How Can China Boost Consumption?

China’s investment-led growth model has reached its limits and household consumption will be the key driver of China’s long-term economic trajectory. Beijing has reform options available, though they vary in financial and political viability.

China’s investment-led growth model has reached its limits, with diminishing returns on credit expansion and infrastructure spending. As this engine stalls, household consumption will be the key driver of China’s long-term economic trajectory. While Beijing has acknowledged the urgency of boosting domestic consumption, its policy response so far has fallen far short of the structural reforms needed to shift China’s economic model in a meaningful way. Beijing has reform options available, though they vary in financial and political viability:

- Meaningfully boosting consumption requires structural reforms to address the rural-urban divide, the precarious position of migrant workers, and the misallocation of capital by SOEs and banks. Many of these issues were recognized in China’s 2013 reform agenda but have remained largely unaddressed due to political and financial constraints.

- Substantial fiscal resources will be required. Tens of trillions of RMB (likely around 30% of China’s GDP) would be needed to fund both one-time investments—such as social infrastructure and financial stabilization measures—and ongoing expenditures to support social transfers and public services.

- A major fiscal overhaul is unavoidable, including tax reform, reallocation of government spending, and more central government borrowing. Crucially, local government incentives must also be realigned to ensure that new fiscal resources are directed toward social spending rather than investment-driven growth.

- While costly, these reforms are plausible. Beijing still has the space to raise fiscal deficits and tax revenues without destabilizing the economy. However, implementing these changes would be politically painful for entrenched interests and would shift costs to China’s urban middle class.

In the short term, Beijing may be willing to tolerate slow structural decay rather than risk disruptive reform—prioritizing stability at the cost of prolonged stagnation, rising financial pressure, and intensifying geopolitical tensions.

Finally appreciating the problem

Over the past six months, Chinese authorities have shifted policies more decisively toward supporting the economy. The government adjusted interest rates, hiked pay for civil servants, announced a RMB 10 trillion multi-year local government debt swap, and promised to expand subsidies for home appliances. Official policy rhetoric has also shifted to supporting “domestic consumption” rather than “domestic demand,” which used to include and implicitly prioritize investment over consumer spending.

Constraints on China’s household consumption growth are both demographic and structural, requiring structural solutions. These include redesigning the fiscal system to spend less on industrial production and investment and more on low-income households and other social service improvements. Last year, we detailed the constraints on household consumption and laid out our expectations for 3-4% real consumption growth as a baseline forecast over the next decade.

But what can Beijing actually do to change this outlook for low rates of household consumption? While there are many hypothetical policy options available, we attempted to narrow them based on the following criteria:

- Must meaningfully impact domestic economic imbalances between investment, exports, and household consumption.

- Must change existing patterns of fiscal revenue generation and spending, which are perpetuating industrial overcapacity and weak consumption growth.

- Must be reasonable within China’s current political constraints. Widespread privatizations of state-owned industries would probably be useful to promote domestic rebalancing, but are unlikely to be seriously considered in China’s political climate.

None of these measures are costless, and most will slow growth in the short term as the economy rebalances and investment activity weakens. But the limited measures Beijing has outlined and proposed so far aren’t enough to alter the structural decay in China’s fiscal system or the long-term slowdown in household consumption. Pay hikes for civil servants only help a limited number of households, and retail sales outside of subsidized sectors remain soft due to weaker income growth.

If Beijing opts to take more drastic measures to boost household consumption and mitigate deflationary pressures, it will need to do so in three categories:

- First, any meaningful reform must address weak purchasing power among the majority of China’s population who live in rural areas and poorer inland provinces. It will also need to reduce the need for precautionary savings among the 300 million migrant workers who still lack full access to urban public services. This requires a reinvigoration of “New Urbanization” policies, including hukou reform, land reform, and expanded public services.

- Second, these reforms will be costly and cannot be achieved without a substantial overhaul of China’s fiscal system to generate additional public revenues and realign local government incentives toward social spending. Potential fiscal solutions include tax reform, increased borrowing, SOE asset sales, and reallocation of existing spending away from investment-heavy projects.

- Finally, for consumption growth to be sustainable, China needs to reform its state-owned enterprises (SOEs) and financial system, which continue to channel wealth and credit into investment-heavy sectors at the expense of household incomes. Reforming SOE governance and dividend policies and financial sector distortions could help redirect resources to households.

Bolder “new urbanization” reforms

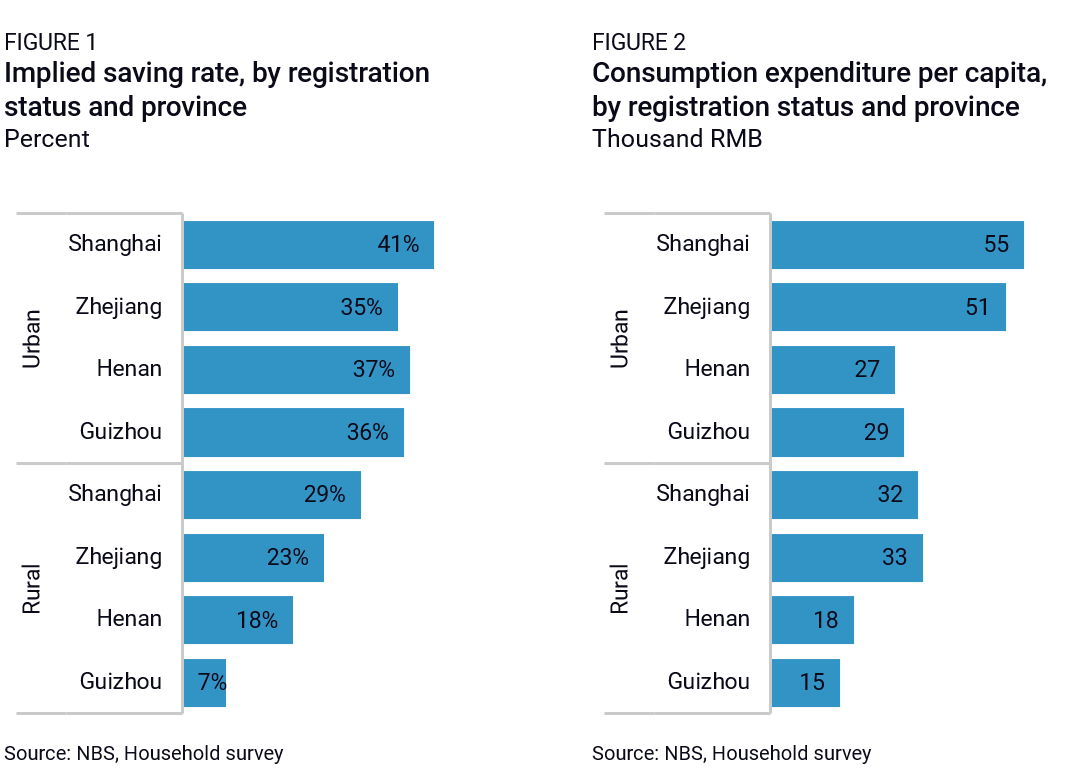

China’s population can be broadly categorized into three groups, with each group consuming less than their potential for different reasons. Urban households have higher incomes and a stronger social safety net, but they maintain high savings—in part due to the cost and cultural importance of homeownership. Migrant workers live and work in cities but lack full access to urban safety nets and public services, so they save nearly twice as much as urban households as a precaution against economic uncertainty. Rural households save a much smaller proportion of their income but still consume little, as their earnings remain significantly lower (Figure 1). Beyond these three categories, provincial disparities play a major role in shaping differences in both per capita income and consumption (Figure 2).

The most effective way for Beijing to stimulate domestic demand is to reduce the need for precautionary savings among migrant workers and boost incomes in rural areas and poorer provinces—reforms that fall under the decade-old but long-stalled New Urbanization agenda.

