China’s Next-Generation Industrial Policy

China’s industrial strategy now touches almost every major sector in the economy and their underlying supply chains. These state interventions are accelerating China’s trade dominance and expanding foreign dependence on Chinese supply chains.

U.S. Chamber of Commerce Preface

A decade after Made in China 2025 (MIC25), China is entering a new phase of industrial policy. Rather than retreating in the face of mounting domestic and international pressures, Beijing is doubling down. State intervention across the economy is becoming broader and more consequential for global markets than ever.

This report assesses how China‘s industrial strategy is evolving and what it means for global competition. Two overarching conclusions emerge. First, China‘s industrial policy is becoming more systemic and pervasive, extending across all layers of production from upstream inputs and industrial equipment to downstream applications, services, and frontier technologies. Second, these domestic dynamics are ushering in a new phase of global impact, characterized by accelerating trade dominance, deepening foreign dependencies on Chinese supply chains, and the rapid global expansion of Chinese firms. Beijing also increasingly deploys policy tools to entrench its dominant position in global value chains and counter foreign diversification strategies.

These conclusions, while significant, are not without precedent, and the analytical foundation for understanding them was laid years ago, in large part by the business community itself.

In late 2015, the U.S. Chamber of Commerce identified and translated the foundational planning document—commonly referred to as the “Green Book“—that set out the localization targets and strategic roadmap underpinning Made in China 2025. That translation was shared broadly with companies, governments, and leading research institutions, and it served as the basis for a series of independent assessments that followed: most notably by the Mercator Institute for China Studies (MERICS) in 2016, the European Union Chamber of Commerce in China in 2017, and the U.S. Chamber of Commerce in 2017.

Published within months of one another, these three reports delivered a strikingly consistent message:

- MERICS (2016): “If China succeeds with ‘Made in China 2025,‘ foreign companies and industrial countries will find themselves confronted with a powerful competitor backed by massive state support across a wide range of advanced manufacturing industries.“

- EU Chamber of Commerce in China (2017): “If implemented as currently envisaged, China Manufacturing 2025 risks distorting markets, crowding out foreign competitors, and fundamentally undermining the principles of fair competition.“

- U.S. Chamber of Commerce (2017): “Made in China 2025 represents a decisive shift away from market-oriented reform toward state-directed economic outcomes, with profound implications for global competitiveness and US economic interests if left unaddressed.“

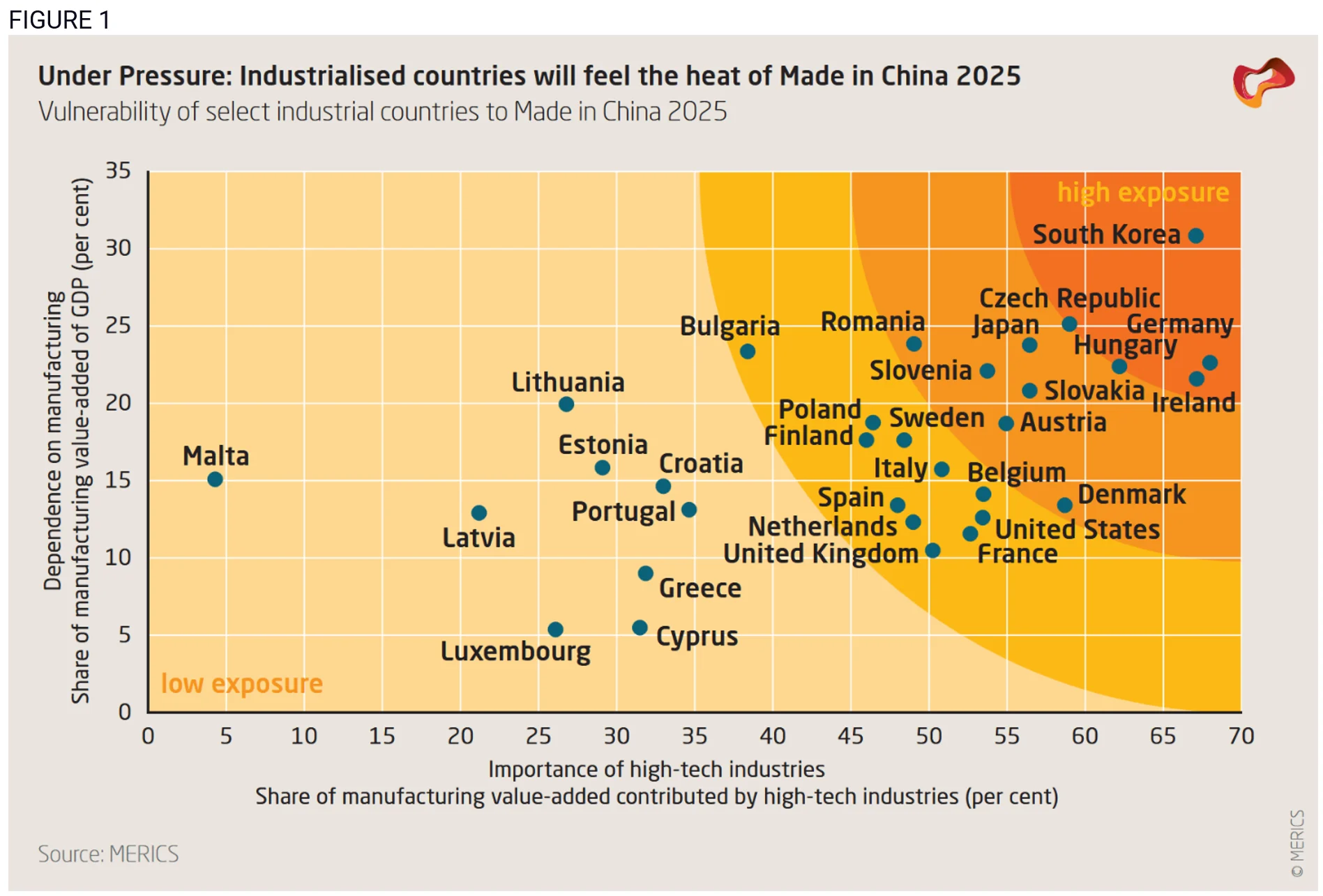

The analysis was clear. The evidence was made widely available. And the implications were articulated in direct terms across multiple credible, independent sources. One widely cited visual distillation was the 2016 MERICS Made in China 2025 Heat Map, which starkly illustrated the exposure of major manufacturing powers—South Korea, Japan, and Germany, along with other European industrial economies—to the blast radius of competitive pressure unleashed by China’s industrial push (Figure 1).

In the years that followed, China executed much—though not all—of the strategy it had outlined. A comprehensive assessment commissioned by the U.S. Chamber and prepared independently by Rhodium Group, Was Made in China 2025 Successful? (May 2025), confirmed that outcomes tracked the original ambitions to a striking degree. China made substantial progress in reducing import dependencies, displacing foreign firms in domestic markets, and building globally competitive positions in sectors ranging from new energy vehicles to information and communications equipment. At the same time, the Rhodium Group assessment found that significant vulnerabilities persist—particularly in high-end semiconductors, advanced aerospace, biomedicine, and other areas where Chinese firms have not yet closed the technological gap. The picture that emerges is not one of uniform success, but of a state-driven industrial campaign that achieved many of its core objectives while falling short in some of the most technologically demanding sectors. The competitive dynamics and supply chain shifts that were forecast a decade ago have, in large measure, become embedded features of the global industrial landscape. In hindsight, the early warnings were not alarmist—they were, if anything, measured.

It is worth acknowledging plainly that the challenge the world now faces is not the result of an intelligence gap. The translations existed. The reports were published. The warnings reached senior levels of government and industry across major economies. Yet in too many cases, the response was insufficient—whether due to competing priorities, political constraints, or a belief that market forces alone would provide an adequate counterweight. The costs of that delayed response are now visible in lost competitiveness, diminished industrial capacity, and strategic vulnerabilities that will require sustained effort to address.

This report is offered in the same constructive spirit as those earlier assessments: as a rigorous, evidence-based analysis of where China‘s industrial policy stands today and where it is heading. The Chamber‘s role is not to dictate policy, but to ensure that decision-makers in government, industry, and multilateral institutions have access to the clearest possible picture of the competitive landscape. The record of the past decade carries a straightforward lesson: When credible analysis is available and the trajectory is visible, the window for effective action is finite. What follows is an assessment of the next phase of China‘s industrial evolution—and of the strategic choices it presents.

Executive summary

China’s industrial strategy is evolving in two significant ways. First, it is becoming more systemic and pervasive, extending across all layers of production, from upstream inputs and industrial equipment to downstream applications, services, and frontier technologies. Second, these domestic dynamics are accelerating China’s trade dominance, deepening foreign dependencies on Chinese supply chains, and the rapid global expansion of Chinese firms in global markets. Beijing is also increasingly deploying policy tools to entrench its dominant position in global value chains and deter foreign diversification strategies.

A more expansive industrial policy

China’s next-generation industrial policy represents a shift from targeted sectoral intervention to what can be described as an “industrial policy of everything.” While MIC25 focused on a defined set of strategic emerging industries, current policy frameworks extend across mature sectors, foundational supply chain nodes, and frontier technologies alike. Chinese leadership views past policies as largely successful in building domestic capabilities and global competitiveness, even as they identify areas to improve policy execution and remain keenly aware of persistent technological dependencies in high-tech inputs. Beijing is not abandoning mature sectors but is instead pushing them toward higher-value segments, while focusing on new products and technologies. In several upstream segments, including critical minerals, wafers, and magnets, China already holds dominant positions, and policymakers are now seeking to extend this across a broader range of industrial products.

Even in mature industries facing overcapacity and severe price pressures, Beijing is providing continued support and pushing firms to upgrade production technologies to gain market share and lower production costs, rather than cutting capacity. While authorities have acknowledged the need to address imbalances, policy responses have so far fallen short of the structural reforms required to shift China’s growth model. Efforts to boost consumption also remain limited, leaving underlying demand weaknesses largely unaddressed.

Services, relatively neglected in earlier rounds of industrial policy, are getting more attention, with visible gains in areas like software, data processing, and drug development. Policymakers also view the current moment as a window of opportunity to pull ahead in disruptive technologies like artificial intelligence, quantum, and future energy systems, mobilizing China’s entire economic system to gain a foothold in future industries. These new technologies are no longer treated solely as areas for R&D and innovation. They are now also supported with public procurement and state-owned enterprises generating demand and adoption of new products at scale. AI has emerged as a central pillar, but the broader pivot to demand creation represents a step change in the leadership’s willingness to fund commercialization of cutting-edge technologies.

Refining the policy playbook under tighter constraints

This expansion is occurring in a more constrained macroeconomic environment. China faces slowing growth, weak domestic demand, rising fiscal pressures, and declining efficiency of capital allocation. Rather than scaling back intervention, Beijing is adapting to these constraints by recentralization and tighter coordination of financial resources. Authorities are strengthening control over fiscal spending, bank lending, capital markets, and state investment funds to ensure that scarce resources are directed toward strategic priorities. Government guidance funds are being consolidated and aligned more closely with national objectives, while bank lending is increasingly steered through targeted relending facilities and regulatory guidance, and wasteful or redundant tax and fiscal subsidies are being culled, especially at the local level. After decades of liberalization, the leadership is re-inserting non-market considerations into the DNA of banks, state-owned enterprises, and investment markets in ways that may prolong the potency of industrial policy, but which will have long-term ramifications for China’s overall economic vitality and efficiency.

However, the expansion of industrial policy across an ever-wider set of sectors risks diluting its effectiveness, while increasing state influence on financial markets may further reduce resource allocation efficiency. Evidence of strain is already visible in declining corporate profitability, weakening private investment, and slowing R&D growth in key sectors. Over time, these dynamics could weigh on China’s productivity and long-term growth potential, even as they support short-term industrial gains.

A new phase of global impact

The global impact of China’s industrial and economic policies has accelerated in the past three years and will likely continue to expand rapidly. The combination of sustained policy support and weak domestic demand has driven a rapid expansion of China’s manufacturing trade surplus, which many observers describe as a “China Shock 2.0.“ Since 2019, the surplus in manufacturing goods has roughly doubled to around $2 trillion, reflecting both rising exports and successful import substitution, and these trends are expected to grow.

While China’s most dramatic market share gains in the 2020s were in electric vehicles and clean energy, its current expansion is increasingly concentrated in key upstream segments of global value chains, such as chemicals, machinery, and industrial equipment—segments traditionally dominated by advanced economies. Chinese inputs and capital goods are increasingly also embedded in products manufactured and exported by third countries, creating indirect dependencies that are difficult to detect and manage. This expansion is also systematically underestimated, as falling producer prices mask the true pace of market share gains: Measured in volume, China’s market share gains are roughly twice as large as in value terms for many products.

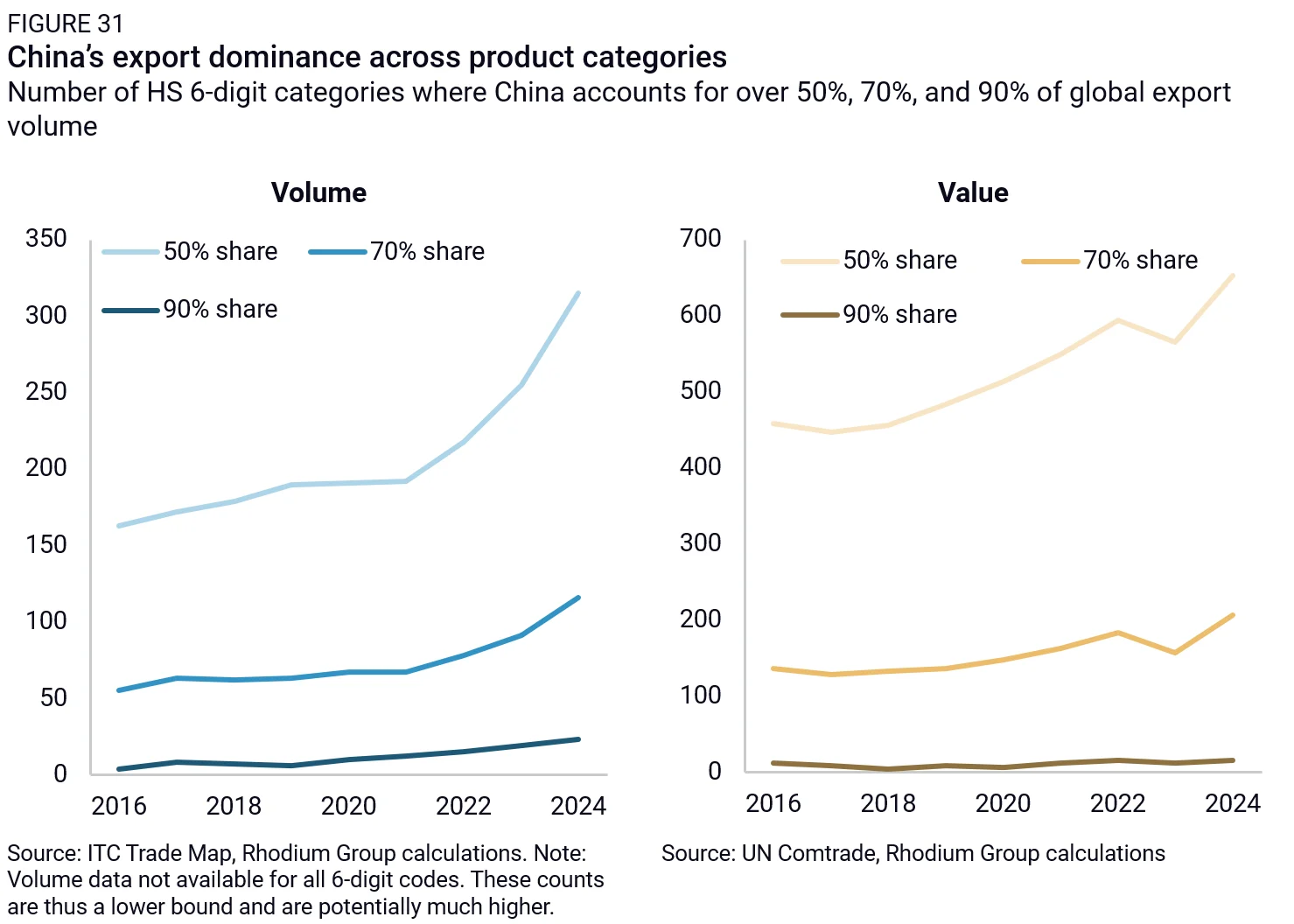

As a result, global reliance on Chinese supply chains is deepening across a growing number of critical products. The number of products where China accounts for more than 50% of global exports, for example, nearly doubled between 2021 and 2024, from 192 to 315. China’s dominance of global manufacturing began with downstream assembly for foreign value-added, but has now flipped—extending into upstream materials, components, and production equipment, giving it increasing leverage over global industrial systems.

Beijing is actively reinforcing its control over value chains using regulations and economic coercion to pre-empt de-risking and lock in its dominance across critical supply chains. It has tightened controls on critical minerals and processing technologies, extended restrictions to downstream products through extraterritorial rules, and introduced new legal instruments that raise the cost for firms and governments seeking to diversify away from China.

Chinese firms are emerging as major global competitors, but Beijing is intent on ensuring that this overseas expansion does not lead to a hollowing out of production or capabilities in China or a loss of control over key supply chains. Overseas investment remains limited relative to domestic production, accounting for only a small share of firms’ total capital expenditure. Chinese firms typically localize assembly or sales abroad while continuing to rely on inputs, components, and technologies sourced from China. As a result, outward investment often reinforces, rather than reduces, global dependence on Chinese manufacturing.

Implications for global competition

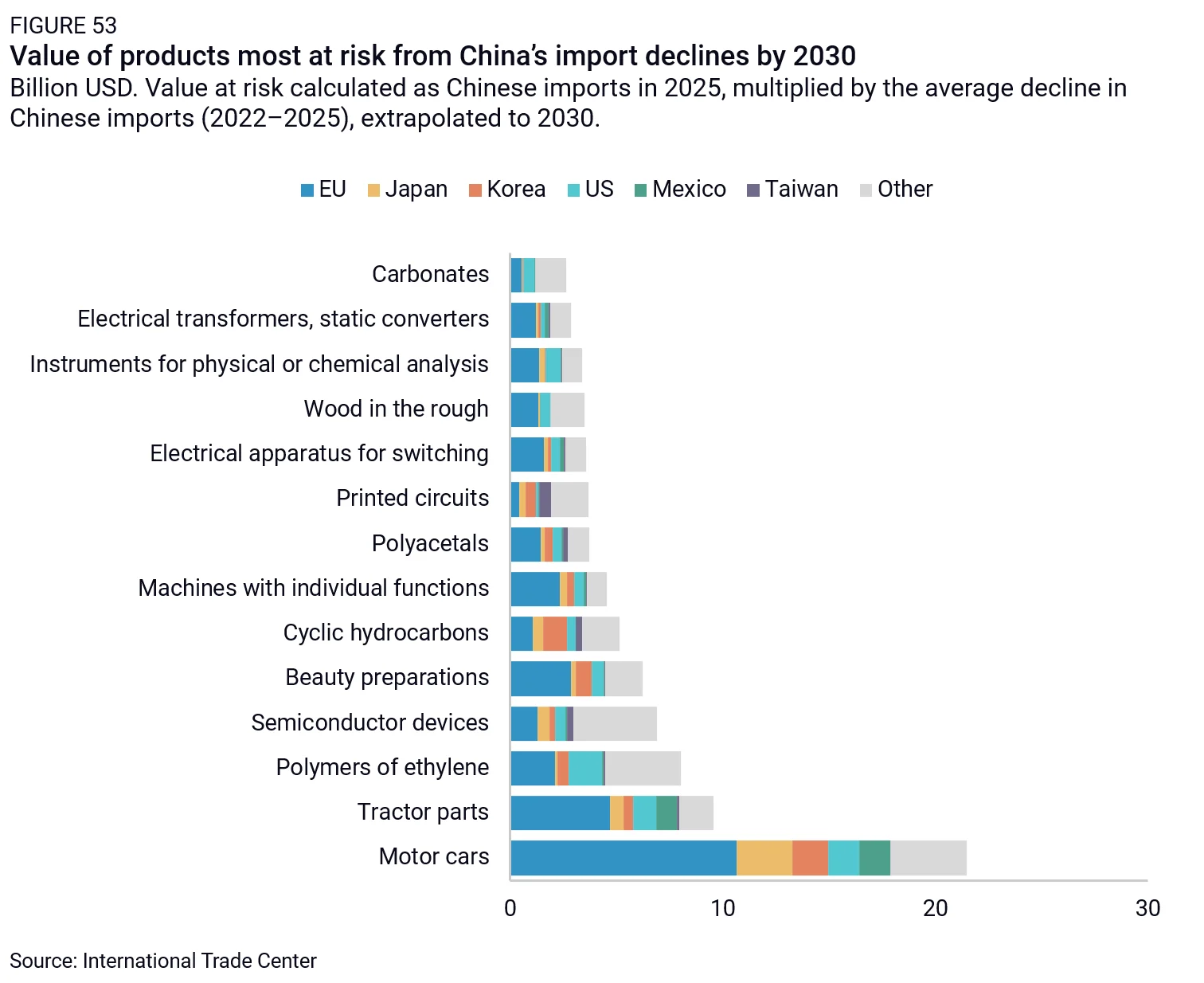

Advanced industrial economies face the risk of sustained erosion in manufacturing competitiveness, particularly in sectors such as automotive, machinery, and chemicals. In aggregate, up to $650 billion—equivalent to around 12% of G7 manufacturing exports—could be directly exposed to Chinese market share gains by 2030 if they continue at the current pace. Over time, this could trigger broader effects, including declining investment, weakened innovation ecosystems, and the loss of industrial capabilities. Emerging economies also face challenges, as China’s continued upgrading limits opportunities to move up the manufacturing value chain. Growing dependence on Chinese supply chains raises strategic vulnerabilities. As China’s control over critical inputs and technologies expands, so too does its ability to weaponize this leverage.

