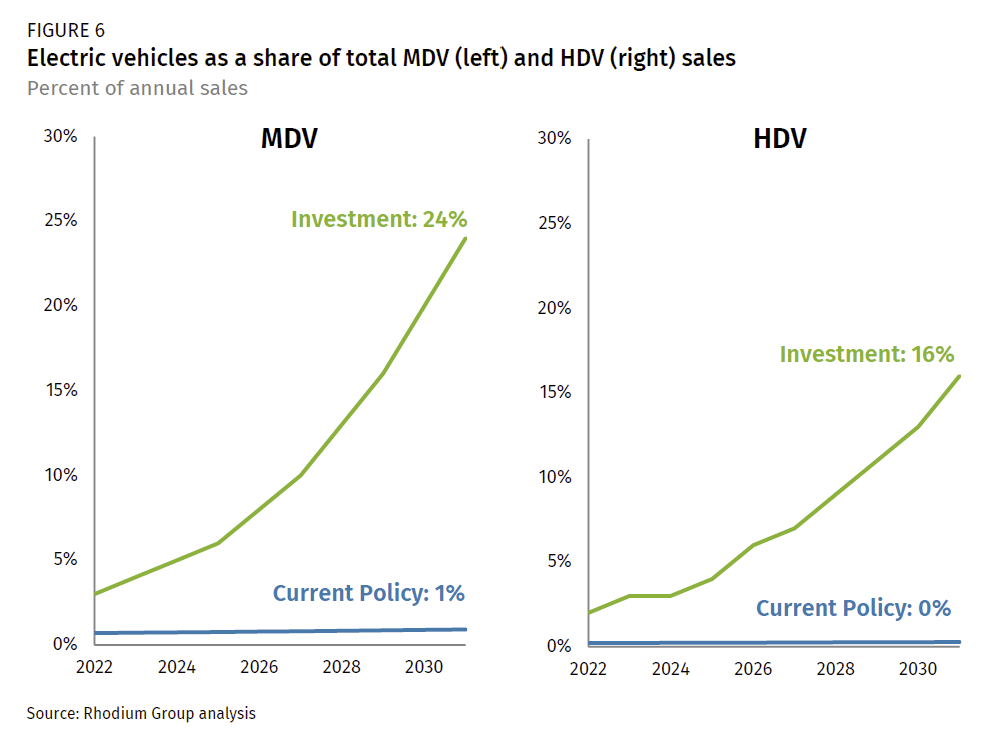

We assume that the spending programs in our investment scenario are enough to accelerate MDV and HDV deployment to match NREL’s EFS high scenario.[2] Under our investment scenario, we see EVs reaching 24% and 16% of MDV and HDV sales, respectively in 2031 (Figure 6). This is a significant increase from the low levels of deployment that occur under current policy.