China’s 2014 New Urbanization Plan aimed to drive urbanization by easing hukou restrictions, reforming land rights, and expanding social security and pension systems. It primarily targeted smaller cities and skilled workers, with a goal of settling 100 million migrants into urban areas by 2020. However, progress has stalled and Beijing has fallen short of its ambitions. Among the ten reform areas outlined in China’s 2013 Third Plenum agenda and tracked in Rhodium Group’s China Dashboard, as of 2021, labor reform had regressed the most and land reform has barely progressed. Meanwhile, China’s migrant population has continued to grow, reaching nearly 300 million people by 2024—half of them in the economically developed eastern provinces.

The 2024 New Action Plan to Boost Urbanization made incremental adjustments, easing settlement restrictions in smaller cities while avoiding any substantive reform. A meaningful policy package to structurally enhance household consumption would likely center on three key measures: hukou liberalization to eliminate job discrimination and expand access to urban public services for migrant workers; land reform to boost rural wealth; and increased public spending on social welfare, particularly in rural areas and poorer inland provinces. All must operate in tandem to have a meaningful effect on household consumption growth.

Liberalizing the hukou system

The institutional divide created by the hukou system reduces migrant workers’ consumption. Administrative hurdles and outright restrictions tied to the hukou status prevent many migrant workers from accessing basic services such as mandatory education for their children and healthcare in cities where they actually reside. As a result, studies show that migrant workers save up to 70% of their income—double the savings rate of urban residents—as they prepare for uncertainties related to housing, healthcare, and education.

Granting full access to these basic urban services for all residents would significantly boost consumption, particularly among lower-income households with a higher marginal propensity to consume. A 2025 study found that after moving to cities, migrants’ per capita consumption increased by 30%, with an additional 30% increase when they are fully integrated into urban life. According to the National Bureau of Statistics, the average monthly income of migrant workers is RMB 4,961. If we assume that relaxing the hukou system would allow China’s 300 million migrant workers to reduce savings from 70% of their income to only 34% (the implied saving rate of urban residents), this could increase consumption by an additional RMB 6.4 trillion annually—equivalent to 13% of current household consumption in China.

Such reforms have gained traction again in the past year. Scholars such as Liu Shijin, Former Vice President of the Development Research Center, a think tank directly under the State Council, identified equalizing basic public services for the 300 million farmer-turned-workers moving to cities as key reforms needed to boost consumption.

However, the cost of expanding public services to this population is a key barrier. One early study estimated the cost of urbanizing one person in Hefei at RMB 154,900, amounting to around RMB 93 billion to accommodate the estimated 600,000 new migrants between 2012 and 2015—not counting existing migrants without access to basic services. A more recent study estimated the cost per migrant at RMB 50,000 to RMB 155,900—this would total between RMB 15 and 46 trillion to integrate all 300 million rural migrant workers in China. Other studies have estimated the financing demand for new urbanization from 2013 to 2020 overall to amount to around RMB 35 trillion.

Even the low-end estimate of RMB 15 trillion would represent a substantial fiscal challenge, equating to 12% of Chinese 2023 GDP and 43% of China’s total current fiscal expenditure (including both the general budget, which covers recurring expenses, and the government fund budget, which is allocated for infrastructure and utilities construction). The average age of migrants is also steadily increasing, which means that health and pension needs will only grow.

Implementing hukou reform gradually over several years would help, especially as the number of new migrants is now barely increasing. Such a transition would likely unfold gradually over several years, either by progressively lowering points-based residency requirements or by phasing out hukou-related restrictions on access to essential public services, particularly in education, healthcare, and social security.

An ambitious hukou reform would also require a profound transformation of China’s fiscal transfer system to ensure local governments have the resources to support newly integrated urban residents. The 2024 New Action Plan to Boost Urbanization has already taken a step in this direction by linking fiscal transfers to urbanization rates. But better allocation mechanisms and stronger fiscal transfers will be needed to ensure resources are available for the new urban population. Importantly, very little structural reform can happen without fundamental changes to China’s fiscal system.

Land reforms

Land reform was launched in 2014, but has largely stalled over the past decade. China’s land ownership system divides urban land, which is state-owned, from rural land, which is collectively owned by villages. Local governments control land allocation and frequently expropriate rural land and sell it, primarily for industrial use. This has led to an oversupply of industrial land, a restricted supply of commercial and residential land, and suppressed income growth for the rural population. By expanding government revenue and widening the urban-rural income gap, these distortions shift resources away from households. Additionally, prioritizing land for industrial development has increased the ratio of gross capital formation to GDP, further crowding out household incomes.

The 2014 “Three Rights Separation” system separated agricultural land ownership, contract, and management rights. This allowed various pilot reforms but fell short of delivering meaningful changes, in large part because of the reluctance of local governments that depend on land sales revenues to function. The Rural Collective Economic Organizations Law, which takes effect in May 2025, will theoretically increase farmers’ participation in land sales development decisions, but local government actors remain the central decision makers of rural land trades.

Meaningful market-oriented land reforms could have a significant impact on household consumption. Studies estimate the market value of homestead conversion around RMB 4.4 trillion each year. Securing property rights could increase the disposable income of rural residents by 34% and reduce the disposable income ratio of urban and rural residents from 2.4:1 to 1.8:1. More efficient, market-driven land supply would further support consumption: A recent study has observed a 1.4% decline in final consumption for every unit increase in the share of industrial land supply.

The greatest constraint on reform is local governments’ ongoing reliance on land sales for revenues. Shifting control over land transactions would direct more of the economic benefits to rural landowners, at the local governments’ expense. Currently, local governments capture most of the appreciation of land value, making land sales a critical funding source—RMB 4.9 trillion in 2024, or 22% of China’s total general public budget revenue in 2023, down from 38% in 2021. Even if only part of these revenues were redirected away from local governments, the short-term fiscal shock would be significant. These revenues primarily belong to the “government fund budget,” which is separate from the general expenditure budget and largely allocated to local infrastructure investment. Reducing infrastructure spending could support economic rebalancing by curbing excessive investment in unproductive projects, but it would come at the cost of slower economic growth and job losses in the short term.

Boosting public spending on rural social welfare

In the medium term, land reforms that benefit China’s 477 million rural residents could just lead to higher rural savings unless they are paired with substantial improvements in rural social welfare. In 2023, rural residents had an implied savings rate of just 13.7%, compared to 33.8% for urban residents—likely because they have far less income to save. Given the severe shortfalls in public services and social safety nets in rural areas, any increase in rural income would likely be set aside as precautionary savings to guard against future uncertainties, rather than spent on consumption.

Generally speaking, Chinese households already bear a disproportionate share of basic service costs. In 2021, out-of-pocket healthcare spending accounted for 35% of total health expenditures in China, compared to just 13% in OECD countries. Similarly, households spent an average of 7.9% of their annual expenditures on education, far exceeding the 1–2% seen in Japan, Mexico, and the US.

