Can Tax Credits Tackle Climate?

As policymakers weigh their options, this independent analysis examines several key energy tax credits that cover zero-emissions electricity, electric vehicles, biofuels, and carbon capture and storage.

Congress is back from the end-of-summer slowdown, and lawmakers and advocates have their sights set on getting a tax credit extension package moving through key committees with the potential for passage by the end of the year. Opportunities to advance a large package of clean energy tax credits do not come often. Depending on the scale of the legislative effort, a tax extenders package could represent this Congress’s largest opportunity to advance clean energy and reduce emissions. As policymakers weigh their options, this independent analysis examines several key energy tax credits that cover zero-emissions electricity, electric vehicles, biofuels, and carbon capture and storage.[1] We assess each tax credit’s ability to make progress towards decarbonization of the US energy system and cut carbon dioxide emissions. We find that:

The US can make progress in reducing emissions by extending tax credits: Extending and expanding tax credits through 2025 for zero-emitting generation including wind, solar or nuclear could achieve reductions of up to 125 million tons compared to current policy in 2025. This could fill up to 25% of the gap between US emissions under current policy and its Paris commitments.

Deployment of key technologies accelerates with tax credit extensions: Providing an incentive for drivers to make the switch from gasoline-powered cars nearly doubles the number of electric vehicles on the road through 2025. By 2030, wind and solar could supply up to 31% of total US electricity. Other key technologies including carbon capture utilization and storage (CCUS) and advanced biofuels could also see additional deployment.

Extending tax credits can provide certainty to new industries and level the playing field: From easing compliance with renewable fuel standards to shelving offshore wind development and postponing tax guidance for CCUS, the current administration has stirred up uncertainty on multiple fronts. These actions could jeopardize critical components of climate mitigation. Extending tax credits can buy time and stability to move projects through the pipeline.

Congress Considers its Options

If the US is going to play a leadership role in tackling the problem of climate change, the energy system will need to achieve net-zero carbon dioxide (CO2) emissions by mid-century if not sooner. This will require rapid deployment of a wide range of clean energy technologies and innovations—far faster than the remarkable progress we’ve seen in the past decade for technologies like wind and solar. In this Congress and with President Trump in the White House, the prospects for comprehensive climate policy are slim at best. However, incremental progress is still a possibility.

Clean energy tax credits continue to garner support on Capitol Hill, part of a bipartisan tradition of extending these incentives on several occasions over the last decade. Legislation introduced this Congress would extend or expand specific credits to support individual technologies. Lawmakers are also looking at ways to streamline and simplify the tax credit regime in an effort to accelerate clean energy deployment. Many of these proposals have supporters on both sides of the aisle and work is underway in each chamber to advance a comprehensive framework. The House Ways and Means Committee is currently constructing a clean energy tax credit package. In the Senate, the Finance Committee last month initiated a process to identify which tax credits should be maintained or removed from the tax code.

The push to extend clean energy tax credits represents a crucial opportunity to make progress towards decarbonization in this Congress.[2] Ongoing efforts by the Trump administration to roll back several rules impacting climate underscore the urgency of the debate. This independent analysis assesses the impact of extending select clean energy tax credits to understand what they can achieve with regards to technology deployment and CO2 emissions reduction. We focus on several existing and proposed tax credits that could contribute to decarbonization in the three sectors of the US economy that emit the most CO2: electric power, transportation, and industry.[3]

The target technologies and tax credits considered in this analysis include:

- Renewable energy: The Investment Tax Credit (ITC) for utility-scale and distributed solar (Section 48), the ITC for offshore wind (Section 48) and the Production Tax Credit (PTC) for onshore wind (Section 45)

- Nuclear power: A new ITC for fuel, operating and maintenance costs at existing nuclear power plants (Section 48)

- Energy storage: An expansion of the ITC to include energy storage technologies like lithium-ion batteries (Section 48)

- Electric vehicles (EVs): A credit of up to $7,500 for each new electric vehicle sold (Section 30D)

- Biofuels: A suite of tax credits for advanced biofuel producers and blenders (Sections 40, 40A and 6426)

- Carbon capture utilization and storage (CCUS): A tax credit for capturing carbon for geologic storage or use in enhanced oil recovery or products (Section 45Q)

As a starting point, we use our Taking Stock 2019 current policy energy and emissions projections through 2030. This includes all federal and state policies on the books as of June of this year. All projections used in this analysis use RHG-NEMS, a version of the Energy Information Administration’s (EIA) National Energy Modeling System modified by Rhodium Group to reflect our own energy market and economic assumptions. We model most of the credits considered in this analysis in RHG-NEMS to quantify the impact on technology deployment and CO2 emissions reductions. We consider each category of tax credits on their own and assume each credit is in place through 2025 to inform the legislative process on the relative merits of extending each credit without having to account for potential interactive effects of combinations of credits. If a package of tax extenders advances in Congress, we will analyze that package in a future research note.

