Chinese Credit Stimulus: Yesterday’s Solution, Not Today’s

In 2008, China launched a massive investment-led stimulus effort. Now, observers are asking whether China will do it again. This time, Beijing does not have the option.

In the teeth of the 2008-09 global financial crisis, China launched a massive investment-led stimulus effort, funded by banking system credit, leading the globe toward recovery. Now, facing a global economic downturn of similar or greater magnitude from the Covid-19 outbreak, observers are asking whether China will do it again. This time, Beijing does not have the option.

Chinese policy-makers are limited by an impaired financial system unable to generate anywhere close to the same volume of credit as in the past. Most of the credit that can be disbursed will just pay interest on the debt incurred after 2008, rather than fund anything new. Past reform delays leave China facing an ugly choice: reduce the magnitude of tomorrow’s debt crisis by acting less heroically with stimulus today, or pull out all the stops to prop up current demand by walking further into a debt trap at home and still having no certainty of stabilizing economic conditions. Even Beijing’s “bazooka” options to boost the economy face difficulties supporting an impaired financial system and indebted state-owned and local government firms.

The Rebound and the Hangover

It feels like 2008 again, with financial markets melting down, the global economy approaching recession, and Beijing’s policy arsenal appearing as the world’s unlikely but most probable savior. China’s economy is moving gradually back toward full employment as migrant workers return to factories and construction sites after lockdowns and travel restrictions. Numbers of new Covid-19 cases reported in China, the origin of the outbreak, are now low, with most new cases imported. It is becoming possible to imagine a return to something like normal conditions by late April.

The January and February output data from China were abysmal, showing record declines in industrial value-added (-13.5%) and fixed asset investment (-24.5%). But at least these numbers are credible, which raises the chance for a stronger recovery in reported data later in the year. China’s GDP growth will undoubtedly drop to record lows in Q1 2020, but seems set to be the first to recover globally as the Western world stands just at the start of a similarly deep shutdown. This expectation of China as “first in, first out” again has driven a series of strange accusations and counter-accusations from nationalist elements both in China and the West.

Beijing’s public message is that their response to the virus was a triumph of the state and should be emulated; they still gloss over the cover-up in Hubei province and the threats to doctors and scientists that led to the virus spreading in the first place, and the political culture that enabled the outbreak has not been repaired. Nationalist voices in both China and the United States circulate reports that the virus is a weapon deployed by the other side. The reservoir of Western goodwill toward China was already low, and Beijing braggadocio while the US and Europe are combating the worst phase of the epidemic will certainly drain it further. Indeed, this is happening. China’s decision to expel all American journalists working at leading newspapers is the most recent provocation; failure to fasttrack export approvals for now-surplus personal protective equipment like medical masks is likely to be the next harrowing headline.

Given the depth of the first-quarter recession and progress restarting transport flows since then, China’s household consumption and services sector activity may start bouncing back starting in April or May, with manufacturing sector employment coming slowly back to make the necessary paychecks available. That is the household consumption component of GDP (“C”). But aggregate external demand for Chinese exports (the net exports component, “NX”) will be severely depressed for some time. Policy measures to boost domestic investment (“I”) as a counter-cyclical measure are the big uncertainty. Talk about providing credit for investment is ample: but do the mechanics of the financing system make it possible? If there is no confidence in the economy, then even cheap credit goes unused by more productive firms. Beijing has instructed state-owned enterprises at the center of funding chains to advance payments to both customers and suppliers to support confidence. This is likely to be more effective than simply ordering commercial banks to lend to SMEs, but pre-payment (or just “on time”) by SOEs is an untested solution, and no one can yet say how close it can come to satisfying corporate funding needs.