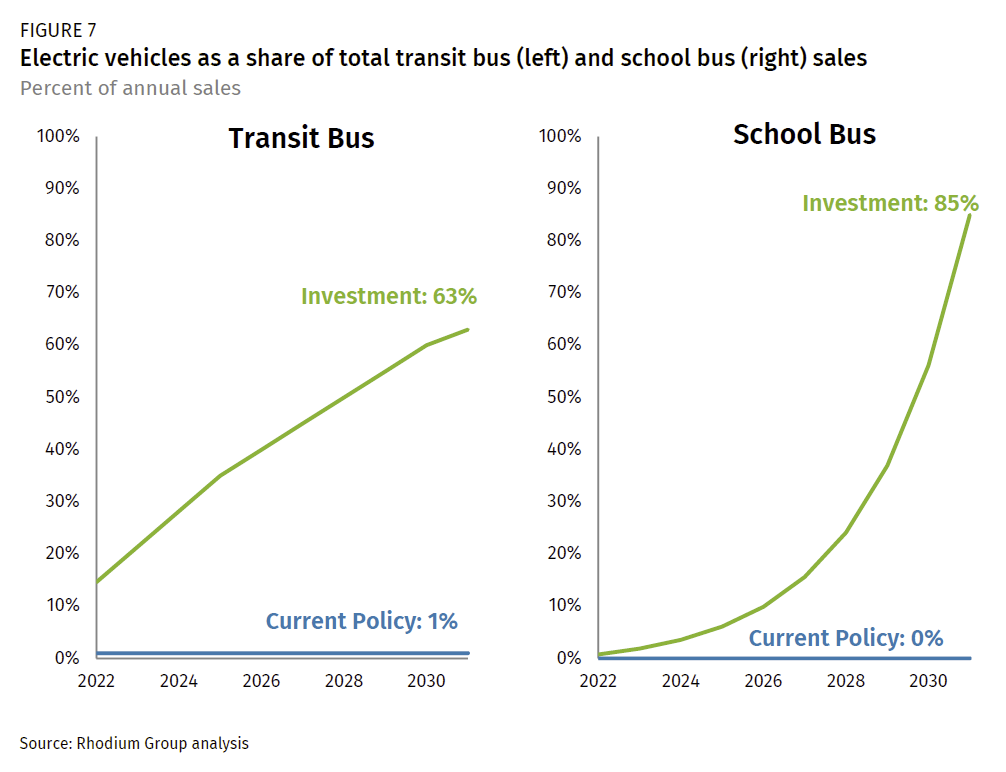

Buses are another important part of the transportation sector to electrify. In addition to climate-warming greenhouse gases, MDVs and HDVs, including buses, are large sources of other pollutants that negatively impact public health, including particulate matter and nitrogen oxide (NOx). School buses in particular are a public health threat for children, where diesel fumes can harm still-developing lungs.

We model the energy system effects of a set of grant and incentive programs targeted specifically at transit and school buses. We structure the incentives to be sufficient to pay down the total incremental upfront cost of the transition to a battery-electric bus, including the higher vehicle purchase price as well as the build-out of charging infrastructure. While electric buses have a significant upfront cost relative to their diesel counterparts, transit authorities and school districts will save money in the long run due to the lower cost of fuel and maintenance. For transit buses, we estimate BEVs will comprise 63% of sales by 2031 and will completely phase out the sales of diesel buses by 2030 (Figure 7). For school buses, we estimate BEVs will comprise 85% of sales in 2031 and 20% of all school buses on the road that year, achieving the target outlined in the AJP.

Shifting gears from fossil to clean transportation

Taken together, this suite of federal investments in electrification leads to a 775-831 trillion British thermal units (TBTU) drop in fossil fuels in 2031 compared to current policy. Fossil fuel consumption is replaced with 491-510 TBTU of electricity. This translates to a 4-5% reduction in gasoline and diesel demand and a 77-119% increase in transportation sector electricity demand from new electric vehicles. The energy shift from fossil to electricity is not one-to-one given the substantially higher road efficiency of electric vehicles.

