Intellectual Property Rights and Global Direct Air Capture Scale-Up

We conduct a comparative study of DAC against two previous energy innovations, hydraulic fracturing and solar photovoltaics, to assess similarities and differences in the centrality of IP in the global dissemination of the technology.

Over the past sixty years, multiple major economies have played complementary roles in supporting clean technologies to reach their commercial deployment stages. Achieving the necessary US domestic manufacturing prospects for direct air capture (DAC) to contribute to mid-century decarbonization will depend similarly on commercial demonstration and deployment across other countries that can help drive significant cost reductions in concert over time. As a result, members of the cleantech community have begun discussions around how critical intellectual property (IP) and efforts to protect it can impact the global scale-up of DAC technology.

Using a combination of literature reviews, industry interviews, and data from the US Patent & Trademark Office, we conduct a comparative study of DAC against two previous energy innovations, hydraulic fracturing and solar photovoltaics (solar PV), to assess similarities and differences in the centrality of IP in the global dissemination of the technology. While balancing IP rights protection and sharing specialized knowledge with equitable technology transfer is essential, enabling policy and supportive infrastructure will likely be more critical factors in scaling up the DAC industry in the US and abroad to levels necessary for achieving domestic and international mid-century decarbonization targets.

DAC is a necessary tool for global decarbonization

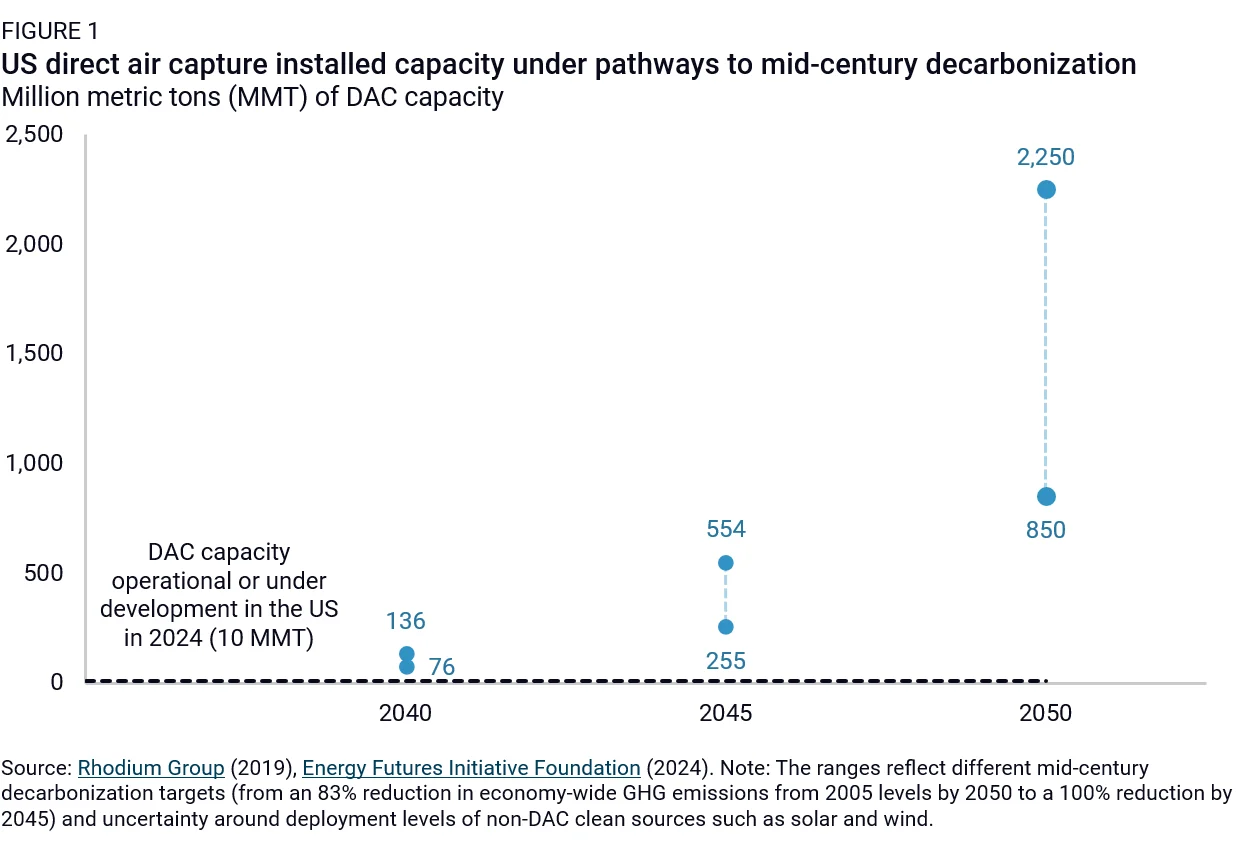

According to the latest climate modeling from the Intergovernmental Panel on Climate Change, all scenarios limiting global temperature rise from pre-industrial levels to 2° or lower by the end of the century will require significant deployment of carbon dioxide removal (CDR) solutions in conjunction with a range of mitigation measures. CDR approaches generally fall into three classifications: natural, hybrid, and engineered. Direct air capture (DAC) is the furthest along in technological maturity of the different engineered CDR solutions. It works by extracting carbon dioxide (CO2) directly from ambient air. Industrialists can then use the captured CO2 to create new products such as synthetic fuels and building materials, for enhanced oil recovery activities, and they can store it permanently in deep underground geological formations. Previous Rhodium Group analysis found that achieving midcentury decarbonization in the US would require gigaton-scale DAC deployment by 2050, far higher than the 10 million metric tons of capacity currently operational or under development (Figure 1).

However, achieving this level of deployment by 2050 will require significant improvements in DAC’s economic viability through cost reductions, learning-by-doing, and by deploying DAC at scale both in the US and globally. Achieving gigaton-level deployment will also depend on developing unique insights around a product or market gained through practice distinct from knowledge known more broadly in a particular industry. Though DAC has made rapid progress in the US through bipartisan policy support and growing private sector investment, there is the risk that overprotection of intellectual property (IP) could serve as a barrier to achieving the requisite level of scaling and deployment abroad for DAC to contribute meaningfully to global decarbonization.

In this note, we first explore the debate around how intellectual property rights protection (IPRP) can both positively and negatively impact technology scale-up. We follow with case study assessments of IP centrality and specialized knowledge for two long-standing energy innovations—solar photovoltaics and hydraulic fracturing—and whether IP rights protection and the need for specialized knowledge are central factors in the global dissemination of these technologies, relative to other factors such as the presence of supportive policy and infrastructure. We then survey DAC’s current state of progress and empirically analyze patent trends across DAC technology developers. Last, we explore similarities and differences in IP centrality and specialized knowledge needs across DAC and other energy technologies to draw inferences about the role they could play in the global scale-up of DAC technologies.

Effects of IP rights protection on technology scale-up

IP broadly refers to intangible but legally protected creations of human ingenuity that hold underlying financial value. The primary types of IP rights include copyrights, trademarks, patents, industrial designs, and trade secrets. Copyrights and trademarks primarily encourage the protection of creative work and enable informed consumer choice, while patents and trade secrets protect technology innovation, design, and creation. The latter two, consequently, serve as the basis for our assessment of how IPRP and the need for specialized knowledge can impact global DAC scalability. Patents offer limited-time rights “to exclude others from” commercial activity around an invention or an industrial design. A trade secret refers to information indefinitely holding economic value when kept private. Specialized knowledge encompasses in-depth knowledge of products, processes, and equipment, which arise uniquely through experience and practical application.

The legal protection of IP rights incentivizes investment in technological research and development (R&D) by reducing the financial risk of supporting early-stage technologies. IPRP also helps foster a broader culture of entrepreneurship and innovation. The interactions of IP rights with the wider global IP system they reside in play an essential role in determining whether technologies developed in one geographic region can be deployed at scale across others.