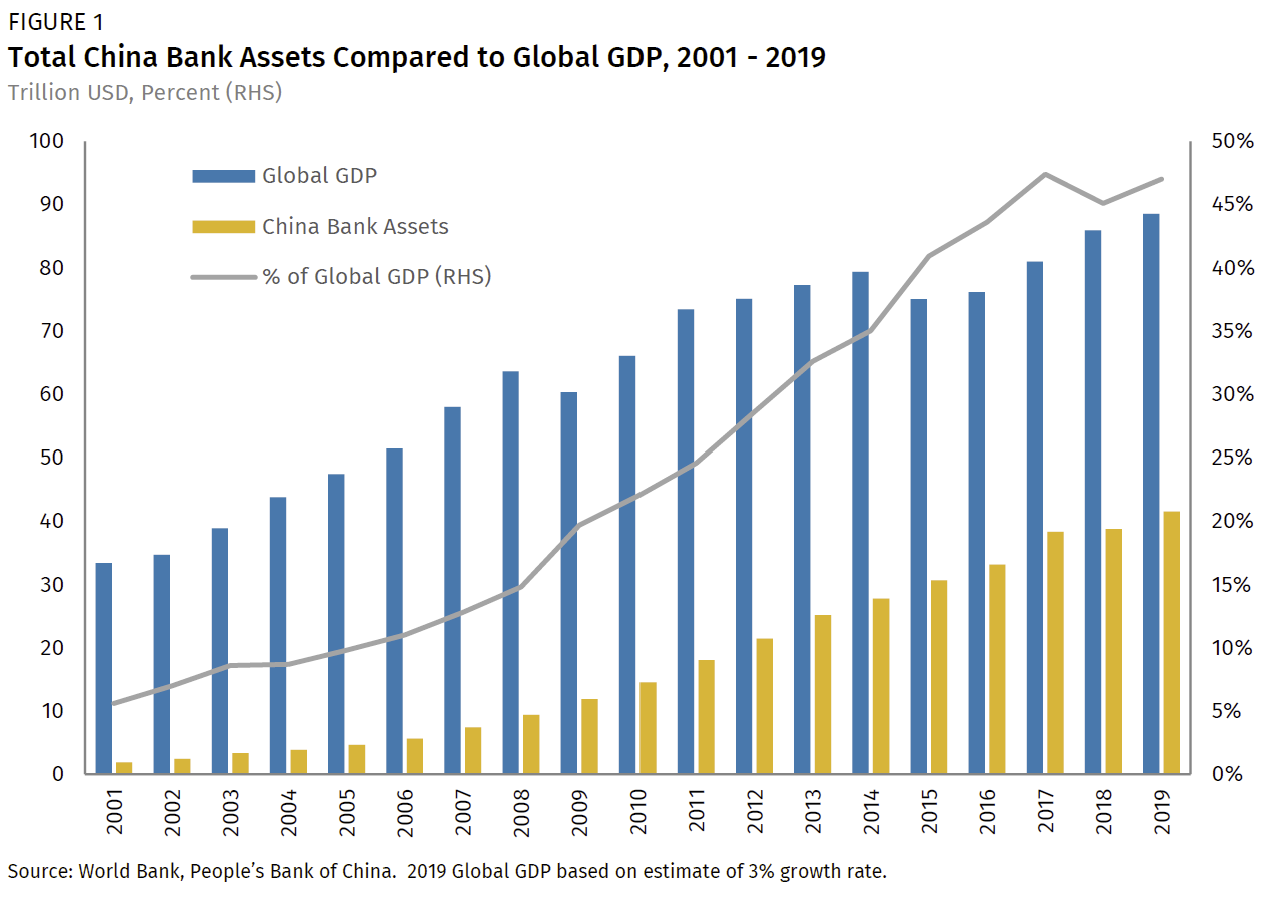

Most importantly, in contrast to 2008, China no longer has a financial system with which it can fire a policy “bazooka” to allay all fears about the sustainability of economic activity. For more than a decade China’s banking system has expanded faster as a proportion of the global economy than any other over the past century. Having quadrupled in size since 2008, it cannot quadruple again. The property market has absorbed a vast amount of investment over the past decade and is highly vulnerable to a price correction that appears underway. Beijing knows this, and wants to avoid a collapse in the property market, but does not want to see even more property speculation make the risk higher still. The hangover after the near-term jolt in activity will be intense when credit growth necessarily slows and property prices slide.

In contrast to 2008, China no longer has a healthy financial system with which it can fire a policy bazooka, or lean upon to generate enough credit and investment to sustain economic activity as we’ve known it.

Over a decade after the global financial crisis, delays in reform of China’s economy now result in less capacity to manage challenges. Economic growth depends more on state-led investment and credit than in economies where private sector activity and consumption-driven growth dominate. This is a problem: potential growth will slow throughout the coming decade in tandem with non-performing asset growth in the financial system, with limited options to smooth the descent.

The options Beijing used in the past included smoothing short-term data to reduce the risk aversion natural in a business cycle and thus keep activity above the troughs that are typical in a cycle. In times of crisis, Beijing also made systemically large injections of financing via fiscal or monetary policy to put a floor under activity. Short-term smoothing today is beyond the point, as sentiment is impossible to gladhand given the immensity of the economic shocks currently underway. And the “bazooka” options are also limited.