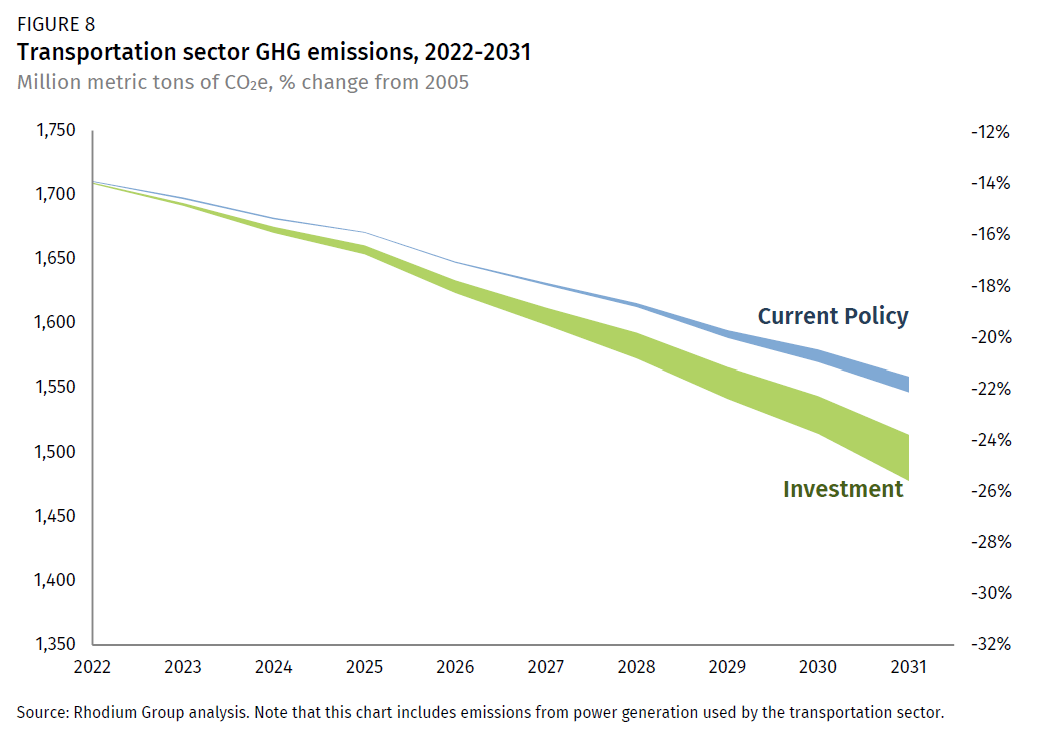

The net GHG emissions result of these shifts in the transportation sector is a 114 to 125 million metric ton reduction relative to current policy in 2031—a 24-26% reduction in total transportation emissions from 2005 levels, compared to a 22% reduction under current policy (Figure 8). The majority of these reductions are attributable to fewer gas and diesel vehicles on the road. But a cleaner electric grid in the investment scenarios relative to current policy helps to mitigate the power sector emissions increase from the higher use of electricity, contributing to further net reductions.

We estimate this transportation investment package would have an average budget impact to the federal government of $34.6-$44.3 billion per year over 2022-2031. The majority of that impact, $29.4-$39.1 billion per year, is for incentives for electric LDVs. It is important to note that for purposes of legislative budget scorekeeping, the estimates that matter come from the Joint Committee on Taxation and the Congressional Budget Office, not the estimates we present here. If either organization uses different approaches to quantifying the impact of investment, the associated budget cost estimates could be far different from ours.

Our budget cost estimates are two orders of magnitude larger than the estimated cost of current EV tax credits. While not explored in this analysis, there are options for reducing budget costs while still roughly maintaining the energy and emissions outcomes we present above. One option is to avoid paying incentives for the sale of electric luxury cars where buyers are far less likely to be price sensitive. This could be done by requiring incentive eligible electric vehicles to have a retail price below a certain threshold. Alternatively, incentives could be contingent on EV buyers meeting certain income requirements. While such an approach has the potential to be cumbersome, it could prevent wealthy individuals from monetizing the tax credit for EVs they may buy anyway.

