Clean Hydrogen: A Versatile Tool for Decarbonization

As Congress considers policy support for hydrogen technologies, it is essential to understand the distinction between how we use hydrogen today and the role of hydrogen in a decarbonized US economy.

As Congress considers policy support for hydrogen technologies, it is essential to understand the distinction between how we use hydrogen today and the role of hydrogen in a decarbonized US economy. Hydrogen currently plays a crucial function in our economy, primarily as an industrial feedstock. Nearly all of today’s supply is from steam methane reformation, an emissions-intensive form of hydrogen production made from natural gas. Retrofitting these facilities with carbon capture is important for near-term carbon emissions reductions. Carbon capture is a cost-effective and commercial technology that can abate nearly 40 million metric tons (MMt) of CO2 emissions per year that current hydrogen facilities would otherwise emit.

While carbon capture minimizes the industry’s present carbon emissions, emerging forms of clean hydrogen (such as hydrogen produced from water via electrolysis) will play a prominent role in long-term decarbonization. Clean hydrogen has three primary applications in a decarbonized economy: energy storage and load balancing, as a feedstock, and as a fuel. These applications occur in all sectors, including transportation, industry, agriculture, and power. Due to its versatility and scalability, clean hydrogen could be a game changer in economy-wide decarbonization.

However, because steam methane reformation is cheap, it will be difficult for clean hydrogen to be competitive without policy support. In order to accelerate clean hydrogen and solidify US leadership on this emerging technology, Congress should pursue new policies and enhancements to existing policies that can bolster deployment. In this note, we discuss the decarbonization and economic benefits of clean hydrogen and assess policy options for scaling it up. We also assess the benefits of and policy options for retrofitting existing hydrogen facilities with carbon capture.

The resurgence of hydrogen

It may seem like hydrogen is a new hot topic in the energy policy world, but this isn’t the element’s first time in the limelight. In the early 2000s, the Bush administration approached energy with a focus on innovation and research and development. As such, hydrogen advancements were a key part of the administration’s Energy Policy Act of 2005 to reduce both the US’s dependence on imported oil and greenhouse gas emissions.

In the wake of the 2008 recession, US energy policy shifted under the Obama administration to focus on installing commercially-ready clean technologies to create job opportunities. Technologies like renewables and efficiency came to the forefront, and emerging technologies, such as hydrogen, took a back seat.

Today, it’s recognized that a hybrid approach to energy policy is necessary to reach climate targets—the US needs both rapid deployment of mature, clean technologies and continued innovation in new technologies. So, alongside growing climate concerns and technological advancements, the topic of hydrogen has made a resurgence in energy policy conversations in recent years, especially because of its versatility. Hydrogen already plays a crucial role in our economy as an industrial feedstock. It also has the potential to be a carbon-free fuel, feedstock, and energy storage technology to help balance a net-zero energy system. Due to its versatility, practically all sectors can use hydrogen, including transportation, industry, agriculture, and power. As a result, it provides a broader range of options when looking into our decarbonization toolkit.

To keep track of the numerous methods of hydrogen production, the dominant practice is to assign each strategy to a corresponding color. We believe this multicolored scheme is an oversimplification of the technologies and ultimately undercuts attempts to be technology-neutral. In reality, hydrogen production strategies (and the associated emissions) are more of a gradient than distinct colors. We believe society should eventually transition away from color-coding hydrogen; however, we sparingly use the various colors to better align our work with today’s broader conversation.