Why the Financial System was Yesterday’s Solution and Today’s Problem

The reasons why a flood of Chinese financing cannot be trusted to sustain a domestic recovery, let along a global one, require further elaboration. In 2008, China’s financial system was a partial workaround to the problem of slow policy implementation around the world. Rather than waiting for government bond sales and fiscal allocations to China’s local governments, Beijing instructed banks to lend to them and related companies—massively, growing aggregate bank assets within the economy by 50% in the two years from 2008 to 2010 and kicking off an infrastructure and property construction boom. The financial system was a solution.

Now, the financial system is a big part of the problem. (We will turn to possible solutions below.) It has increased in size by 4.5 times since the global financial crisis, rising from 64.2 trillion yuan ($9.4 trillion) in assets as of the end of 2008 to 292.5 trillion yuan as of last month ($41.8 trillion). To put the current value in context, it represents about half of global GDP. In the same interval, China’s GDP roughly tripled in size, adding around $9 trillion in annual output.

But that growth was overwhelmingly dependent upon the financial system itself funding output-demand expansion. That is, the level of GDP activity is predicated on debt, not sustainable demand. And thus the growth of that debt is the essential question. Interest on credit in China’s economy has exceeded nominal GDP growth since 2012, and even conservative estimates suggest interest on debt absorbs more than half of new credit extended every year, meaning most new credit just pays bankers, it doesn’t fund new productive activity. These financial conditions cannot drive growth as was seen in China’s past. Credit growth has now slowed, from a pace of 18% between 2007 and 2016, to an average of 7.7% over the past two years, leaving even less for healthy new activity.

Our own analysis of the 49 listed banks reveals about 1.5 trillion yuan in unrecognized overdue, restructured, or otherwise undeclared non-performing loans on top of the supposedly modest 2% non-performing loans (NPLs) in official data (as of the end of February: see our Feb. 10, “The Virus Spreads to Banks”). Undoubtedly the true level is much higher than this, given the magnitude of the growth in credit relative to underlying economic performance. Financial statements from smaller banks seeking private share placements often reveal NPL levels of 9-20% or higher, but these are unaudited. Four banks had to be explicitly restructured last year for the first time since the 1990s, after the surprise default of Baoshang Bank in May 2019.

China’s banking system is too unprofitable to continue growing at double-digit rates. Banks need capital to continue expanding credit, and most bank capital growth in China comes from bank profits themselves. Yet returns on assets throughout the banking system are only around 1%, and banks must pay dividends to the state and other shareholders out of these profits. Therefore, any recognition of loan losses will require provisioning or writeoffs, reducing profitability further, limiting bank recapitalization out of retained earnings, and slowing future growth. This is the tradeoff between cleaning up today to prevent failures, and propping up growth.

There are many banks similar to Baoshang in terms of reliance upon interbank or wholesale funding, who also hold large pools of riskier shadow banking assets.

The risk introduced to the banking sector last year with the failure of Baoshang Bank in Inner Mongolia will not disappear. 2019 was a watershed year for China financial system credit risk, with banks, local government financing vehicles, and state-owned enterprises defaulting on their interbank liabilities or debt, with local governments such as Tianjin now unable to support their state-owned enterprises. Traders are reluctant to lend to riskier banks liable to face losses, and increasingly uncertain which those are. Most assume that more bailouts for bank failures will follow, but at some point, the number of bank failures will be too large for the government to support. As long as that point was in 2021 or later, the rise in bank defaults would probably be tolerated, but evidence suggests that “some point” could emerge even this year. There are many banks similar to Baoshang in terms of reliance upon interbank or wholesale funding, with large pools of risky shadow banking assets on their books.

Chinese banks vary in asset quality, of course, but this is a system-wide problem: maintaining regulatory capital requirements requires slower asset growth, and in a credit-fueled economy that by definition means slower economic growth. Relaxing capital requirements permits more asset growth, but larger proportions of credit simply roll over interest on existing debt. Reducing interest rates to reduce the drain of corporate interest burdens on the economy reduces bank profitability and capacity to grow and power the economy. There is no easy way out of this problem, even if the state wanted to take a much larger short-term role within the banking system.

Beijing needs to worry about the short term before it can address the next few years. Existing financial system pressures and the virus outbreak are creating additional non-performing loan pressures for China’s banks. Officially, the banking regulator has urged banks to exercise forbearance and avoid recognition of non-performing loans for firms in Hubei province and others that “have been impacted” by the outbreak. This does not mean the loans are being repaid, nor removed from the burden of corporate liabilities.

So Then What?