IPRP and the global IP regime can positively impact the scaling of different technologies like DAC to other countries beyond the US. For instance, the World Trade Organization’s Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS) sets global minimum standards for IP rights protection that all member countries must comply with. These standards lower the risk that one country may infringe upon IP rights protected in another, creating a more favorable environment for patent holders to license their technology abroad. Licensing is one such mechanism by which technology transfer occurs broadly in countries outside the US. A company holding a US-based patent can license its technology to companies abroad and obtain royalty fees to finance their product, allowing foreign companies to build on and deploy the technology locally and collectively drive down costs over time.

IPRP also signals companies and investors that they can trust licensing and technology transfer to companies abroad, knowing that their invention will be safe from piracy and misuse. In such cases, IP rights are a legal deterrent for other companies wanting to enter a nascent market. As a result, IPRP can encourage the creation of international joint ventures with local partners in new countries for R&D and manufacturing, primarily when favorable industrial policy incentives exist.

Other features of the IP system also encourage global market diffusion. When applying for patent protection, for example, parties can file a single common patent application under the World Intellectual Property Organization’s (WIPO) Patent Cooperation Treaty (PCT), which simultaneously enacts a national application for a patent to each signatory of the treaty. This process allows firms to concurrently begin obtaining a patent in multiple countries, which will later enable them to move more easily into new markets and scale technologies in new regions. The Patent Law Treaty (PLT) also has similar intentions in streamlining patent application procedures. For companies seeking US-based patents, the patent process also requires public documentation of any invention via the US Patent & Trademark Office (USPTO), which adds to the shared knowledge pool and allows inventors worldwide to build on existing knowledge.

IPRP can also, however, serve as a barrier to scaling technologies outside of the US. Some firms strategically aim to stifle competition by developing patent thickets, a system of overlapping patents pursued by companies to preserve the market exclusivity of their technologies. In addition to inhibiting further innovation, such strategies increase costs and legal risks for new market entrants. Barriers to entry arising from IPRP can also exist in other ways. For instance, US-based patent holders sometimes demand royalty payments that are prohibitively expensive for companies abroad that are hoping to obtain licenses.

Though infrequently, global IP signatories have sometimes allowed emergency waivers of TRIPS protections, such as for COVID-19 vaccine patents in 2021. This waiver enabled countries such as India and South Africa to manufacture these vaccines at scale without needing express approval from US patent holders, allowing the innovation to scale across international borders. While measures like these reflect some degree of flexibility, they are temporary solutions, more so than permanent, default structures within the IP system that are necessary for sustained global technology scale-up. As such, critics of the international IP regime have often argued that the system has slowed the diffusion of clean energy technologies and bolstered monopolies held by large corporations. Economic research indicates that, at times, too-strong IP rights protection can even discourage innovation.

IP centrality and the advancement of previous energy innovations

While we know IPRP and industrial policy will likely impact the ability of DAC technologies to scale up globally over the next several years, it is unclear whether these factors will have more of an enabling or limiting effect. We find insight in surveying previous energy technology innovations and exploring whether IPRP and specialized knowledge proved to be driving factors in the deployment outcomes of these technologies in the US and abroad. We focus on solar photovoltaics (solar PV) and hydraulic fracturing, two very different energy technologies initially developed in the US.

For energy technologies, we believe that the three leading factors that matter most for scaling across borders are public policy, infrastructure support, and IPRP. For each comparative technology, we assess the centrality of these three factors. We explore the extent to which policy helped scale the technology, followed by a similar analysis of infrastructural support, and examine the effects of IPRP on the technology’s diffusion worldwide.

Solar PV

Some energy technologies, such as solar PV, are deployed globally without IPRP playing a significant role in either direction, owing to successful public policy support and the availability of critical infrastructure. While some countries saw slower solar PV deployment domestically due to their strong IPRP, enough scale-up occurred collectively over time to yield sufficient cost learning for solar PV.

In the 1950s, Bell Laboratories developed the first solar cells in the US, for the purpose of powering telephone systems. Two decades later, the US government began its first significant investment into solar PV R&D as a means of spurring early deployment. The US continued its extensive policy support for solar PV, including the Block Buy procurement program. By the 1980s, after the beginning of the Reagan administration, solar PV engineers found that other countries were offering more substantial support for the technology and, subsequently, left for more supportive prospects.

Japan had, meanwhile, been focusing on its own R&D commitment since the 1950s. There, producers took advantage of small-scale applications to help push solar PV forward. After progress slowed, the government delivered substantial policy support for larger-scale systems, creating a successful rooftop solar program in 1994. Over time, however, high labor costs and a preference for next-generation solar technologies limited Japan’s potential to further scale solar PV.

As a result, Germany then took the stage as the primary site of solar PV innovation, expanding policy support through the Electricity Feed-In Act of 1991 and the Renewable Energy Law (EEG) in 2000, attracting investment and attaining cost reductions through significant learning-by-doing. The EEG introduced feed-in tariffs that increased investment, and the government simultaneously held successful competitive auctions. Solar PV developers also worked towards building turnkey systems, allowing developers to meet increased demand more quickly.

After the German feed-in tariff expired, China rose to the challenge of meeting growing German and global demand, massively scaling up their commercial solar production. They engaged in a number of key measures, building up the necessary supporting finance and labor capacity, developing logistics infrastructure, and enacting new policies to further solar PV deployment. These policies included, for instance, their own feed-in tariff in 2011.

Further, necessary supporting infrastructure allowed grids worldwide to integrate variable renewable energy and support solar PV as it settled into early commercial-scale deployment. Countries like Germany, for instance, used small distributed systems to install capacity widely and load balance effectively through reliance on ancillary services markets.