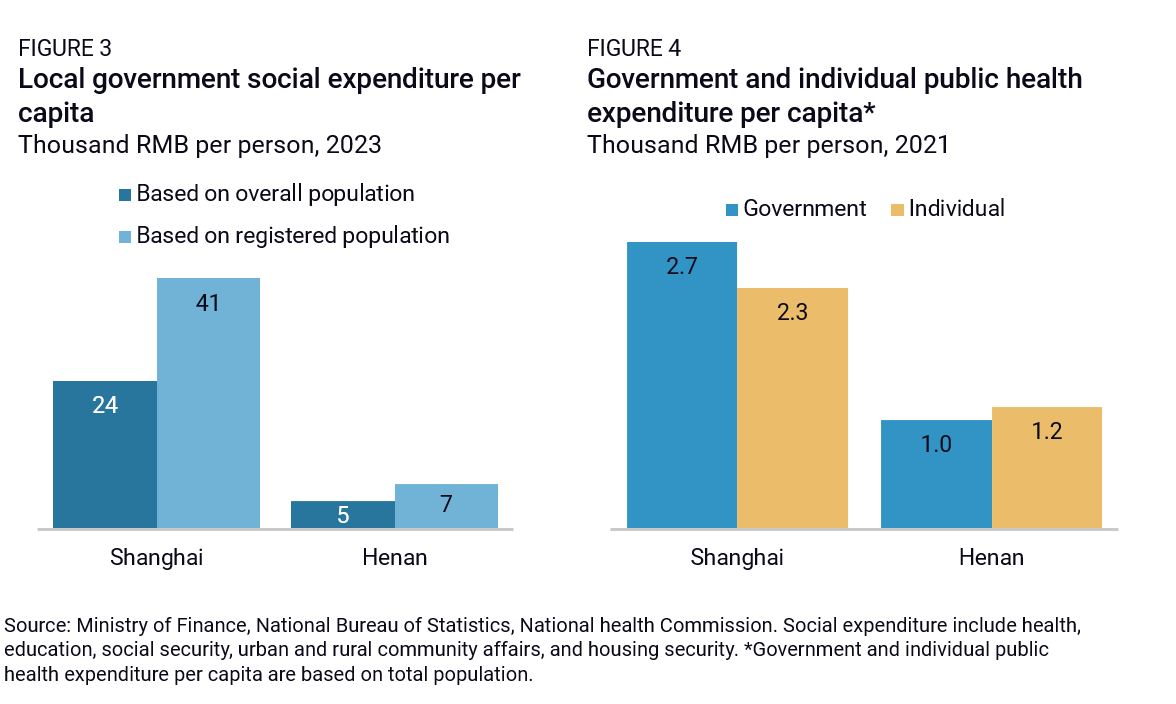

However, these figures mask significant regional disparities. In 2023, per capita social spending by local governments in Shanghai was RMB 24,328—or RMB 41,118 when considering only registered residents with full access to public services—compared to just RMB 9,249 in Henan (Figure 3). The gap is also evident in healthcare funding: In 2021 in Shanghai, government contributions per capita exceeded individual contributions by 20%, while in Henan, they fell short by 10% (Figure 4).

Just as with hukou liberalization and land reforms, the cost of fully equalizing access appears prohibitively high. For example, raising Henan’s per capita public social spending to just half of Shanghai’s level would require the province to more than double its current spending, increasing its total fiscal expenditures by 70%. Scaling this across all rural inland provinces would place an unsustainable strain on local government budgets.

However, while fully equalizing access is financially unfeasible in the near term, gradual but substantial increases over the next decade could still meaningfully boost household consumption. Existing studies show a strong correlation between public social spending and household consumption, particularly in economies where consumption as a share of GDP is low and savings rates are high. A 2010 IMF study estimated that a sustained 1% of GDP increase in public social expenditures, distributed equally across education, healthcare, and pensions, could permanently raise China’s household consumption ratio by 1.25 percentage points of GDP.

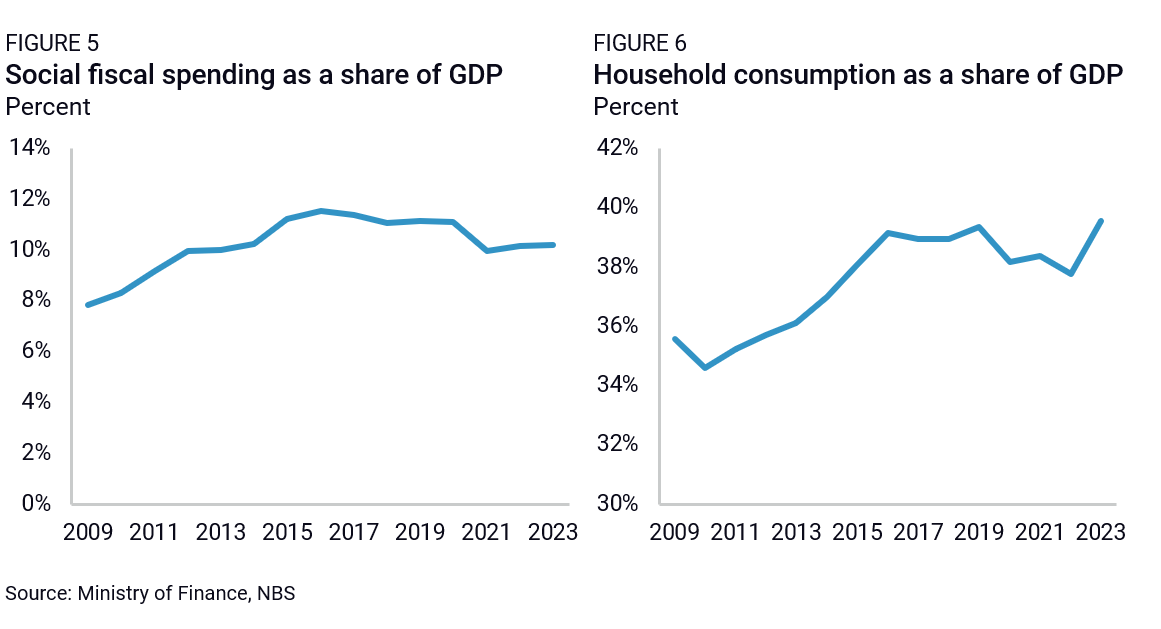

Since the publication of this study, China’s public social expenditure as a share of GDP has increased by 2 percentage points, while household consumption as a share of GDP has risen by 5 percentage points. But both indicators stagnated or declined after 2016 (Figure 5 and 6).

Applying the IMF’s estimates to bring China’s household consumption-to-GDP ratio in line with South Korea’s 49% would require an 8 percentage point increase in public social spending as a share of GDP. This would mean an additional RMB 11 trillion in public social spending, assuming 2023 GDP levels, effectively raising China’s current public budget by nearly 40%—a high, but not unachievable short-term goal if significant fiscal reforms are put in place.

Fiscal reforms

All three reforms outlined above—hukou liberalization, land reform, and the expansion of rural social welfare—would require substantial increases in fiscal spending. However, two major obstacles stand in the way of boosting public social expenditures in China. The first challenge is securing adequate funding amid slowing economic growth, particularly given mounting debt pressures. The second challenge is local government implementation, as competing incentives and priorities often dilute policy objectives. Addressing both challenges would require a fundamental overhaul of China’s fiscal system to create fiscal space while changing the incentives for local officials.

Creating fiscal space

To create additional fiscal space for consumption spending, Beijing needs either more fiscal firepower or a fundamental reallocation of expenditures, shifting resources away from traditional investment projects and toward social welfare and household support.