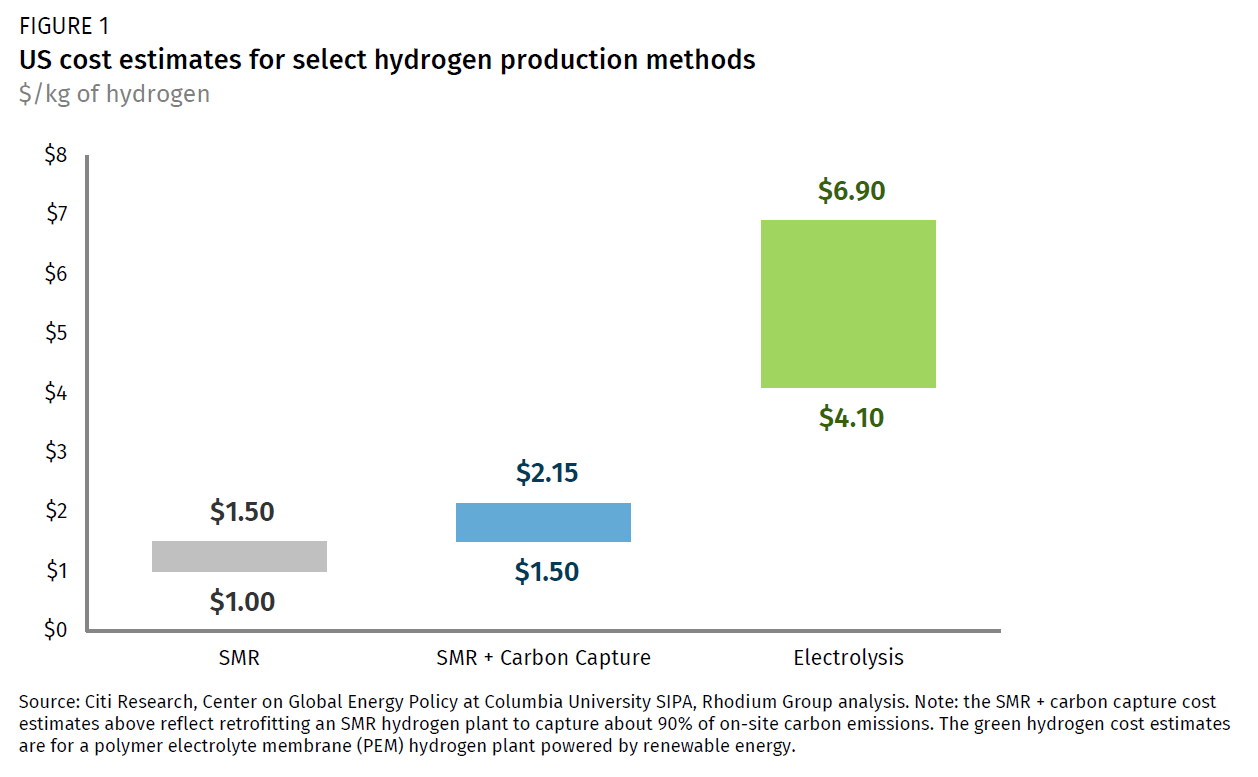

In this note, we primarily discuss three types of hydrogen production, commonly known as gray, blue, and green hydrogen. Gray hydrogen is the nickname for traditional hydrogen production via steam methane reformation (SMR), a process where hydrogen is produced from natural gas without any climate controls. Though it’s the dirtiest form of hydrogen production, it’s been around for nearly a century, making it the most widespread and cheapest form of hydrogen production. This note focuses on two types of hydrogen production that are referred to as “clean” hydrogen—blue and green. Blue hydrogen uses the same SMR process with the addition of carbon capture technology. Finally, green hydrogen is an emerging technology that separates hydrogen from water molecules via electrolysis. As long as zero-emissions electricity is the power source, green hydrogen results in no direct emissions and is one of the cleanest forms of production. It’s also currently 3 to 5 times more expensive than blue or gray hydrogen production (Figure 1).

We emphasize SMR retrofits and electrolysis as clean hydrogen options because they are receiving the most attention in the US context. It’s important to note that other clean hydrogen production methods can play a role in a decarbonized US economy as well. Two examples are autothermal reforming (ATR) and biomass gasification, both coupled with carbon capture. Similar to SMR, ATR also uses natural gas to produce hydrogen; however, it allows for a higher carbon capture rate (98% or more) at a lower cost. But the technology is not yet commercial in the US. Moreover, hydrogen produced via biomass gasification can result in negative emissions if the carbon is captured and stored. Yet, this is a nascent technology and will have to compete with other demands for biomass in a low-carbon energy system.

Carbon capture: the near-term decarbonization opportunity

In today’s economy, hydrogen is an essential feedstock for numerous industries, including refineries, fertilizer production, metal treatment, and petrochemicals such as plastics. Given its value across our economy, hydrogen production (and its associated emissions) will not be coming to a screeching halt in the next decade. Currently, SMR accounts for nearly all of the 10 million metric tons (MMt) of hydrogen produced in the US annually. These facilities contribute about 44 MMt of CO2 emissions per year, or about 3% of annual emissions from US industry.