The window for effective policy response is narrowing. While many governments have begun to react through trade defense measures, industrial policy, and efforts to de-risk supply chains, responses remain fragmented and largely uncoordinated. This risks amplifying trade diversion, duplicative investment, and intra-allied competition, while leaving underlying imbalances unaddressed. Without more coordinated action, China’s industrial policy is likely to continue reshaping global markets, entrenching dependencies, and eroding industrial competitiveness across both advanced and emerging economies.

Chapter 1: China’s next-generation industrial policy

China’s economic policy strategy is increasingly oriented around its aggressive pursuit of self-reliance, import substitution, technological leadership, and dominance across critical global value chains. China’s industrial policy extends far beyond traditional tools like subsidies or tax incentives to a pervasive, system-wide state role in shaping the economy. Chinese policymakers appear convinced that they have found a superior model that delivers results. Though cognizant that their model has shortcomings and produces unintended consequences, they believe they can refine and expand it to new industries and niche supply chain nodes to fuel economic growth, technological upgrading, and global competitiveness across multiple sectors.

This confidence is driving an expansion of policy ambition. Industrial policy is no longer confined to high-priority final goods but is increasingly focused on the foundational layers of production—materials, components, machinery, and industrial services—that underpin the entire industrial system. In several of these upstream segments, from critical minerals to wafers and magnets, China already holds dominant positions, and policymakers are now seeking to extend this across a much broader range of industrial products. Services, relatively neglected in earlier rounds of industrial policy, are getting more attention, with visible gains in areas like software, data processing, and drug development. Policymakers also view the current moment as a window of opportunity to pull ahead in disruptive technologies like artificial intelligence, quantum, and future energy systems, mobilizing China’s entire economic system to gain a foothold in future industries. Meanwhile, even in the face of excess investment and severe price pressures, Beijing is providing increased support and pushing mature sectors to upgrade and gain market share, rather than cutting capacity.

Yet Beijing is also confronting quickly growing constraints in its fiscal and financial system, which suffers from decades of misallocation. This evolution is unfolding against a weaker macroeconomic backdrop where growth is slowing, productivity growth is stagnant, and domestic demand is weak. Rather than retreating, Beijing is intensifying its control over the allocation of resources, both public and private. After decades of liberalization, the leadership is re-inserting non-market considerations into the DNA of banks, state-owned enterprises, and investment markets.

This chapter examines how China’s industrial policy is evolving, both in terms of its sectoral scope, and the instruments used. The first section looks at the sectoral expansion of China’s industrial policy to a wide range of critical inputs throughout the supply chain, to mature industries, to frontier technologies, and services. The second section examines the new instruments Beijing uses to tighten control over financial and capital markets to ensure that scarce resources flow to strategic sectors.

1. An industrial policy of everything

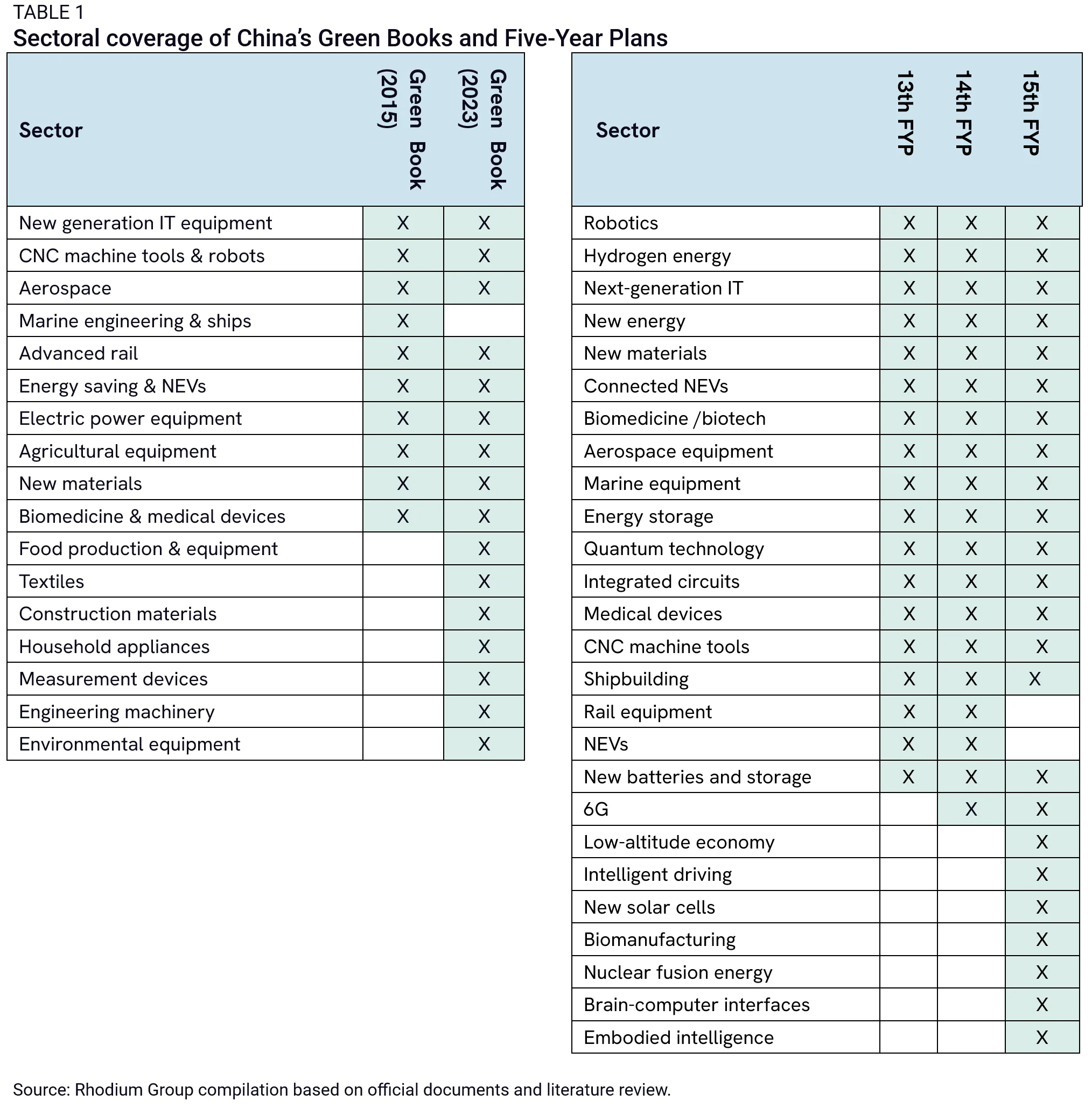

China’s leadership appears confident that its industrial policy playbook is working, despite the need for targeted adjustments. They are actively refining and expanding their policy focus to cover a huge range of industries and supply chains. The elevation of “new industrialization” to a central national priority, alongside repeated emphasis on strengthening supply chains and advancing technological self-reliance, shows industrial policy is at the center of all economic policy. Made in China 2025 (MIC25) largely focused on industries where Chinese companies still had to catch up, such as next-generation IT, high-end equipment, and new materials. This was seen in the original technology roadmap (the Green Book) accompanying MIC25. But now, coverage is expanding: A revised version of the Green Book released in 2023 included several traditional industries such as textiles and household appliances, as well as equipment such as measurement devices and engineering machinery. The latest 15th Five-Year Plan (FYP) issued in March 2026 expanded its sectoral coverage to many more frontier technologies, such as biomanufacturing, embodied intelligence, and intelligent driving (Table 1).

This sectoral expansion, from mature industries to cutting edge technologies, suggests that China’s industrial policy is evolving from a strategy focused primarily on breakthroughs in strategic sectors toward a broader effort to reshape the entire industrial ecosystem. The growing sectoral breadth of these objectives is complemented by an increasingly granular, product-level mapping within each sector, with different segments of the same industry subject to different policy objectives. The result is a much more comprehensive effort to target specific niche technologies and capabilities.

This section examines in more detail the expanding sectoral scope of China’s industrial policy, looking at emerging industries, established industries, frontier technologies, and services.

Strategic emerging industries and supply chain chokepoints

Beijing’s national industrial policy initiatives of the past decade have targeted a range of advanced manufacturing sectors, notably through MIC25 and the Strategic Emerging Industries (SEI) framework, introduced in 2010 and updated in 2016. While the emphasis differs across these policy frameworks, these industries share common characteristics: The Chinese leadership believes they underpin future economic growth and global competitiveness, and they are areas where China has faced persistent dependence on foreign technologies. These industries, from semiconductors to robotics and advanced pharmaceuticals, remain at the forefront of China’s industrial policy strategy.

However, as China progressively reaches greater self-sufficiency across sectors, its sectoral targets are shifting. Beijing is still laser focused on eliminating its dependencies on foreign countries for the most critical technologies. According to the 15th Five-Year Plan, it is implementing “extraordinary measures to achieve decisive breakthroughs in key core technologies” in sectors where it still lags foreign competitors. These are identified in the plan as “integrated circuits, industrial machine tools, high-end instruments, basic software, advanced materials, and biomanufacturing,” a list we also noted in previous reports (Was Made in China 2025 Successful?).

By contrast, some sectors such as high-speed rail or shipbuilding have moved out of the core policy spotlight, reflecting their global competitiveness and technological maturity. This does not mean support has disappeared. Leading firms continue to receive substantial state backing: For example, CRRC remains the 7th largest recipient of direct subsidies among listed companies, and China Shipbuilding Industry Company ranks within the top 3%. This is because support in China’s system is persistent, not temporary: Firms enter the policy ecosystem but rarely exit, especially when they are central state-owned enterprises.

In other sectors where China’s industrial upgrading has been extremely successful, like clean tech and automotives, policy attention shifts within them toward more advanced and specialized segments. For example, moving from batteries in MIC25 to “new types of batteries” in the 15th Five-Year Plan, from solar to “new solar cells,” and from NEVs to “connected and smart NEVs.” This reflects a continuous upgrading logic, where achieving dominance at one stage prompts a move to the next technological frontier.

While MIC25 emphasized catching up and attaining leadership in a set of strategic emerging end-use industries, Beijing is strengthening its focus on addressing gaps in the underlying layers of production across the entire economy. The objective of targeting supply chain chokepoints is not new: It was introduced in 2014 through the “four industrial foundations” framework and subsequently embedded in a range of targeted policy initiatives. But there are clear signs that this objective has since been elevated, with new tools and resources deployed to target specific nodes in supply chains. Official documents consistently stress that China’s manufacturing system is “broad but not strong,” with persistent weaknesses in foundational inputs. This shift is visible in successive five-year plans. References to “industrial foundations” and “industrial chains” rose sharply in the 14th and 15th Five-Year Plans, and the 14th Plan introduced the concept of “industrial foundation re-engineering,” signaling the renewed attention to strengthening underlying capabilities.

The list of supply chain gaps to address is also broadening. The earlier focus on the “four industrial foundations” (basic components, materials, processes, and technology platforms) expanded to six in the 2021 “Catalog of Industrial Foundation Innovation and Development,” adding industrial software and high-end equipment. The Catalog shifted from a targeted, sector-centric bottleneck list (682 items across 11 sectors) to a system-wide capability map (1,047 items across 21 sectors). In 2016, product coverage concentrated in a few strategic, high-end equipment sectors (such as IT, aerospace, marine equipment, and machine tools) reflecting a focus on closing critical gaps in core components and systems. By 2021, emphasis expanded horizontally to materials, industrial software, and energy systems, as well as into more industries (e.g., steel, textiles, home appliances, petrochemicals).

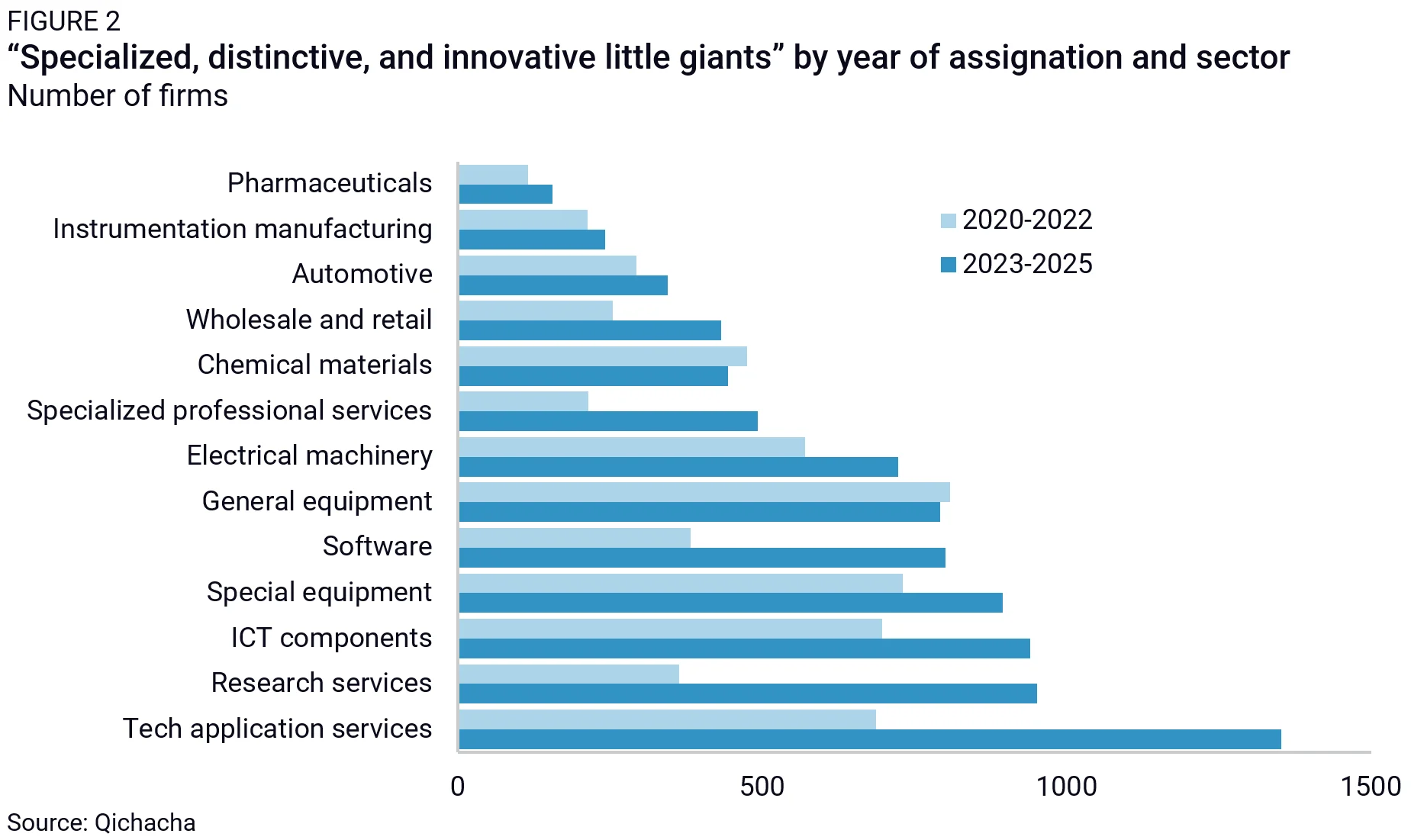

Policymakers are focusing on system-wide capacity-building through a tiered program for innovative small and medium companies. Launched in the late 2010s, the system allows firms to progress through a hierarchy: from Specialized, Streamlined, Characteristic, and Novel (SSCN), to “Little Giant,” and ultimately to “Individual Champion.” At its core, the program functions as an industrial upgrading mechanism. Firms must meet minimum thresholds on R&D intensity, technological capability, and operational efficiency to qualify. Firms that qualify receive a wide range of policy support, including central and local subsidies, tax incentives, and preferential access to financing and research programs.1 The program’s importance rose sharply under the 14th Five-Year Plan and was formalized in 2022 as the current three-tier system. As its role expanded, policymakers set ambitious scaling targets—ultimately aiming for roughly 100,000 SSCNs, 10,000 “Little Giants,” and 1,000 “Individual Champions.” The innovative SME program illustrates the evolution of the core products targeted by China’s industrial policy, from four to six “industrial foundations,” but also to future industries (Table 2).

While the program initially focused on firms embedded in advanced manufacturing supply chains, it is also gradually expanding into services. The fastest growth in new program qualifiers between 2020-22 and 2023-25 occurred in technology services, research services, software, and professional services (Figure 2).

This expanding focus on every node of the supply chain may significantly reshape global value chains. It will likely displace incumbents, especially Japanese, German, and South Korean firms, in core upstream niches. China already dominates parts of this upstream landscape, from critical minerals to wafers and magnets. The next generation of China’s industrial policy may push this dominance broader and deeper, extending it across thousands of inputs, components, and production equipment products that underpin entire manufacturing systems.

Upgrading established industries

Established industries are increasingly at the center of China’s industrial policy. Established industries, such as steel, petrochemicals, shipbuilding, EVs, and solar, are characterized by technological maturity, where Chinese firms have largely caught up with global peers, but also by slowing growth and mounting overcapacity pressures. Each of these industries was at one point the object of intense policy support. For example, the 2009 Ten Major Industry Revitalization Plans introduced a set of industrial adjustment measures prioritizing automobiles, steel, electronic information, logistics, textiles, equipment manufacturing, non-ferrous metals, light industry, petrochemicals, and shipbuilding. Over time, Chinese firms mastered these technologies, expanded production at scale, reduced or eliminated import reliance, and achieved global competitiveness.

In earlier periods, the maturation of these sectors led policymakers to focus on rebalancing and capacity management. While these sectors remained central to employment, investment, and local GDP in the mid-2010s, policy focused on addressing the consequences of excess capacity, fragmentation, and pollution through capacity cuts, consolidation mandates, and tighter environmental enforcement.2 In the 2020s, however, mature sectors were revalorized as strategic pillars and increasingly treated as strategic assets to be supported and upgraded. The 15th Five-Year Plan reflects this shift: A dedicated section on “optimizing and upgrading traditional industries“ now occupies a leading position in the industrial policy chapter.

Growing emphasis on mature industries likely reflects the renewed importance of supply chain security in Beijing. First, maintaining and upgrading these industries is seen as a way to strengthen China’s control over key global chokepoints. The 15th Five-Year Plan, for example, mentions “enhancing the competitive advantages of rare earths,” an objective that was absent from previous policies. Second, the focus on traditional industries reflects a strategy to maintain labor-intensive manufacturing domestically. As the Central Commission on Financial and Economic Affairs highlighted in 2023, China must “insist on promoting the transformation and upgrading of traditional industries and cannot regard them as ‘low-end industries’ to simply abandon.” Last, traditional industries are increasingly viewed as a strategic industrial buffer that underpins supply chain resilience. The chapter on legacy industries in the 15th Five-Year Plan, for example, includes a section on “self-reliance and controllability of the industrial chain,” which calls for building redundancy and “backup of key industries,” to reduce exposure to external disruptions.

This renewed focus does not imply indiscriminate support across entire sectors. Policy is directed toward the most advanced segments in each sector, with the aim of accelerating the adoption of next-generation equipment, promoting higher value-added and technology-intensive product lines, and steering investment away from lower-end or redundant capacity.

Beijing recognizes the threat of overcapacity, but is still more focused on investing in advanced production technology than reducing capacity. Industrial upgrading is implemented through equipment renewal, investment guidance, and the expanded use of environmental and technical standards. Introduced through the “Two Policies” (Large-Scale Equipment Upgrades and Trade-in Program for Consumer Goods) in March 2024 and reinforced by the Guidelines for Equipment Upgrading and Technological Transformation in September 2024.