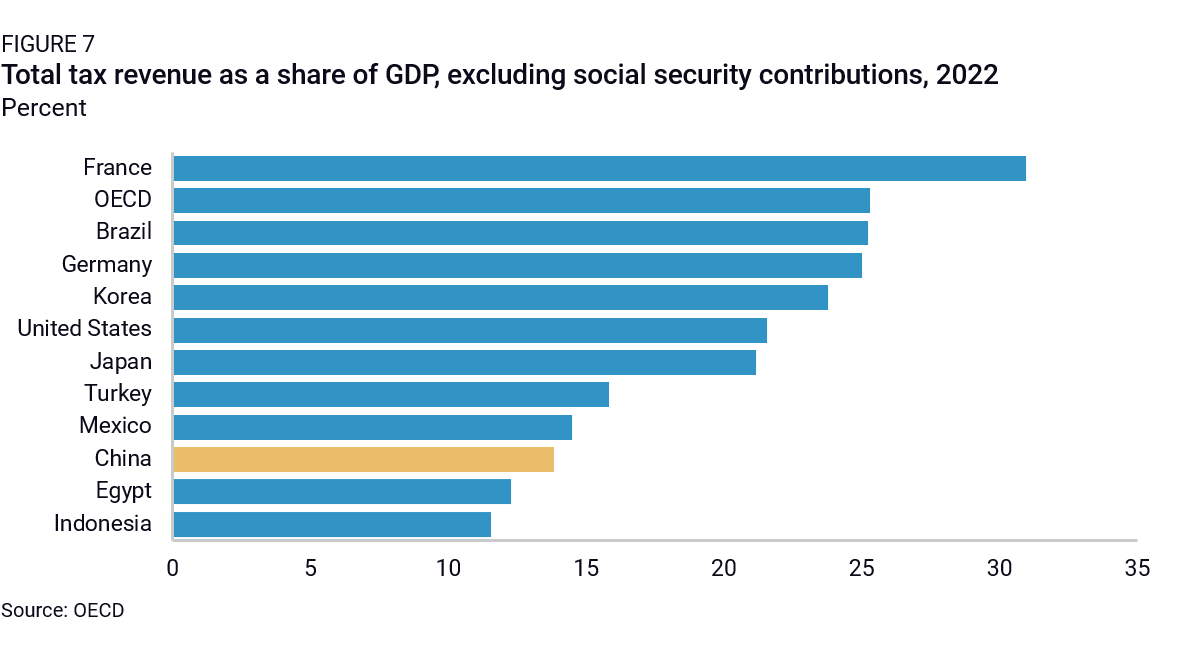

Generating more tax revenue is challenging, given the slower economic growth. However, China is currently an outlier in tax collection. In 2022, China’s tax-to-GDP ratio stood at just 14%, the second-lowest among major economies—compared to 18% in G20 countries and 23% in G7 economies (Figure 7). One major discrepancy lies in individual income tax collection, which remains exceptionally low by international standards, at just over 1% of GDP. The share of the individual income tax in total tax revenues was only 8% in 2023 in China, compared with 24% in 2021 in OECD countries.

This suggests untapped fiscal potential that could be unlocked with feasible tax reforms. The IMF has outlined several potential measures that could increase China’s tax-to-GDP ratio by 5–6 percentage points over five years, with roughly half of the additional revenue benefiting local governments. These measures include:

- Individual income tax reform, including higher average rates combined with lower social security contributions and greater taxes on capital income

- Value-added tax optimization to reduce distortions and administrative costs

- Property tax implementation and reducing subsidies to owner-occupied housing

However, in the absence of faster economic growth, the burden of these reforms would fall disproportionately on the urban upper-middle class—a demographic that is already experiencing economic strain and rising dissatisfaction, and which is arguably a key pillar of political legitimacy for the regime. The political cost of such reforms would therefore be very high. In addition, as the IMF acknowledges in the “authorities’ views” section of the 2023 Article IV report, China has already pushed back against reforms to increase overall revenues.

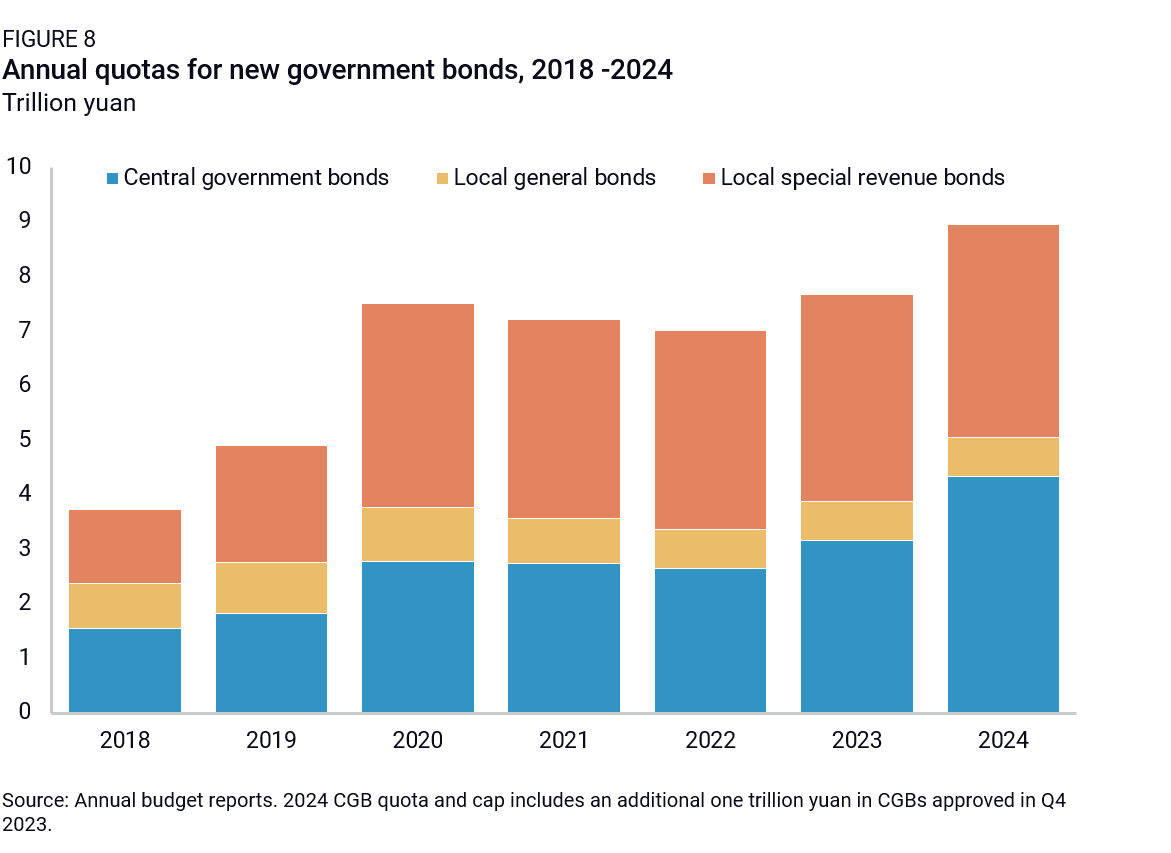

An alternative approach is to increase borrowing. Beijing has already signaled its intent to do so. In late 2023, the government announced the extraordinary issuance of RMB 1 trillion in special treasury bonds, with RMB 150 billion earmarked for consumer subsidies. Special treasury bonds, an instrument only rarely used before by Beijing, are expected to increase to RMB 3 trillion in 2025. Of that three trillion yuan, one trillion yuan will be used for one time capital injection for large state owned banks while the other two trillion yuan will fund infrastructure projects and expanded consumer subsidies. In addition, Beijing is reportedly likely to raise the ceiling on the issuance of local government special revenue bonds (SRBs) to RMB 4.7 trillion in 2025, up from 3.9 trillion in 2024.

While these announcements suggest a substantial increase in the formal fiscal deficit, they fall short of what would be required to meaningfully expand fiscal social expenditures (Figure 8). A more ambitious version of this strategy comes from Liu Shijin, who proposed issuing RMB 10 trillion in special treasury bonds over time to finance new urbanization initiatives.

Issuing additional local government bonds also raises concerns given China’s already high local government debt burden. Most of the additional funding will likely be used to restructure old local government debt, rather than for public social spending. Here again, Beijing has already taken some action—in 2024, it announced a RMB 10 trillion local swap bond program over five years to reduce local governments’ debt burden and free up room for additional spending. But those bond swaps are not nearly enough to resolve local governments’ debt problems and pivot local priorities back to spending. Local government financing vehicles’ (LGFVs) interest bearing debt alone is easily in the range of 50-60 trillion yuan, not to mention money borrowed through SOEs and affiliated government institutions like schools and hospitals which could total another 20-30 trillion yuan. Also, debt swaps do not remove the debt burden from local governments, as they only reduce annual interest payments. Ultimately, while Beijing still has fiscal space to increase central government borrowing, the constraints are mainly political as Beijing historically preferred to put the burden on local governments’ shoulders. A significant increase in central government borrowing, though not impossible, would constitute a sharp departure from previous trends.

Another way to generate fiscal resources is through the sale of SOE assets. Total reported SOE-controlled net assets reached 131 trillion RMB in 2023, or around 101% of GDP, and even a small fraction of these holdings could provide substantial fiscal firepower. While Beijing made some efforts in this direction during Xi’s second term, tangible results were minimal. Instead, momentum reversed as state capital expanded within the private sector, rather than SOEs divesting stakes to private investors to raise funds. Over the past year, there have been renewed attempts to sell state assets, but these have largely been aimed at repaying local debt rather than financing new spending. The main constraint here, once again, is political. Beijing has so far been unwilling to loosen its grip over key state assets or challenge the powerful vested interests that control SOEs.

