Going Beyond Carbon: Closing the Non-CO2 Ambition Gap

Efforts to mitigate emissions have largely focused on CO2. We assess the gap around non-CO2 emissions, in particular methane.

At the upcoming COP28 climate summit in Dubai, the world will take stock of progress toward meeting the Paris Agreement goal of limiting warming to well below 2º Celsius. This Global Stocktake will be an opportunity to identify gaps in the collective effort to address global climate change and ways to enhance ambition. The Group of 20 (G20) highlighted one such gap in its most recent Leaders Declaration, noting many countries do not yet have economy-wide absolute emission reduction targets and calling for them to be reflected in nationally determined contributions (NDCs) “in light of different national circumstances.” This means reducing not just carbon dioxide (CO2), but also short-lived climate forcers like methane, hydrofluorocarbons, and other non-CO2 gases, which contribute roughly a quarter of global greenhouse gas emissions. To provide context on the contribution of these gases, in this note we assess the scale and key sources of non-CO2 emissions from some of the world’s largest greenhouse gas emitters—the G20 members themselves.

Global non-CO2 emissions

Efforts to mitigate greenhouse gas (GHG) emissions over the past few decades have largely focused on curbing CO2 emissions. Indeed, CO2 has contributed the most to warming experienced to date and contributes three-quarters of total global GHG emissions. Keeping warming below 2ºC also requires significant and sustained reductions of non-CO2 emissions as well. According to the Intergovernmental Panel on Climate Change, reducing emissions of short-lived climate forcers is “critical to meet long-term climate goals and might help reduce the rate of climate change in the short term.” Reductions in methane emissions are particularly critical to keeping the Paris Agreement goals within reach. Due to its much shorter lifetime, methane has a disproportionate impact on near-term temperature and is estimated to account for almost a third of the warming observed to date.

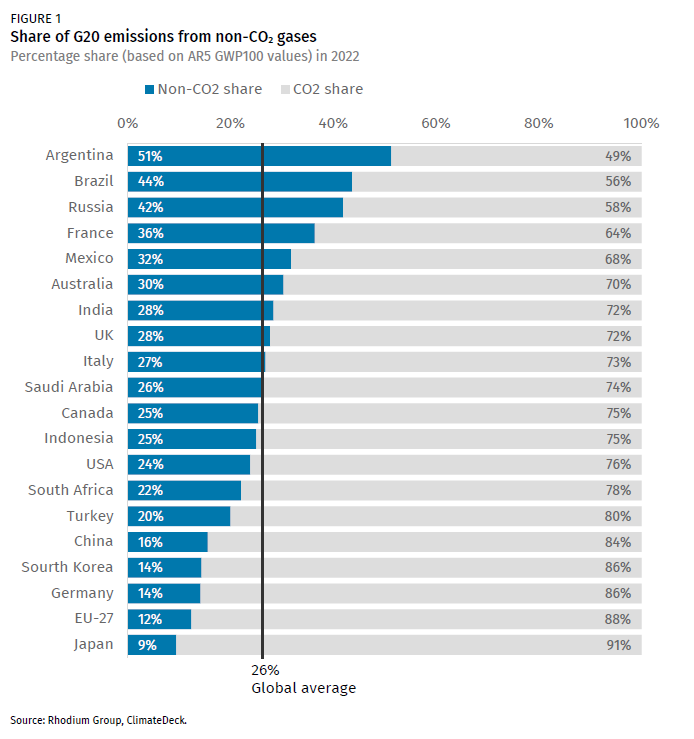

Globally, non-CO2 gases contribute roughly a quarter of GHG emissions today, but there is wide variation among countries. Among the G20 economies, non-CO2 shares of total GHG emissions range from only 9% in Japan to as high as 51% in Argentina (Figure 1). Most G20 economies’ non-CO2 shares are on par with the global average, though several countries have much higher-than-average shares, including Argentina, Brazil (44%), Russia (42%) and France (36%).