SMR has two streams of carbon emissions: process emissions, a byproduct of hydrogen production, and combustion emissions from burning fuel. If carbon capture is applied to both the process and combustion emissions, it can capture almost all on-site carbon emissions. Though capturing nearly all of the facilities’ emissions is technically feasible with current carbon capture technology, the economics vary for the percent capture on a facility-by-facility basis. If carbon capture technology is added to existing SMR facilities assuming a 90% capture rate, it will capture nearly 40 MMt of CO2 emissions per year.

Since the technological processes are distinct, replacing SMR production with green hydrogen would require a complete overhaul of the facilities at inhibitive capital costs for at least the next decade. In contrast, carbon capture is a commercial technology that can be used to retrofit existing structures, making it the most economical and efficient way to achieve meaningful reductions in carbon emissions from current hydrogen production.

Though carbon capture retrofits will capture nearly all on-site carbon emissions from traditional hydrogen production, it does not account for the upstream methane emissions associated with natural gas production. Fortunately, the technology and policy mechanisms exist today to address upstream methane emissions in a low-cost manner. To successfully achieve a net-zero emissions economy, the US must include these mechanisms in policies supporting carbon capture retrofits to account for upstream emissions.

Carbon capture retrofit jobs

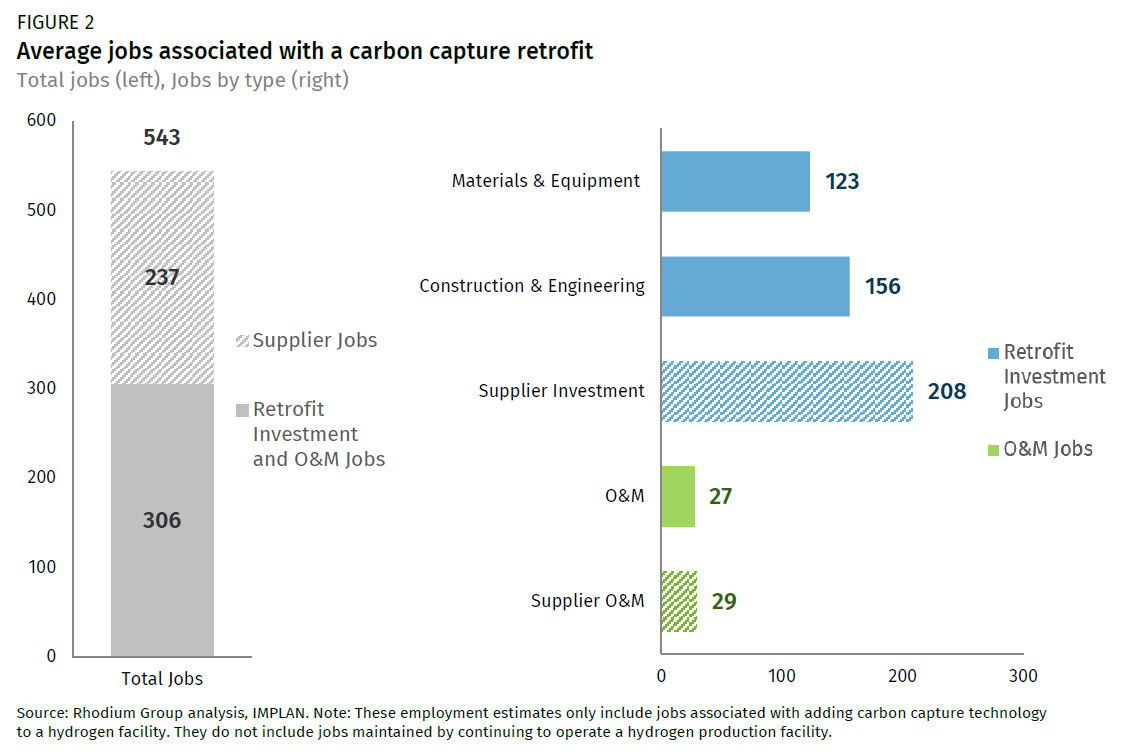

In addition to near-term climate benefits, carbon capture also has economic benefits. We estimate that, on average, 543 jobs are associated with retrofitting a typical gray hydrogen facility with carbon capture (Figure 2, left). This total includes 306 jobs to install and operate the retrofit technology and 237 jobs from the required supply chain.