Lastly, without securing additional fiscal resources, Beijing could reallocate existing expenditures to consumption-driven spending instead of infrastructure investment. This would involve redirecting a greater share of bond proceeds toward social welfare programs rather than capital-intensive projects. Currently, Beijing borrows approximately RMB 8 trillion annually through central and local government bonds. Half of this amount is allocated to general obligation (GO) spending, while the other half is issued by local governments as SRBs, whose proceeds fund infrastructure and utilities. Repayments come from revenues generated by those projects.

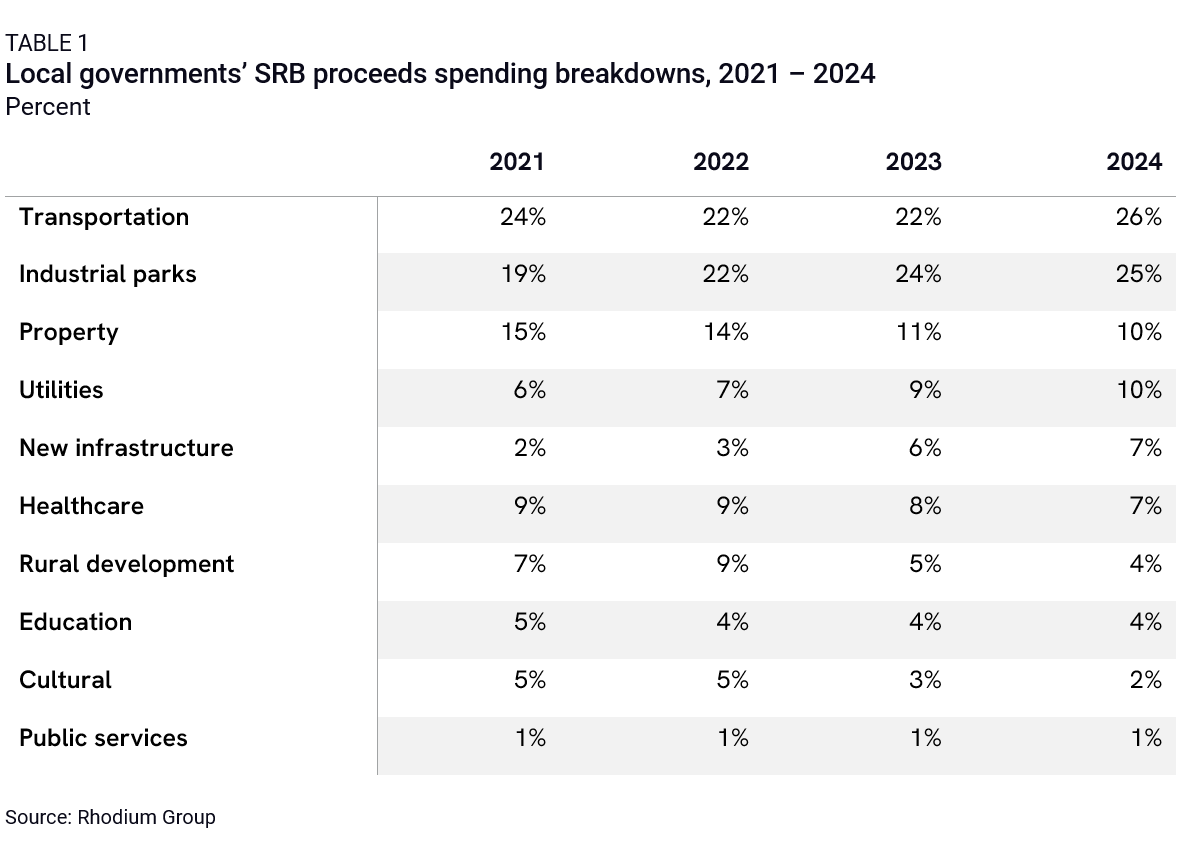

A recent Rhodium Group survey examining SRB-funded projects in eight provinces found that the majority of these bonds are allocated to transportation infrastructure and industrial parks. Meanwhile, spending on healthcare and other welfare infrastructure has declined as a proportion of total bond proceeds (Table 1). Shifting the spending structure to allocate more funding to social welfare coverage—such as healthcare, education, and public services—could significantly boost consumption growth by reducing household precautionary savings and increasing disposable income. Ultimately, SRBs only fund infrastructure and utilities development and cannot be used for recurring welfare programs. Shifting the issuance of SRBs to GOs that could be used for social spending would go a long way in reallocating budget to boost consumption. The downside is that they would raise the fiscal deficit ratio because GOs count towards fiscal deficit while SRBs do not. Although not impossible, that would be a break from past policy where Beijing tried to hold the line at a 3% of GDP fiscal deficit.

Changing local government incentives

The second major challenge in rebalancing the economy is implementation at the local level. Even if local governments receive additional fiscal resources, they are unlikely to prioritize social welfare spending unless they have a direct financial incentive to do so. This creates a fundamental disconnect: Beijing wants local governments to promote consumption, but the current system does not reward them for doing so.

A range of institutional factors reinforce these misaligned incentives—including the revolving door between government officials and SOE executives, informal power structures, and the administrative framework that shapes local decision-making. One approach to address this misalignment would be making consumption growth an important KPI for local officials. However, a more effective solution might be to ensure local governments benefit financially from consumption-driven growth, rather than solely from production-driven growth.

Consumption tax reform

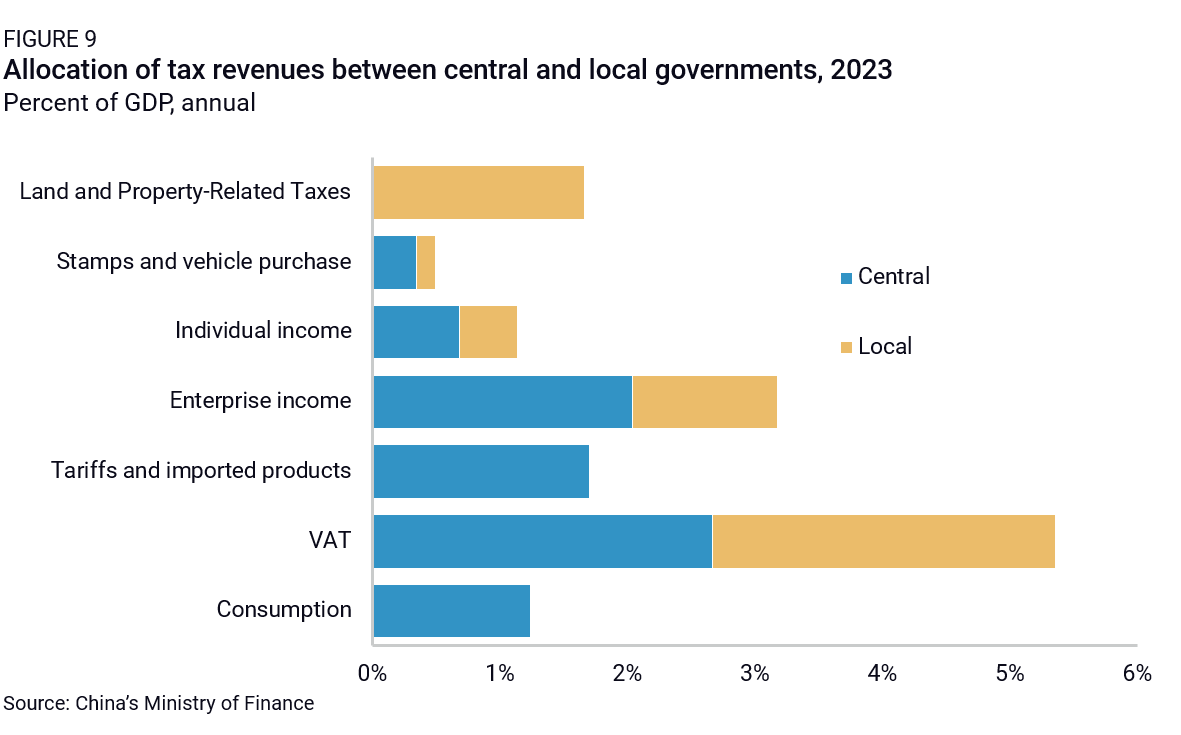

The main issue with China’s consumption tax is that all revenues go to the central government, leaving no incentive for local governments to support consumption-driven growth (Figure 9). While China’s consumption tax accounts for about 9% of total tax revenues—similar to the OECD average of 8%—its base is extremely narrow, covering fewer than 20 consumer goods. Four products—tobacco, alcohol, autos, and fuel—account for 98% of total consumption tax revenues. A meaningful reform would be to broaden the tax base to include more consumer goods and services while shifting part of the revenue to local governments. This would give local governments a direct fiscal stake in increasing household consumption, creating an incentive to develop service-oriented industries rather than just manufacturing and infrastructure.