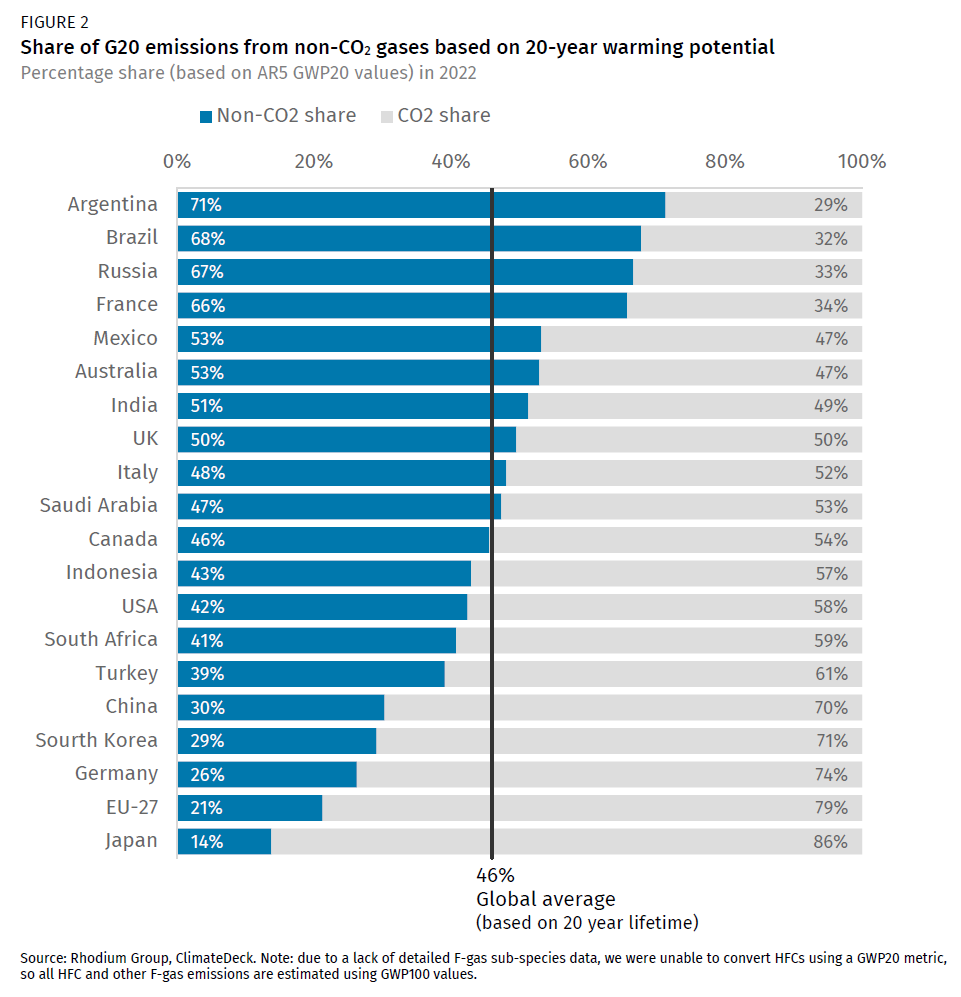

To account for methane and other short-lived climate forcers’ relatively short atmospheric lifetimes, a different metric (GWP20) can be used to compare non-CO2 gases to CO2 equivalents using a 20-year lifetime rather than 100 years (as in the conventional approach of using GWP100 values). The choice of metric, including time horizon, should reflect the policy objectives for which the metric is applied.[1] According to the IPCC, “all metrics have limitations and uncertainties, given that they simplify the complexity of the physical climate system and its response to past and future GHG emissions. No single metric is well-suited to all applications in climate policy.” When methane and nitrous oxide are considered on a 20-year horizon, non-CO2 gases represent a much larger share of total GHG emissions. Based on this metric, the share of non-CO2 gases rises to over 30% for the majority of G20 economies. Half of the G20 members have non-CO2 shares that exceed the global average of 46% non-CO2 based on a 20-year lifetime (Figure 2).