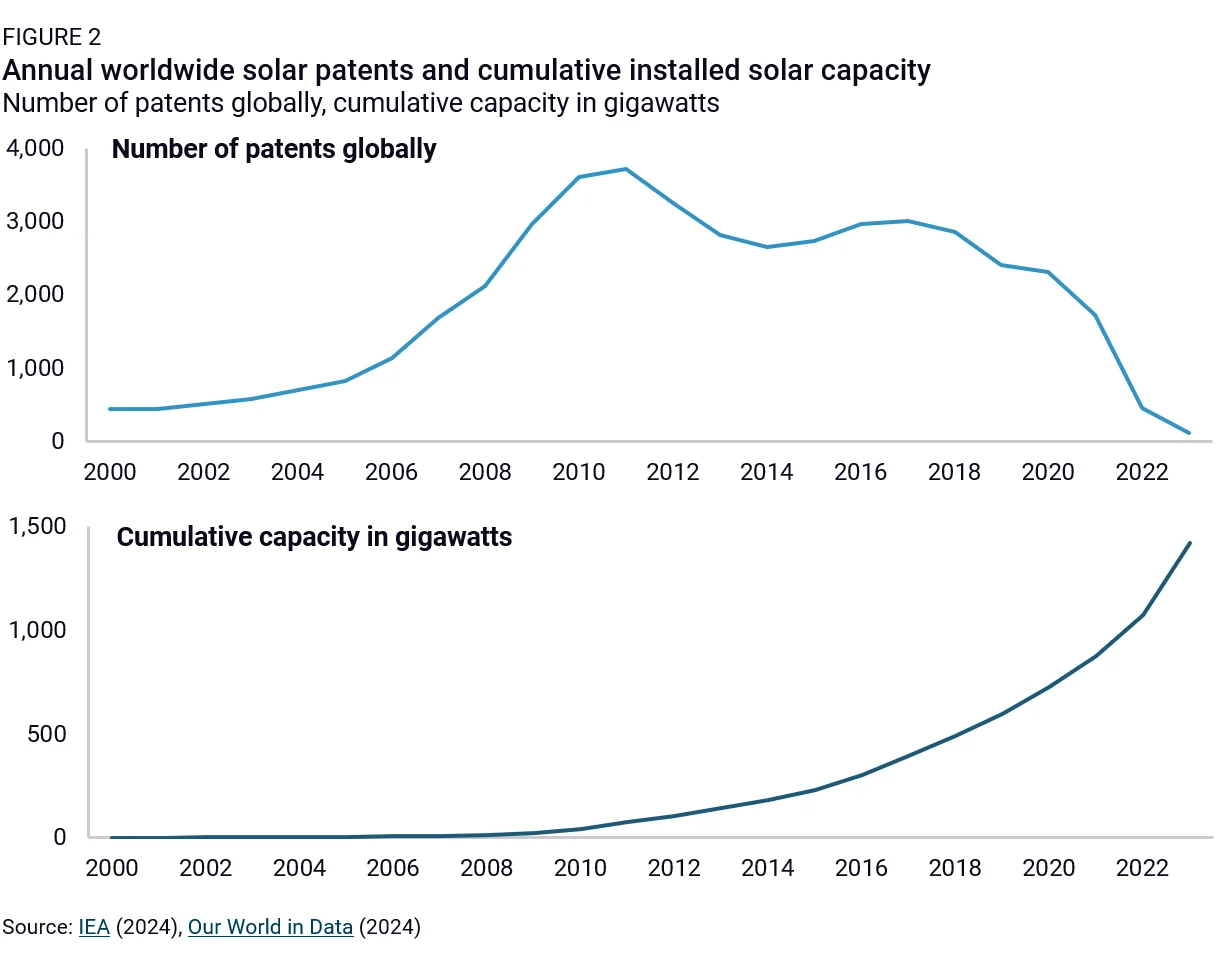

While there is some indication that strong IPRP for solar PV may have slowed its scaling in many non-Organization for Economic Co-operation and Development (OECD) countries, on an overall global basis, solar PV was still able to attain the necessary deployment levels in enough countries to benefit from learning-by-doing and reduce costs over time. Historical data on patents for all solar technologies, as a proxy for IPRP, are mostly well-organized only post-2000.1 Still, a comparison of annual global patenting activity and cumulative deployment of all solar technologies broadly over that period shows that sizable increases in cumulative capacity occurred during periods of both high and low patenting activity (Figure 2). This indicates that IPRP seemed not to significantly limit large-scale solar PV deployment, likely due to its firm policy and infrastructure support, suggesting that the latter two factors were likely more central in shaping the trajectory of global solar PV capacity.

Other innovation-focused IP rights besides patents do not apply heavily to solar PV, as competitors can generally reverse-engineer them. Solar PV also does not face prohibitive trade secrets or require specialized knowledge.

Hydraulic fracturing

Though IPRP was not a significant barrier to the global deployment of solar PV, it has significantly limited widespread adoption outside of the US for other technologies like hydraulic fracturing. Unlike solar PV, which enjoys commercial-stage deployment across many countries, large-scale hydraulic fracturing has not spread widely outside the US, primarily occurring only in Canada, China, and Argentina. Even in those countries, hydraulic fracturing has emerged more slowly than in the US. Though not zero-emitting, hydraulic fracturing remains instructive as a corollary in our discussion of DAC scale-up, as one of only a few major energy technologies that have not found much commercial success abroad. While policy environments and underdeveloped infrastructure outside the US have served as barriers, IPRP has also significantly contributed to that outcome.

Hydraulic fracturing has enjoyed deep public policy support within the US. However, in other countries, supportive policy either exists but varies in the extent to which it has enabled scale-up, or it does not exist. The few non-US countries where hydraulic fracturing has been deployed have seen broader policy issues. Argentina, for example, has a large shale resource base, but deployment has been slower than expected due to broader macroeconomic challenges that have made project financing more difficult. Governments have banned hydraulic fracturing in many European countries due to environmental concerns, and deployment has not taken off.

In contrast, public policy support has been much more meaningful in the US. Public-private R&D partnerships were especially significant in helping hydraulic fracturing achieve commercial success; in the 1970s, the US began investing significant R&D into hydraulic fracturing and related technologies. Federal appropriations helped fund key programs, research, and policies, such as the Eastern Gas Shales Project, a public-private research initiative funded by the US Department of Energy (DOE) that conducted field experiments to evaluate shale gas recovery from hydraulic fracturing. Another example is the Section 29 production tax credit that supported unconventional natural gas production from 1980 through 2002. In 2005, Congress passed the Energy Policy Act of 2005, which explicitly exempted most types of hydraulic fracturing from the US Environmental Protection Agency (EPA) regulation under the Clean Water Act and the Safe Drinking Water Act.

This government support also helped incentivize the private sector to invest in R&D and commercialization activities. Other US policy incentives have included federal oil and gas subsidies, minimal regulatory oversight, and ease of financing. Moreover, in the US, property owners can lease underground mineral rights to oil and gas drilling companies. However, mineral rights outside the US belong to the government (even in countries with large shale resource bases, such as Argentina, which has seen only moderate deployment).

Differences in infrastructure (and associated economic dynamics) also played a significant role in advancing hydraulic fracturing within the US. The industry benefited from extensive pre-existing oil and gas pipelines and resources close to pipelines and terminals. Though countries like China have a resource base similar to the US, they have been slower in developing infrastructure for gas distribution. As a result of lower commodity prices, US supply is high, and American exporters have readily sold those abroad, making unconventional drilling investment beyond the US less attractive. Hydraulic fracturing also uses significant amounts of water. Hence, its availability is another major infrastructural issue: many countries outside the US have unconventional oil and gas resources in regions where water is scarce.

Unlike solar PV, the need for specialized knowledge has significantly limited the scale-up of hydraulic fracturing abroad. Scientists and engineers in the US developed hydraulic fracturing techniques over almost a century. The country then accelerated progress through directional drilling and digital tools for seismic interpretation, with key companies developing a significant amount of easily accessible technical expertise. The long lead time for development concentrated much of that knowledge within the US. Transferring the knowledge to a shale formation in a different country is also complicated and not directly applicable. This is because the knowledge necessary for hydraulic fracturing is very specialized, as techniques are more regionally specific due to the unique challenges of different shale formations. Moreover, transferring results from lab experimentation to actual well sites is challenging because lab conditions, such as high temperature and pressure, cannot replicate the high levels that engineering companies encounter in the field.

Current progress on DAC policy and infrastructure

While there may be the potential for IP rights and the need for specialized knowledge to act as limits on the scale-up of DAC globally, interviews with major DAC developers have reflected that policy support and availability of infrastructure are far more central concerns to the industry than aiming to protect IP vigorously (or the requirement of specialized knowledge). Developing policy and other types of public support, such as large-scale CDR procurement by the government, is particularly important because CDR is a pure public good, where the benefits of removing CO2 accrue to any citizen without limiting its benefits to anyone else. Because of this, the government must create end markets to establish demand artificially.2

The US currently has a supportive policy environment for DAC. For instance, at the federal level, the bipartisan Infrastructure Investment and Jobs Act (IIJA) provided $3.5 billion to build out four DAC hubs as well as $4.6 billion in total to develop geologic storage wells and CO2 pipelines. IIJA additionally extended $115 million in funding for DAC prize competitions. The Inflation Reduction Act (IRA) also modified and expanded the Section 45Q tax credit for CO2 sequestration, offering up to $180 per captured ton of CO2 for DAC. A recent Rhodium Group analysis determined that the US has enacted significant support for DAC by ramping annual federal appropriations for research, development, demonstration, and deployment. There have also been a multitude of complementary measures at the state level. Given all these incentives, between 2021 and 2025, the US saw an increase of more than 500% in the planned capture capacity of announced DAC plants.3

By comparison, the policy environment for DAC outside the US has shown more moderate progress. Countries in Asia have limited support. In China, for instance, while the national government has enacted action plans and guidance for carbon management and DAC technologies, there has been limited concrete policy support for DAC or other forms of CDR broadly at the national level. Some policy progress has been made in India, including ongoing efforts to develop more detailed policies.