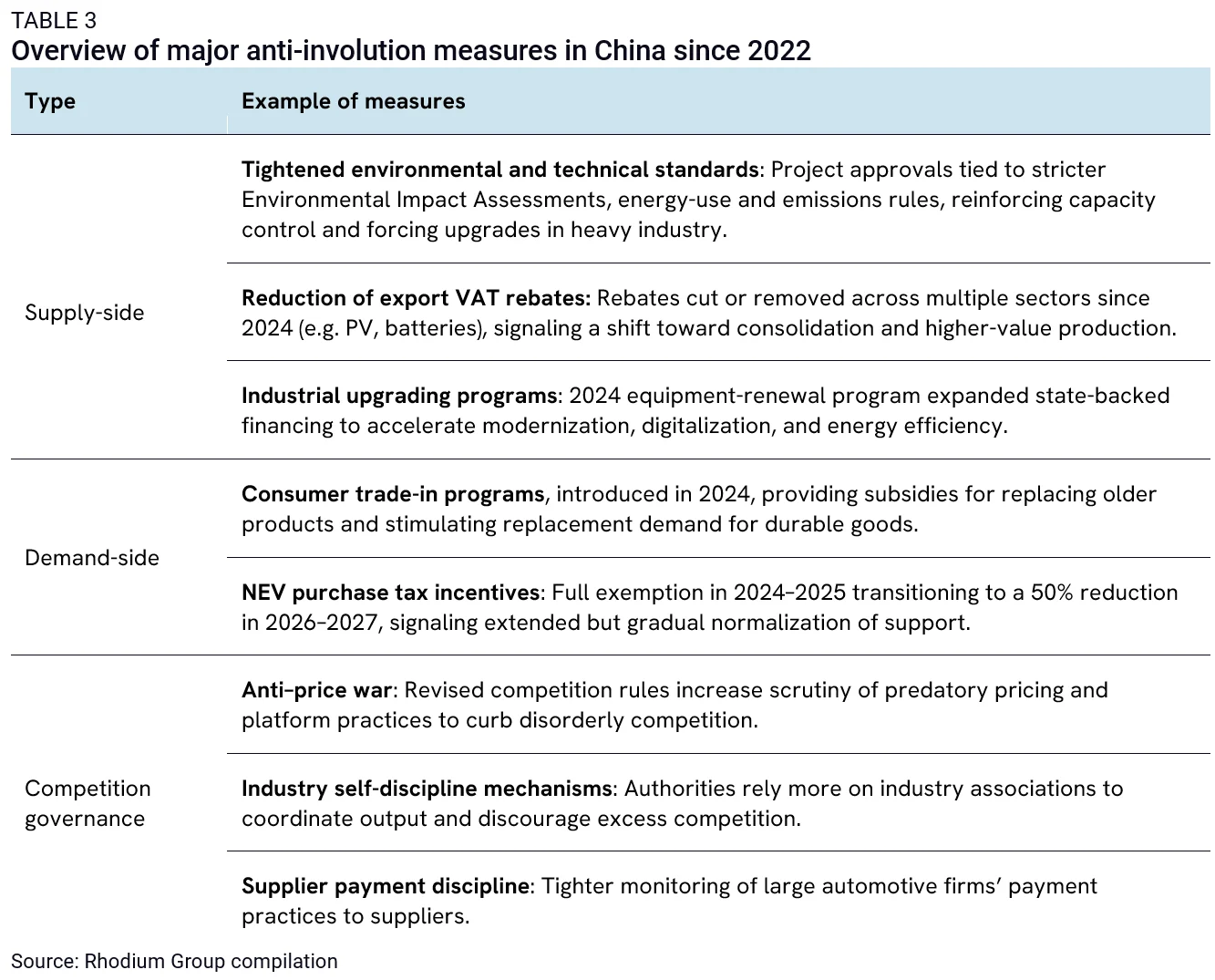

Unlike in previous rounds of supply-side reforms in response to overcapacity, current capacity upgrading is not accompanied by strict targets for cutting old capacity. In 2016-2018, central authorities assigned provincial quotas for factory closures and national capacity ceilings, enforced through local officials’ KPIs. Those instruments have largely disappeared in recent years (Table 3). Capacity replacement policies have not disappeared, but they are concentrated in a few heavy industries and are aimed primarily at regulating incremental capacity rather than mandating large-scale closures of existing plants. Similarly, consolidation through mergers and acquisitions has become more indirect and less binding, resulting in lower levels of restructuring activity than in the previous cycle.3

Anti-involution policies in the petrochemical industry show how the focus is on industrial upgrading, not demand-side stimulus or large-scale supply cuts. In September 2025, China released a national work plan aimed at stabilizing the chemicals sector, which was followed by local policy initiatives and corporate announcements. However, the scale of potential closures remains limited. The measures primarily target outdated facilities, but China’s petrochemical production base is relatively modern. For example, the “Action Plan for Intensifying the Upgrading and Transformation of Old Plants in the Petrochemical Industry” issued in April 2026 targets factories over 20 years old as outdated facilities, but only about 5% of polypropylene capacity and 6% of polyethylene capacity in China is more than twenty years old, meaning the scope for large-scale capacity reductions is inherently constrained.4 At the same time, the plan places strong emphasis on upgrading the sector’s product structure, particularly by shifting from bulk petrochemicals toward higher-value specialty chemicals. The document sets explicit growth objectives, stating that from 2025 to 2026 the added value of the petrochemical industry should grow by more than 5% annually while significantly strengthening technological innovation capabilities.

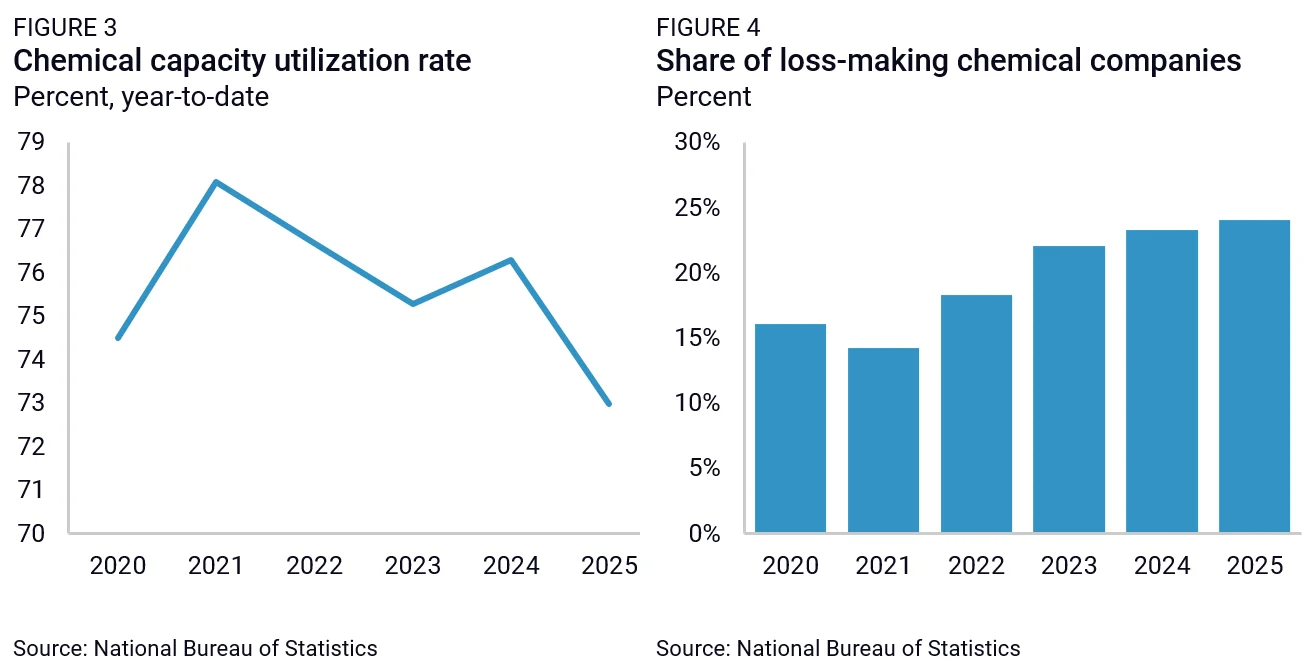

The chemical sector also provides a good illustration of the limitation of the current approach to significantly tackle overcapacity. Over the past few years, the chemical industry’s capacity utilization rate has continued to decrease, while its share of loss-making companies has continued to increase (Figures 3 and 4). The Iran conflict is likely to cement overcapacity in the sector by accelerating China’s efforts to reduce external dependence, thereby driving further investment in coal-to-olefins (CTO), a coal-based pathway to petrochemical inputs deployed at scale only in China.

Overall, the use of an industrial policy playbook in mature sectors that emphasizes continued investment in equipment upgrading and higher-tech segments of the industry will likely cement overcapacity in large parts of the Chinese economy. This will be particularly problematic, given weak domestic demand growth. Overcapacity may also appear in new product categories that are currently targeted as investment priorities—for example more high-tech specialty chemicals.

Promoting frontier technologies

Beijing is working to deploy frontier technologies at an accelerated pace, investing more in commercializing its cutting-edge R&D and innovation investments. In contrast to emerging industries, Chinese industrial planners define “frontier technologies“ as pre-commercial domains with high technological uncertainty and strategic importance for long-term competitiveness. Historically, China maintained a functional distinction between innovation policy that focused on foundational research, talent, and national S&T programs, and industrial policy that targeted sectors already commercialized or nearing commercialization.5 While closely coordinated under past policy regimes, these domains were distinct. For example, they featured in separate chapters of the 13th FYP issued in 2016. The 14th FYP began to blur these boundaries, but frontier technologies were still framed largely as areas for exploration and incubation rather than full-fledged industrial policy targets. By the 15th FYP, the focus has shifted toward industrial ecosystem development for frontier technologies, including through public investment in enabling infrastructure, direct incentives for market creation, and mobilization of central SOEs in purchasing key products.

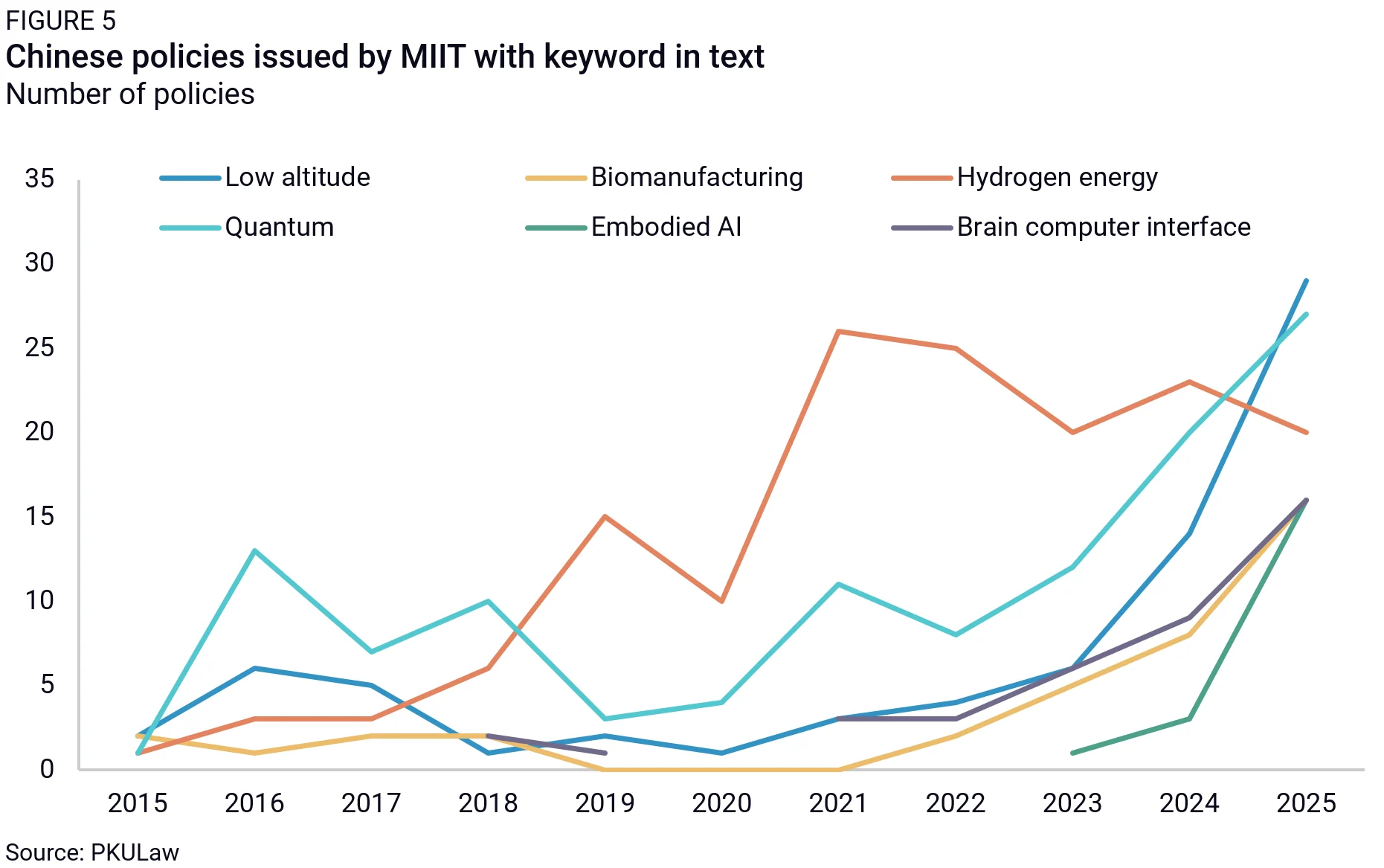

Frontier technologies such as embodied AI, brain–computer interfaces, fusion energy, and 6G are now supported by both R&D programs and efforts to commercialize nascent technologies. This elevation is also visible in the policy landscape, where the Ministry of Industry and Information Technology (MIIT), traditionally responsible for industrial policy, has published a rapidly growing number of policies on frontier technologies such as low-altitude aviation, embodied AI, brain–computer interfaces, biomanufacturing, hydrogen energy, and quantum technologies (Figure 5).

In practice, addressing frontier technology through the industrial policy toolbox means orchestrating downstream markets and resources to create demand. In earlier strategic sectors, from renewable energy to electric vehicles and batteries, China paired supply-side support for domestic producers with demand creation policies. The EV sector is a prominent example. Manufacturing subsidies and local content support were combined with consumer purchase incentives, charging infrastructure rollout, and regulatory measures such as license plate privileges and fleet electrification mandates.

A similar approach is increasingly used to encourage the commercialization of frontier technologies, with the concept of “scenario-based development.” First introduced by MIIT around 2021-20226 the concept quickly diffused across ministries and was incorporated in a State Council policy by 2025, before being incorporated into the 15th Five-Year Plan. Scenario-based policy aims to incentivize and subsidize demand for technologies that are not fully commercialized yet. The 2024 “Implementation Opinions on Promoting Future Industry Innovation” formalized this approach, identifying a range of technologies (from ultra-large AI computing centers, to satellite internet, eVTOL aircraft, deep-sea exploration equipment, and digital-twin-enabled healthcare), for commercialization.

In practice, this involves mobilizing firms, especially central SOEs, as well as local governments and public institutions to identify and create “use scenarios” that can absorb new technologies that do not yet have a demand base. For example, in the “low-altitude economy,” authorities are encouraging actors across sectors such as agriculture, urban governance, logistics, tourism, and public services to integrate drone and aerial technologies into their operations. Use cases for drones range from basic package delivery to spraying pesticides on crops and medical uses such as rapid medical supply delivery and emergency rescue. This is complemented by public investment in enabling infrastructure, including the use of local government special bonds to finance low-altitude networks and facilities. Policy tools also include direct incentives for market creation, with local governments offering cash rewards and subsidies to firms that develop and scale application scenarios. For instance, cities such as Suzhou have introduced financial incentives for companies operating low-altitude logistics distribution.

The 15th Five-Year Plan also more explicitly links large S&T research programs with industrial and technological applications. It elevates demand for key enabling technologies as a central criterion for public R&D support and opens the national system to the inclusion of enterprise-led projects. Large national S&T programs are operationalizing this through an increased focus on industrialization. For example, the “Pilot Projects for the Industrialization of High-Tech Achievements from the National Key R&D Program“ issued in 2025 identifies mature research outputs and pairs them with companies for industrial scaling. The pilot started with a first batch of 67 technologies, concentrated in sensors, advanced materials, industrial software, and advanced manufacturing equipment, illustrating a broader effort to connect state-funded R&D more directly with industrial supply chains and large-scale production.

Artificial intelligence as a core industrial policy strategy

Artificial intelligence (AI) illustrates both the promise and the constraints of China’s frontier technology strategy. It stands out as a special case because it has been elevated above other future industries to the status of a cross-cutting, foundational technology. The term appears four times in the 13th FYP, six times in the 14th FYP, and 52 times in the 15th FYP. At the local level, the number of policies with AI in their title has surged from two in 2016 to 235 in 2024 and 584 in 2025.7 The role of AI in China’s industrial policy ecosystem is also evolving. Rather than treating it simply as a technology to develop, the 15th FYP frames it as an infrastructure-like technology, underpinning entire industrial ecosystems. The goal is to use AI to achieve all the other objectives of China’s industrial policy: upgrading mature industries, addressing chokepoints in emerging industries, developing services, and accelerating productivity growth.

At the same time, AI policy closely reflects the standard industrial policy playbook China is now applying to frontier technologies. China is leveraging its entire industrial policy toolbox in the sector, with enormous resources dedicated to solving chokepoints in the semiconductor segment, encouraging innovation in the software segment, and incentivizing diffusion across the economy. Policy initiatives like the “AI+” initiative, issued in August 2025, and the subsequent “AI + Energy” and “AI + Manufacturing” policies issued respectively in September 2025 and January 2026, aim to create a market for AI applications. The government is mobilizing demand and asking state actors to contribute to demand for AI products. Public procurement (including both SOEs and government entities) has emerged as a particularly visible lever: In the first half of 2024 alone, government and SOE buyers issued hundreds of tenders for large-model-related projects, with total contract values exceeding RMB 1.3 billion, more than double the total for all of 2023. SASAC explicitly instructed SOEs to pursue “demand-driven” AI development strategies and accelerate the construction of enabling infrastructure. The new guidelines, effective January 2026, formalize preferential treatment for domestic products in public procurement, including in software development and digital infrastructure, thus effectively creating a protected market for Chinese players.

Because China already has a vast domestic demand base in its manufacturing industry, particular attention is given to scaling applications in that market. MIIT’s “Artificial Intelligence + Manufacturing” Special Action Plan, for example, focuses specifically on industrial adoption, targeting the deployment of 3-5 general-purpose large models in manufacturing, the creation of 1,000 industrial AI agents, 100 industrial datasets, and 500 application scenarios, alongside the development of globally competitive ecosystem leaders. The plan outlines the use of AI in smart robotics, predictive machine maintenance, automatic quality control, and AI-enhanced design and R&D.

However, the Chinese market remains structurally constrained in its ability to translate rapid AI deployment into sustainable revenues. Despite strong adoption metrics, monetization remains limited. In global comparisons of leading AI companies by annual recurring revenue, Chinese firms account for only a marginal share of total revenues. According to a joint analysis by Unique Research and Tech Buzz China, only four Chinese companies rank among the world’s top 100 AI applications by ARR, generating a combined $447 million (just 1.23% of the $36.4 billion total) while the overwhelming majority of revenues are captured by US-based firms.

These outcomes are closely tied to structural features of China’s domestic economy. First, low willingness to pay for digital services, both among consumers and enterprises (even SOEs), compresses pricing power and limits the scalability of recurring revenue models.8 This is reflected in pricing dynamics: Chinese AI developers have been undercutting international competitors by as much as 90–97%, triggering an intense price war that prioritizes user acquisition over profitability.

Second, the small size of China’s services sector limits the impact of the most potent applications of AI. Globally, services represent the fastest-monetizing segment for AI, due to their high data intensity, frequent user interaction, and standardized processes. Services (such as finance, e-commerce, logistics, customer service, search, marketing, coding, and professional services) are also among the earliest adopters in China as well, according to recent reports by the China Academy of Information and Communications Technology.9 Even in manufacturing companies, 74% of LLM adoption is concentrated in marketing, services, operations, although adoption in manufacturing processes is growing fast.10

These constraints are pushing Chinese AI firms to look outward and experiment with alternative commercialization strategies. A growing number are adopting a “born global” model, targeting overseas markets where pricing power is significantly higher. As Red Xiao, founder and CEO of Manus, put it: “Overseas users may be willing to pay up to five times more for software than Chinese users, and pricing can be set in US dollars. With an exchange rate of seven, that translates to a market that is at least 35 times larger.” So far, many Chinese AI companies have embraced open-source models as a means of expanding globally, rapidly capturing a growing share of global downloads with cheap high-end models.11 This strategy is already visible in firm-level data. In a ranking of the 100 largest AI products worldwide by annual recurring revenue, among the 23 Chinese developers, 19 generated most of their revenue overseas. Companies like MiniMax have rapidly reoriented toward international markets, with overseas revenue rising from 19% of their total revenues in 2023 to over 70% by 2025 (with 24% from the Americas). Others, such as Zhipu are scaling global markets, offering coding tools at around $3 per month (roughly one-seventh the price of comparable US products) to attract users across more than 180 countries. Even large US firms such as Airbnb are adopting Chinese models because of their low costs. However, this strategy may prove difficult to sustain, and some Chinese firms like Alibaba have recently started shifting strategies to better monetize their large language models.

At the same time, China’s manufacturing strength may monetize embedded AI in physical products. More than 20 Chinese automakers have announced plans to integrate large models such as DeepSeek into vehicles, enhancing features like voice control, navigation, and in-car assistants. All major smartphone brands, including Huawei, Xiaomi, Oppo, and Vivo, have incorporated similar models into their operating systems, while companies like Midea are marketing AI-enabled appliances as “understanding” user needs in real time. Huawei’s push to integrate AI deeply into its HarmonyOS ecosystem, across phones, cars, and home devices, illustrates the ambition to turn AI into a layer embedded across exported hardware. Even if foreign countries raise barriers to Chinese AI software, this “embedded intelligence” model may offer a workaround and still be exported at scale, allowing China to capture value through manufacturing while diffusing its technology globally. The model is not without tensions, even within China. Many third-party apps resist attempts by AI agents to access and control their data within integrated ecosystems, while state-owned telecommunications firms and private internet platforms compete over data standards. Huawei occupies a unique position in this power struggle as it spans all layers of the AI stack and is therefore well placed to capture a disproportionate share of value, both in China and abroad.

Overall, China’s AI strategy illustrates both the strength and the fragility of China’s frontier technology push. China is betting heavily on its ability to leap ahead in future technologies, and its model has demonstrated clear strengths in rapidly scaling production and commercializing innovation. Future technologies create a genuine opportunity to achieve global dominance. But that strategy creates challenges, given domestic economic weaknesses and shortcomings in demand and willingness to pay for services. The domestic economic environment may therefore limit the extent to which these technologies can translate into sustainable growth. Weak demand, low willingness to pay for digital services, and compressed profit expectations all constrain incentives for innovation and diffusion, but also are forcing the PRC government and its companies to be more aggressive in seeking opportunities abroad. Whether China can translate its technological advances into sustainable economic growth will depend not only on its capacity to innovate, but also on its ability to generate viable business models, particularly in overseas markets when monetization at home remains constrained.