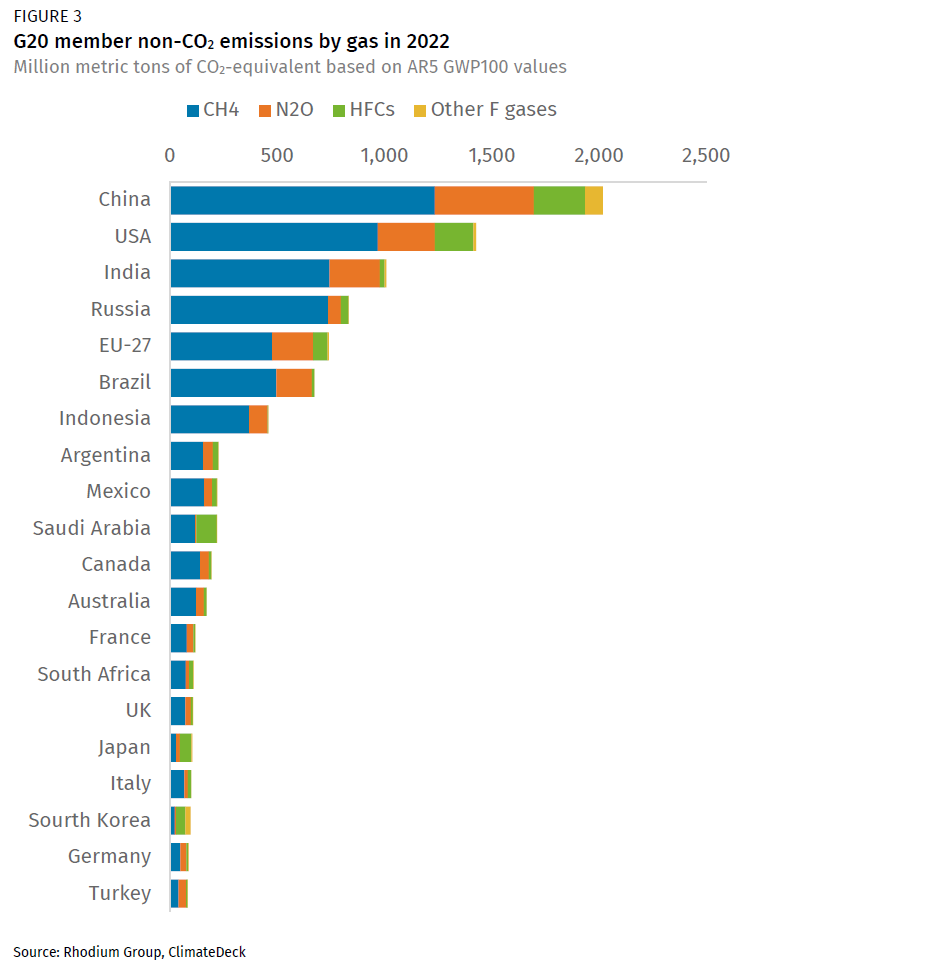

For some G20 economies, even if non-CO2 emissions represent a quarter or less of total emissions, on an absolute basis these emissions are quite sizeable (Figure 3). Even if you excluded China’s CO2 emissions entirely, its non-CO2 emissions would rank as the world’s third largest GHG emitter (using both 20- and 100-year GWP values). The non-CO2 emissions from the US and India would rank them as the world’s sixth and seventh largest emitters, respectively, and Russia’s non-CO2 emissions alone would rank it the world’s 10th largest emitter. The EU-27’s non-CO2 emissions would earn the rank of 11th largest emitter, while Brazil’s would land at 13th.