Investment can complement regulatory action

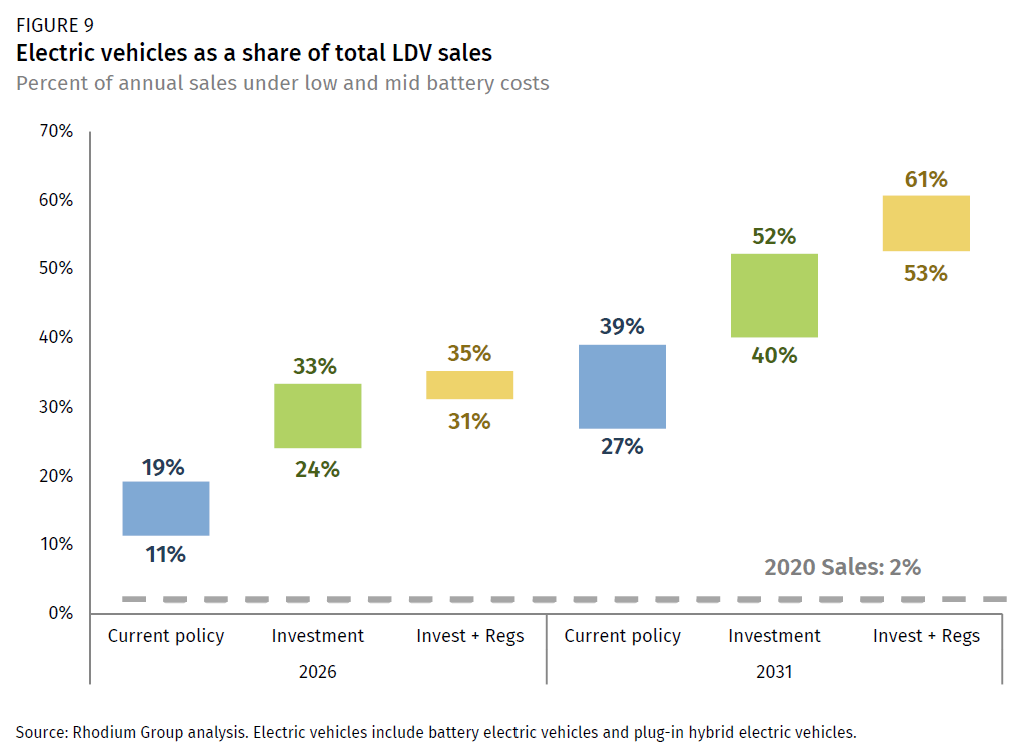

Investment in EV deployment yields impressive energy system benefits, but at the levels we assessed above, investment alone is not enough to put the US on a path to 100% electric LDV sales by 2035—a commonly cited goal. In order to achieve that level of EV sales, policymakers must consider other available tools. One such approach could be pairing investments with aggressive but achievable LDV GHG standards under the Clean Air Act. We estimate that setting a footprint-based CO2 standard of 90 grams per mile for new LDV sales in 2031 would firmly establish the US on that 100% ZEV pathway. With investments plus this regulatory target, we estimate EVs can comprise 53-61% of all LDV sales in 2031 (Figure 9).