The magnitude of the current crisis calls for policy-makers globally to think big about solutions. The US Federal Reserve and European Central Bank acted aggressively last week and today, and additional fiscal policy support from developed economies will follow. For China, if short-term palliatives like data smoothing are out (and frank January-February numbers suggest they are), and traditional “bazooka” deployments of liquidity are too likely to backfire, then what are Beijing’s options and what is it likely to do?

First, China does have conventional large-scale policy options. Beijing’s focus should be on policies that can unleash credit and investment by increasing room for restructuring. Fiscal policy support for the economy can be a short-term palliative, but in China, the benefit of even a significant boost in fiscal stimulus will be limited because the fiscal policy stance is already very supportive. Most fiscal stimulus comes in the form of local government special revenue bonds (SRBs), of which over 3 trillion yuan are expected to be sold this year, up from 2.15 trillion yuan last year. The problem is that the proceeds of these bonds are ultimately channeled to the same companies—local SOEs and LGFVs—that are struggling with high debt levels and need to manage interest burdens as well as continuing infrastructure construction projects. Structural reform means creating space for firms that are not maxed out on debt to invest in order to take market share and increase their future presence.

Beijing may also employ “bazooka-lite” approaches to boost growth while bypassing the stressed financial system. A massive bailout of banks via the creation of another multi-trillion yuan asset management company (AMC) to buy bad loans at marginal discounts (at perhaps 75% of par value) could help banks shed those loans and improve credit transmission. The problem with this idea is that China has over 4,000 banks, and only a few hundred of them produce credible financial information that would allow a rational troubled assets takeover program.

Another potential solution could be a significant upgrade in the role of the policy banks to fund investment, with funding provided directly via Pledged Supplementary Lending (PSL) from the central bank’s balance sheet. While this bypasses commercial banks, the resulting investment projects would still need to be executed by debt-laden state-owned companies. This obstacle was one reason that local government financing vehicles were created in the first place in 2009-10—because something with a clean balance sheet needed to exist. Beijing is unlikely to walk that road again after trying for the last decade to clean up the resulting mess, especially because the next round of hastily announced infrastructure investment projects would be even less productive than the last, after a decade of funding for anything that could be put on paper.

Reducing localities’ interest burdens by refinancing local government debt as lower-cost central government debt would be another option, but this would further reduce bank profitability, since banks are primary holders of existing government bonds. Massive consumption subsidies might boost household disposable incomes in the short term, but would do little to alleviate the financial system problem hanging over long-term growth potential.

So what do we think Beijing will actually do?

Despite global calls for China to “go big” Beijing is likely to stay more cautious than in 2008. Beijing will attempt to maintain cyclical momentum in domestic demand, but fixate on keeping that support at home. Fiscal policy will be more expansive, with additional local government SRB issuance and a larger fiscal deficit. Interest rates will almost certainly move lower to keep real borrowing costs stable in the face of deflationary pressure. And as the US dollar is rising while external demand falters, it is probable that the central bank will permit some degree of yuan depreciation rather than defend a certain level; that process has already started, with the yuan weakening below 7.10 per dollar in the past week (but still rising on a trade-weighted basis). Bank bailouts and rescues will continue, but most likely reactively, after financial stress emerges.

Damage to the financial system in the form of a banking crisis would take growth projections even lower.

But none of those short-term measures will alter the rising vulnerabilities in China’s financial system, nor provide a sustainable driver of medium-term growth. China is unlikely to place a floor under the global economy. In that way, China’s position is now similar to that of France in the early years of the Great Depression in the 1930s, running larger surpluses than its trading partners, but unwilling and unable to act more aggressively to prop up domestic demand that might alleviate global deflationary pressures.

China’s potential GDP growth rate has slowed. Demographic change is one reason: the workforce is shrinking, and the labor variable subtracts from growth rather than boosting it. Policy reform used to bring GDP gains in the form of more productivity driven by capital formation, but for all the reasons discussed above, that is flatlining. The logical takeaway is that potential GDP growth (what can be expected over time once cyclical tinkering averages out, since stimulus today must be paid back tomorrow) has fallen to 3-4% over the next five years, if all goes well! A banking crisis would reduce potential growth projections further, by further disrupting fixed capital formation.

Beijing’s headline external policy message has been the inevitability of China’s economic rise. This anchors both its foreign policy and its nationalist political economy at home. Doubts about that narrative were on the rise pre-virus. It is too soon to stocktake the additional damage to global confidence in China’s future footprint from the health calamity slamming the planet, inside and outside the Middle Kingdom where it originated. But beyond a doubt, any commercial or geostrategic assumption underpinned by faith in the credibility of China’s system and stimulus should be discounted.