Of these jobs, 487 are associated with the retrofit investment, including the necessary materials, equipment, construction, and engineering (Figure 2, right). There are also 56 ongoing jobs associated with the operations and maintenance (O&M) of the carbon capture technology (Figure 2, right).

Carbon capture retrofits will occur in communities where there are existing SMR facilities. Retrofitting all SMR facilities in the US with carbon capture would produce approximately 50,000 jobs. Much of this opportunity is in the Gulf Coast, with significant opportunities in the Midwest and California as well.

Clean hydrogen: the long-term decarbonization tool

It’s important to distinguish between the role hydrogen currently plays in the US economy and the potential demand for clean hydrogen as a fuel and feedstock in a decarbonized energy system. Though it’s logical from an infrastructure and economic perspective to retrofit current hydrogen facilities with carbon capture (blue hydrogen), it will likely be other clean hydrogen forms (including green hydrogen) that step in as widespread decarbonization tools. In this section, we first discuss why we think clean hydrogen will play an important role in a decarbonized US economy, and then assess its long-term benefits.

Making the case for clean hydrogen

Clean hydrogen has three main roles to fill in a decarbonized US energy system—1) energy storage and balancing, 2) as a feedstock, and 3) as a fuel. Other technologies can fulfill these roles, but the versatility and scalability of clean hydrogen make it a game-changer when it comes to systemic decarbonization.

Energy storage and balancing: Studies show a wind and solar dominated electricity system will prevail as a mechanism for economy-wide decarbonization. As the share of renewables on the grid continues to increase, hydrogen is one of the few technologies that can help balance the electricity system year-round. During times with high wind and solar supplies, excess renewable energy can produce green hydrogen for long-term energy storage. When renewable supplies are low, the stored hydrogen can provide a clean energy source to meet demand.

Hydrogen as a feedstock: Alongside energy storage and balancing, hydrogen can be used as a feedstock and fuel in other hard to abate sectors. Namely, hydrogen is a key feedstock needed to produce electrofuels—clean, electricity-derived, drop-in hydrocarbon fuels. In previous work, we’ve shown electrofuels are a subset of the clean transportation fuels necessary to achieve net-zero emissions by midcentury. In a low-carbon economy, clean hydrogen will also be an essential feedstock for major industrial processes, including the production of chemicals, iron, and steel.

Hydrogen as a fuel: As a fuel, hydrogen can be used in fuel cells in the transportation sector for medium to heavy-duty vehicles and shipping, which have limited decarbonization options. Hydrogen is also one of the few low-carbon ways to provide the high-temperature heat required for industrial processes such as cement and chemical manufacturing. When using hydrogen, the combustion process can produce nitrogen oxide pollutants (NOx). The impact of these pollutants on local communities needs to be factored into decision-making and evaluations of the environmental and climate trade-offs of decarbonization plans. Specifically, NOx pollution impacts can be mitigated with policy support and existing technological processes to control the amount of NOx produced.