Non-US OECD countries have had comparatively more support, though they can enact further support to catch up to the US. For instance, the United Kingdom (UK) announced over $100 million in R&D funding for DAC technology development and a Contracts for Difference scheme supporting CDR technologies. Canada proposed an investment tax credit covering qualifying DAC projects. At the same time, the European Commission put forward R&D programs for DAC and adopted an EU-wide monitoring and verification framework for CDR and carbon storage. The EU Innovation Fund also provides funding for CDR through competitive auctions, while Australia started the Carbon Capture Technologies Program, which supports demonstration activities for DAC.

The EU, Norway, and the UK have also implemented clear permitting rules for storage sites. They require a thorough analysis of new storage sites around their ability to store CO2 before the sites can receive permits permanently, and they mandate storage site operators to monitor them consistently. Other policy support mechanisms do not have specific carve-outs for DAC yet, but the government will likely adapt to support it. For instance, in 2026, the European Commission will likely issue greater clarity around the ability of the EU Emissions Trading System to integrate DAC and other forms of CDR.

The US has begun investing in the necessary infrastructure for DAC, though far more progress must occur to support commercial-scale deployment in the next decade adequately. Though the Class VI well permitting program has existed since 2010, the federal framework has evolved. Thus far, EPA has granted four states Class VI primacy for geological storage—West Virginia, North Dakota, Wyoming, and Louisiana. This authorizes these states to permit and regulate Class VI wells more quickly, which project developers use to sequester CO2 deep underground permanently. According to the medium estimate from the National Energy Technology Laboratory’s NATCARB Atlas, the US has a total saline storage capacity of approximately 8.3 trillion metric tons of CO2.4

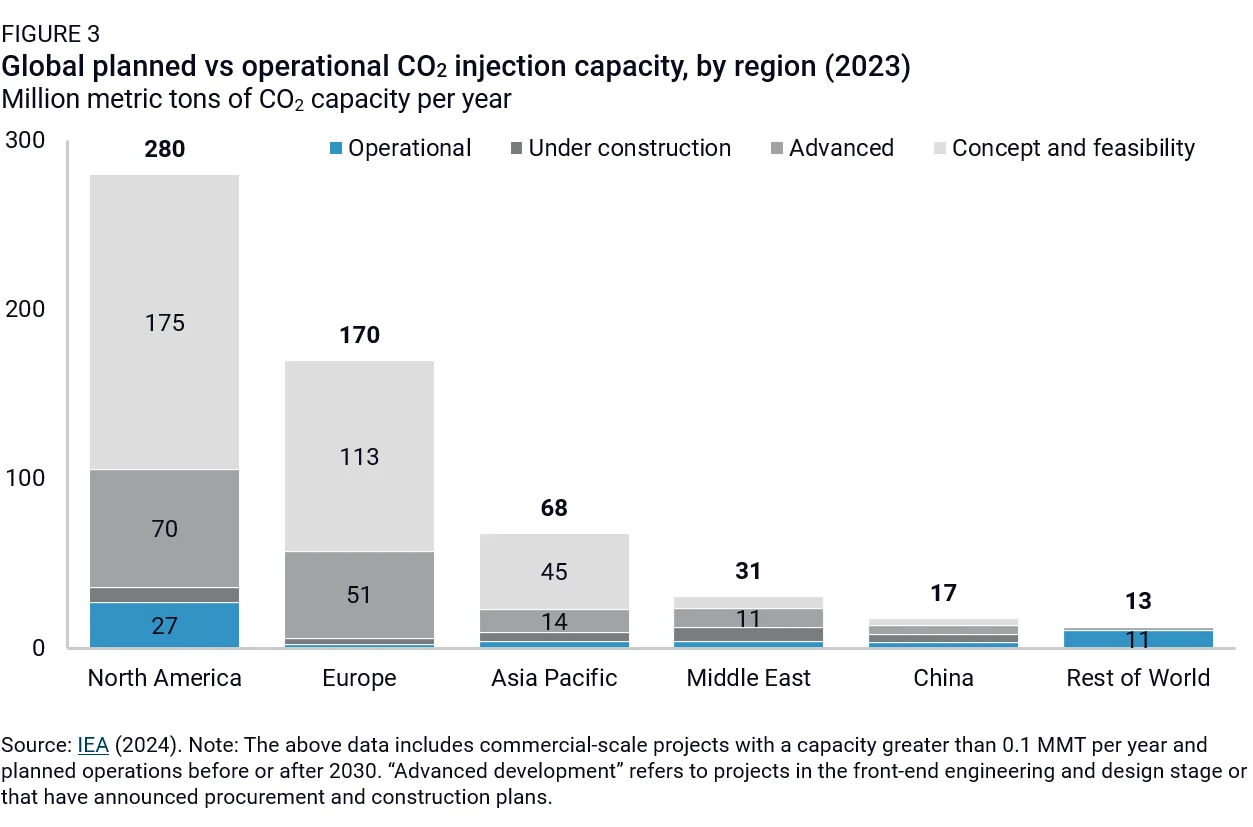

Many regions outside the US have some supporting infrastructure for DAC, though capacity is being deployed more slowly. According to 2023 estimates from the International Energy Agency, the US has almost twice as much planned and operational storage capacity as Europe and more than fifteen times the current levels in China. Moreover, only a small fraction of planned CO2 injection capacity is fully operational worldwide, indicating significant work ahead (Figure 3).

Other countries also lack adequate CO2 pipeline infrastructure to support DAC development. For example, China only recently completed construction of its first-ever long-distance dense CO2 pipeline, which became operational in July 2023. It can transport 1.7 MMT of CO2 annually over 67 miles. According to a study by the Beijing Institute of Technology, however, China needs far more capacity than it currently has, requiring construction of over 10,500 miles of CO2 pipelines to meet its annual peak CO2 reduction target in the power sector in 2060.

While our interviews with developers mostly suggested policy and infrastructure as the most significant barriers to scaling DAC, environmental factors could also limit attempts to scale DAC globally. The land requirements of DAC systems may enable diffusion more easily to countries with abundant, available non-agricultural space, and overall DAC system economics may also vary regionally. Countries may also face constraints around water requirements or interactions between their specific climatic conditions and the DAC systems’ resulting economic viability, since DAC capture capacity performs best at particular temperatures.

Other key factors, including the local energy mix and an innovation policy environment, may vary across regions. To the latter point, for instance, when companies pursue cost arbitrage and expand manufacturing in lower-cost countries, industrial policy can ensure that those technologies scale to those markets. In the case of other energy technologies, governments have enacted requirements for foreign companies to relinquish IP rights in exchange for desired market access and manufacturing incentives. As the US DAC industry pursues technology transfer over time, such requirements across regions may emerge and could significantly impact outcomes for global DAC scale-up. Moreover, the varying strength of IP enforcement regimes in different countries can encourage or limit scale-up in specific countries.

Assessment of the current DAC IP landscape

Although industry experts view policy support and infrastructure availability as the leading barriers to building global DAC capacity, IPRP remains essential when considering DAC scale-up. Interviews with DAC companies have revealed that significant specialized knowledge and IP arise during DAC development.

Various DAC technology types exist today, including liquid solvent, solid sorbent, mineral looping, electrochemical, cryogenic, membrane, and other novel forms. However, the leading developers in the US focus primarily on liquid solvent, solid sorbent, and mineral looping approaches. Solid sorbent DAC passes air through solid sorbents to capture a pure stream of CO2, while liquid solvent DAC passes air through liquid solvents to separate CO2. Mineral looping DAC loops a mineral sorbent (notably, calcium oxide or magnesium oxide) through its oxide and carbonate forms to react with and capture atmospheric CO2. While different DAC approaches vary in their respective technological readiness levels (TRL), experts consider the three types we focus on in this note to be closest to commercialization, while other types are currently at earlier stages of development. While a more exhaustive future analysis could explore nuances in the IPRP strategies that DAC developers operating across varying TRLs employ, this note focuses on those used for DAC technologies closer to commercialization.