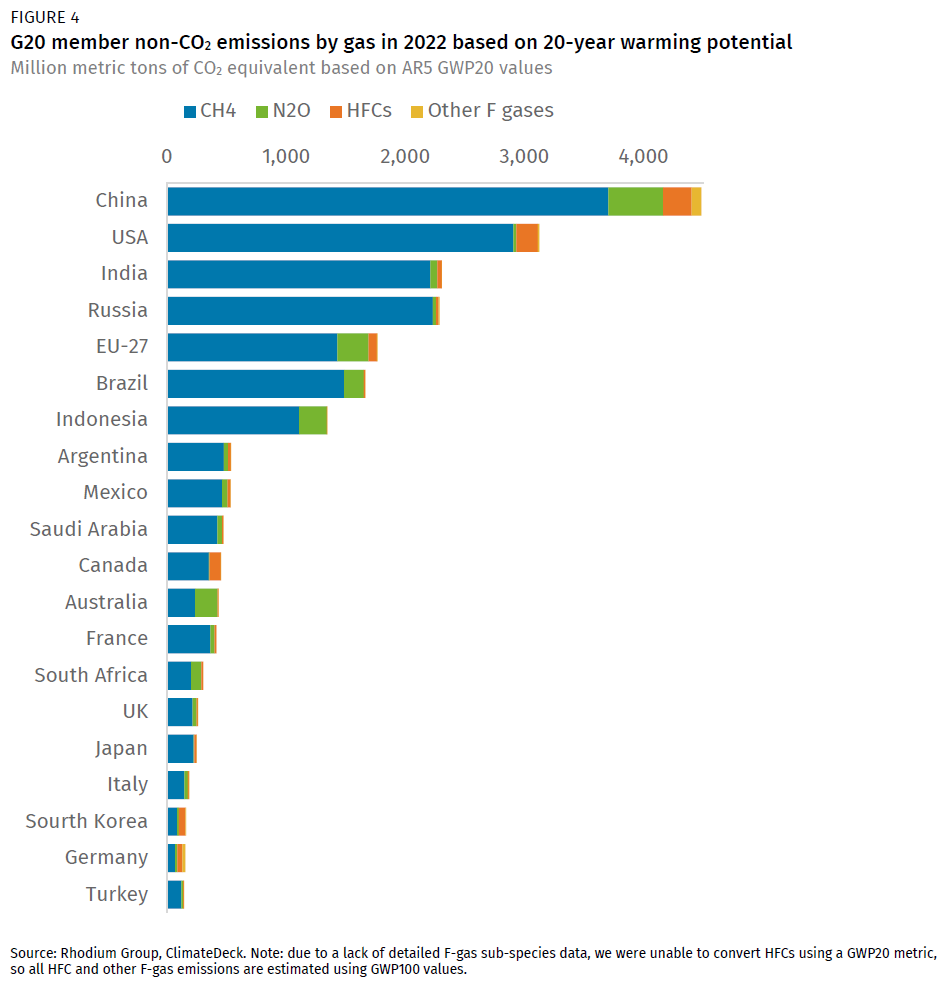

When considering a 20-year lifetime for methane (CH4) and nitrous oxide (N2O), the total CO2 equivalent of non-CO2 emissions jumps considerably (Figure 4).