For each tax credit scenario, we consider a range of energy and technology costs to account for future market uncertainty. We account for the tax rules governing familiar incentives. Where commence construction safe harbor provisions are already in place, we include them in each scenario. Technologies at relatively early stages of deployment, including advanced biofuels, offshore wind, CCUS, and energy storage tax credit extensions, are assessed qualitatively outside of RHG-NEMS. While our scenarios do not represent specific legislative proposals, they are informed in part by bills submitted in this Congress sponsored by members of both parties.

Extending Electric Power Sector Credits Can Drive Large Near-Term Emissions Reductions

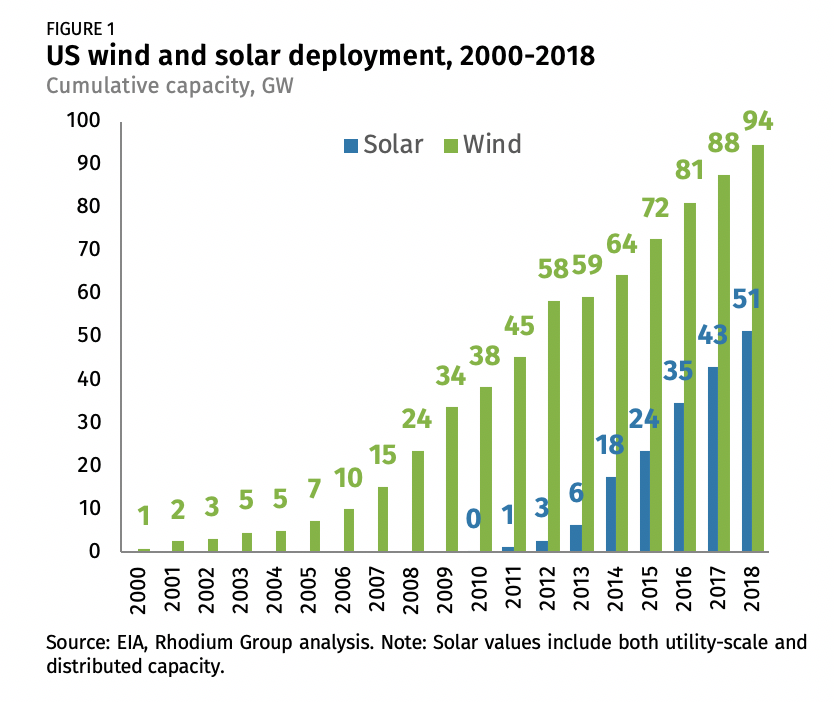

The Business Energy ITC and Renewable Energy PTC have supported the growth of the solar and wind industries since 2006 and 1991 respectively. Currently, the ITC provides a 30% tax credit, and the PTC provides a 2.5 cent per-kilowatt-hour credit for the first ten operating years of a plant. These tax incentives have bolstered deployment of solar and wind (Figure 1). Nevertheless, in 2018 solar and wind combined contributed just 8% of total electricity generation, while fossil fuels accounted for 64%. Achieving a decarbonized power sector requires even faster growth of these and other zero-carbon technologies. But the days of federal support for renewables are coming to an end. The value of these credits begins to phase down starting in 2020.

Credit extensions can maintain momentum for wind and solar

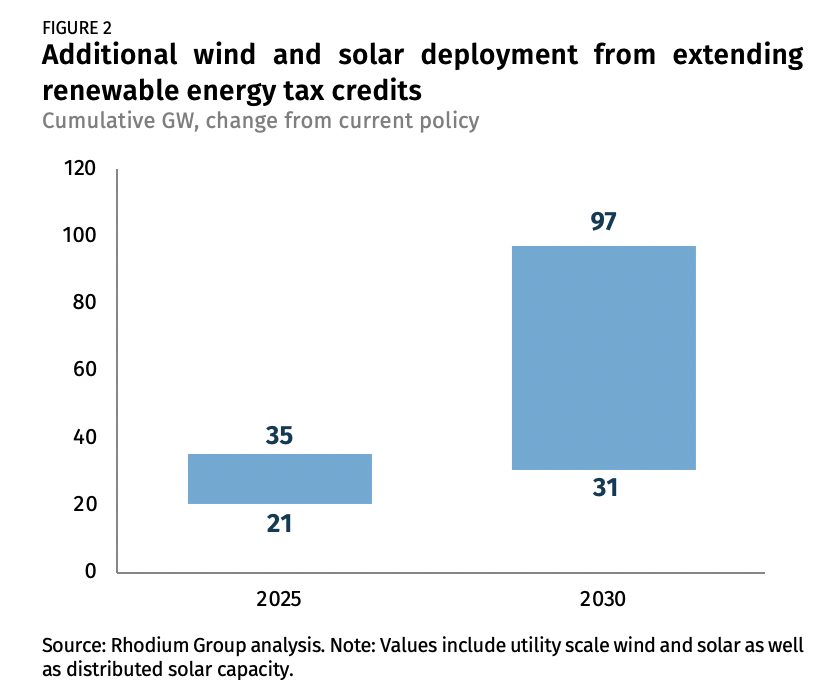

Extending renewable energy tax credits through 2025 can create new acceleration for the renewables industry. In 2025, we find an additional 21 to 35 gigawatts (GW) of solar and wind capacity online—above and beyond what would occur under the current policy where credits phase down (Figure 2). Substantially more capacity additions are squeezed into the following five years, as more plants finish construction in time to maintain eligibility for the tax credits. By 2030, extending renewable tax credits drives 31 to 97 GW of additional cumulative solar and wind capacity over current policy deployment. This results in 19% to 31% of total US electricity generation coming from wind and solar, roughly two to four times the market share held by these technologies today. The range of outcomes shows how the impact of extending renewable tax credits highly depends upon future gas prices and further progress in cutting renewable energy technology costs.