In general, liquid solvent, solid sorbent, and mineral looping DAC technologies have significant technical characteristics that impact their replicability and, therefore, their potential for scaling and deployment. Sievert et al (2024) distinguish between “novel” and “off-the-shelf” DAC components. Under their definition, a novel component “is specifically developed for the DAC industry and not commercially available from any other industry.” In contrast, off-the-shelf components are “commercially available and do not require adaptation for DAC.” Some components they categorize as novel, such as sorbent materials, have often been available off-the-shelf (including zeolites and some recipes for metal-organic frameworks). While the authors acknowledge that sorbent materials broadly are well-established, they characterize the sorbent as novel because it is technically complex and used specifically for DAC processes. In other cases, components they categorize as novel, like air contactor units and calciners, are based on established technologies in different industries, specifically adapted for DAC. For instance, while the design of the air contactor units was based on industrial cooling towers, the internal geometry and fluid chemistry of the air contactor units operate differently, and engineers tailor them specifically towards DAC applications. As a result, even though the “novel” distinction does not precisely reflect novelty in the sense of innovation, the paper’s intellectual framework remains useful for our current assessment. Further analysis may assess the novelty of DAC components using a bottom-up approach, but such a method is outside the scope of this note.

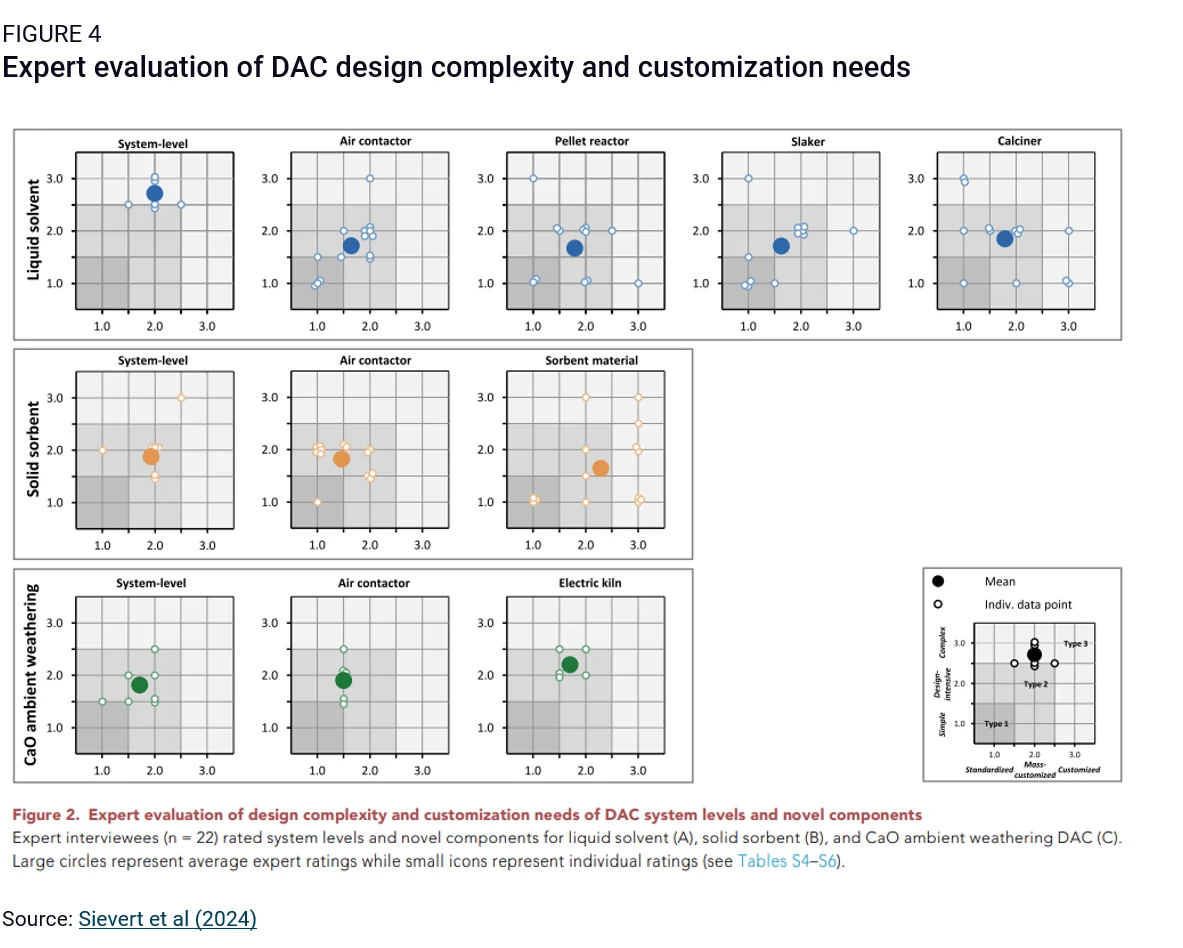

For solid sorbent DAC, from the authors’ characterization, the novel components are the adsorbent equipment (including the sorbent material) and the air contactor unit; for liquid solvent DAC, the novel components are the air contactor unit, pellet reactor, slaker, and calciner. The authors capture mineral looping DAC through a specific subtype (CaO ambient weathering), noting its novel components as the air contactor unit and the calciner (kiln). The off-the-shelf components in DAC systems include the condenser, compressor, fan, and vacuum pump. The authors’ survey of experts indicates that they consider DAC systems and their various novel components to have medium-to-high design complexity and require moderate customization relative to other clean energy technologies (Figure 4).

Experts view sorbent material for solid sorbent DAC as requiring the most site-specific customization of the novel components. Under that conceptual framework, they also generally note higher design complexity for liquid solvent DAC than solid sorbent DAC or mineral looping DAC. That said, many DAC developers across the spectrum of technologies, such as Carbon Engineering and Soletair Power, aim to ensure that their technologies can function as modular, turnkey systems (i.e., mass-manufactured, ready-to-operate), allowing for lower design complexity and less customization.

Surveys of the academic literature and interviews with leading DAC academic experts and developers confirm high technological complexity across the major DAC technologies.5 While patents require public disclosure of an invention, significant amounts of specialized knowledge arise such that competitors cannot easily replicate the technology from publicly available information. Since leading DAC technologies are in their demonstration phase, patenting is less about obtaining a competitive advantage and more about filing to ensure that competitors do not block them from first using some method or technique. This strategy reflects the “first-to-file” patent rule in the US. Further, developers focus patent efforts more strategically on technological aspects that competitors might be able to discover more easily through reverse-engineering and maintain less easily attainable information as trade secrets.

Given that developers hold the latter information proprietary rather than accepting the risks of public disclosure, analysis of IPRP requires a high-level understanding of what types of data they generate and insight into what knowledge they view as most competitively sensitive. For instance, for solid sorbent DAC, companies maintain secrecy around the chemistry and three-dimensional structure of the sorbent material, the ideal DAC process temperature, mechanical engineering knowledge for the capture unit, and engineering methods for steam integration. DAC developers generally hold the air contactor unit designs proprietary.