Developing services

Lastly, China’s industrial policy increasingly targets services. China’s service sector remains relatively underdeveloped compared to economies at similar income levels, particularly in knowledge-intensive business services. Services’ value added accounts for just over 50% of China’s GDP, far below the average 75% of advanced economies. The gap is especially pronounced in high-value business services such as professional services and R&D services. China’s value added in computer programming and information service activities’ share of GDP is only 3% in China, compared to 8% in the US and the UK, and 6% in Germany and South Korea. This relative weakness reflects China’s long-standing emphasis on manufacturing and industrial upgrading for economic development.

China’s economic strategy has long been ambivalent toward the service sector, which persists to this day. The 13th FYP framed the expansion of services as a structural objective, including a target to increase the share of services’ value-added contribution to GDP from 50.5% in 2015 to around 56% by the end of the plan in 2020. However, support for services had declined by the start of the 14th FYP, which called to “maintain the basic stability of the manufacturing sector‘s share.” The 15th FYP largely maintains this orientation. Manufacturing remains the organizing principle of the industrial strategy, and the plan reiterates the goal of “maintaining a reasonable proportion of manufacturing and building a modern industrial system with advanced manufacturing as the backbone.”

Yet, below the surface, industrial policy is emphasizing high-tech services in targeted areas. Chinese government actors see the potential for growth in services to benefit consumption and encourage the deployment of new digital technologies. AI, in particular, generates value primarily through downstream markets in service activities such as software development, finance, logistics, legal analysis, design, and other knowledge-intensive tasks. Reflecting this, the State Council’s “AI+“ initiative calls for expanding AI deployment across these sectors and developing new AI-driven service models. The 2024 Opinions on Promoting the High-Quality Development of Trade in Services through High-Level Opening and the 2025 Measures to Promote Service Exports, for example, aim to strengthen China’s competitiveness in internationally tradable services such as digital services, professional services, outsourcing, and R&D services. Additionally, the 2026 Opinions on Promoting the Expansion and Quality Improvement of the Services Sector promote the adoption among government agencies and SOEs of large-scale models and intelligent agent services.

The shift in emphasis and scope of services industrial policy is also visible in the attitude toward foreign investment. Traditionally, China used selective attraction of foreign companies’ investment to drive localization and import substitution. That strategy is now used in services, where the December 2025 Central Economic Work Conference emphasized opening up to foreign services, aiming “to attract more high-quality foreign investment to participate in the development of China‘s service industry.” This is implemented in practice with successive iterations of the Catalog of Industries Encouraging Foreign Investment between 2020 and 2025, where the number of encouraged investment products grew the most in service sectors. The 2025 catalog expanded the range further toward knowledge-intensive, digital, and creative services, adding categories such as knowledge process outsourcing, advertising and language technology services, and non-clinical drugs. Yet, this opening is tempered by China’s broader security framework, which continues to expand risks for foreign companies investing in the service sector. Notably, the revised Counter-Espionage Law broadens espionage definition to include overseas entities and the transfer of data, increasing legal uncertainty for overseas investors.

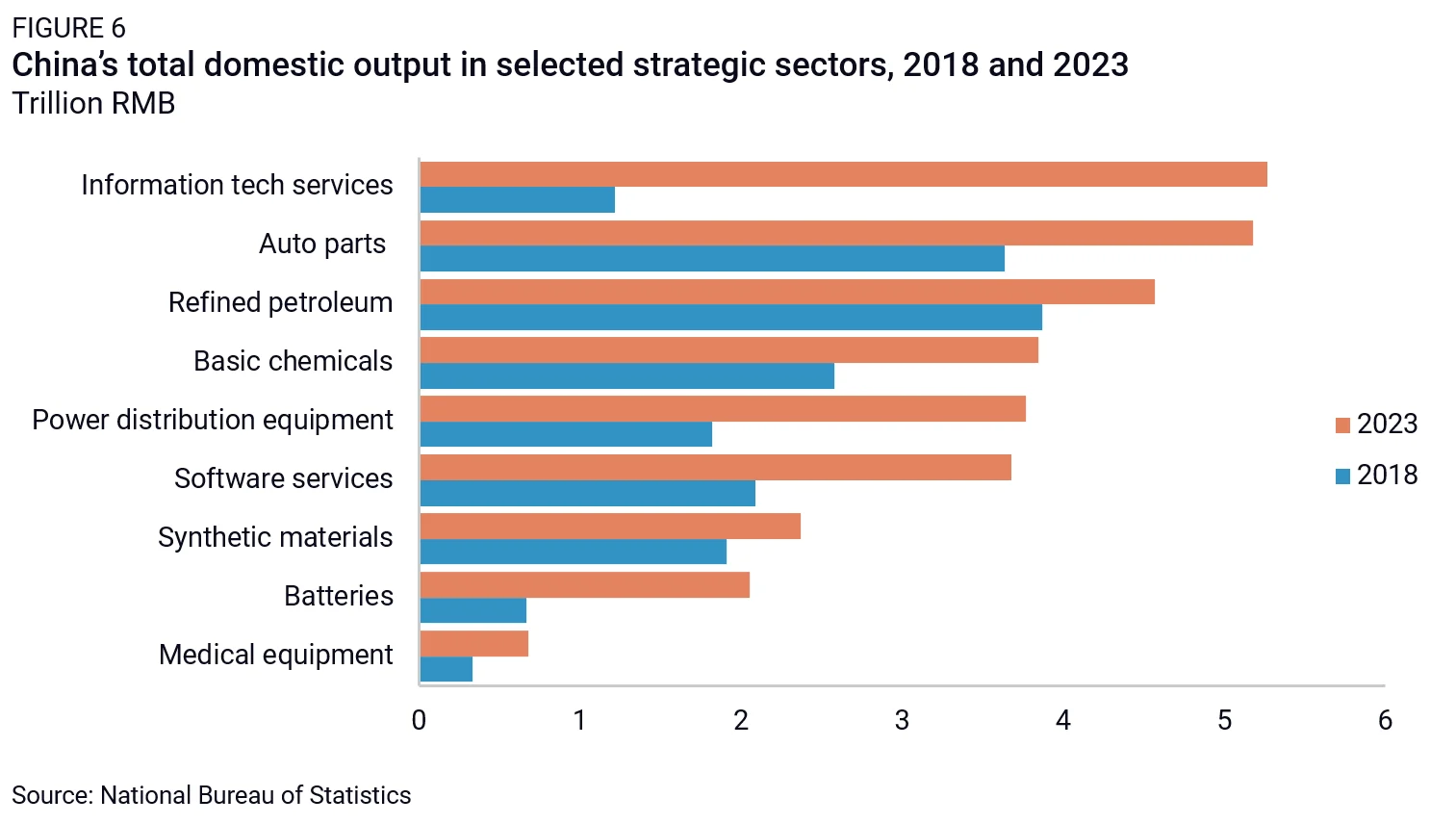

The growing policy emphasis on services is already showing up in sectoral growth patterns. According to China’s National Bureau of Statistics’ input–output tables, information technology services recorded the fastest output growth among all sectors from 2018 and 2023. Internet and related services ranked third, behind only gas production and supply (Figure 6).

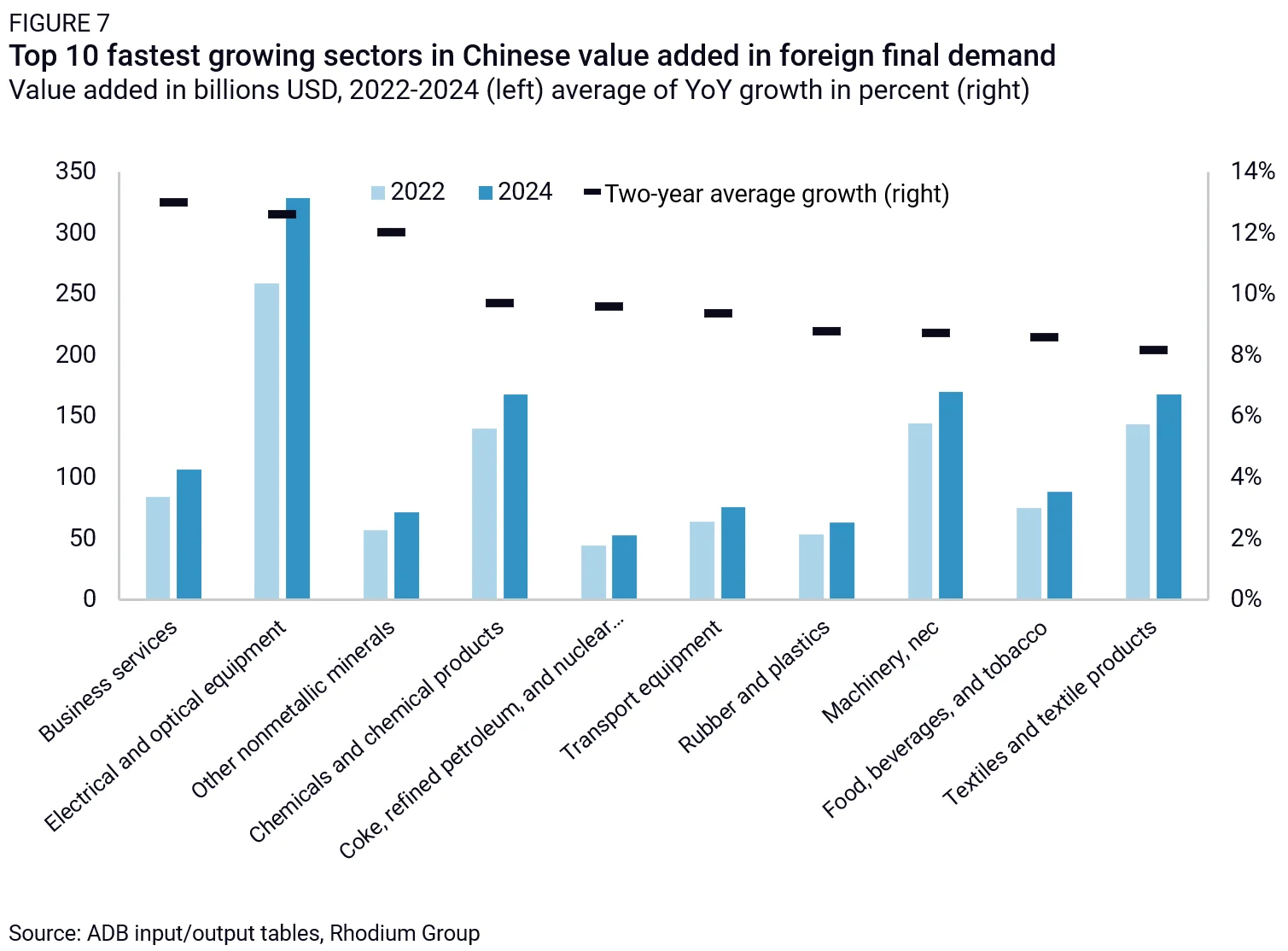

The recent growth in China’s service sector output is also visible abroad. Among all industries, the share of value-added output from China’s business services sector in other countries’ final demand grew the most from 2022 to 2024 (Figure 7), though from a low base level prior to this period.

These aggregate categories also mask an important shift within the service sector itself, where the industries showing the strongest growth are knowledge-intensive and technology-driven. Recent data show that high-tech services are expanding faster than high-tech manufacturing, growing 17.2% year-on-year in January and February 2026, compared with 14.5%, with R&D-related technical services particularly strong, posting revenue growth of 23.6% in the first two months of 2026. The biopharma sector illustrates this pattern, with rapid expansion of research and contract services supporting drug development. China’s contract research and manufacturing (CRO/CDMO) industry (companies providing outsourced R&D, testing, and manufacturing services to global life-science firms) has grown from $5.9 billion in 2018 to $11.6 billion in 2022 and is projected to more than double this size by 2027.

This shift is likely to accelerate in coming years. As manufacturing becomes more high-tech, it requires services to play a greater role. The next generation of manufacturers will likely be highly agile, networked firms that use information and analytics as skillfully as they employ talent and machinery. Moving to robotics and smart manufacturing processes highlights this change as they require servicing and software updates to be maintained. Similar to China’s downstream demand subsidies promoting upstream production, by fostering high-tech and smart manufacturing, China is creating downstream demand for a wider variety of services. Advances in AI will only drive this further.

2. Improving the industrial policy playbook

Despite Beijing’s confidence in its industrial policy playbook, its push for industrial policy and technological self-reliance comes as its traditional policy tools are weakening. Fiscal resources are increasingly constrained, credit growth is slowing, and the efficiency of capital allocation is declining. Beijing is not retreating from intervention, but is instead responding by tightening control over financial and capital markets to ensure scarce resources are concentrated on strategic sectors. The government is intervening more in equity markets, banking, and other regulatory measures in the face of tighter fiscal conditions.

Fiscal and financial pressure

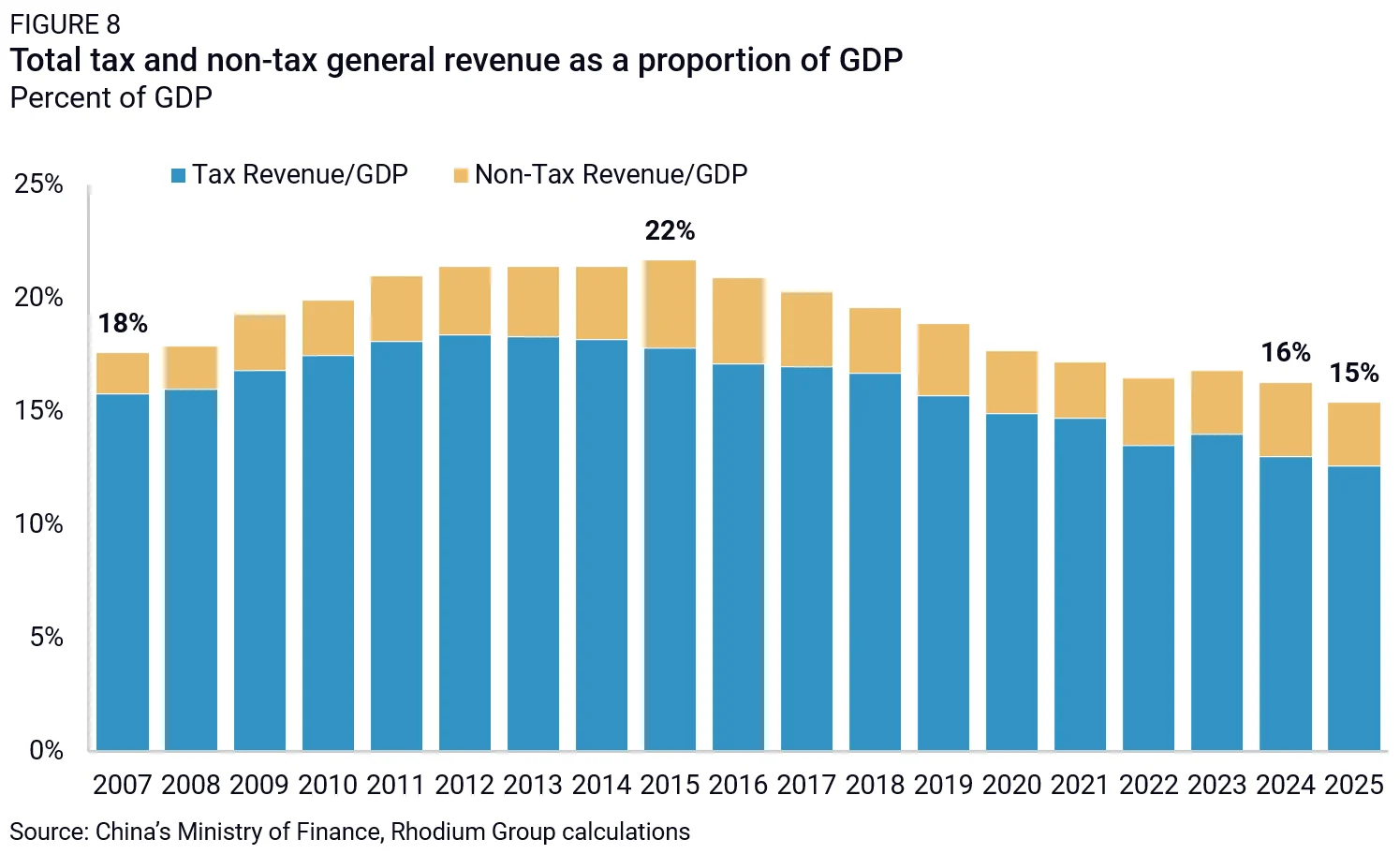

China’s fiscal capacity has weakened significantly in recent years and is increasingly tied up in sectors struggling with overcapacity. Tax and non-tax revenues fell to 15.4% of GDP in 2025, among the lowest levels across major economies and far below the OECD average of around 34% (Figure 8). As a result, the IMF estimates that the augmented fiscal deficit reached 14.3% of GDP in 2025. Faced with growing fiscal constraints, Beijing has so far adopted a conservative approach of austerity, rather than launching a stimulus by expanding fiscal deficit as a share of GDP.

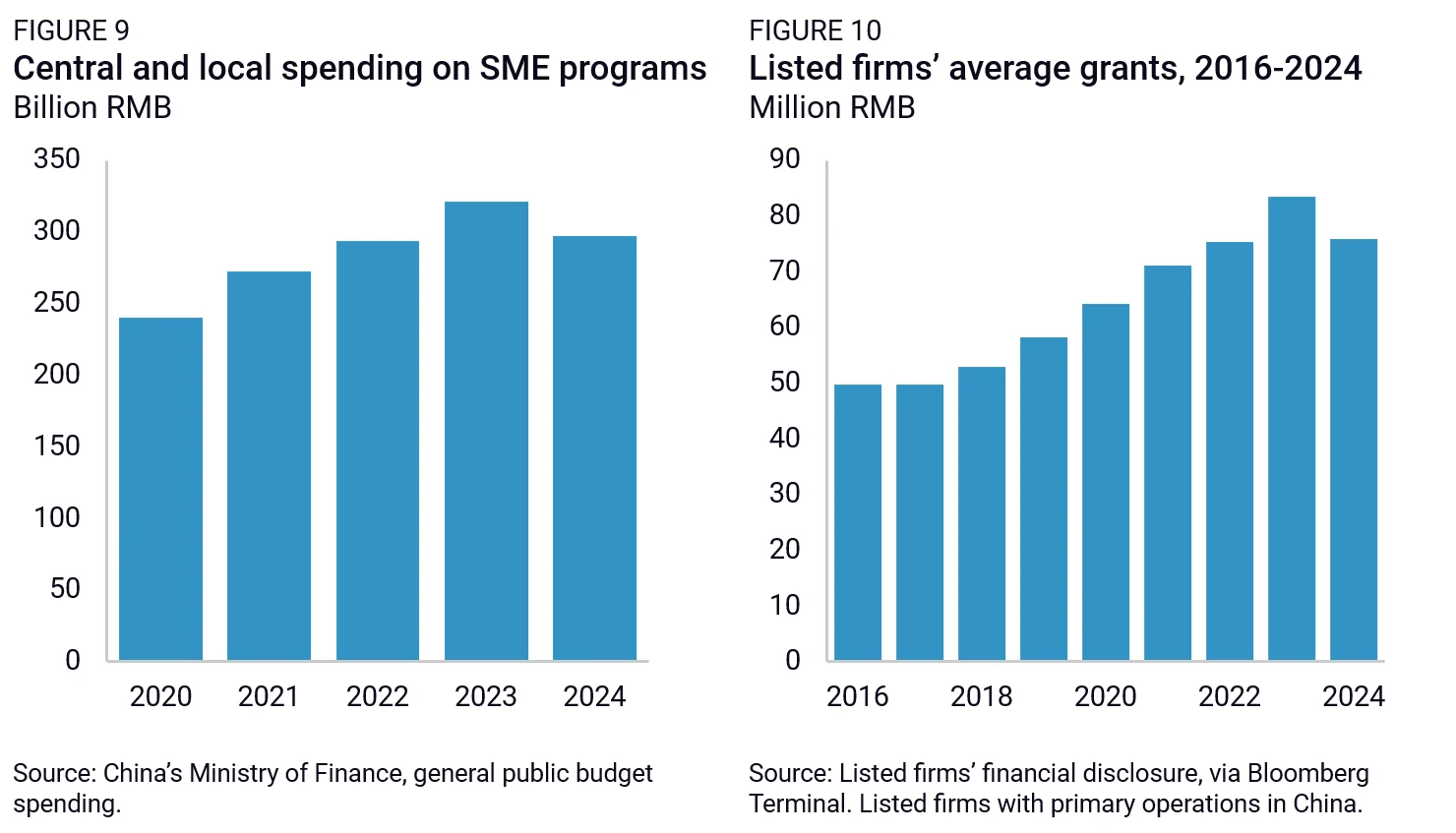

These pressures are already visible in direct subsidy programs. Government funding for SME innovation programs, which support firms designated as SSCN enterprises, Little Giants, and Individual Champions, declined slightly in 2024 (Figure 9) according to official statistics. Similarly, in 2024, average direct grants to listed firms fell to their lowest level since 2022, the first decline since at least 2016 (Figure 10) according to listed firm disclosures.