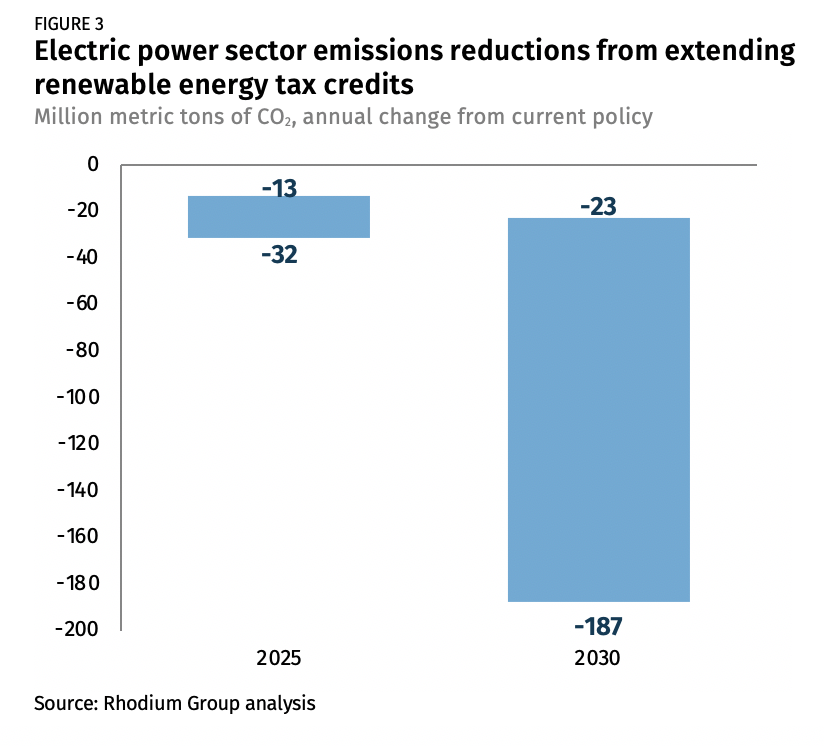

Extending renewable energy credits can also achieve meaningful progress towards reducing emissions. As more renewables come online, they displace incumbent generators, primarily natural gas-fired units. With more zero-emitting resources and less natural gas compared to current policy, electric power sector CO2 emissions fall 13 to 32 million metric tons below current policy in 2025 (Figure 3). Emissions reductions grow over time, reaching 23 to 187 million metric tons below current policy in 2030. The tax extension could push electric power sector emissions down 42% to 48% below 2005 levels in 2030.

Extending the Offshore Wind ITC can calm the permitting storm

Offshore wind has been slow to take off in the US compared to Europe and other markets. State policies have been put in place over the past several years to drive new development, especially in the windy and shallow waters off the Northeast coast. An ITC initially set at 30% for offshore wind has been phasing down over the last few years and will go to zero at the end of this year. Any project that meets the Internal Revenue Service (IRS) commence construction requirements before then will be able to receive a credit equal to 12% of total project costs.

If states meet all current procurement capacity, the US could see at least 20 GW of offshore wind installed by 2035. Developing offshore wind could bring much-needed diversity to natural gas-heavy grids such as New England’s or foster a wave of new clean energy jobs and manufacturing. But state goals are not guaranteed. Most state policies require offshore wind projects to benefit ratepayers by being reasonably cost-competitive over the long run. This high bar for the first wave of projects would be much easier to meet with federal tax credits in place.

Uncertainty surrounding permitting poses separate challenges for meeting state targets. The Department of Interior recently directed the Bureau of Ocean Energy Management (BOEM) to conduct a cumulative analysis of all proposed projects off the Northeast continental shelf. Regulators set no firm timetable for completion, placing all final permits for proposed projects on hold until the analysis is complete. In the meantime, the US has no domestic supply chain up and running to support offshore wind development. All turbine components are shipped across the Atlantic from Europe, adding costs. An extension of the ITC at the full 30% value through 2025 will help projects currently in limbo maintain their financing until BOEM’s review is complete. Beyond 2025, the tax credit can provide critical certainty for the industry to invest in a domestic supply chain that will bring down costs and increase American clean energy manufacturing. If all of these developments come to pass, US offshore wind costs will decline substantially as projects get built. This makes an extension of the federal ITC for offshore wind an important and potentially necessary complement to state deployment policies.