VAT reform

China’s value-added tax (VAT) revenues are significantly higher than OECD countries’ (38% of total tax revenues in 2023, compared to 21% in the OECD in 2021). However, the current revenue-sharing mechanism favors production over consumption: VAT revenues are split 50-50 between the central government and local governments, but local governments collect revenue based on where goods are produced, not where they are consumed. This means local governments have a strong incentive to promote production rather than consumption-driven sectors. Given the importance of VAT in local revenues, shifting the VAT revenue distribution toward consumption-based collection could significantly reduce the bias toward production-driven policies, and could reduce China’s industrial overcapacity in several industries.

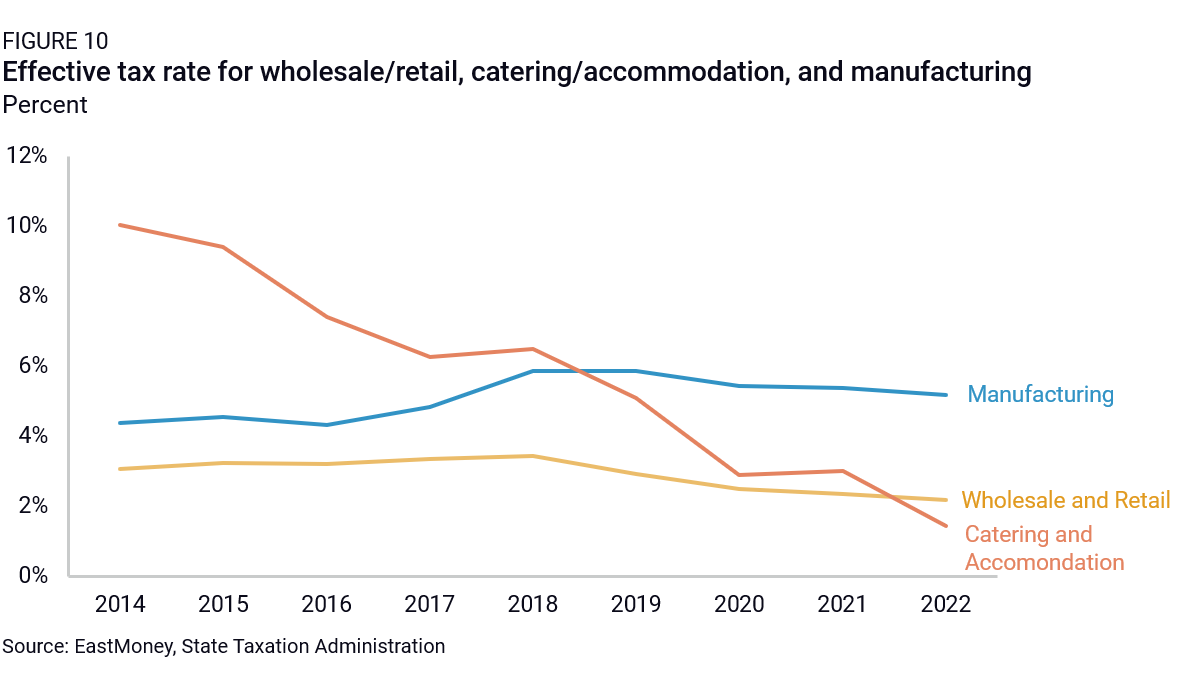

The VAT also has sectoral imbalances. Currently, the manufacturing sector faces much higher VAT rates than consumption-related industries: The catering sector has an effective tax rate of only 2%, and the wholesale and retail sectors also benefit from lower rates (Figure 10). Tax breaks for small businesses and the expansion of digital payments have further reduced VAT contributions from services, reinforcing local governments’ preference for supporting manufacturing and industrial activity over service sectors that drive consumption.

China could adjust the VAT system to tax luxury goods and services more heavily while reducing VAT on most manufacturing products. This would make the tax system more progressive, while realigning local government incentives and making consumption growth a more attractive policy objective. There are trade-offs involved, of course, because as consumption expands, aggregate tax collection and the tax base need to expand as well, even though this may discourage consumption in some sectors.

These changes would not be easy to implement. The primary political challenge is that higher consumption taxes and VAT adjustments would primarily benefit lower- and middle-income households while increasing the tax burden on the upper-middle class and wealthier individuals—a demographic that is crucial to Beijing’s political support. A less politically sensitive reform would be to change the VAT revenue-sharing system so that revenues are allocated based on where goods are consumed rather than where they are produced, giving local governments a direct incentive to support consumption growth. However, this would require a major overhaul of China’s fiscal system, making it bureaucratically complex and difficult to implement in the near term.

SOEs and bank reform

A final, and even more structural, set of reforms needed to boost consumption involves overhauling China’s SOEs and financial system, both of which fundamentally skew the allocation of wealth and credit toward industry and investment instead of households. Despite years of discussion on reform, SOE dominance in the economy has only expanded, concentrating economic power within the state sector and reinforcing investment-driven growth while limiting resources available for household income and consumption. Similarly, China’s financial system perpetuates domestic imbalances by prioritizing lending to state entities and local governments over private enterprises and consumers, further constraining disposable income growth.

To sustainably rebalance the economy toward consumption, household participation in SOE wealth would need to increase through broader shareholding and dividend redistribution. The financial system would also need to shift credit allocation away from inefficient local government borrowing and toward private enterprise and households.