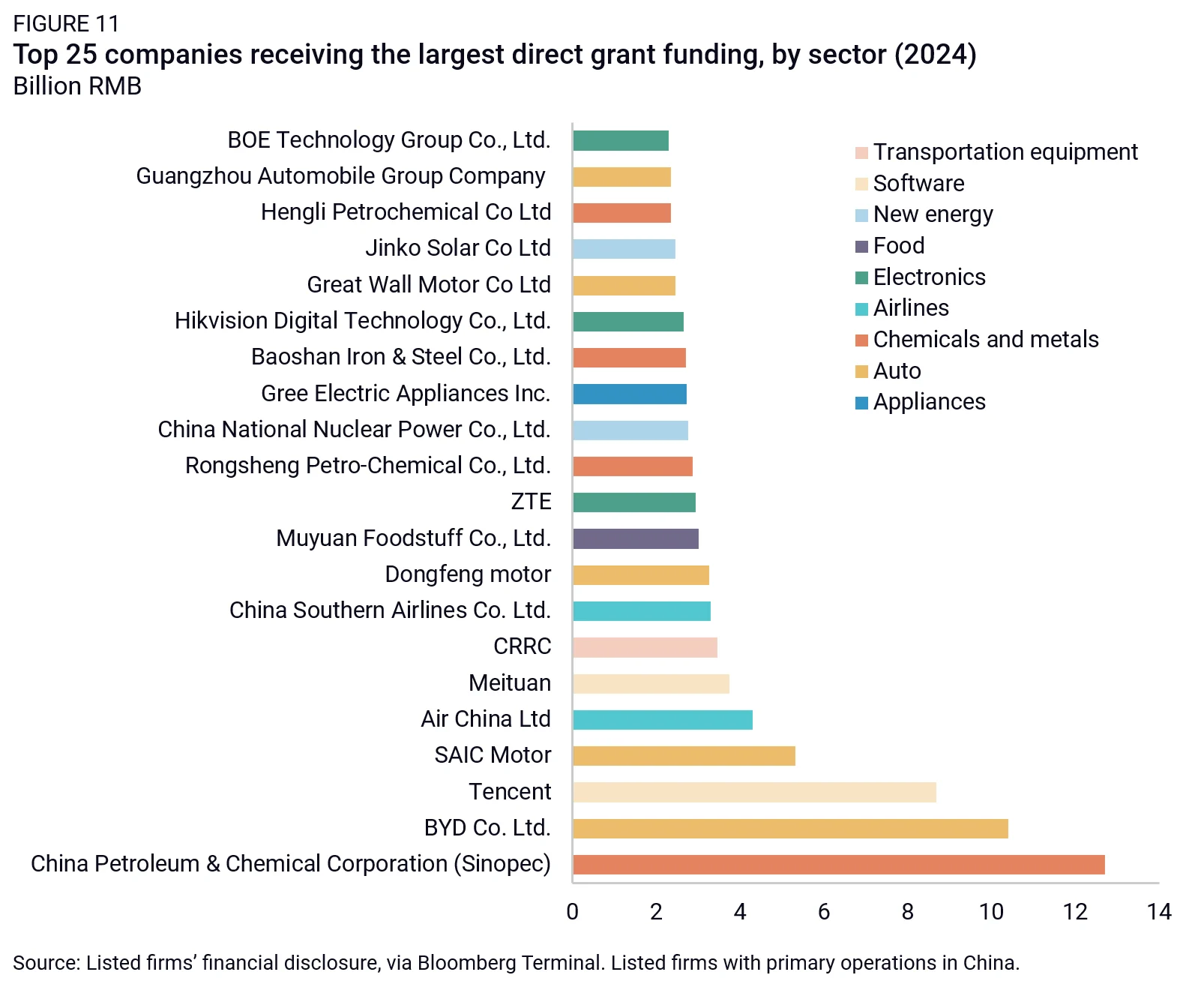

Fiscal and banking resources are also increasingly tied up supporting companies suffering from overcapacity. In the EV and battery value chain alone, manufacturing subsidies reached $17.5 billion in 2024, equivalent to 1.3% of central government revenues.12 Among the largest recipients of direct government grants in 2024 were automobile manufacturers, oil and gas producers, airlines, commodity chemical companies, new energy power producers, and steelmakers (Figure 11). Many of these industries are characterized by excess capacity and weak profitability. In recent years, authorities have also directed the banking system to extend special lending to state-owned enterprises and government financing vehicles facing financial stress, most of which are in sectors with heavy overcapacity, including to help clear overdue payments owed to small and medium-sized suppliers.

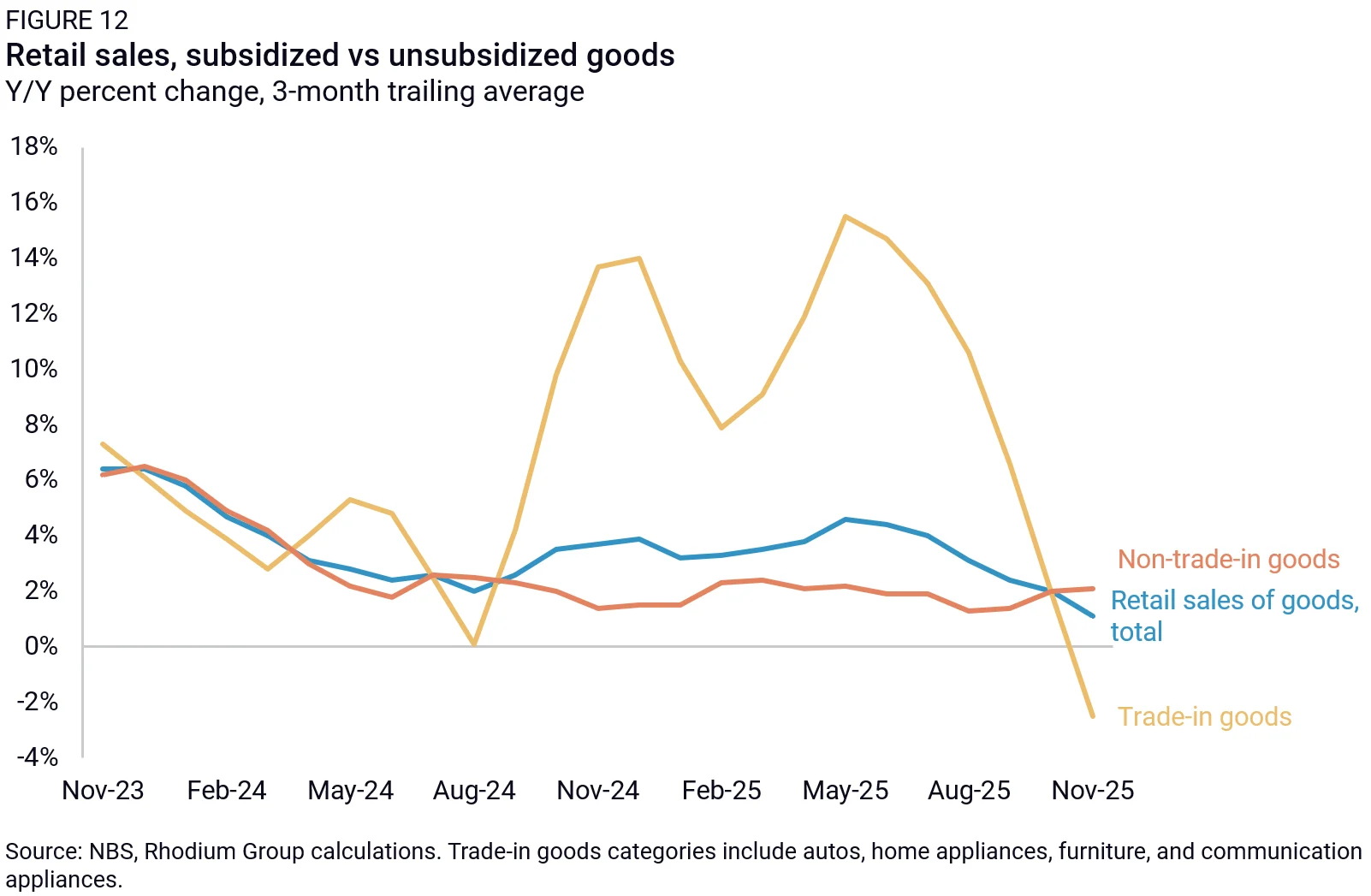

Demand-side subsidies are also under strain. Stimulating demand has long been central to China’s industrial policy, both via targeted programs for specific products (e.g., EVs) and broad-based incentives for consumption (e.g., the trade-in program). Public procurement, purchase subsidies, and infrastructure investment were critical to earlier success. Today, however, these tools are increasingly stretched, as policymakers use them to prop up sectors facing overcapacity. In 2025, the Ministry of Finance allocated roughly RMB 300 billion in trade-in subsidies, a short-term incentive scheme to encourage demand for industries under stress. Auto-related subsidies alone are estimated at a record RMB 342 billion. This includes RMB 150 billion for scrappage and trade-ins and RMB 192 billion in NEV purchase tax exemptions. Together, these incentives amount to about 3.4% of central fiscal expenditure. For 2026, another RMB 250 billion has been earmarked for trade-in support.

The scale remains modest compared to past stimulus episodes, such as the post-2008 infrastructure surge or the shantytown redevelopment program after 2015. Their effectiveness is also limited because these subsidies tend to pull demand forward rather than sustain it. The result is a costly, short-lived boost that does little to address underlying demand weakness, while constraining the state’s ability to deploy fiscal resources elsewhere (Figure 12).

Lastly, China’s financial system is also under strain. Bank asset growth averaged 18% annually between 2007 and 2016, but slowed to around 9% from 2017 to 2024, with credit growth falling further in 2025. At the same time, the efficiency of credit allocation has deteriorated. By December 2025, 58% of bank loans were issued at or below the loan prime rate (3%), more than double the share seen in 2020–2021. This likely reflects an increasing concentration of lending to SOEs and state-directed relending programs, which are better able to negotiate very low credit prices. Profitability across the banking system deteriorated in 2025 despite RMB 520 billion in capital injections into major banks. Overall, the fiscal and financial strains mean that Beijing will have to do more to support a growing set of industrial policy objectives, with less resources and less capacity to reallocate resources.

Recentralizing state resources

Faced with these growing constraints, Beijing is rationalizing resource allocation and tightening central control. Two major policy documents issued in 2025—the Guiding Opinions of Seven Departments on Financial Support for New Industrialization and the Policy Measures to Accelerate the Construction of a Science and Technology Finance System—outline a coordinated strategy to direct fiscal spending, bank lending, capital markets, and state investment funds toward technological innovation and strategic industries. Together, they formalize a whole-of-finance approach in which credit, equity markets, and state capital are explicitly tasked with supporting industrial upgrading and “new quality productive forces.”

To start with, the government is prioritizing the allocation of fiscal resources for science and technology spending. While overall fiscal expenditures grew only around 1% annually in 2024–2025, spending on science and technology increased around 5%. The 2026 budget plans nearly RMB 1.3 trillion in national S&T spending, a further 7.1% increase.

At the same time, the central government is curbing excessive local industrial policy competition in areas that are not central priorities. The 2025 Budget Report, for example, proposed standardized tax incentives and a negative list for local subsidies, prohibiting unauthorized incentives and requiring existing programs to be reviewed or abolished if they conflict with national priorities. Authorities are also considering a nationwide negative list specifying circumstances in which local governments are barred from granting fiscal subsidies. Oversight is also tightening: Following a 2024 audit findings of fraudulent subsidy claims, a late-2025 rectification report shows local governments recovered or reallocated RMB 5.975 billion in misused funds, revoked firms’ eligibility, and strengthened verification.

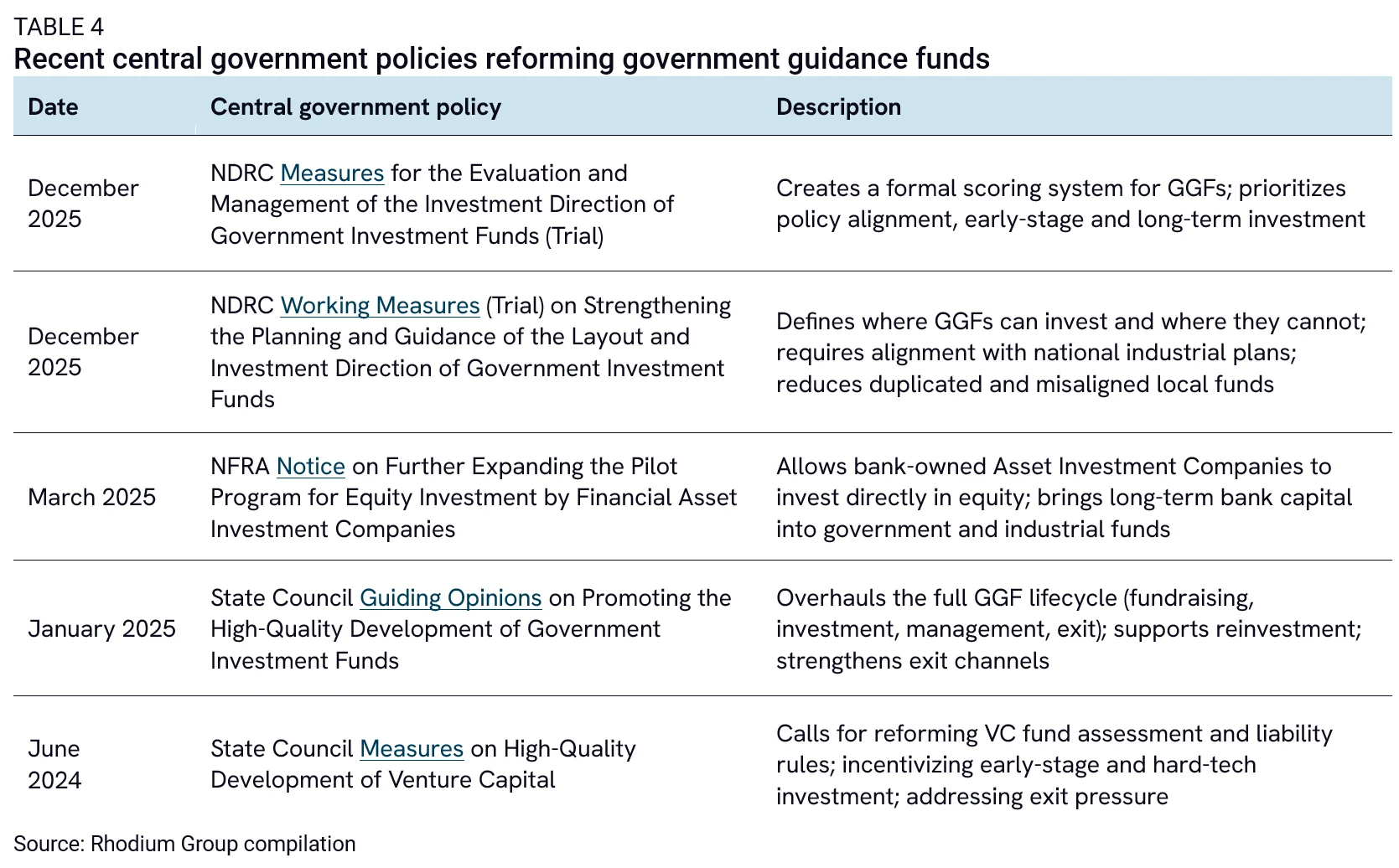

A second, and central, target of reform is the government guidance fund (GGF) system. GGFs are state-directed investment funds that combine public and private capital to support strategic industries. Over the past decade, thousands of such funds were created by local governments, often resulting in duplicated investments and inefficient capital allocation.13 Governance structures encouraged risk-averse behavior, which in many cases undercut their primary objectives: Fund managers typically operated under short performance cycles with strict audit requirements and low tolerance for losses. As a result, GGFs often favored large, politically connected firms or late-stage companies rather than early-stage technological innovation. This dynamic crowded out private capital and inflated valuations in favored sectors, but may not have aided China’s innovation goals.14

Recent policy initiatives aim to overhaul the system. New regulations introduced in 2024–2025 establish evaluation frameworks for investment direction, strengthen central guidance over fund deployment, and expand participation by financial institutions such as bank-owned asset management companies (Table 4). These reforms also emphasize longer investment horizons and greater tolerance for early-stage technological risk.

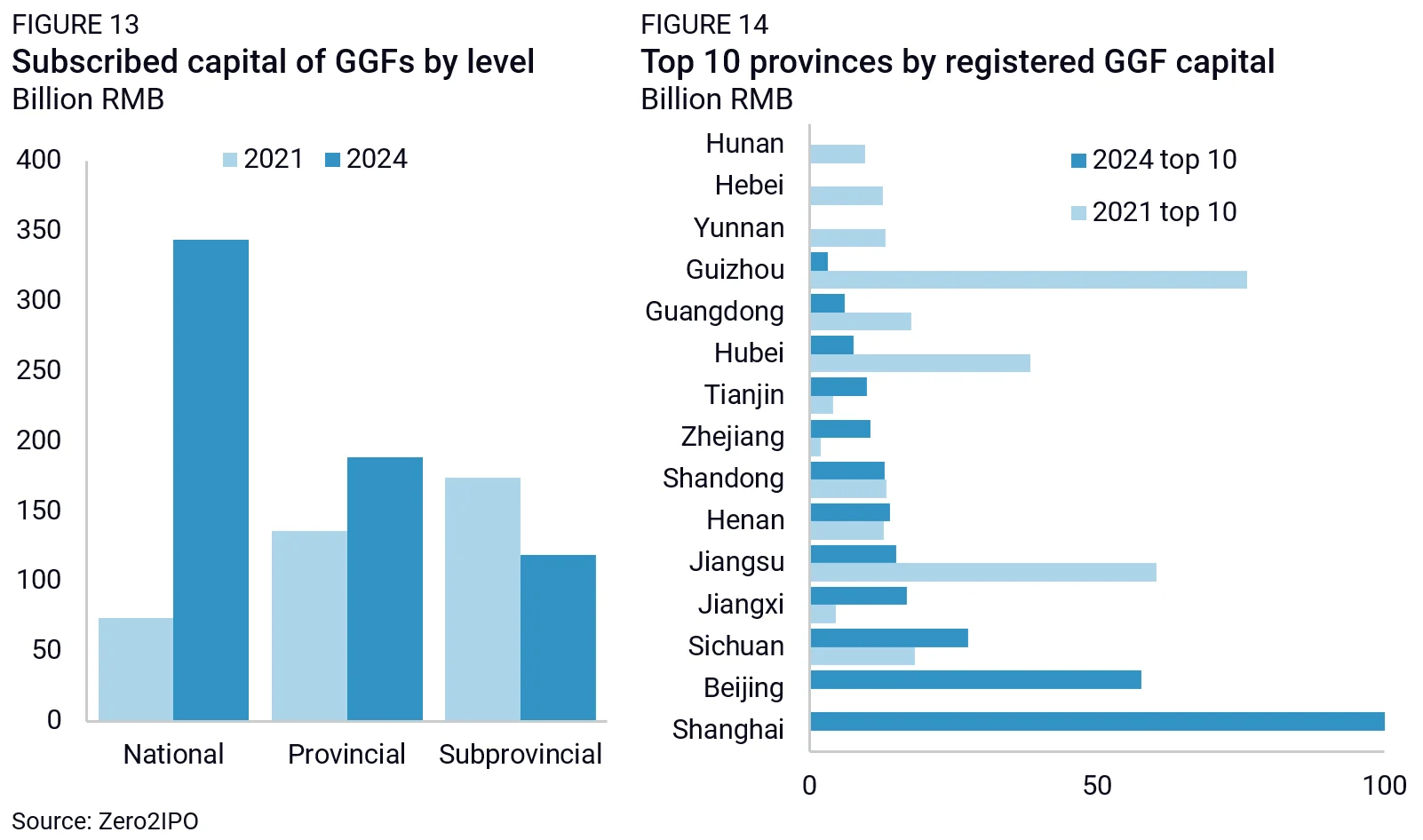

GGF activity is also becoming more centralized. Policy documents now stress coordination between central and local governments and explicitly criticize the proliferation of duplicative local funds. In practice, capital is increasingly concentrated at the national level (Figure 13) and in a smaller number of wealthy provinces with established industrial ecosystems (Figure 14).

The “Little Giants” program is undergoing rationalization, shorthand for China’s broader system of tiered SME selection and upgrading. In the lead-up to the 15th Five-Year Plan, implementation weaknesses had become increasingly evident, as local authorities prioritized quantity over quality of companies, resulting in uneven firm performance. Recent policy revisions in early 2026 introduce stricter eligibility criteria (including higher revenue thresholds), cap provincial nomination quotas based on past approval outcomes, and strengthen oversight through audits, data verification, and penalties for misreporting.

Lastly, a similar rationalization is underway among central SOEs. Over the past decade, SOEs were encouraged to establish funds and act as PE and VC investors, often with limited discipline and weak alignment with core business.10 More recently, policymakers have pushed them to refocus on strategic sectors and reduce scattered, non-core investment. In practice, after a sharp decline in SOE participation in PE funds in 2021–2023, activity rebounded in 2024–2025 in a more concentrated and professionalized form, centered on a smaller number of large, policy-aligned vehicles (Table 5). One prominent example is the Central SOEs Strategic Emerging Industry Development Fund, which became one of the largest new funds in 2025, along with the Phase II of the National Military-Civilian Integration Industry Investment Fund. Beijing recently signaled further moves to overhaul how SOEs are evaluated, emphasizing metrics tied to their contribution to strategic objectives such as economic security, technological self-reliance, and supply chain resilience, in key sectors.