Tax credits to support nuclear can provide large but temporary emissions reductions

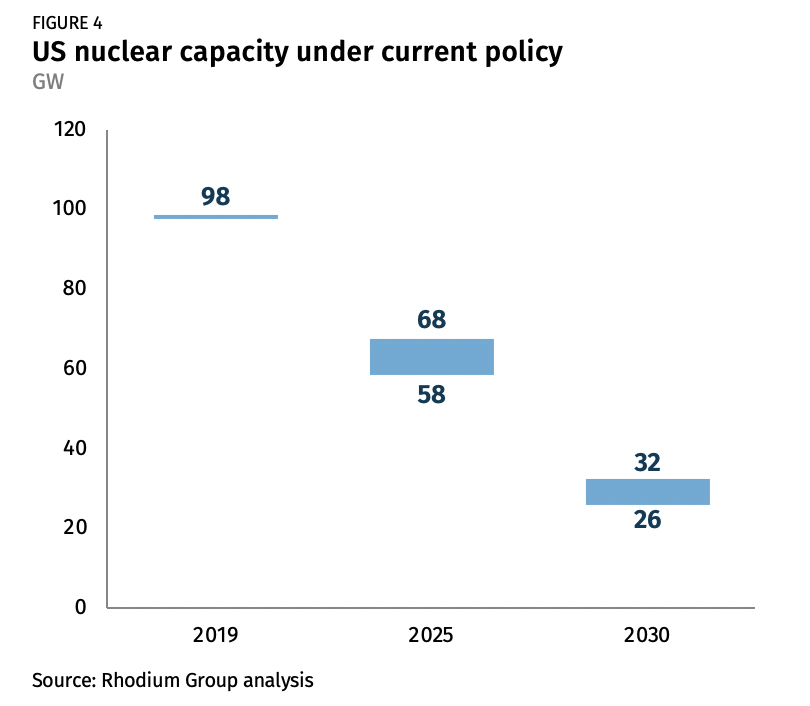

Nuclear power is the US’s largest source of zero-emission electricity, providing about 20% of total utility-scale electricity generation. But high operations and maintenance costs plus increasingly steep competition with cheap natural gas and renewables threaten the economic viability of existing nuclear plants. Under current policy, the US nuclear fleet could shrink from 98 GW today to 58 to 68 GW in 2025 and 26 to 32 GW in 2030 (Figure 4). Natural gas generation fills in behind most of these retirements, leading to higher CO2 emissions. Tax credit support for existing nuclear plants represents one way to provide a leg up for struggling plants.

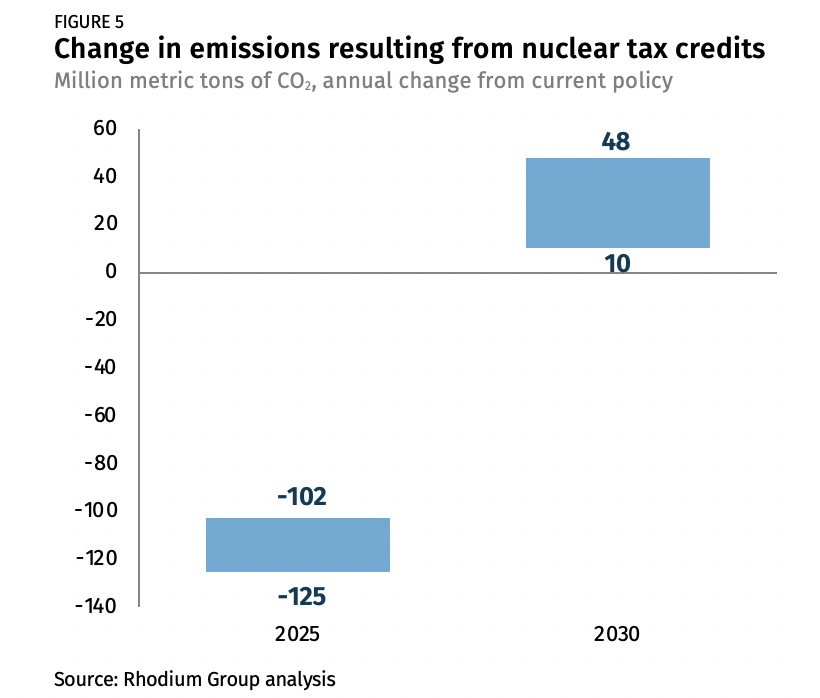

To assess a nuclear ITC, we assume the credit is sufficient enough to prevent the retirement of any nuclear plant that has not already publicly announced retirement. This means that the ITC saves 24 to 33 GWs of nuclear capacity through 2025. Preserving this zero-emissions capacity results in substantial and immediate emissions reductions. Under current policy, the US is projected to blow through its 2025 Paris Agreement commitment to reduce emissions, by at least 435 million tons of CO2. With the nuclear ITC in place, electric power sector emissions are 102 to 125 million tons lower in 2025 (Figure 5). This represents driving down US emissions roughly 25% closer to the Paris target.

Unlike extending renewable energy tax credits, the nuclear ITC delivers only temporary abatement. Once the tax credit expires at the end of 2025, a wave of nuclear plants relying on the credit retire absent additional policy action. These simultaneous retirements create an emissions rebound of 10 to 48 million metric tons of CO2 relative to current policy in 2030 because market dynamics shift back towards favoring fossil fuels. Supporting the current nuclear fleet, at least in the near-term, could buy time for broader policy action such as a carbon price or a clean energy standard that can provide long-term, predictable, market-based support for both the existing nuclear fleet and for long-term deep decarbonization of the electric system.