SOE reform

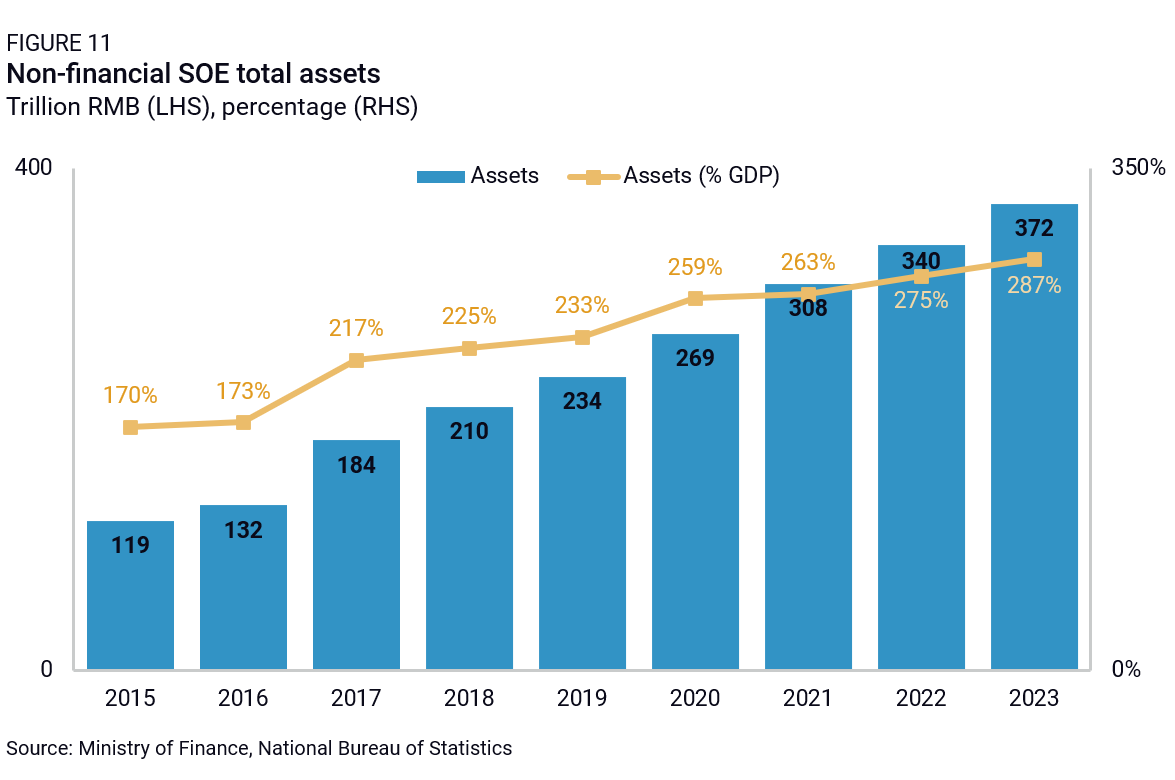

Under Xi Jinping, the role of SOEs in China’s economy has expanded steadily. In 2023, they accounted for 65% of market capitalization of the top ten firms across industries, up from 51% in 2021. Total assets controlled by SOEs more than doubled, rising from RMB 184 trillion in 2017 to RMB 372 trillion in 2023 (Figure 11). China now has the largest public sector of any major economy: In terms of output, Chinese SOEs alone now account for 4-5% of global GDP.

Ideally, the wealth accumulated by large public enterprises would filter down to households—after all, SOEs are nominally owned by the public. In most economies, this happens through shareholding mechanisms (allowing households to benefit from SOE valuations) or profit remittances to the government, which are then used to fund social transfers. While full-scale privatization of China’s SOEs is not a viable option, as SOEs remain central to the CCP’s economic control, there are still meaningful reforms that could strengthen both of these redistribution mechanisms.

The first mechanism—increasing shareholding of listed SOEs—has stalled since the SOE privatization campaign in 1996-2007 (“grasping the large, letting go of the small”), leaving the state still in control of nearly 80% of major non-financial SOEs. Increasing external shareholding may not be a silver bullet for boosting consumption because, as in Europe, and unlike in the United States, Chinese households have low stock market participation and hold a relatively small share of their wealth in financial assets. However, scholars have proposed innovative ways to increase broader household participation in SOEs. For example, Xu Gao proposed a “universal shareholding scheme for SOE stocks” that would pool SOE equity into state-owned investment funds and distributes these fund shares equally among all citizens. Citizens would then convert their shares between different funds after a holding period and collect dividends or sell their equity.

Beyond wealth redistribution, this approach could also enhance market discipline within SOEs. Currently, the public sector produces the lowest return on assets of any enterprise type in China, and has significantly lower total factor productivity and lower profit margins than private firms. This weak performance reduces the taxable base available to the central government and results in excessive capital being funneled into inefficient industrial investments, crowding out consumption. Under the proposed shareholding reform, investment funds would compete for public favor based on their performance and dividend policies, creating pressure on SOEs to improve efficiency and returns. This would help redirect capital toward more productive uses, reinforcing both household wealth accumulation and broader economic rebalancing.

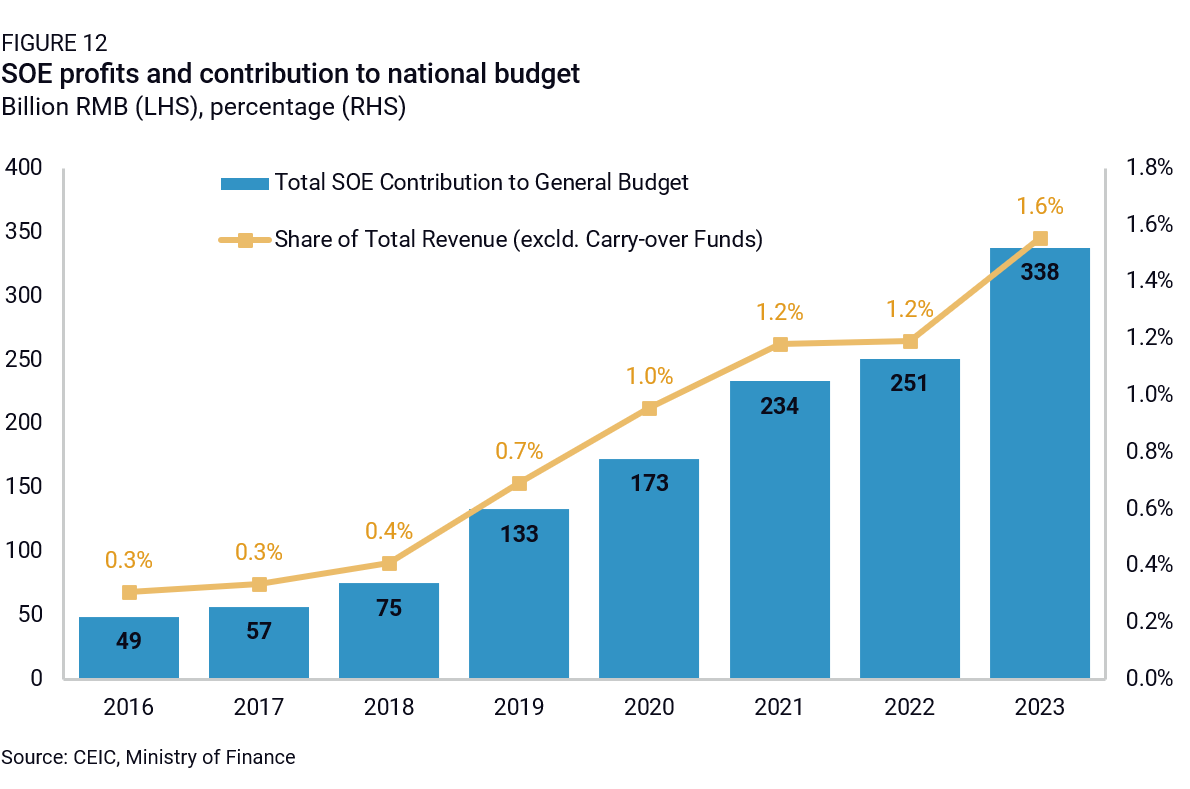

A reform of the SOE dividend policy would be another way to boost social transfers and support consumption. China’s SOEs have long been required to remit profits to the central budget at rates far below global norms, and have consequently constrained the potential size of social transfers that could otherwise be allocated to citizens. Although a plan was announced at the 2013 Third Plenum to increase dividends to up to 30%, SOEs has largely fallen short of that bar. Profit remittances still comprise a small share of national budget revenues, though they have been relative increases in recent years (Figure 12). Even where remittances have increased, they often do not go to social transfers. In 2019, approximately 70% of dividend payments were subsequently sent back to SOEs to be reinvested, and only 2.4% of central SOE profits contributed to social program funding in China’s general budget. Upping dividend payments would potentially add hundreds of billions of RMB in new available spending that could be directed toward household transfers.

Bank reform

Beyond the inefficiencies and wealth concentration within SOEs, China’s financial system itself perpetuates the country’s domestic imbalances by channeling resources to the state sector at the expense of China’s more dynamic private sector and households. These biases are long-entrenched, based on a system that prioritizes lending on the basis of state guarantees and the availability of collateral. The fact that such a large proportion of China’s lending since the global financial crisis has been to local governments and their related companies extends these problems: Lending on commercial terms to companies building public infrastructure means that very few loans can be serviced out of project cash flows. As a result, banks are required to continuously roll over and extend these loans to local governments and SOEs at the expense of lending to more productive and dynamic sectors of the economy.

The logical step to change these practices would be to write off the bad loans, stop lending to unproductive local governments, and create a different set of incentives for banks to lend on the basis of market signals and market-based interest rates. The problem for China is that isolating the non-performing loans themselves is far from straightforward, since the loans are technically to state-owned firms and continue to perform, once rolled over. Local governments are unlikely to disclose non-performing loans to Beijing unless it promises to take the bad loans onto its own balance sheet, which may increase the associated costs of recapitalization. This kind of restructuring would not necessarily eliminate the government guarantees that enabled the previous patterns of lending, so the same problem could regenerate even after a recapitalization of the banks. Ultimately, unless local government companies can publicly default—which would spark a wave of panic throughout China’s financial system—it would be difficult to prevent another wave of inefficient lending even after recapitalization.