Leveraging financial resources

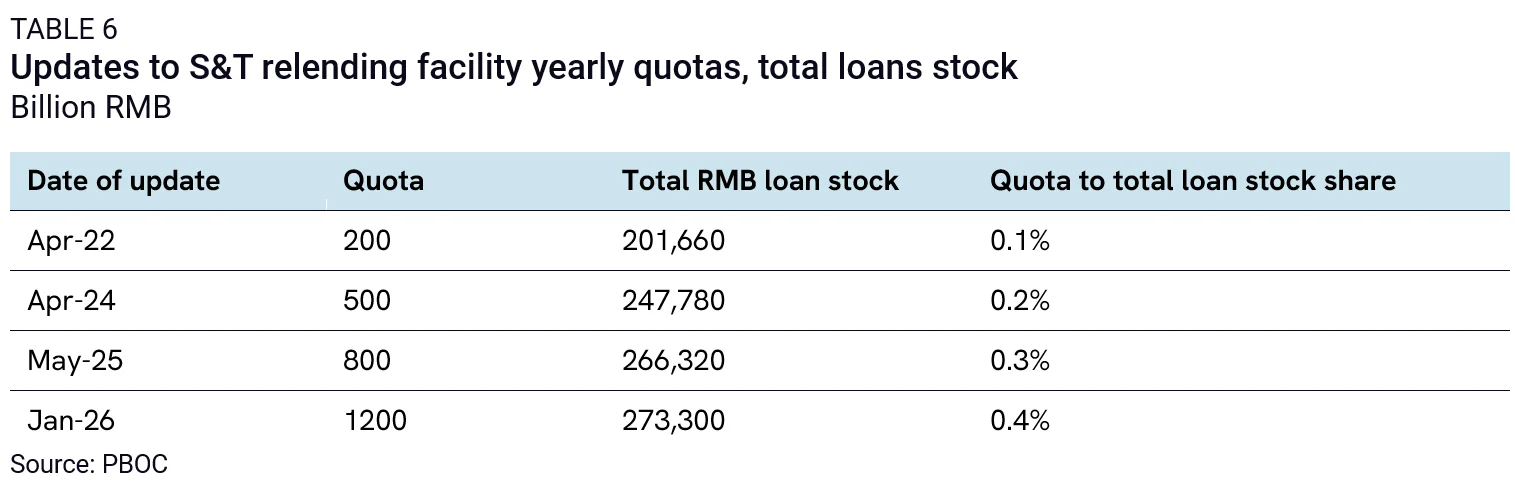

Beijing has expanded its control over bank lending decisions. Chinese authorities have long guided bank lending through a combination of regulatory tools and informal guidance, but in recent years, the People’s Bank of China (PBOC) has dramatically increased its ability to “guide” commercial bank lending to priority sectors. It has deployed a range of targeted relending facilities—low-cost central bank funding provided to banks, conditional on lending to designated sectors—as a way to incentivize and monitor banks’ support for the firms, technologies, industries, and even cities that central policymakers want to prioritize. Initially focused on rural finance and small businesses, these relending programs now channel hundreds of billions of dollars (trillions of yuan) to firms that advance science and technology, industrial upgrading, and strategic emerging industry objectives. The quota for the science and technology innovation relending facility increased from RMB 200 billion in 2022 to RMB 1.2 trillion by early 2026, equivalent to 0.4% of total RMB loan stock, and roughly 8% of new corporate lending (Table 6).

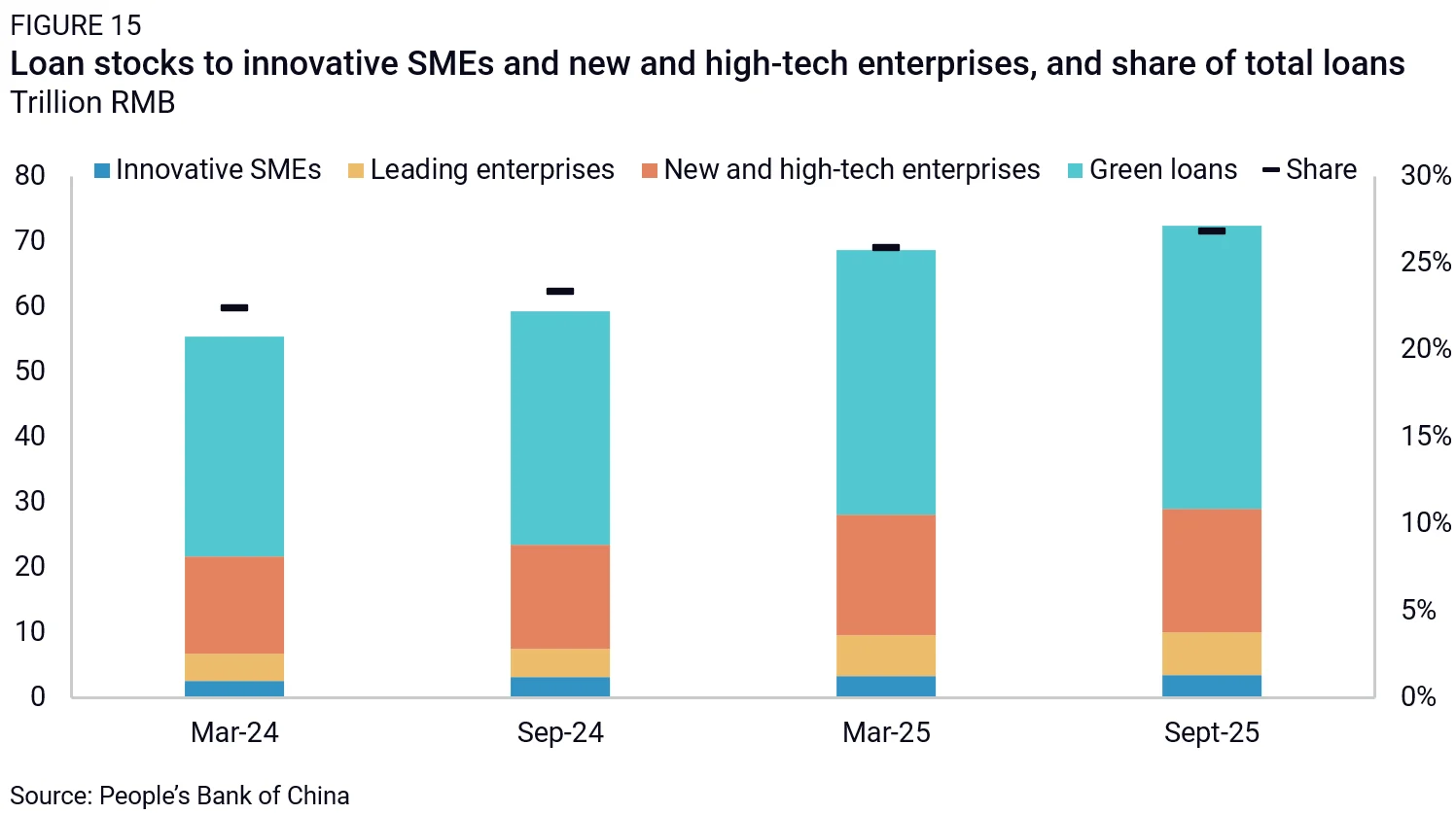

State-guided credit appears to be shifting toward innovative firms, including innovative SMEs, “new and high-tech enterprises,” and “leading enterprises,” categories that reflect different classification frameworks, all tied to technological capabilities, as determined by industrial planners. Together with loans to green loans, their share of total loan stock has increased from 22% to 27% over the past two years (Figure 15).

Lastly, China’s capital markets are also being reshaped to support industrial policy. After authorities tightened IPO approvals in 2023–2024 in a bid to stabilize equity markets, listing activity collapsed. Only about 100 companies completed A-share IPOs in 2024 (compared to 313 the previous year), raising RMB 675 billion, the lowest level in a decade. Beginning in 2025, regulators gradually reopened listing channels, but they did so selectively to prioritize strategic sectors. During the 14th Five-Year Plan period, the Shenzhen Stock Exchange added 649 new listed companies, of which high-tech enterprises and private enterprises each accounted for over 80%, and the proportion of specialized and innovative enterprises increased from 38% to 46%, with nearly half of the companies belonging to strategic emerging industries. Reforms to the STAR Market in 2025 aimed to further prioritize innovative and strategic companies. Upcoming reforms of ChiNext board have similar objectives.

Hong Kong is being repositioned as a complementary offshore financing channel, allowing capital to continue flowing to priority sectors under looser constraints. Investment from mainland investors into Hong Kong-listed equities has surged, from HKD 13.1 billion in 2014 to HKD 807.9 billion in 2024, reaching HKD 1,072.9 billion by September 2025. It is increasingly concentrated in sectors such as technology and healthcare. In parallel, Hong Kong’s IPO market has rebounded sharply after years of stagnation, with fundraising up over 220% year-on-year in 2025. Targeted regulatory reforms, including lower listing thresholds and fast-track channels for “innovative” firms, have supported this shift, effectively extending China’s industrial policy toolkit offshore.

The trade-offs of China’s industrial policy strategy

In the long term, the strategy Beijing is pursuing is likely to compound wasteful spending and inefficiency in the economy, even if it helps advance industrial goals in the short-term. By leaning on banks and capital markets to serve as a major policy instrument—for regional and other economic objectives, in addition to science and technology—the leadership is inserting non-market considerations into the DNA of its most important institutions. In the long-run, this will reduce resource efficiency, as capital and credit chase after policy priorities not profits. In the short run, it is also creating new pressures on bank profitability due to the strain of lending to SMEs and other low-return or high-risk endeavors. In capital markets, trying to do an industrial policy of everything also risks making the system less effective. The lack of clear prioritization may create more confusion for local governments and financial institutions tasked with implementation, and lead to capital being spread thinly rather than concentrated in strategic sectors and technologies.

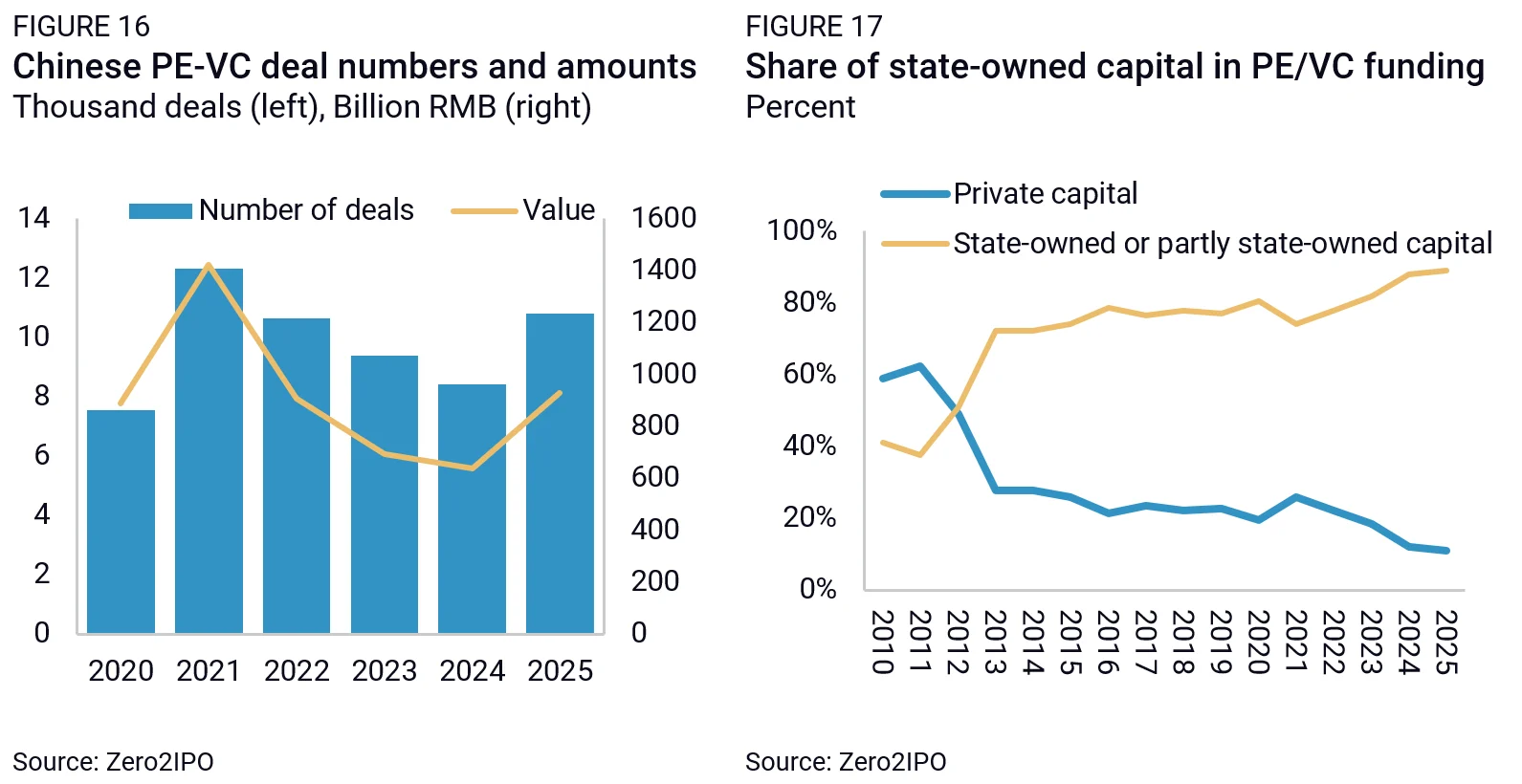

There are already clear signs of strain that will constrain the effectiveness of China’s industrial policy in the short term. Private equity and venture capital activity remains well below its 2021 peak (Figure 16)—partly because public capital crowded out private investors. Government-led funds contributed 81% of fund capital as limited partners in 2025, up from 65% in 2019, when accounting for investments made by SOEs (Figure 17).

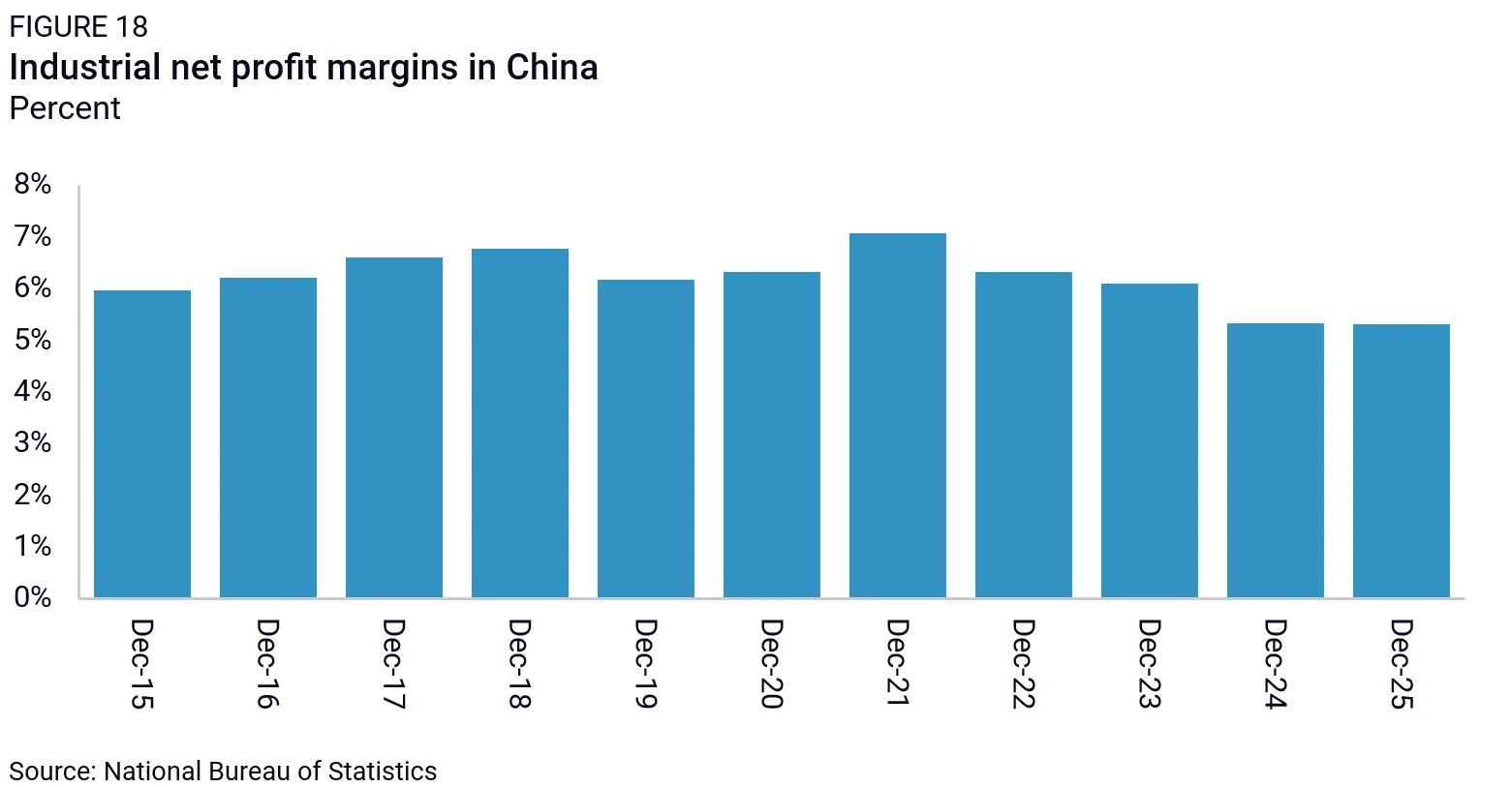

Corporate profitability in industrial sectors is at its lowest level in at least a decade (Figure 18). For many industries, from metals to automotive and ICT equipment, aggregate corporate profits have fallen in recent years.15 This means they have less ability to invest in Beijing’s industrial policy agenda.

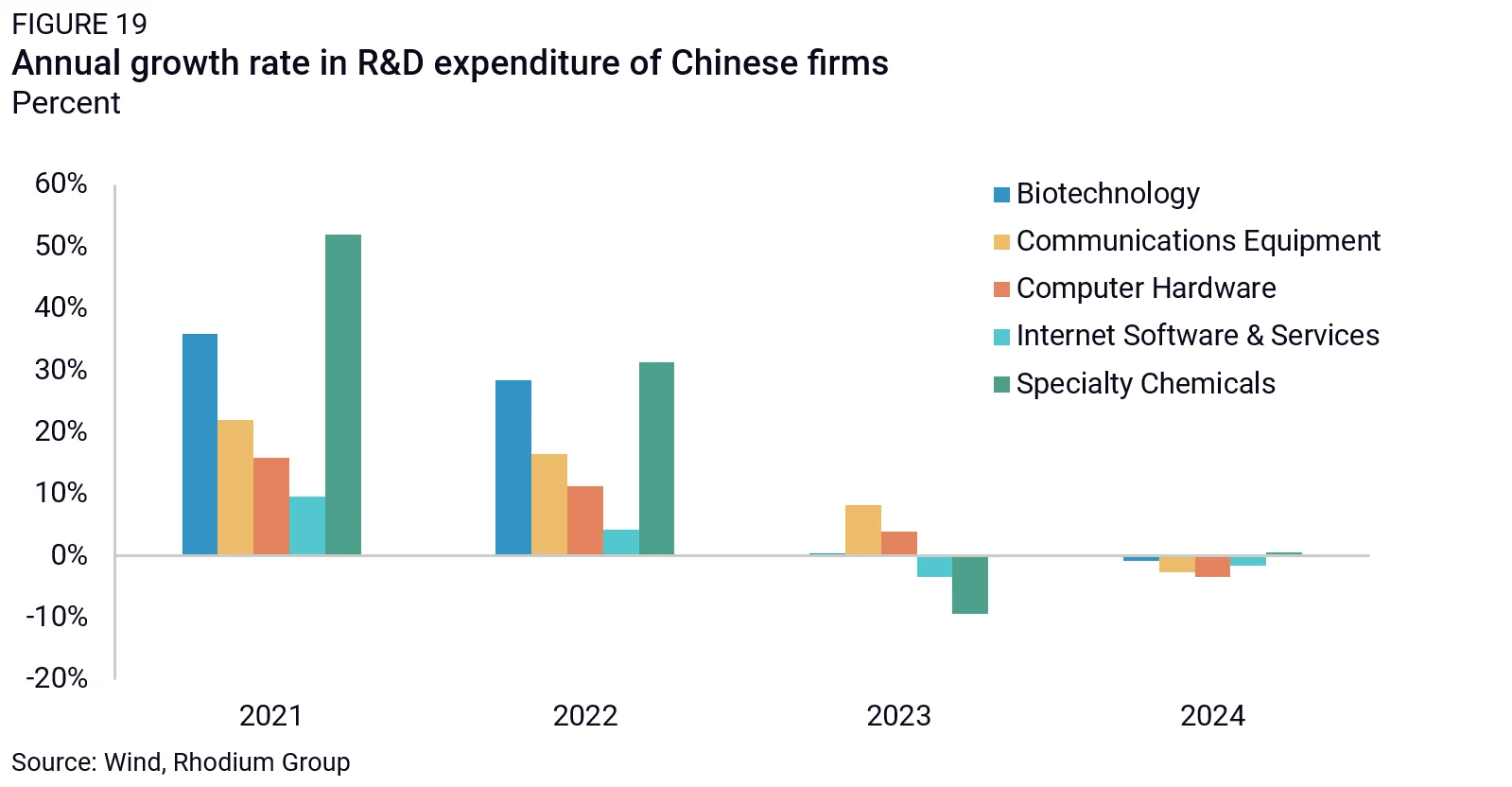

More concerning still, firms are starting to pull back on R&D spending, including in key sectors such as biotech, software, specialty chemicals, and computer hardware (Figure 19). This is not due to a lack of strategic importance, but a lack of financial capacity: Without sufficient profits, firms cannot sustain high levels of innovation investment. Absent meaningful reforms to boost demand or address structural overcapacity, this is likely to persist.

Lastly, at its core, the push to recentralize decision-making and refine industrial policy is at odds with Beijing’s stated ambition to support virtually all industrial sectors. One possibility is that headline ambitions mask a more selective prioritization of projects and key firms within target industries. Pressure will likely grow for this to happen over time, and it appears to be happening in some sectors, like semiconductors. But overall, available evidence suggests the opposite: Support is becoming more diffuse, including toward legacy and struggling sectors. The most likely outcome is that that overall industrial policy funding will become increasingly dispersed, even if fiscal and financial constraints mean that the pace of overall funding increase will slow.