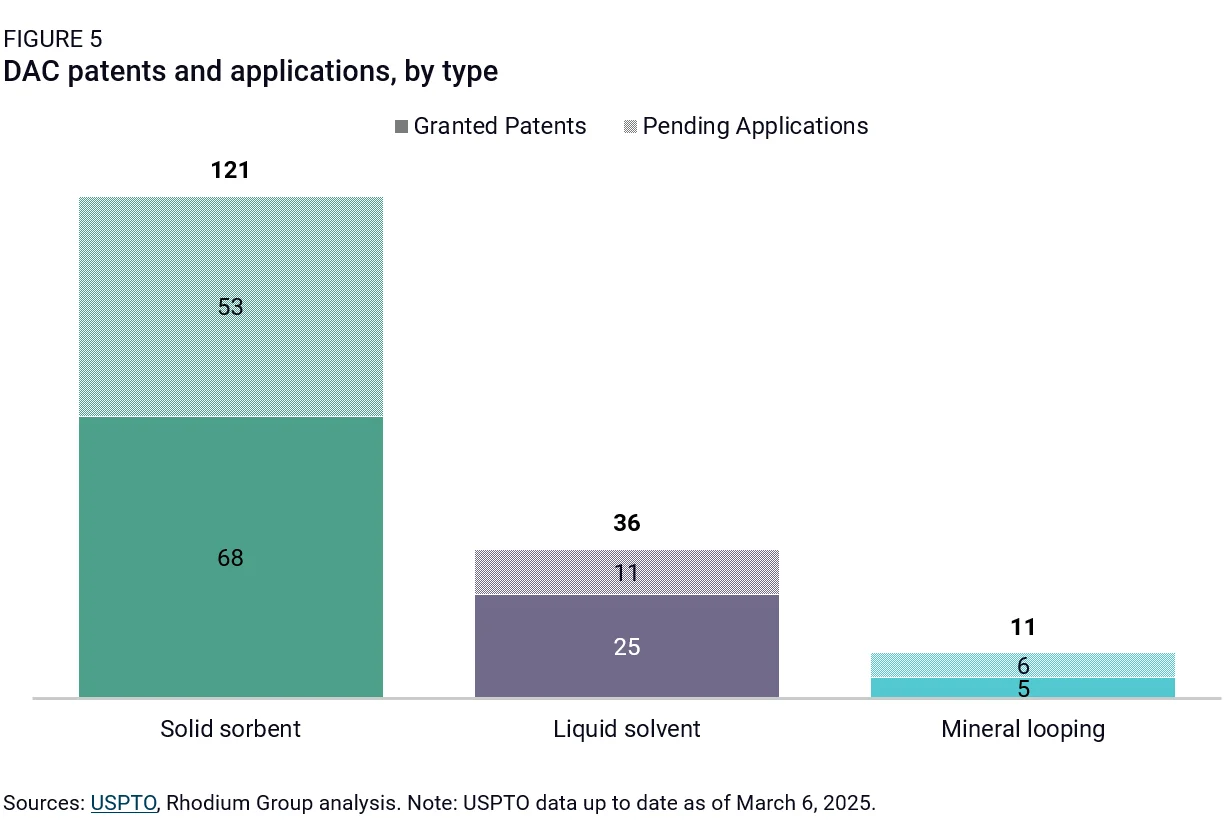

Looking across the field of established DAC developers, we analyze patent data from the USPTO Patent Public Search database for developers of solid sorbent, liquid solvent, and mineral looping DAC systems, for which the highest patenting activity has occurred for solid sorbent DAC (Figure 5).6 Solid sorbent DAC companies have filed over three times as many patents as liquid solvent DAC companies and more than ten times as many as mineral looping DAC companies. The USPTO data shows that a handful of the earliest-operating companies—Climeworks, Carbon Engineering, Carbon Capture, Heirloom, Zero Carbon Systems, and Infinitree—own a disproportionate share of DAC patent grants and pending applications.7 Collectively, these six companies own and have submitted more than half of all grants and pending applications. Given that the leading DAC technologies are still in the demonstration phase, it is understandable that some IPRP concentration exists.

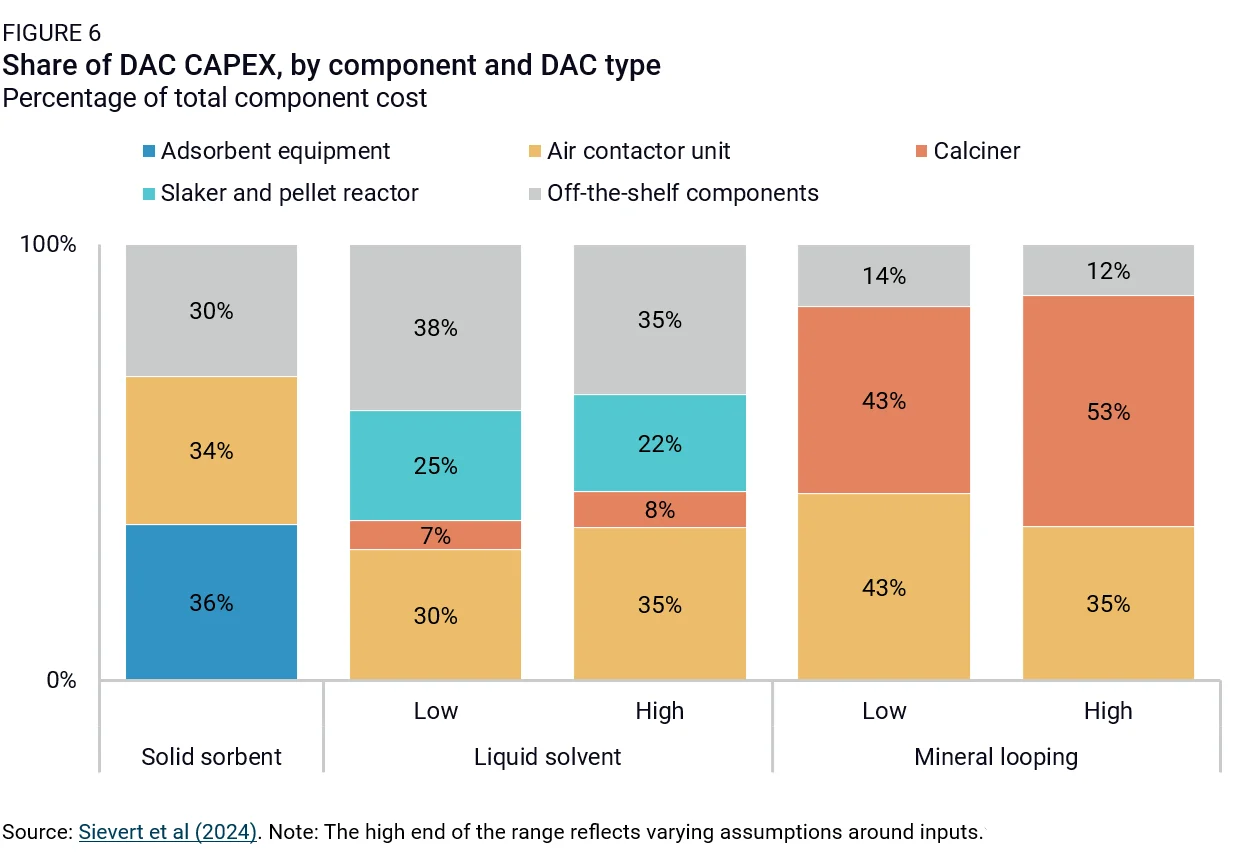

Trends in the patenting activity of DAC components are also instructive in understanding which components IP developers find most critical to protect. We find that, on average, there is some correlation between IP criticality and cost. For liquid solvent, solid sorbent, and mineral looping DAC, novel components comprise most of the component capital expenditure (CAPEX) requirements (Figure 6).8 While investigating causality between cost drivers and IPRP is beyond the scope of this note, patenting activity generally concentrates more on novel components than off-the-shelf components.