Expanding the ITC to energy storage can level the playing field

Significant energy storage capacity will be needed to achieve deep decarbonization over the long-term. This is especially the case if variable renewable generation from solar and wind end up playing dominant roles in the US electric power mix. Just as states led renewable deployment, they are now at the vanguard in setting ambitious storage targets to drive innovation and cost reductions. Meanwhile, the current solar ITC allows storage costs to be counted in credit valuation, but any stand-alone storage application does not receive federal tax credit support. As the technology takes off, these mismatched incentives will lead to inefficient investment and deployment of storage in places that are not ideal for the broader electric grid.

Expanding the current ITC to include all storage technologies will level the playing field and drive storage deployment where it’s most useful. It can also lower the cost to consumers from the rate impacts of meeting state storage mandates. Currently, lithium-ion storage technology with a discharge duration of 4 to 6 hours is the leading option in the storage space. As the US moves to a deeply decarbonized grid, longer duration storage technologies may be needed that can support seasonal imbalances in energy demand and production. A tax credit incentive that rewards storage for specific grid services, or at least provides more support for technologies at earlier stages of development, could be important to drive investment into a broad portfolio of storage technologies.

Tax Credit Extensions Can Kick EV Sales into High Gear

While power sector emissions are on the decline, thanks in part to the influx of renewables, transportation emissions have risen in recent years. In fact, the transportation sector has been the US’s top-emitting sector since 2016. Transportation is difficult to decarbonize due to a range of issues, such as slow stock turnover, lack of affordable low-carbon substitute fuels, and the high cost of electric vehicles. One way to decarbonize light-duty transportation is to simultaneously electrify vehicles and decarbonize the electric power sector. Rapid technology development has already lowered EV prices through steady reductions in battery costs by over 80% since 2010. Still, the average EV remains more expensive than the average internal combustion engine (ICE) vehicle.[4]

As technology continues to improve and costs continue to drop, EV tax credits can provide that extra bit of incentive for consumers to make the switch to electric. New battery electric vehicles (BEV) and plugin hybrid electric vehicles (PHEV) purchased starting in 2010 are eligible for a federal tax credit of $2,500 to $7,500, depending on the vehicle’s battery capacity. However, the credit applies only to the first 200,000 eligible vehicles sold by each manufacturer, after which it phases out. Tesla and General Motors hit this 200,000-vehicle cap in 2018 and 2019, respectively, and are now in the process of phasing out the credit.