Even if that proves to be the case, Beijing still commands vast resources across the economy, from banks and SOEs to public and private investors, and can sustain levels of industrial policy funding far beyond what most other countries can afford – at least for the next five years. More importantly, while sectoral prioritization remains unclear, Beijing has made clear that it will prioritize production overconsumption, and the growing scope of its industrial policy will only compound the economy’s bias toward industry.

This systemic bias within the Chinese economy, similar to what the IMF has termed “macro industrial policy,” is a central driver of structural imbalances. As we have documented in previous reports, political and financial incentives systematically direct fiscal and financial resources away from households and toward firms, especially in capital-intensive industries. Public spending is heavily skewed toward industrial infrastructure rather than public services, while widespread implicit guarantees encourage banks to extend large volumes of low-cost credit to companies to fund investments. At the same time, discrimination against foreign products and informal market access restrictions act as broad-based trade protection. On the demand side, consumption remains constrained by low household income and a highly unequal distribution of income.

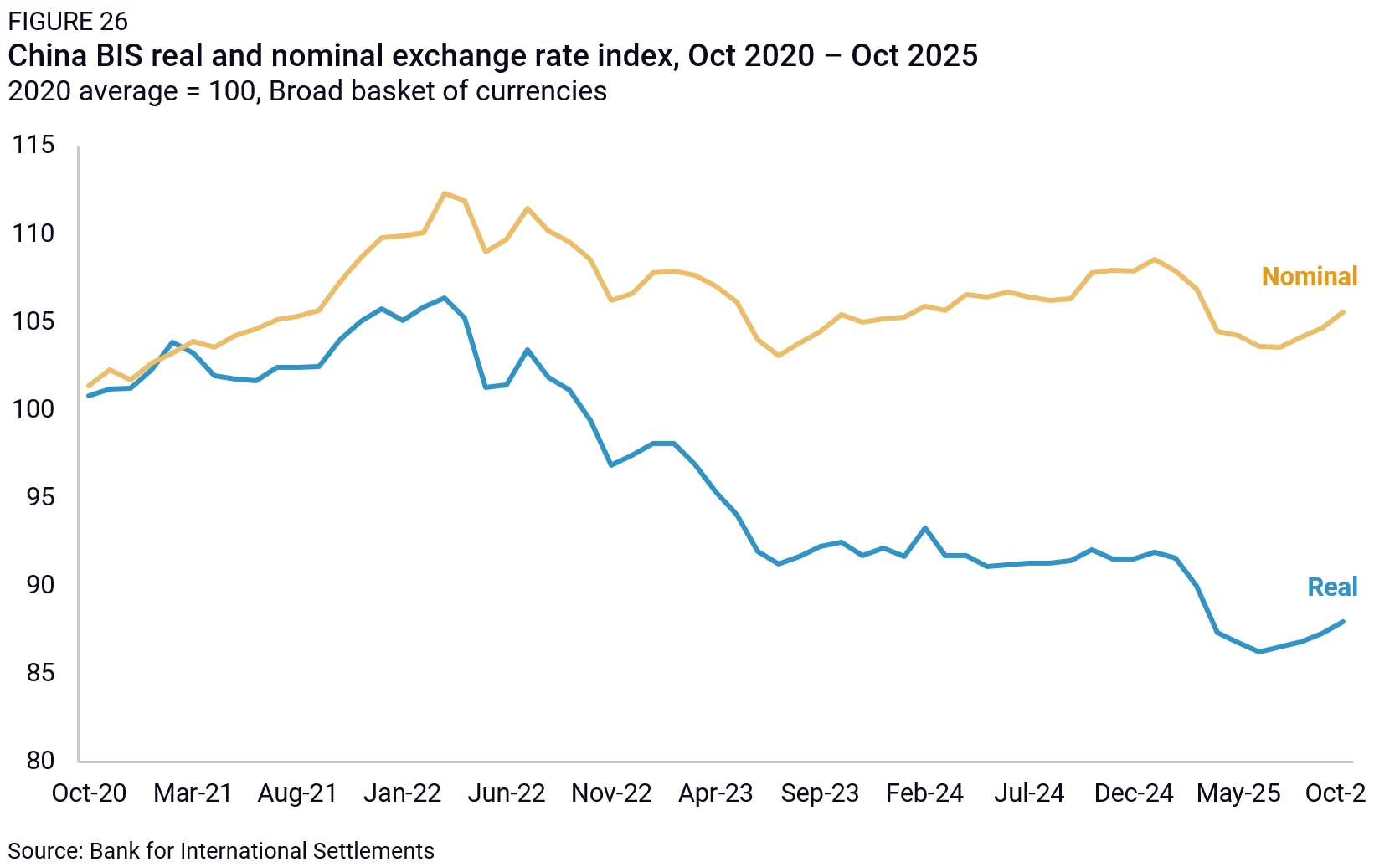

Foreign exchange dynamics exacerbate these imbalances. The RMB is widely considered undervalued, based on models of what levels might balance the current account. While the IMF conservatively estimated in February 2026 this undervaluation at about 16%, other analysts have estimated it at around 25%.

As the emphasis on industrial policy intensifies and efforts to boost domestic consumption remain limited, these dynamics are likely to strengthen. The result will be continued gains in manufacturing capacity, global market share, and China’s trade surplus. A return to a more state-directed economic model will further entrench these imbalances, making them difficult to unwind. Meaningful adjustment would require a fundamental restructuring of the economy, including fiscal reforms and a redistribution of income toward households.