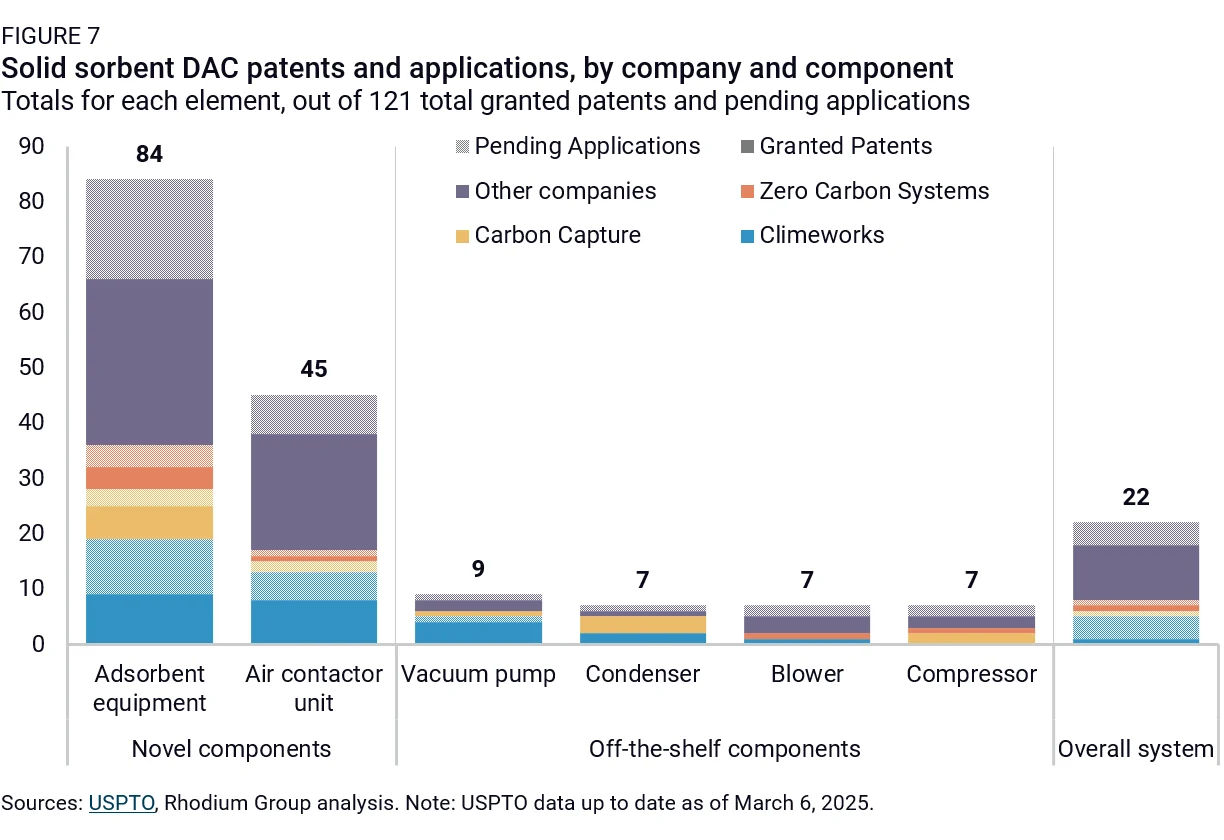

From USPTO data, more than 35% of all solid sorbent patents and pending applications have focused on these novel components (Figure 7).9 Put another way, solid sorbent developers have been pursuing IPRP for components they cannot obtain off-the-shelf, for which R&D and innovation will provide a more cost-effective return on investment. Solid sorbent companies deal with more customizable components that require more novelty, such as sorbent materials and adsorption/desorption bed design. Since sorbent material is key to their competitive advantage, developers generally find and capitalize on more opportunities to pursue patent protection. For instance, nearly 70% of solid sorbent patent grants and pending applications protect the sorbent material and related adsorbent equipment.