Methane is a majority

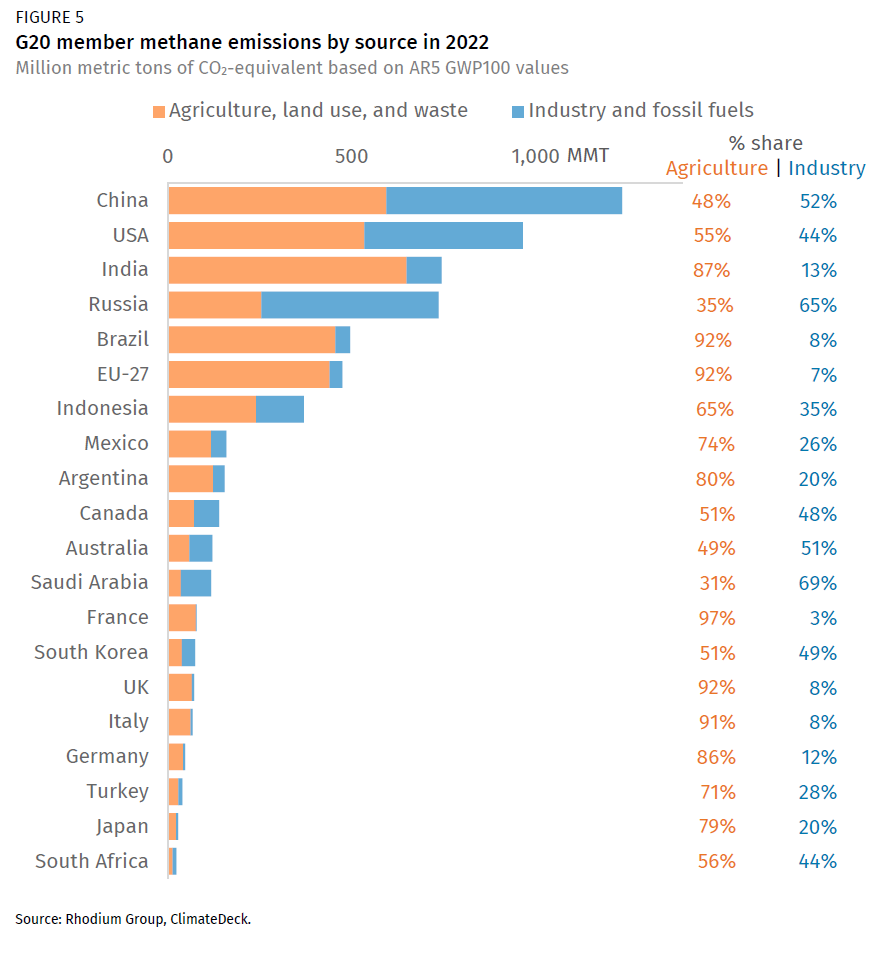

Methane is by far the largest source of non-CO2 emissions, contributing 69% of all non-CO2 gases. In all but two G20 economies, methane makes up the majority of non-CO2 emissions. In some countries (e.g., Russia, Brazil, Indonesia), methane makes up more than three-quarters of total non-CO2 emissions (on a GWP100 basis). In 2021 at COP26, a coalition of countries launched the Global Methane Pledge with the aim of reducing global methane emissions at least 30% from 2020 levels by 2030. Since then, over 150 countries have signed the pledge to contribute to collective action to reach the 2030 goal. All G20 member states—with the exception of China, India, Russia, and Turkey—have signed the pledge.

The two primary sources of methane emissions are 1) agriculture, land use, and waste; and 2) industrial sources including the production and use of fossil fuels. For most G20 member economies, the majority of methane emissions come from agriculture, land use, and waste. Several fossil fuel-producing members—including China, the US, Russia, Canada, Australia, and Saudi Arabia—have sizeable methane emissions from the fossil fuel industry.

Closing the non-CO2 ambition gap

At the conclusion of the first Global Stocktake at COP28 in Dubai this year, the world should walk away with a clear sense of what remains to be done to meet the Paris Agreement goals of limiting warming to well below 2ºC. One critical next step is to enhance the ambition of countries’ nationally determined contributions (NDCs). As the Paris Agreement itself lays out, each country’s successive NDC should represent a progression beyond their earlier commitments, reflecting their highest possible ambition. More specifically, Article 4.4 provides that “Developed country Parties should continue taking the lead by undertaking economy-wide absolute emission reduction targets. Developing country Parties should continue enhancing their mitigation efforts, and are encouraged to move over time towards economy-wide emission reduction or limitation targets in the light of different national circumstances.” To date, the NDCs of two G20 member states—India and China—do not include coverage of non-CO2 gases. Given the significant contribution of emissions of non-CO2 gases to global GHG emissions and their meaningful short-term impact on warming, integrating absolute reductions of non-CO2 emissions into countries’ NDCs (for those that do not currently) and adopting progressively ambitious absolute reduction targets that include non-CO2 reductions in current and future NDCs will be critical to closing the ambition gap and putting the world on track to meet the Paris Agreement long-term goals.

[1] According to the IPCC, the GWP time horizon can be linked to the discount rate used to evaluate economic damages from each emission. For methane, GWP100 implies a social discount rate of about 3–5% depending on the assumed damage function, whereas GWP20 implies a much higher discount rate, greater than 10%.