Tax credits nearly double EV growth through 2025

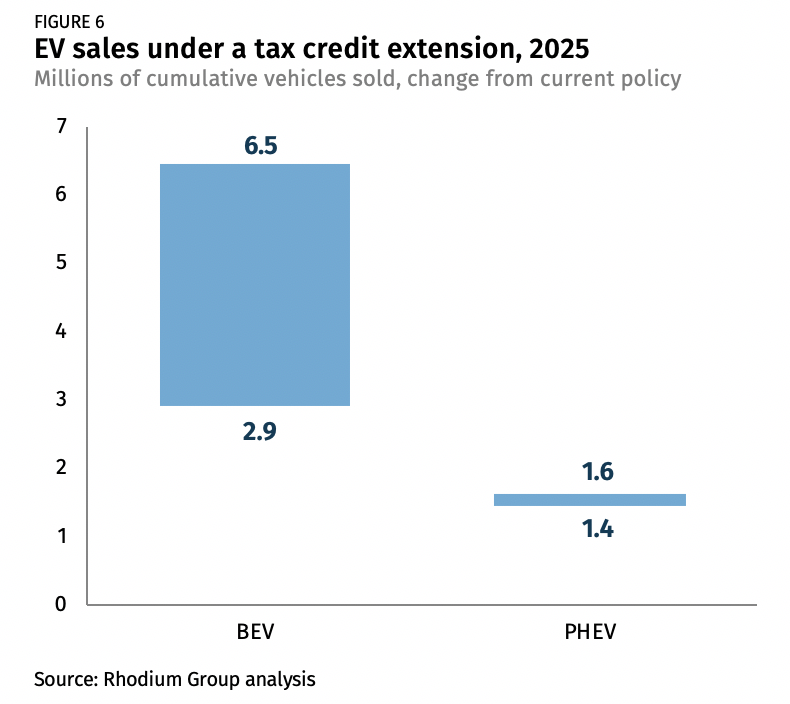

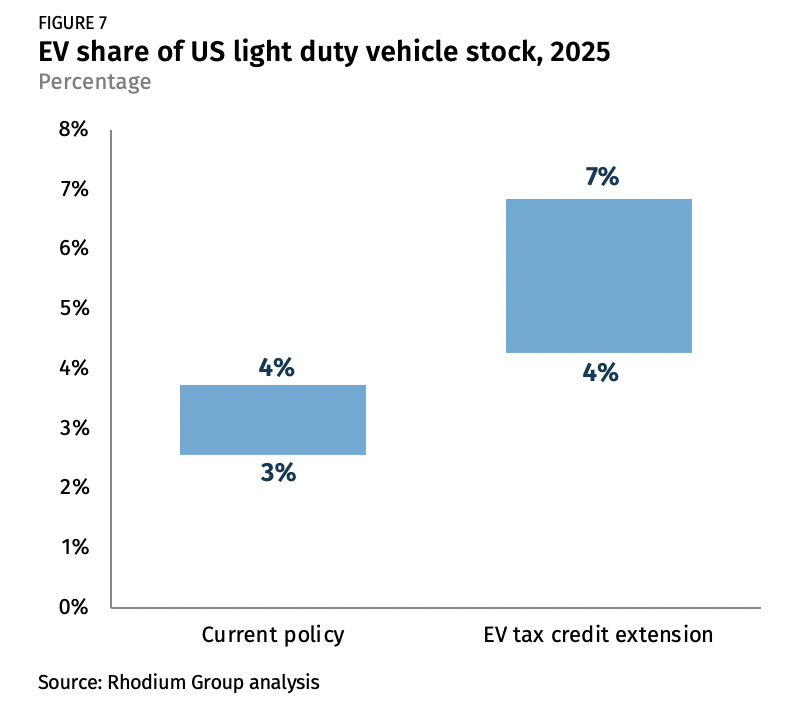

Extending the current tax credit through 2025 with no cap for all vehicle manufacturers will push millions of new EVs onto America’s roads. We find that an additional 2.9 to 6.5 million BEVs and 1.5 to 1.6 million PHEVs are sold through 2025 compared to current policy (Figure 6). This represents nearly double the EVs on the road in the US compared to current policy in that year (Figure 7). The range reflects uncertainty around oil prices and EV battery costs.

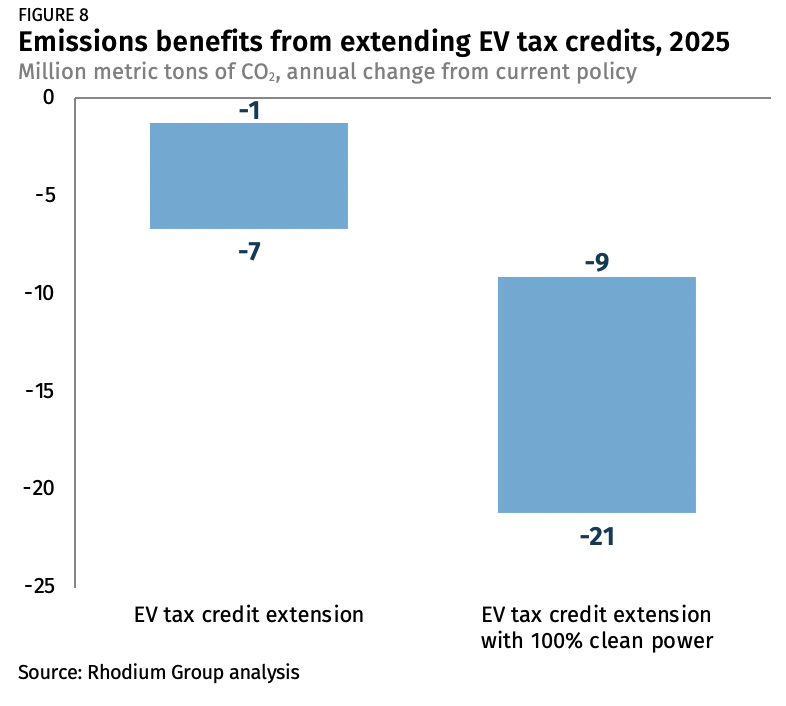

Due to the combination of slow stock turnover and a relatively carbon intensive power sector, EV tax credits yield small emissions benefits in the near term. We find that the tax credit extension reduces transportation emissions by 1 to 7 million metric tons of CO2 in 2025 (Figure 8). The near-term emissions impact may be small, but EV tax credits put more EVs on the road, supporting the industry at a critical time. While sales have been increasing rapidly over the past few years, EVs remain a relatively early-stage technology. Incentives and policies that speed up deployment today will drive further technology development, drive down costs and increase customer acceptance. They will also assist the development of the infrastructure (e.g. public charging networks) necessary for a deeply decarbonized future. Meanwhile, if the US does decarbonize electric power, then the emissions benefit of extending EV tax credits through 2025 would expand to 9 to 21 million metric tons in 2025 (Figure 8).

Tax Credits Can Accelerate Low-Carbon Fuels

Replacing gasoline and diesel fuels with low-carbon substitutes can help to reduce transportation emissions while light-duty and medium-duty vehicles transition towards electrification. They are also needed to decarbonize areas of transportation such as shipping and aviation, where electrification isn’t practical. Key supply options for low-carbon fuels include biofuels and synthetic fuels. Biofuels derived from plants and waste make up 5% of current US liquid-fuel demand and synthetic fuels made with captured CO2, hydrogen, and other inputs are in the demonstration phase. Currently, conventional ethanol is the most economic and prolific biofuel supply option, making up 88% of the total biofuel market. Though conventional ethanol has a lower life cycle emissions profile than gasoline, even less carbon-intensive biofuel options will be needed in a low-carbon future. These low-carbon biofuels, referred to as advanced biofuels, include biodiesel and cellulosic ethanol. Because they are expensive to produce, advanced biofuels have struggled to penetrate the fuel market—current levels are less than 1% of total US liquid-fuel demand.