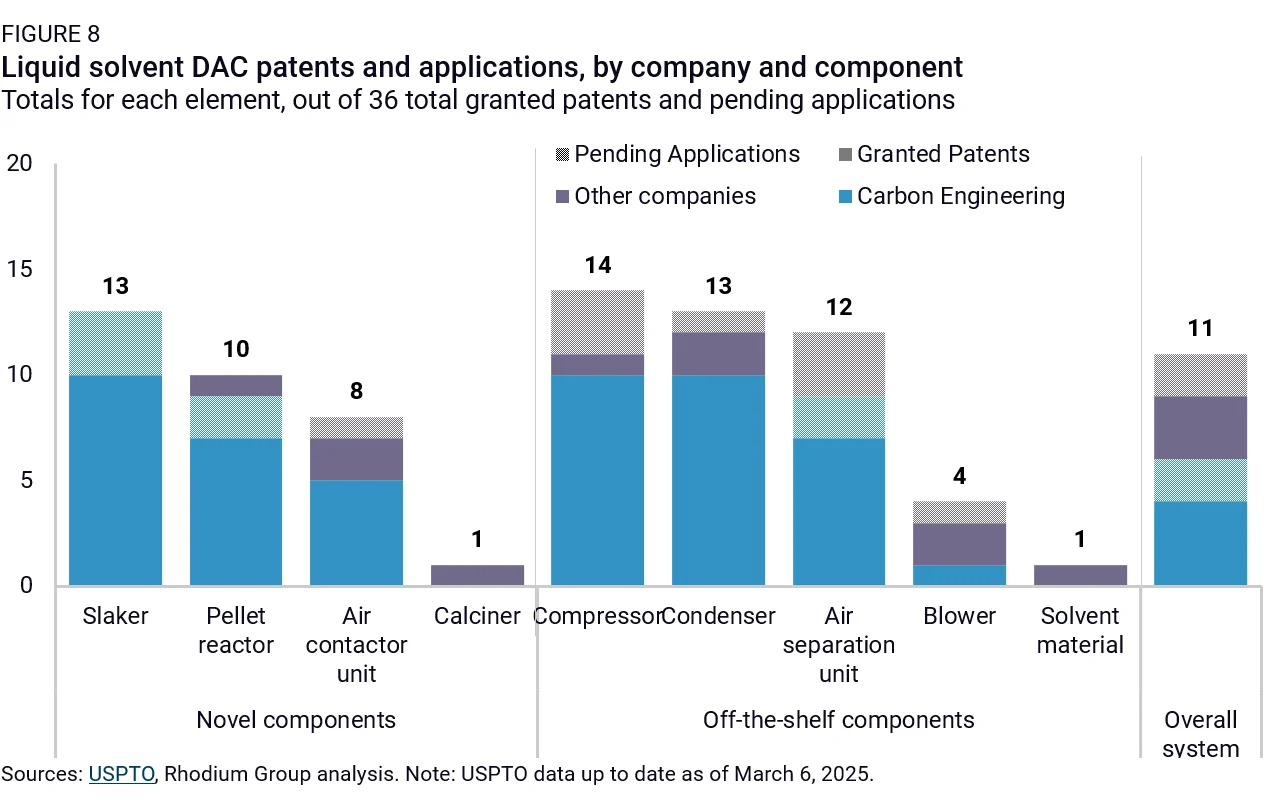

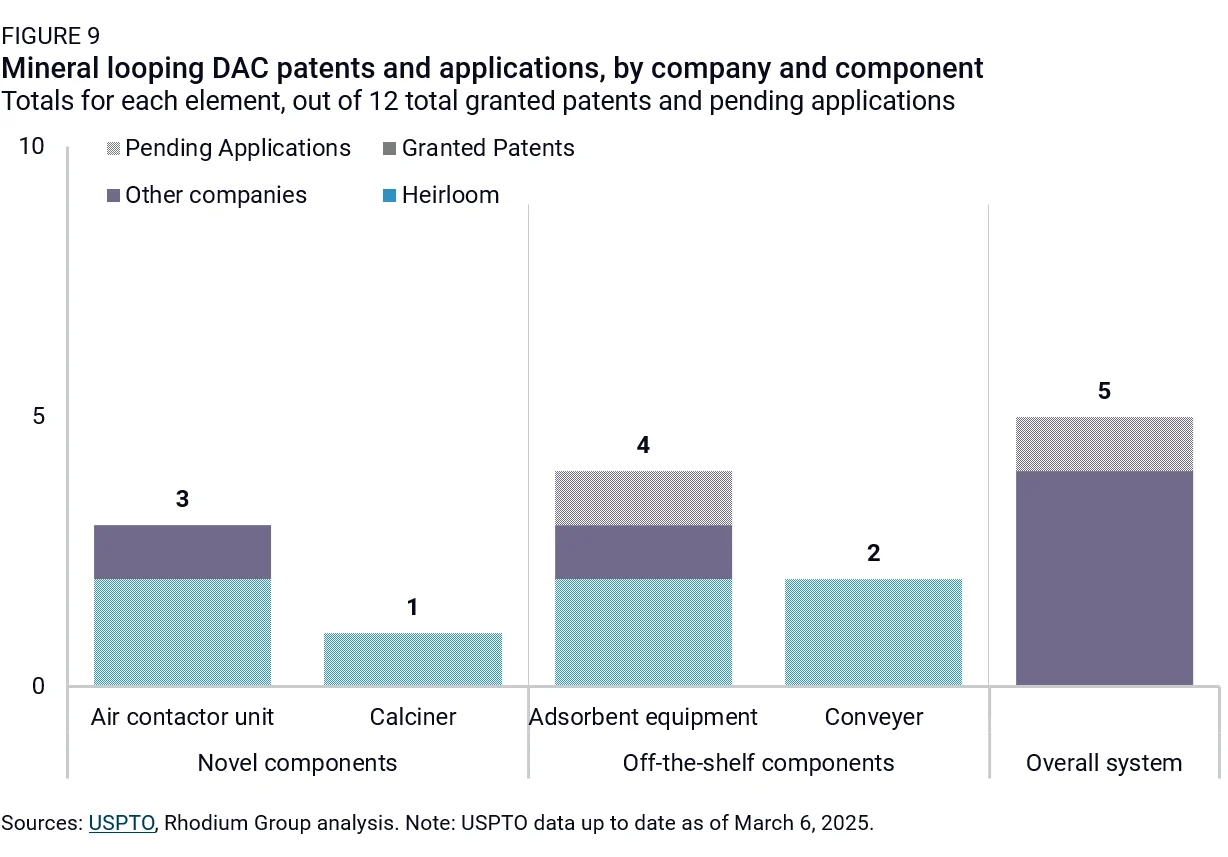

The patenting focus is even for liquid solvent DAC and mineral looping DAC (Figures 8-9). There are minor differences in patent grants and applications between different components, and patenting activity around the overall system plays a larger role. This more even strategy to IPRP may be due to less maturity overall, as there are two to three times fewer companies focused on liquid solvent approaches than solid sorbent companies, and only a handful are focused on mineral looping. Additionally, for both liquid solvent and mineral looping DAC, there are fewer opportunities for customization at present, relative to solid sorbent technologies.

Will IPRP create significant barriers to global DAC deployment?

DAC is still a relatively early-stage technology today. Thus, it is unclear how much of a role IPRP and specialized knowledge will play in the ability to scale DAC technologies worldwide. However, we can look to our survey of previous energy technology innovations—more specifically, hydraulic fracturing and solar PV—to make inferences about the criticality of IPRP and specialized knowledge, and how they can potentially affect the broader dissemination of DAC technologies beyond just the US market.

Based on the discussion above, in its technical characteristics, DAC is ostensibly more like hydraulic fracturing than solar PV, as it requires significant site-specific customization and specialized engineering know-how. Though labor in the oil and gas industry developed specialized knowledge over a much more extended period than DAC has even lived outside of the lab, at present, DAC manufacturing is similar in that it relies heavily on specialized knowledge. Cost-efficient replication and scaling of DAC systems require chemical engineering techniques for sorbent material, mechanical engineering knowledge for unit designs that may be uniquely suited to specific geographies, and understanding of optimal climatic conditions for capture economics.

Like hydraulic fracturing, liquid solvent DAC, solid sorbent DAC, and mineral looping DAC are technically complex. Across the set, their most cost-efficient deployment similarly emerges at specific temperatures and pressures and through design details that developers do not generally share publicly. Our analysis of patent data confirms that patenting activities have thus far resembled sites of early jockeying for any potential future market positioning around costly components rather than avenues for protecting their most critical innovations. For such inventions, developers see the information they patent as being more easily reverse-engineered and less easily kept secret. For solid sorbent DAC systems, especially, where finding cost-efficient structures and materials for the sorbent will be the main bottleneck for longer-term cost reductions, developers are focusing on extending early patent coverage around it before the industry reaches maturity.

Solar PV, conversely, was much less specialized and relatively more straightforward to replicate, using modular designs. Historically, the most essential factors for its global scale-up were public policy support and the availability of enabling infrastructure. However, for hydraulic fracturing, because of its high technological complexity, the need for specialized knowledge was just as central as public policy and infrastructure, limiting its scale-up beyond the US and a handful of other countries. This suggests that, while policy and infrastructure will be essential to ramping up successfully, IPRP will likely play a less central but still significant role alongside them in determining the extent of DAC’s scalability.

While noting that, DAC developers are working early to find potential solutions that work around any IPRP barriers that may arise. As mentioned previously, some companies have begun developing turnkey solutions, enhancing the modularity of DAC systems. If these approaches are successful and widely adopted across the industry, developers could deploy DAC systems quickly at scale, as was true in the case of solar PV, and decrease some of the need for specialized knowledge. IPRP and specialized expertise could be moderate to high barriers for DAC scale-up globally. Still, collectively, they will likely be less critical to get right than favorable policy or infrastructural readiness.

Moving DAC forward will require continued efforts

The path to commercial-scale DAC deployment over the next decade will undoubtedly be steep. Leading DAC technologies have reached their demonstration phase in the US. Still, they require further investment and cost learning to develop into a competitive commercial option alongside more established clean technologies like solar PV, wind, and nuclear. The US and other countries worldwide must continue to enact even more supportive policies and accelerate progress toward building vast supporting infrastructure. DAC’s most essential support mechanisms over the long term are public policy and infrastructure. At the same time, DAC technology developers must balance protecting their IP to maintain a competitive advantage and licensing their patents (and sharing specialized knowledge) widely enough that the entire industry can effectively drive down costs over time.

Footnotes

Due to constraints in data availability, we plot patents and installed capacity for total solar (including both solar PV and concentrating solar power). Since the vast majority of solar has been solar PV, we assume that the patterns remain broadly applicable to our discussion of solar PV. Further granularity remains beyond the scope of this note.

DAC only offers private value if companies use the captured CO2 as an input in various industries. See: https://www.american.edu/sis/centers/carbon-removal/fact-sheet-carbon-capture-and-use.cfm

Given ongoing discussions around the federal reconciliation bill at the time of publication, particularly the potential repeal of IRA tax credits, this assessment of the US policy landscape is subject to change.

Here, we report NETL’s medium (P50) estimate for CO2 saline storage resource potential, produced using a storage efficiency factor (Esaline) of 2.0%. This metric refers to the volumetric fraction of subsurface sites available for saline CO2 storage, due to various physical characteristics of storage sites. NETL’s low scenario assumes Esaline = 0.51% and estimates roughly 2.4 trillion metric tons of available CO2 storage capacity, while the high scenario assumes Esaline = 5.5% and estimates available capacity of around 21.6 trillion metric tons.

As part of the research process, we conducted interviews with academic experts and multiple DAC developers to obtain further information.

In the “Pending Applications” category, we aggregate data across both provisional patent applications and full utility patent applications.

Given Global Thermostat’s sale to Zero Carbon Systems in May 2024, for the purposes of understanding patent concentration by company within the DAC industry, we include Global Thermostat’s patenting activity within the figures for Zero Carbon Systems.

These include factors such as electricity costs, heat integration costs, new technology cost premium, equipment costs, etc.

For all DAC types, we mapped each patent and pending application to all components the developer aimed to protect, based on the description in the USPTO patent publication. For example, one individual patent by a solid sorbent developer might map to the adsorbent equipment, air contactor unit, and other components.