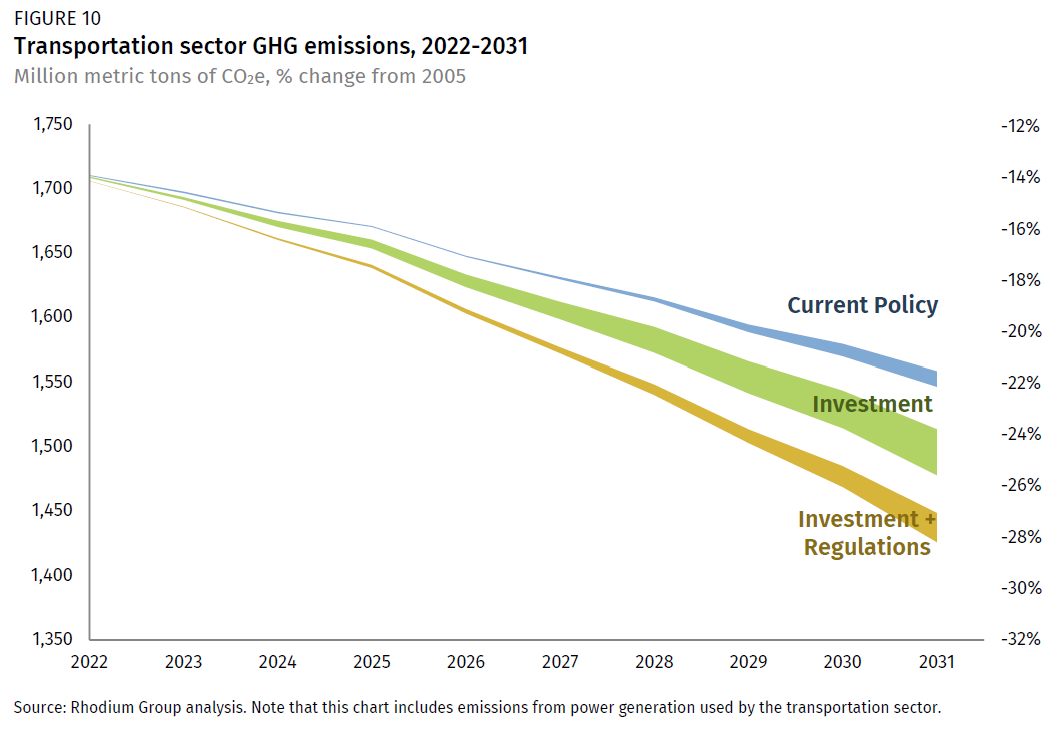

This increase in EV sales plus continued improvements in the fuel economy of conventional LDVs to meet the 90 grams/mile standard yields still further GHG emissions reductions, 177-179 million metric tons below the current policy case in 2031, or 27-28% below 2005 transportation sector emissions (Figure 10).

The challenge of slow stock turnover makes it difficult to contemplate much larger GHG reductions than what we show here solely from investments in electrification and regulations on LDVs in this decade. If the US can get on an ambitious EV deployment pathway, greater emission reductions will materialize in the 2030s. In the meantime, shifting travel to less carbon-intensive modes such as bikes and transit, reducing travel demand through smarter planning, and investments in decarbonizing shipping and aviation can all make contributions to greater reductions in the next decade. Another opportunity not explored in this analysis but under discussion in Congress is investments in clean liquid fuels that can serve as substitutes for fossil fuels in conventional vehicles on the road today. Bio-based fuels as well as synthetic hydrocarbon fuels produced with recycled or atmospheric CO2 and clean hydrogen are promising options that overcome stock turnover in the near-term and can accelerate emission reductions. Multiple legislative proposals contain clean fuel tax credits that may help to scale these fuels over the next few years.

Investment can reduce the consumer cost of regulatory action

In addition to the direct GHG benefits of displacing fossil fuel cars and trucks with electric vehicles, investment policies that result in high levels of EV deployment have a multitude of additional benefits, including substantial battery cost reductions and the potential to build a thriving domestic EV manufacturing industry.