China’s banking system comprises $60 trillion in assets as of the end of 2024 and is around 30-40 times the size of the banking system that was restructured in the early 2000s. Recapitalizing the system on its own would involve tens of trillions of yuan in direct fiscal costs, and contemplating some of the same tradeoffs between saving the banks and increasing spending on public goods and services. Even if loans could be effectively separated from “good banks” and placed into “bad banks,” Beijing would still need to provide funding to the “bad banks” to remove the assets from the rest of the financial system and restructure the remaining debt. Even the benefits of doing this would be uncertain, as banks may still face pressures to lend to local governments and their related companies after any banking system restructuring, unless there is considerable loan demand from private firms and consumers. Credit growth within a Chinese economy where government guarantees are weaker would likely be far lower as well, slowing investment growth and the overall economy.

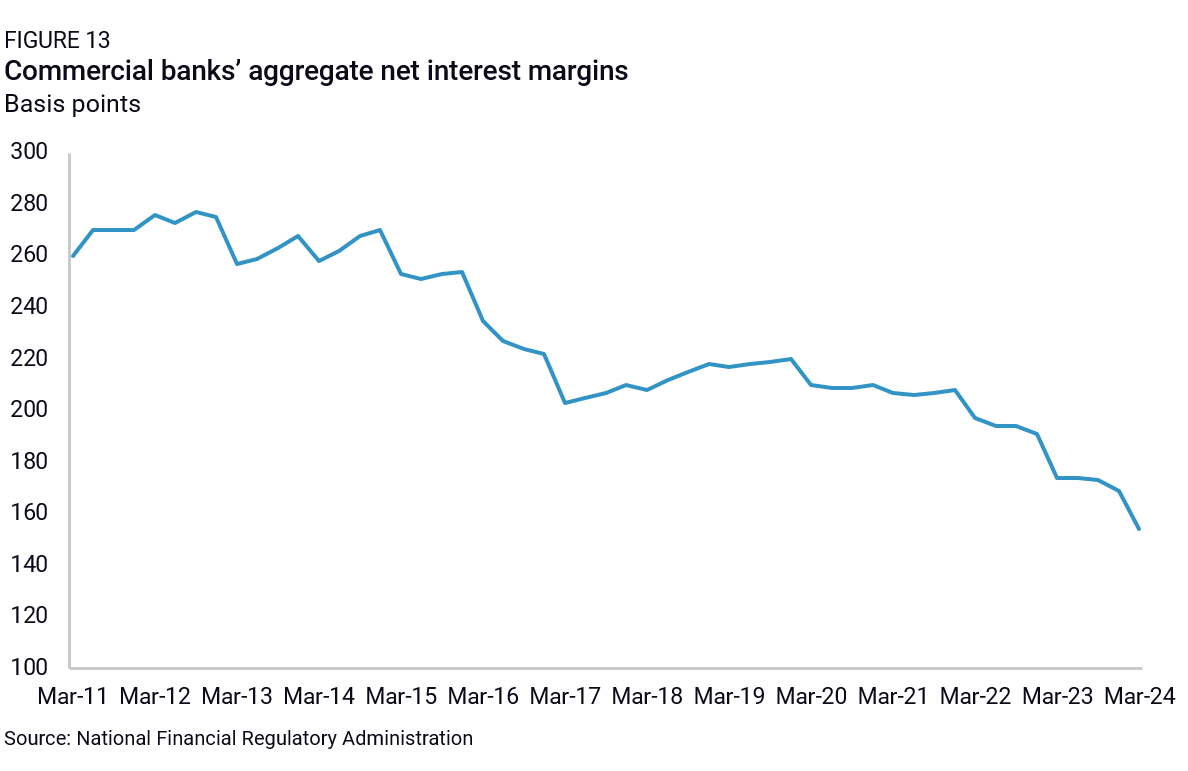

Banks already face considerable financial pressure to maintain credit growth as their profit on every new loan continues to decline (Figure 13), with net interest margins for banks almost cut in half over the past decade. The decline in profits will continue as interest rates need to move lower to counter deflationary pressures in the economy.

Restructuring the financial system is a necessary condition for rebalancing the economy away from investment and toward household consumption, but it needs to be paired with changes to state and local government guarantees that would continue to channel credit to less productive uses. And there are few political benefits to undertaking a restructuring with high reputational and fiscal costs, with few concrete benefits for credit efficiency.

All of these arguments partially explain Beijing’s inaction in cleaning up the banking system so far: there are few good options available that would allow China’s economy to maintain a reasonable pace of investment growth. But the other explanation for China’s inaction is the systemic risks that can be created by reforming the system. China’s banking system may be inefficient, but there are few threats to its broader stability. Those threats arise from actually recognizing some assets as potentially risky without the funds to remove them from the banks’ balance sheets at their current values—bailing them out. Any attempt to shift to government-directed “bail-ins” among depositors or investors in the banks as part of a restructuring could lead to a broader panic among depositors, withdrawing funds from the banks and generating a liquidity crisis. China’s financial system is most vulnerable at the point of reform, not from ongoing inefficiency. And that creates a powerful incentive not to reform the banking system.

Conclusion and net assessment

China’s economic model faces mounting structural challenges. The reforms outlined here are deeply interconnected, meaning that no single policy can work in isolation. New Urbanization cannot succeed without fiscal reform, as expanding social services and integrating migrant workers into urban areas requires sustainable funding. Land reform, while unlocking rural wealth, risks being counterproductive without a stronger safety net to prevent newly liquidated assets from simply increasing precautionary savings. Bank reform, meanwhile, would be fiscally expensive, requiring new revenue sources to manage bad debt and stabilize the financial system. Even if China creates more fiscal space, meaningful change will not happen unless local government incentives are realigned to prioritize social spending over investment-driven growth, which may also require removing implicit guarantees from local government companies.

Overall, implementing these reforms would be extraordinarily costly, requiring tens of trillions of RMB (probably at least 30% of GDP) in one-time costs as well as an ongoing rise in fiscal expenditures. Some of this spending would be one-time investments in public services and infrastructure, but much would need to be recurring to sustain long-term improvements in social welfare. This makes structural fiscal reform the foundation of any meaningful shift in China’s growth model or the rebalancing of China’s economy toward household consumption—without it, no other policy can be effective.

While politically difficult, fiscal reforms are not impossible. China still has room to increase tax revenues, as its tax-to-GDP ratio lags behind OECD peers. The central government has fiscal space to borrow more, and SOE asset sales remain a viable—if politically contentious—option for raising funds. The primary barriers are political and ideological, rather than purely economic. They require facing the decay in the current system head-on.

The final category of reforms—SOE and financial sector restructuring—is the most structural and arguably the most politically difficult for Beijing. SOEs and banks play a crucial role in China’s political economy, and years of misallocated capital have created deep path dependencies that stymie change. However, without reform in this area, China’s financial system will continue to misallocate capital, reinforcing the country’s reliance on unproductive investment rather than household consumption.

Ultimately, the longer these reforms are delayed, the more costly they become. As economic growth slows and capital misallocation worsens, China’s fiscal constraints will only tighten. At the same time, the clear limits of Beijing’s investment- and export-driven model—particularly amid rising global trade tensions—are making reform increasingly urgent.

The pressures pushing for reform are strengthening, because the costs of inaction are multiplying. But inaction is always an attractive option, as decay is a slow process. It creates comfort among leadership who are not seeing urgent requests for change until they venture out of Beijing and see the reality of local fiscal crises on the ground, as Xi Jinping reportedly discovered in Gansu last September. Change will come to China’s decaying fiscal system one way or the other—it will either break at the local government level or the leadership will finally try to rebuild it completely rather than patching it up around the edges.