Chapter 2: The global impacts of China’s industrial policy

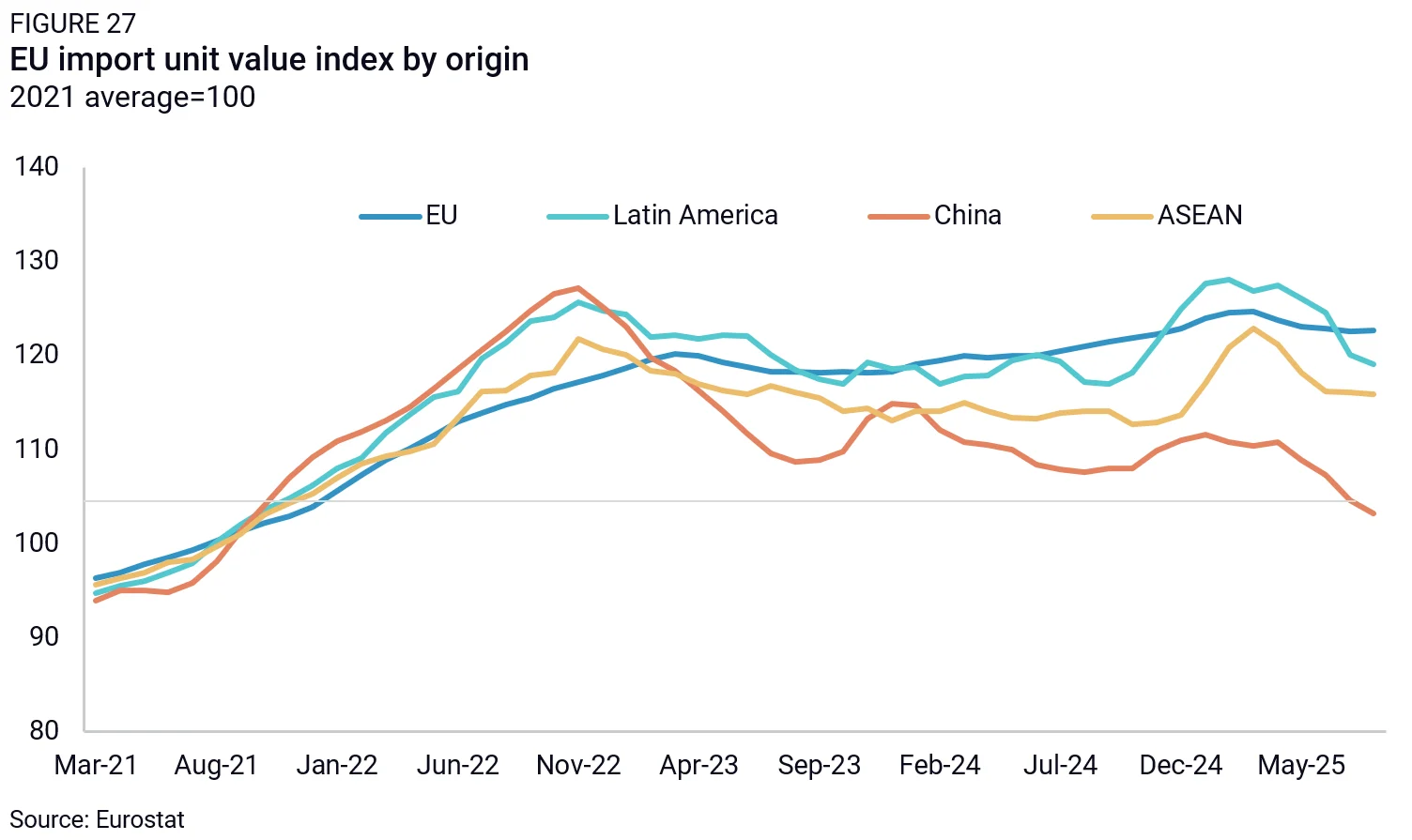

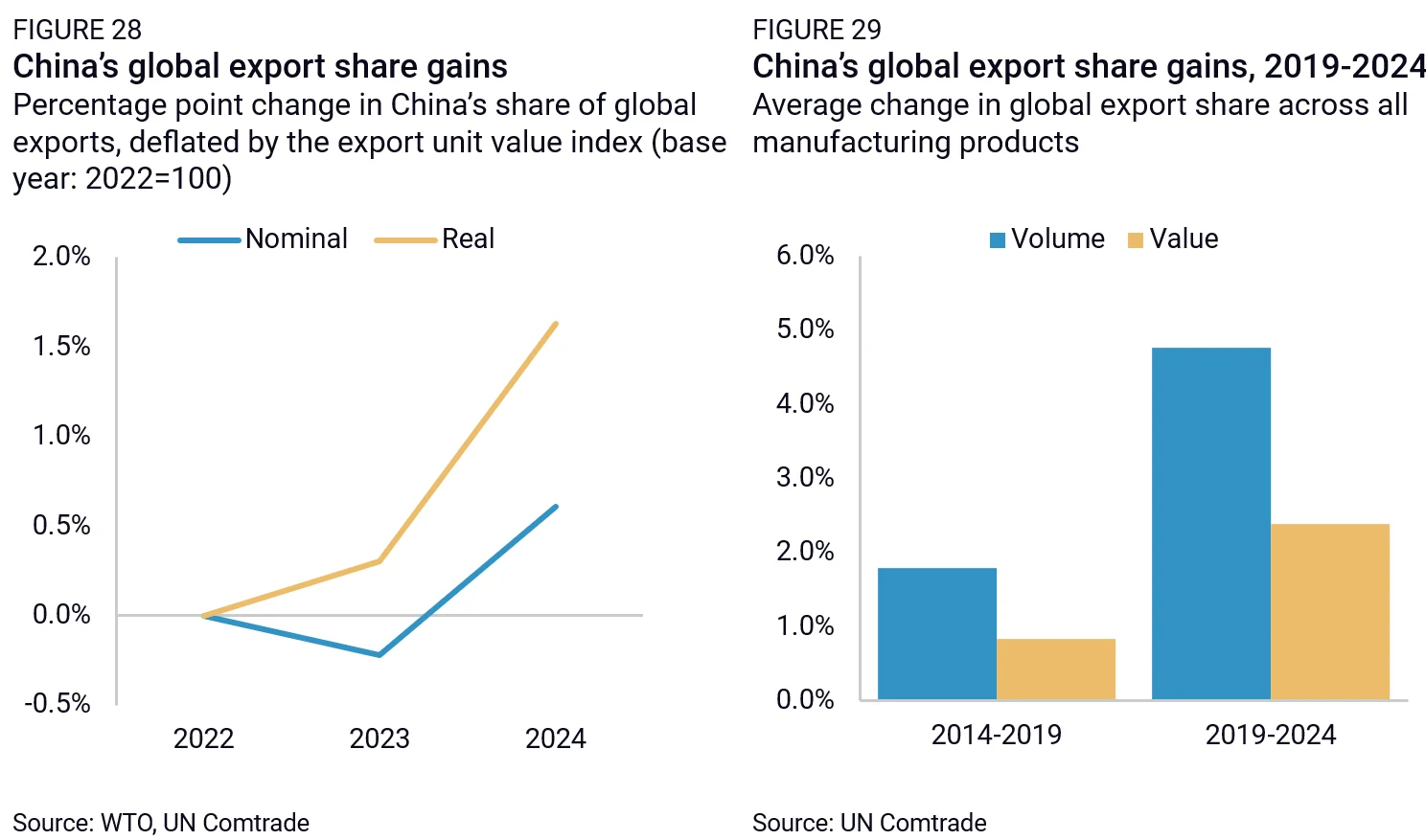

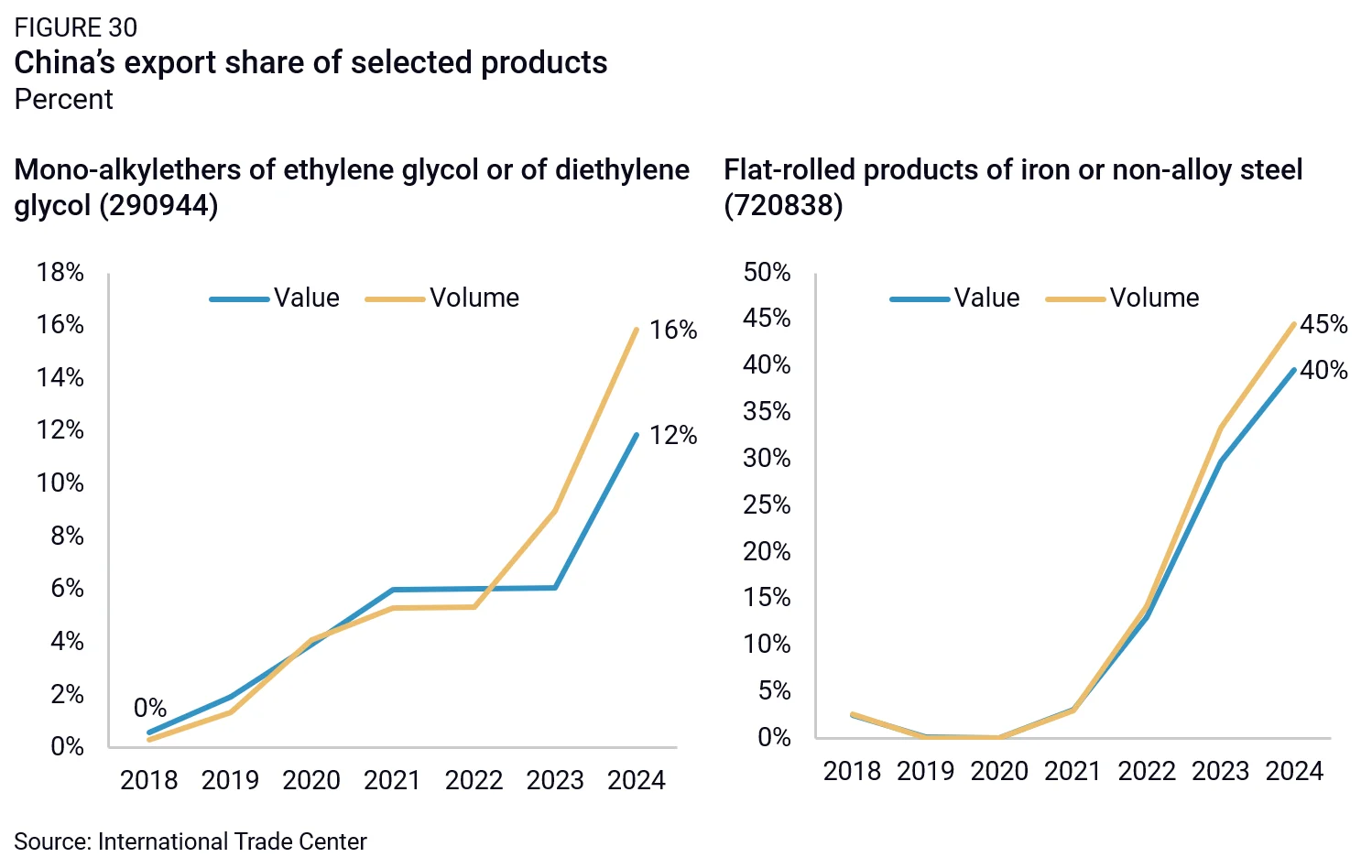

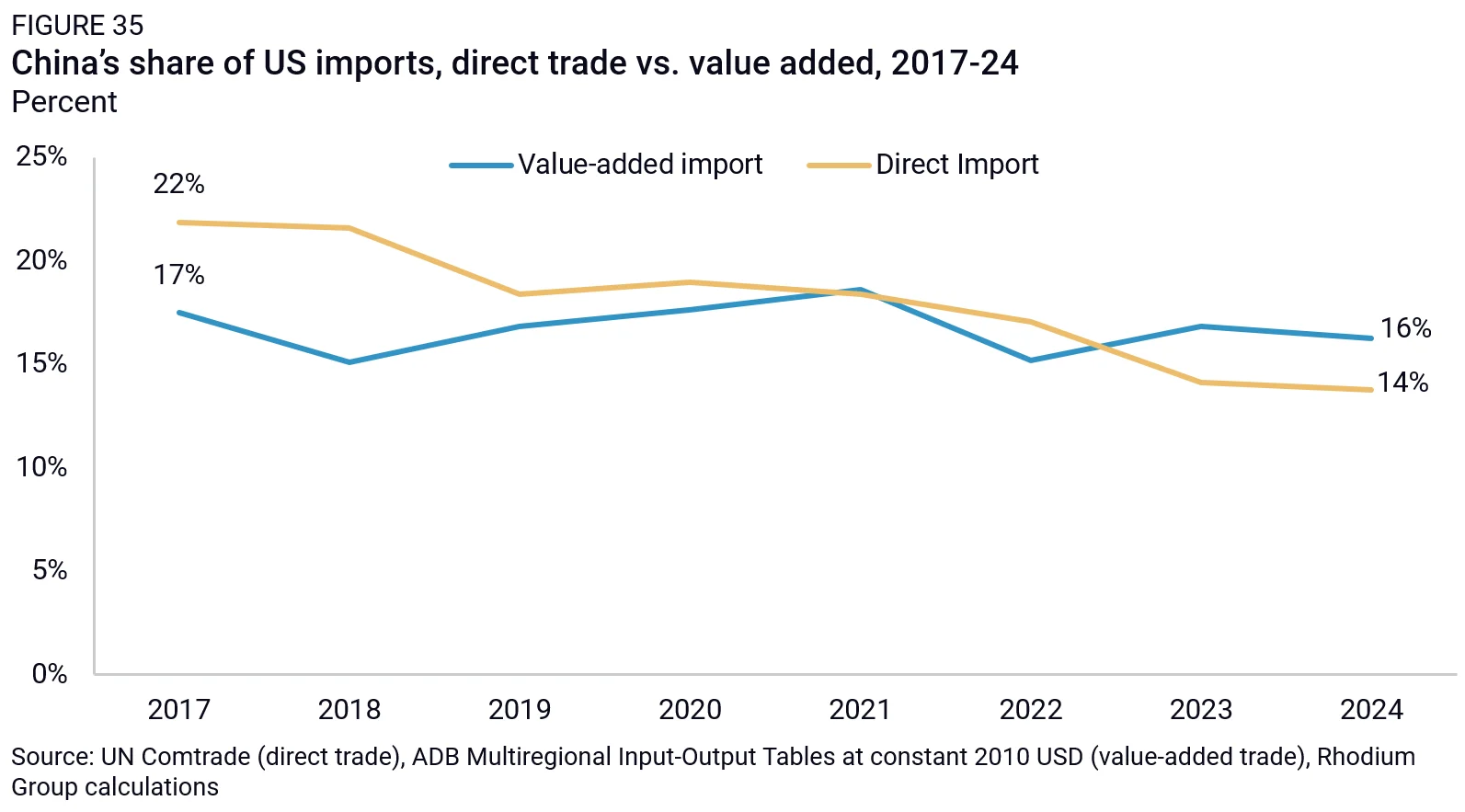

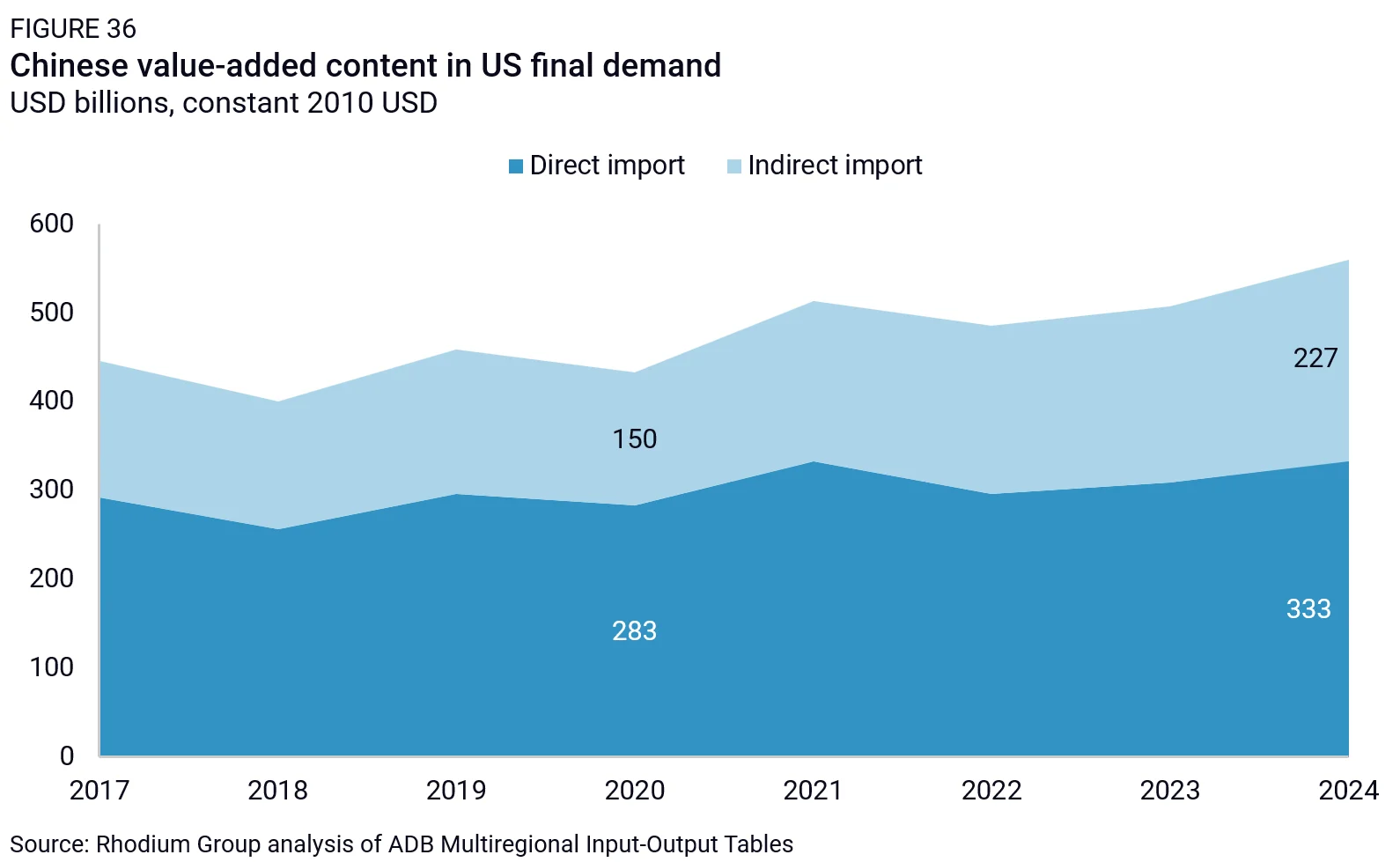

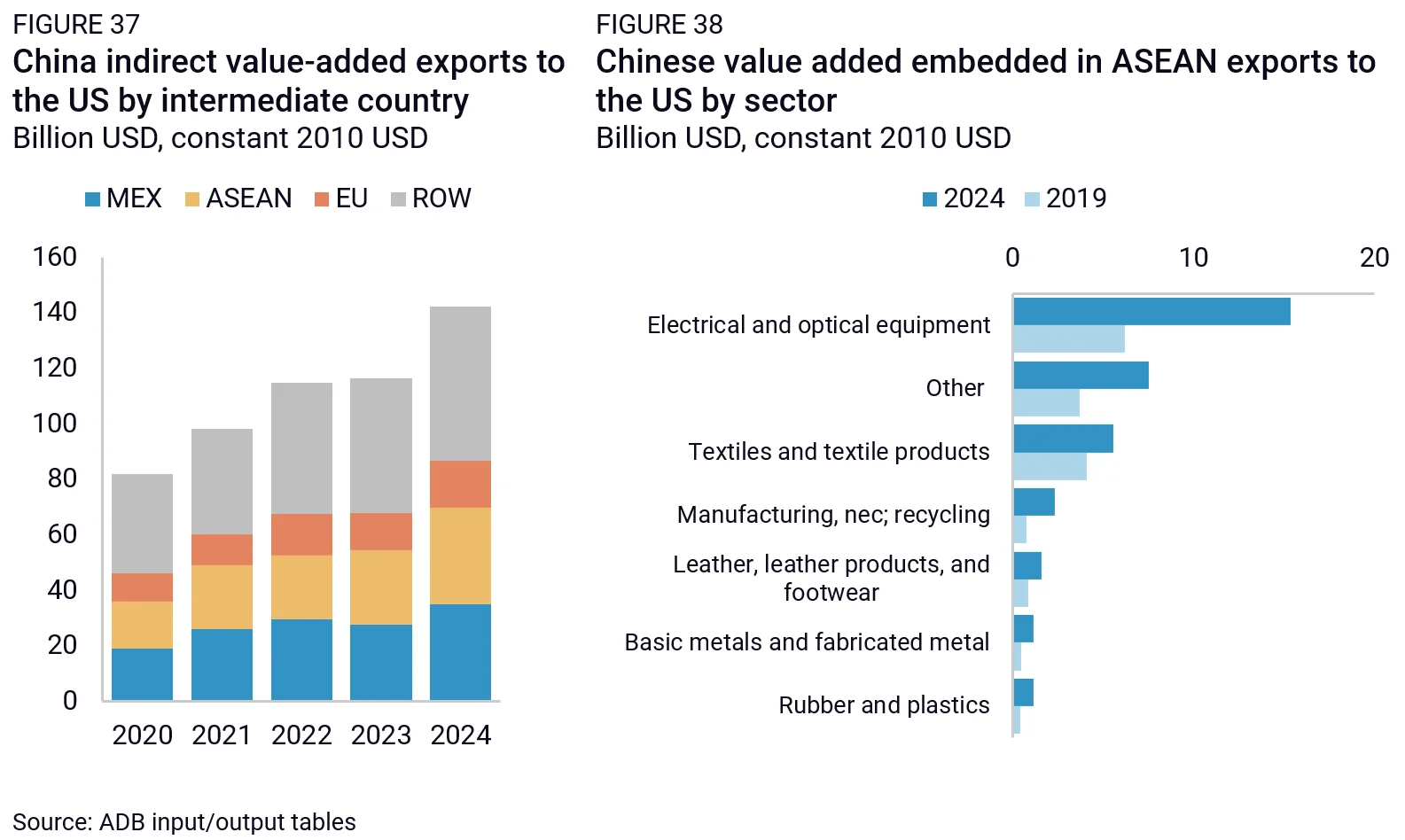

China’s industrial and economic policy has translated into a rapid expansion of China’s manufacturing trade surplus and trade dominance—a “China Shock 2.0,” where rising Chinese exports threaten industrial ecosystems in third countries. This expansion is concentrated in advanced manufacturing, with an acceleration in chemicals and machinery, deepening global dependencies at the upstream and midstream stages of production. The scale of this shift is larger than conventional trade data suggests. Standard trade statistics understate China’s market share gains because persistent producer-price deflation is compressing the nominal value of exports even as volumes surge. Dependence on China is also becoming more indirect and therefore less visible, as Chinese inputs, machinery, and components are increasingly embedded in goods produced and exported by third countries.

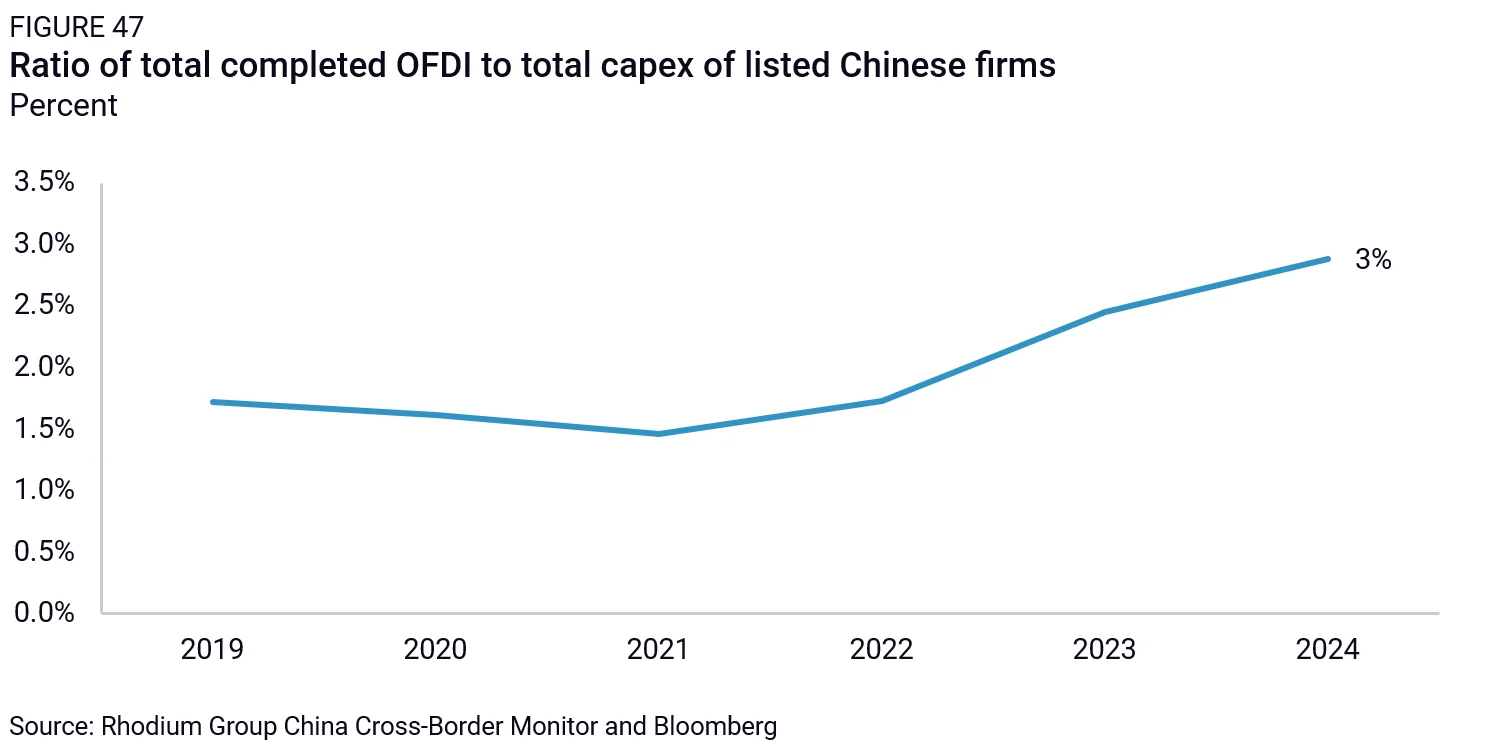

Chinese outbound investment is reinforcing this trend. Chinese firms are becoming true multinationals with operations spanning multiple countries around the world. The value of OFDI transactions announced by Chinese firms increased almost 20% year on year in 2025, more than double the value in 2020. Yet this fast expansion does not necessarily bring deep localization. Chinese firms often retain high-value activities, inputs, and technology within China, while Beijing is increasingly focused on preventing the kind of know-how diffusion that once helped China benefit from foreign direct investment.

Beijing is actively reinforcing this position and has expanded its toolkit to do so, through price suppression to displace competitors, control over inputs and technologies to restrict entry, the growing use of economic coercion to deter diversification, and strengthened control over companies’ activities overseas, including not only through technology controls but also travel restrictions on essential personnel, so that their investment footprint serves China’s domestic manufacturing dominance.

This chapter examines how that process is unfolding. The first section analyzes the rapid expansion of China’s trade dominance, including the rise in upstream and midstream dependencies and the growing importance of indirect exposure through third countries. It also highlights Beijing policies to entrench China’s manufacturing dominance and prevent other countries from de-risking. The second section turns to the rise of Chinese multinational firms, showing that, in many cases, their overseas expansion reinforces rather than reduces reliance on Chinese manufacturing.

1. Growing Chinese trade dominance

Since 2019, China’s industrial policy—both at the sectoral level and through macro-economic distortions—has combined with weak domestic demand to produce a rapid expansion of China’s manufacturing trade surplus. Advanced economies have framed this dynamic as a “China Shock 2.0” where rising Chinese exports threaten industrial ecosystems in third countries. But standard trade data understate the scale of the shift, because deflation in China is masking the true pace of global market share gains. Adjusted for price effects, China’s share of global exports has been increasing at nearly double the nominal pace between 2022 and 2024 (by 1.6 percentage points, rather than 0.6 percentage points in nominal terms).

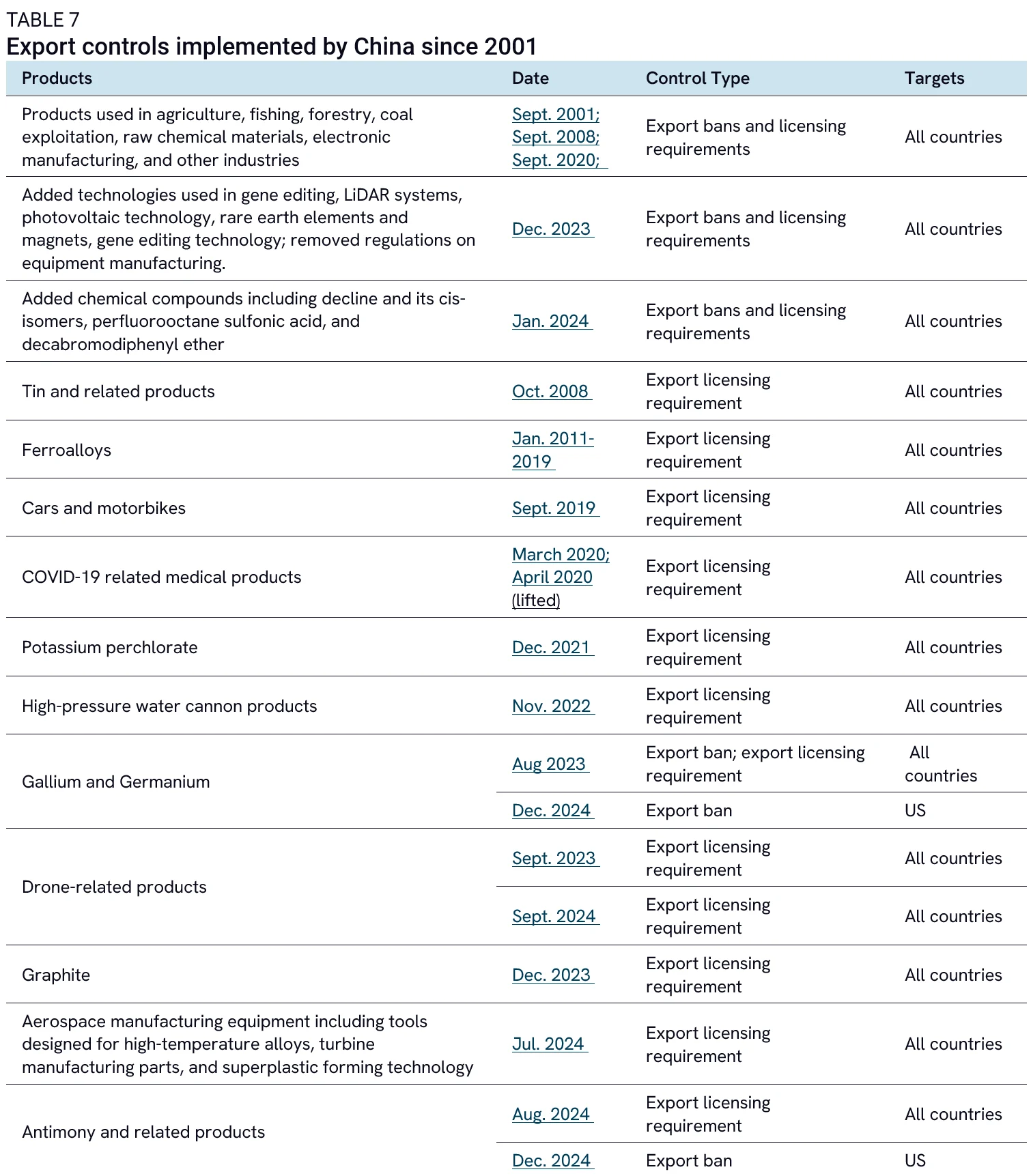

This expansion is concentrated in advanced manufacturing, with an acceleration in chemicals and machinery, deepening global dependencies at the upstream and midstream stages of production. Chinese value added is also increasingly embedded in third-country exports, creating indirect dependencies that standard trade statistics fail to capture. These trends are reinforced by policy tools such as export controls that allow China to maintain and extend its dominance.

Growing trade surplus concentrated in advanced manufacturing

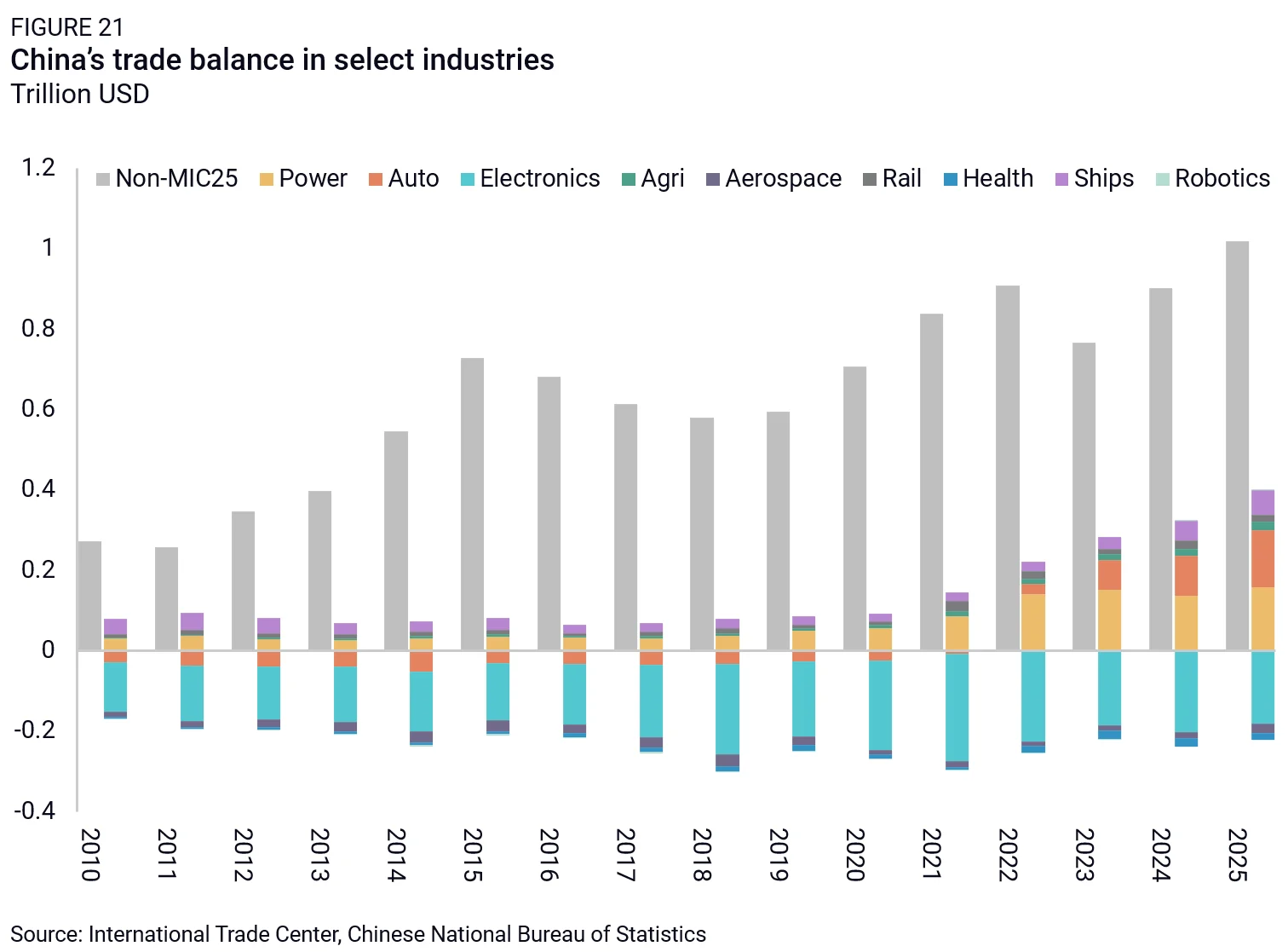

In the past few years, Chinese companies across a wide range of sectors have expanded production capacity far faster than domestic demand can absorb. While these imbalances are not new, they have reached unprecedented levels since the pandemic: China’s overall trade surplus has nearly tripled over the past six years. The manufacturing trade surplus is even larger, doubling from roughly $1 trillion in 2019 to about $2 trillion—an increase equivalent to the entire GDP of Switzerland. As a share of GDP, the surplus is now over 6%, a 15-year high.

This growing trade surplus reflects both rising exports and success in substituting them away from imports. On the export side, Chinese manufacturing exports grew by around 11% between 2021 and 2025, with much of the increase directed toward Asia. Countries such as Vietnam (up 45%, or $58 billion), India, Russia, and Thailand have been key recipients. At the same time, imports have weakened, particularly affecting major manufacturing economies. German exports to China fell by 25% between 2021 and 2025, a loss of nearly €31 billion, equivalent to about 2% of Germany’s total exports in 2021. China dropped from Germany’s second-largest export market to sixth. Japan experienced a similar decline, with exports to China also down 25% ($38 billion), representing more than 5% of its 2021 exports. Other economies, including Malaysia, have also been affected: Its exports to China fell by 5% over the same period, with China slipping from its largest to third-largest export destination. Overall, the European Union and ASEAN have been the most affected by China’s growing trade surplus, each accounting for roughly one-third of this increase, with the remaining third spread across other markets.