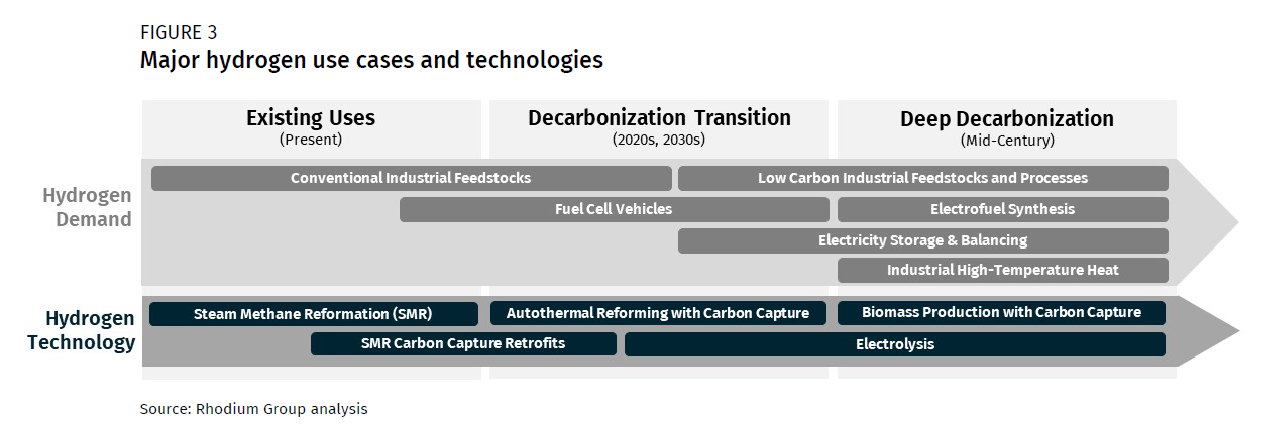

Across the energy system, hydrogen has a pivotal role to play. We’ve covered the big use-cases for hydrogen here and have summarize their roles over the next few decades as well as the timing of the current hydrogen technologies in Figure 3. Note there are many more places where this element can plug in to help solve the enormous challenge at hand. Depending on the emissions reduction path we head down, a recent decarbonization study showed that the US will need on the order of 56 to 133 MMt of clean hydrogen by mid-century—roughly 5 to 15 times the amount of current hydrogen production in the US.

The benefits of clean hydrogen in the long run

Scaling up US hydrogen production to meet the decarbonization challenge won’t be an easy feat. As we said previously, the central role for blue hydrogen will be in retrofitting existing hydrogen production facilities with carbon capture. From there, new blue hydrogen facilities that use autothermal reformation (ATR) with carbon capture will be useful until other forms of clean hydrogen are economic and at scale, as it can play the same role as feedstock or fuel. Green hydrogen is a group of technologies that use electricity to produce hydrogen from water via electrolysis. This use of electricity gives green hydrogen a unique advantage that enables its role in electricity storage and balancing in a decarbonized energy system, which is heavily dependent on a high-renewable electric grid. Additionally, green hydrogen has the potential to have one of the lowest carbon footprints out of the different types of hydrogen production (besides biomass production, which can be net-negative) assuming all the electricity used is from renewables, because there are no upstream methane considerations as there are with blue hydrogen. However, policy support is necessary to dramatically reduce the cost of green hydrogen.

Note that some express concerns that green hydrogen would be diverting renewable energy from the power sector. This is a small-scale and near-sighted concern that will ease in the long term when hydrogen is used as an electricity storage and balancing resource. Nevertheless, as the US decarbonizes, we will consistently face complex trade-offs involving near-term and long-term goals as well as temporary environmental and climate trade-offs. This is a challenge we face for all emerging decarbonization technologies and solutions, especially when it comes to emerging clean technologies like hydrogen. As mentioned previously, the current focus should be deployment of these technologies, irrespective of the application. The US will need to take risks and make compromises now to have the toolset necessary to decarbonize by mid-century.