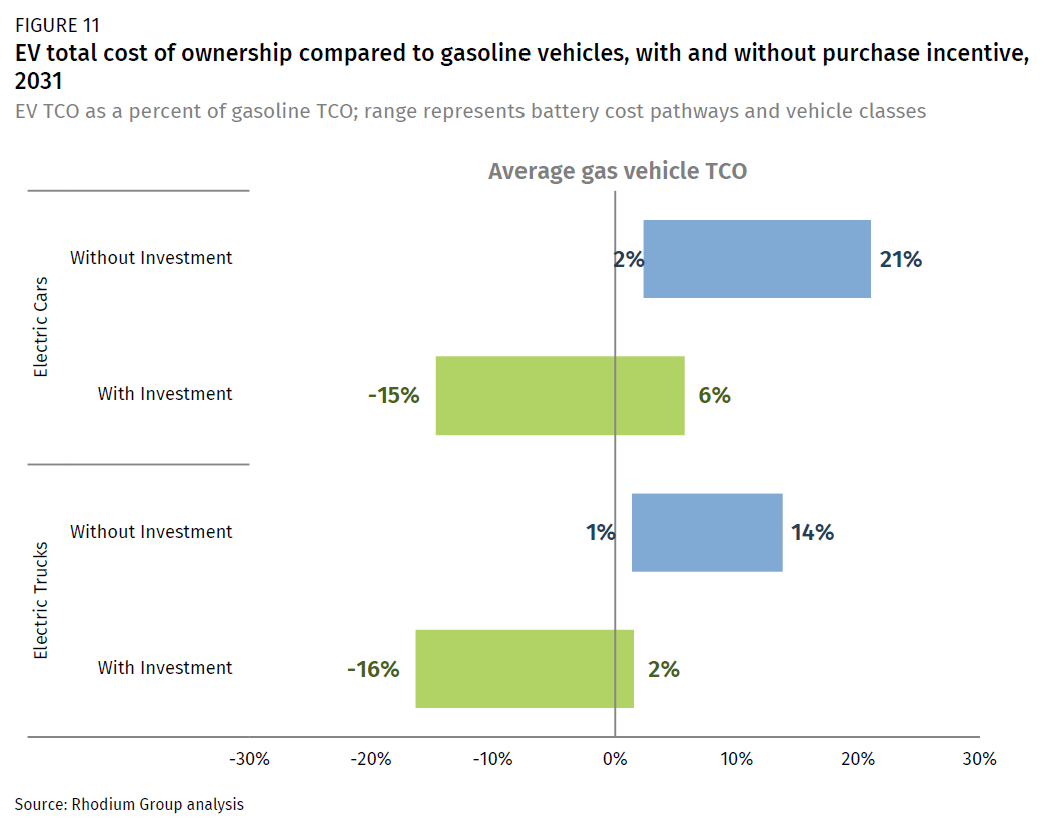

We calculate the TCO for a range of electric vehicle classes in 2031 under both our mid and low battery cost trajectories.[3] Due to 15-30% declines in the purchase price of an electric vehicle in 2031 relative to 2022 in our investment scenarios, we find that the total unsubsidized cost of owning an EV is very close to cost parity with gasoline vehicles in 2031 for some vehicle classes under our low battery cost pathway (Figure 11). This gap shrinks even further in the investment and regulations scenario, as the cost of gasoline vehicles increases with the need to use more advanced technologies to improve fuel economy in order to meet the more stringent GHG standard. And, of course, a $7,500 vehicle purchase incentive makes EVs cheaper than gas vehicles on a TCO basis (and in some cases on an upfront purchase cost basis as well) in most cases. Only certain larger classes of cars and trucks are not cheaper to own when the subsidy is factored in.

Consumer costs are an important factor for EPA and NHTSA in determining the ambition of LDV GHG and fuel economy standards. Our results show that if Congress implements a robust, decade-long EV incentive, there may be no incremental cost for most consumers of getting on a path to 100% ZEV. While the cost of owning a vehicle is only one factor in setting LDV GHG and CAFE standards, approaching and even surpassing TCO parity is one indication that the Biden administration can pursue more aggressive regulatory requirements than ever before without raising consumer costs and generating net economic benefits.

There are a few unknowns that can change our findings. The most significant factor is EV component supply and associated costs. With EV demand ramping up globally, concerns about the medium and long-term availability of key materials such as lithium and cobalt have also increased. Just as important, most of the current production of key materials and components is located outside the US. If supplies of key materials are not available for trade or geopolitical reasons or become too expensive because of too much demand and lack of supply, EVs will be more costly and deployment will be lower than what we present in this note.

A key goal of the Biden administration’s American Jobs Plan is to invest in US manufacturing. New federal investments in US EV production and upstream materials have the potential to meaningfully expand global supplies and may help to meet demand, keeping costs down. Investments can also create US manufacturing jobs. Adding domestic content and labor standard requirements to the incentives discussed in this analysis may also have a similar impact. While we focus on energy and technology impacts, the economic and geopolitical case for investment may be just as important in the political debate to come.

Next steps

If a major clean energy investment package is going to make a difference, it first has to get through Congress. The ultimate size and scope of a package and the process for getting it to President Biden’s desk is still unclear. What we know is that a major investment in clean transportation has the potential to get the nation a few miles further down the long road of decarbonization. We’ll continue to monitor developments and assess just how far Congress may be willing to go on clean transportation in 2021.

[1] We take a straightforward approach to calculating TCO, accounting for vehicle purchase price, the cost of needed charging infrastructure, and annual fuel and maintenance costs. We estimate TCO ranges based on costs from California Air Resources Board with a higher vehicle purchase price sensitivity from analysis conducted by Argonne National Laboratory using their Autonomie modeling platform.

[2] High electrification represents “a combination of technology advancements, policy support and consumer enthusiasm that enables transformational change in electrification” per NREL.

[3] As in the MDV/HDV sector, we take a simplified approach to calculating TCO, only including the purchase price of a vehicle and the discounted costs of fuel and maintenance over the vehicle lifetime.

This nonpartisan, independent research was conducted with support from the ClimateWorks Foundation, the Energy Foundation, the Heising-Simons Foundation, the Linden Trust for Conservation and the William and Flora Hewlett Foundation. The results presented in this report reflect the views of the authors and not necessarily those of supporting organizations.