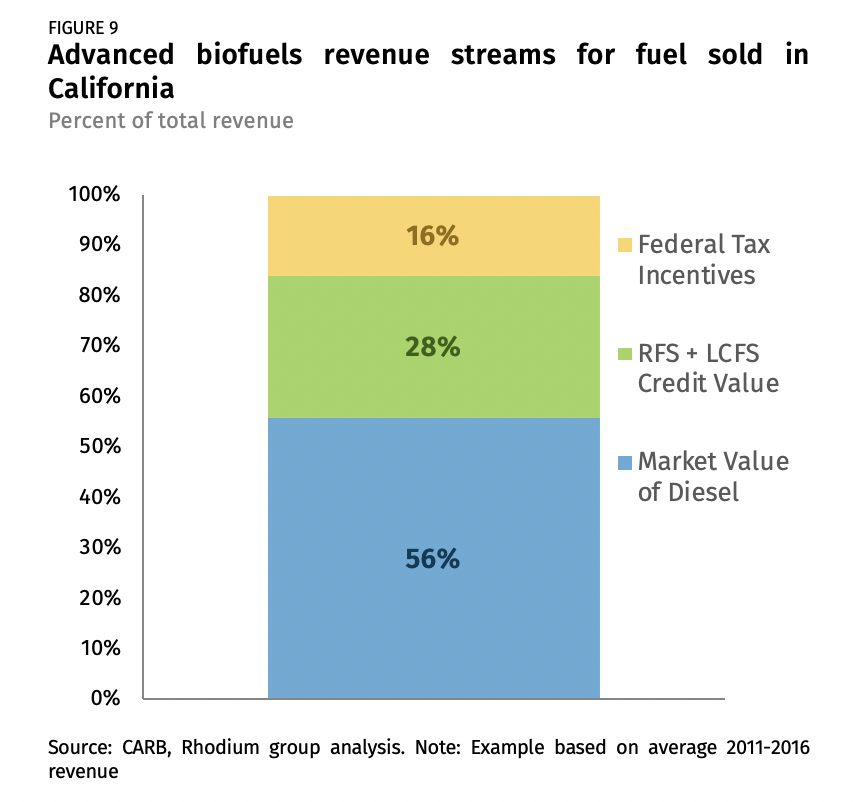

In order to stay in operation, most advanced biofuel producers look to price signals from multiple policy and market incentives illustrated in Figure 9. These include state-level policies like the California Low-Carbon Fuels Standard (LCFS), the Renewable Fuel Standard (RFS) Renewable Identification Number (RIN) credits and several currently-expired federal tax credits aimed at different advanced biofuel producers and blenders (e.g. the Second Generation Biofuel Producer Tax Credit, the Biodiesel Income Tax Credit and the Biodiesel Mixture Excise Tax Credit).

Bolstered by this combination of revenue sources, advanced biofuels consumed in the California market doubled over the past five years. Despite this success, the advanced biofuels industry has struggled to make progress nationally due to the inconsistent price signals from federal policy, including tax credits and the RFS. Advanced biofuel tax credits for producers and blenders have been subject to short-term extensions, expirations, and even retroactive extensions. This inconsistency combined with RFS rule revisions, annual waivers of compliance obligations, and the looming 2022 program expiration cause multiple sources of uncertainty for the advanced biofuel industry. Without market certainty, it’s not clear to advanced biofuel producers what the long-term value of their product is.

With relatively cheap oil prices and the unreliable nature of key policy mechanisms, the advanced biofuels industry faces a steep climb just to keep current plants in operation, let alone accelerate deployment. Extending the suite of current advanced biofuels tax credits for five years is one way the federal government can provide a lifeline and, potentially, a bridge to a more reliable policy landscape. Another option that could provide the same incentive to a wider array of fuels involves consolidating all advanced biofuels tax credits into a single low-carbon transportation fuel credit with a value based on the lifecycle carbon intensity of the fuel relative to fossil fuels. This technology-neutral approach could enable the development of a more robust competitive low-carbon fuels industry needed to decarbonize the energy system in the long run.

Tax Credits Could Help the US Maintain CCUS Leadership

CCUS technologies capture CO2 from factories, power plants, and other sources. From there, the captured CO2 can be stored deep underground or used as a feedstock for products or for enhanced oil recovery (EOR). CCUS added to existing facilities or included in new infrastructure will be an important technology for decarbonizing the industrial sector, where low-carbon fuels and electrification are either too expensive or not feasible. CCUS is the only technology that enables fossil-fuel fired power plants to play a significant role in a decarbonized electric system. In previous research we found that carbon removal using a CCUS technology called Direct Air Capture (DAC) will be a critical technology for the US to meet deep decarbonization goals alongside renewables, efficiency, electrification, low-carbon fuels, and other key solutions.