Green hydrogen jobs

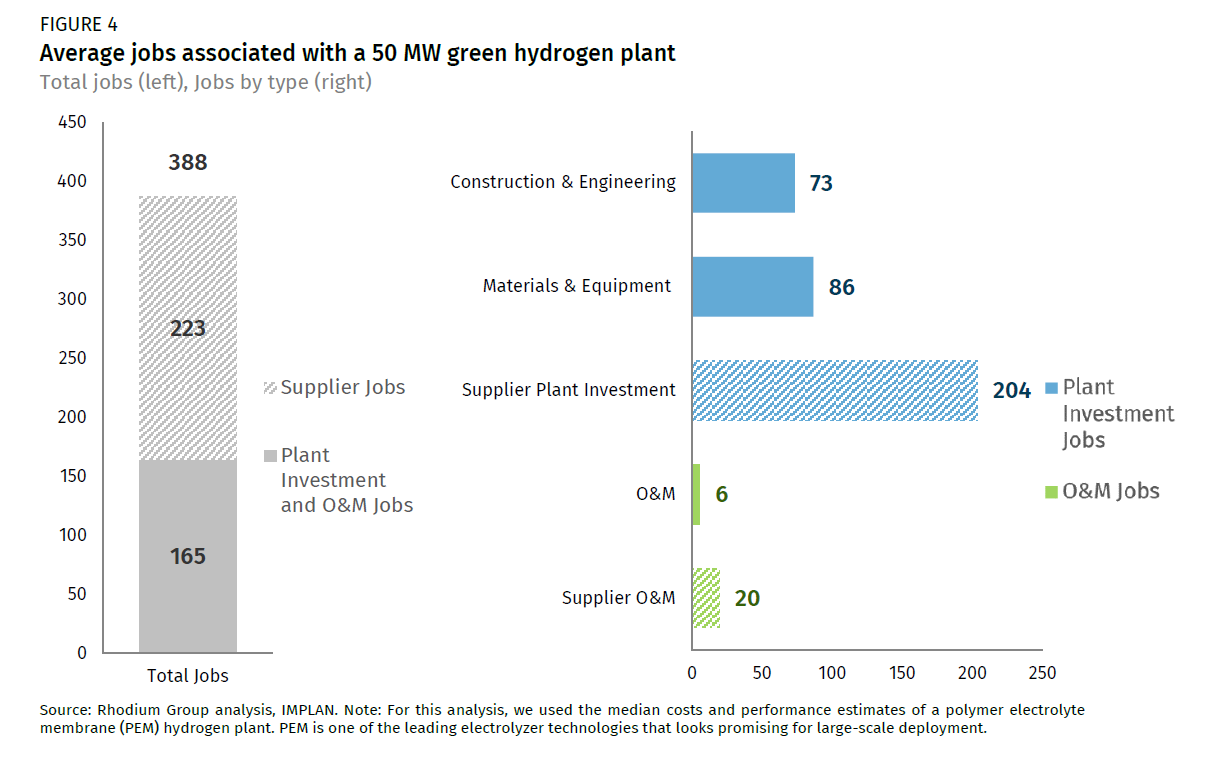

Like carbon capture retrofits, green hydrogen has significant economic benefits. We estimate that the average number of jobs associated with one 50 MW green hydrogen plant is 388 jobs (Figure 4, left). This total includes 223 jobs stemming from the supply chain required to build and operate the facility.

The bulk of these jobs, an average of 363, are associated with the plant investment, including the construction, engineering, materials, and equipment required to build the facility (Figure 4, right). Additionally, a 50 MW plant will result in an average of 26 ongoing jobs for operations and maintenance.

It’s important to note that a 50 MW electrolyzer facility is much smaller by nature than a carbon capture retrofit, as referenced above. This is a first-of-a-kind commercial-scale electrolyzer plant involving nascent technology. In contrast, the average blue hydrogen retrofit is based upon existing hydrogen facilities that are part of an already booming industry. For reference, the average blue hydrogen facility will produce about 100 times more kilograms of hydrogen per year than this illustrative 50 MW green hydrogen plant. This is another reason why it’s important to not pit the two technologies against each other, as they have very different production scales in the near to intermediate term. The long-term goal in the US is to scale green hydrogen facility sizes to gigawatt (GW) levels.

In terms of location, having multiple hydrogen facilities co-located, also known as hydrogen hubs, helps bring down the upfront capital costs by sharing infrastructure across projects. A coalition of stakeholders already announced plans to make Los Angeles the first green hydrogen hub in the US. In addition, the Gulf Coast is positioned to be one of the largest hydrogen hubs in the world. Due to the immense industrial activity in the region, the demand for hydrogen and corresponding transport infrastructure already exists. Additionally, Gulf Coast states, such as Texas, have high renewable energy resources to power the electrolyzer technology.

Policies for scaling up clean hydrogen

The world is in the early stages of the decarbonization race, with some countries making substantial investments to be leaders in the manufacturing and deployment of emerging clean technologies. Clean hydrogen is one of these technologies. There are no clear frontrunners on clean hydrogen just yet. Still, many countries, including China, EU member states, Japan, and South Korea, have announced generous investment commitments and ambitious deployment goals.

If the US wants to lead the world in clean hydrogen, policymakers should pursue new policies and enhancements to existing policies that address all stages of technology development, from lab-scale research to commercial deployment. This should include support tailored to all clean forms of hydrogen production. Policies that promote domestic manufacturing of clean hydrogen production and consumption equipment will also be needed.

Doubling down on RD&D

The bipartisan Energy Act of 2020, enacted at the end of last year, made major gains in clean hydrogen research, development, and demonstration (RD&D). The law folds clean hydrogen production and consumption into a variety of existing and new research initiatives, including nuclear energy, carbon management, clean manufacturing, energy storage, and transportation.

To build on this recent momentum, RD&D programs need continued funding through annual appropriations. The bipartisan Infrastructure Investment and Jobs Act, recently passed by the Senate and under consideration in the House, meets both of these objectives. If enacted, the bill establishes a new cross-cutting clean hydrogen RD&D program at the Department of Energy (DOE) as well as several other new programs. The bill also funds the Energy Act RD&D programs for multiple years. Additional policy efforts that focus on the next wave of clean hydrogen breakthroughs will also be needed as emerging leading technologies begin to scale.

Getting steel in the ground

Beyond RD&D, clean hydrogen technologies need to be deployed at scale quickly to drive down initial high costs, specifically for electrolyzer and biomass technologies. To do this, the federal government can support early-stage deployment through grant programs and other cost-shares. DOE is leading by example with its recently announced Hydrogen Earthshot goal, which aims to bring down the cost of clean hydrogen to $1/kg in the next decade. Furthermore, the Infrastructure Investment and Jobs Act creates a new regional hydrogen hub development program intended to support initial commercial-scale deployment of a variety of clean hydrogen technologies and use cases. The program will need annual funding if it is enacted.

Sector-based standards to scale up

A long-term policy framework for clean hydrogen scale-up will ultimately be needed to provide certainty as the technology matures and supply chains develop. Ideally, such a framework would be a comprehensive, technology-neutral federal climate policy that establishes a market for the most economically efficient decarbonization pathways to take off. It’s hard to say when the political landscape might foster such a policy. In the absence of comprehensive climate policy, sector-focused policies, targeted incentives, and actions that address non-cost barriers to deployment will enable commercial scale-up.

Sector-based policies can foster both investment in the supply of clean hydrogen and demand for it as a fuel and feedstock. For example, a technology-neutral federal clean fuels standard will drive demand for clean hydrogen at ports and heavy-duty transportation applications and catalyze new investments in production. A clean product standard will do the same in the industrial sector, where hydrogen can provide clean high-temperature heat and serve as a low-carbon product feedstock. Policies that incentivize electric power decarbonization will also spur demand for green hydrogen, specifically as an option for long-duration energy storage.

Kick-starting commercial deployment with tax incentives

Ambitious, sector-based policies may take time to get enacted into law. In the meantime, tax incentives actively under consideration in Congress can go a long way in kick-starting commercial deployment. Incentives can build on the foundation laid by federal RD&D programs and demonstration projects. Currently, the Clean Energy for America proposal in the Senate contains a clean hydrogen production tax credit that provides up to $3/kg to clean hydrogen producers that achieve a 95% reduction in lifecycle GHG emissions relative to gray hydrogen. A separate proposal to revive and revamp the section 48C tax credit that incentivizes domestic manufacturing of clean technologies (including clean hydrogen) is also under consideration. It’s important that these incentive structures are designed to address the unique barriers to deployment for all forms of hydrogen production.

Even with new policies that boost supply and demand for clean hydrogen, several non-cost barriers will constrain scale-up if not addressed. Congress and federal agencies need to set clear, common-sense siting and permitting rules for hydrogen infrastructure. Regulations may also be needed for the safe transportation, handling, and storage of hydrogen. Certifications for equipment that runs on hydrogen may also be required for consumers to have confidence in using it as a fuel. Fortunately, the Infrastructure Investment and Jobs Act deals with many of these issues. Additionally, clean hydrogen incentives are under discussion in the clean energy portion of the Democrats’ investment package in Congress now.

The US can lead the hydrogen economy

It is clear that clean hydrogen is an important technology that can help the US and the world decarbonize. What is not clear is what role the US will play, if any, in leading the world in clean hydrogen production. There is an array of clean hydrogen technologies at various stages of development that are ready for takeoff, each with its own challenges and trade-offs. If the US wants to be a leader in both clean hydrogen technology and in production, it can leverage recent investments in RD&D by enacting the Infrastructure Investment and Jobs Act as well as new deployment incentives for clean hydrogen production. These actions can go a long way in cementing US clean hydrogen leadership. More will be needed, but action this year could change the game for clean hydrogen in the years to come.

This nonpartisan, independent research was conducted with support from Breakthrough Energy. The results presented in this report reflect the views of the authors and not necessarily those of the supporting organization.