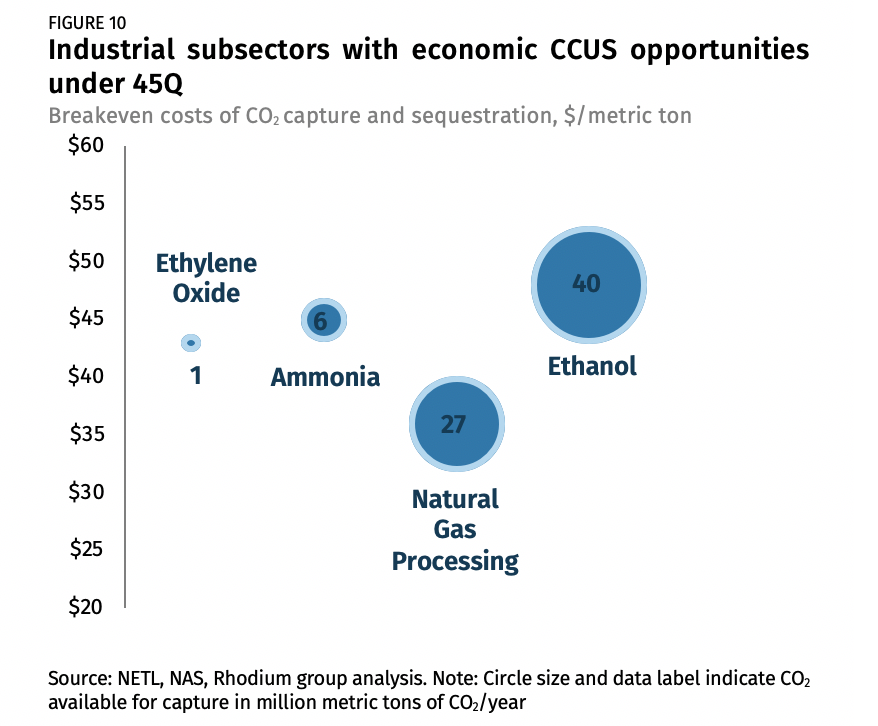

The US has invested heavily in CCUS research and development and leads the world in deployment policy support. The Section 45Q tax credit (45Q) is the marquee federal policy incentive for CCUS deployment and plays a critical role in reducing costs and mobilizing investments in the first wave of projects in the US. Section 45Q provides CCUS projects up to $50 per ton of carbon captured and directly sequestered, and up to $35 per ton of carbon sequestered via EOR or used in products. To qualify for 45Q, a project must commence construction before January 1, 2024. Once a project has qualified, projects can claim the tax credit for 12 years.

Before Congress improved 45Q in 2018, CCUS technologies struggled to compete financially. With 45Q in place, CCUS now makes economic sense for several industrial subsectors with relatively pure CO2 emissions streams, such as ethanol production and natural gas processing (Figure 10). If all of these opportunities are pursued, 74 million metric tons of annual emissions can be captured. Meanwhile, a west Texas project to construct the largest DAC plant in the world, 250 times larger than anything in place today, will rely on 45Q.

However, the IRS is behind schedule in finalizing guidelines for 45Q claims. Without concrete guidance from the IRS, companies do not have the certainty they need to move forward with the first wave of CCUS projects. Meanwhile the window for breaking ground shrinks each day that guidance is delayed. Extending 45Q through 2025, will give CCUS project developers flexibility and certainty while they await IRS guidance. The longer time horizon could increase the number and diversity of projects.

There are other ways 45Q could be enhanced to drive more deployment of CCUS and provide additional certainty for project developers. Extending the payout period beyond the current 12 years would lock in emission reductions over longer periods of time. For DAC, a technology at an earlier stage of development than other CCUS options, a higher credit value just for this technology could drive a wave of new projects. The longer the runway of support for these critical but early-stage technologies, the better the chance they will be available at the scale needed for deep decarbonization in the decades ahead.

All Eyes on Congress

Clean energy tax credits can provide market certainty and accelerated deployment of technologies that are key for long-term decarbonization of the US energy system. Additionally, extending and expanding zero-emissions electricity tax credits or 45Q can deliver meaningful progress in reducing emissions over the next decade. Heading into the fall, we will track developments in Congress. Should a tax package advance, we will assess the implications for clean energy technology deployment and cutting greenhouse gases.

Related Work: An Assessment of the GREEN Act (Dec 2019)

[1] This nonpartisan, independent research was conducted with support from the William and Flora Hewlett Foundation and the Heising-Simons Foundation. The results presented in this report reflect the views of the authors and not necessarily those of supporting organizations.

[2] For more on the energy system transformation required to achieve decarbonization see Chapters 2 and 5 of Larsen, et al. 2019 as well as Haley, et al. 2019

[3] Other credits in place or that have recently expired that focus on other sectors are out of scope for this analysis.

[4] Throughout this note EV’s refer to both plugin hybrid and battery electric vehicles.