Slaying Self-Reliance: US Chip Controls in Biden’s Final Stretch

With its December 2 chip control rules, the US is deploying a powerful combination of long-arm measures and entity listings that center on China’s self-reliance nexus of Huawei and SMIC.

The US Department of Commerce released its third edition of semiconductor controls targeting China on December 2. While markets responded positively to media reports casting the rules as lightweight, a close read reveals a different picture: The US is deploying a powerful combination of long-arm measures and entity listings that center on China’s self-reliance nexus of Huawei and SMIC. Additional Japanese and Dutch controls are likely to emerge in the wake of this rule, completing the picture of what US measures are trying to achieve.

The rules cover new chokepoints, namely high bandwidth memory for AI chips, and expand semiconductor manufacturing controls in coordination with key partners. In doing so, the US is gambling it can “impair” China’s ability to produce advanced node chips and buy the US and partners more time to widen their lead over China. This is a big bet, given the uncomfortable truth that US tech controls have so far accelerated China’s state-backed campaign to indigenize semiconductor supply chains, and its success hinges on partner cooperation.

The stakes are rising precipitously: While the US is leveraging US-origin technology to amplify long-arm controls in this rule, China is exercising its clout in critical materials production and invoking extraterritorial restrictions that mimic US long-arm provisions. In addition to prepping a negotiation with Trump, Beijing is moving swiftly with retaliatory moves to dissuade US partners from harmonizing controls.

This note breaks down the most striking features of the chip controls, assesses potential impacts on China’s semiconductor ecosystem, and interrogates the implications of this combustible mix of tightening US tech controls, tense partner relationships, and a new phase of Chinese retaliation.

Creative “calibration”

The December 2 semiconductor controls are remarkably candid about their objective: to “impair” China’s production or development of advanced chips. The Commerce Department’s Bureau of Industry and Security (BIS) is trying, first and foremost, to address China’s “independent and controllable” campaign to indigenize semiconductor production. BIS describes this state-backed program as an accelerant to China’s military modernization and a threat to US and partner tech leadership. The US is now being more explicit about its goal while reluctantly acknowledging that the results have been mixed. US controls have fueled rampant stockpiling of foreign equipment over the past two years while accelerating China’s tech indigenization efforts through the two engines of its self-reliance drive—Huawei, China’s leading chip designer, and SMIC, China’s leading foundry. Consequently, BIS frames the rule as a “calibration” of chip controls.

“Calibration” in this context means concentrating US firepower on Chinese targets via entity listings and long-arm measures. But there is more to it: BIS has woven in a complex web of partner carveouts conditioned on their implementation of equivalent controls. This has several purposes. For one, BIS cannot assert a “foreign persons” rule like it has for US persons to extend its long-arm reach, but it can use the Foreign Direct Product (FDP) Rule and de minimis provisions to create similar effects and push key partners toward alignment.

For major producers of advanced semiconductor manufacturing equipment (SME), like Japan and the Netherlands, this means imminent, albeit quiet, steps to patch up and align SME controls are likely forthcoming. Had the US not coordinated with key partners on harmonizing controls, it could have just as easily removed the carveout and relied on FDP and de minimis measures alone. Disrupting the service and repair of China’s existing installed base of advanced SME has been a core priority of US negotiations—we will be looking for signs of those areas being covered in subsequent partner controls and licensing practices. The US is betting that, without foreign assistance to keep complex lithography, deposition, etch, and other tools running, Chinese yield will decline to critically low levels and significantly slow China’s production in advanced node chips.

Germany will be another key country to watch. Berlin has resisted alignment on US export controls thus far, but if it does not align with the product scope for SME in the new rule, the US could opt to revoke its carveout and subject it to FDP-level restrictions in a subsequent rule update. US partner countries that play a role in SME supply chains but have not yet harmonized controls (most notably, South Korea and Singapore) are subject to licensing requirements unless they impose equivalent controls. Countries that are allies of the US but are not SME-producing also get a carveout, though this is more symbolic than substantive.

Understanding the chip rule stack

To understand the potential impact of these measures, think of the December 2 controls as operating in one big stack. The layers of the stack may vary in scope and target, but the full (potential) effects are only visible in the complex interplay of these layers.

Layer 1: Target Huawei-SMIC nexus with extraterritorial measures

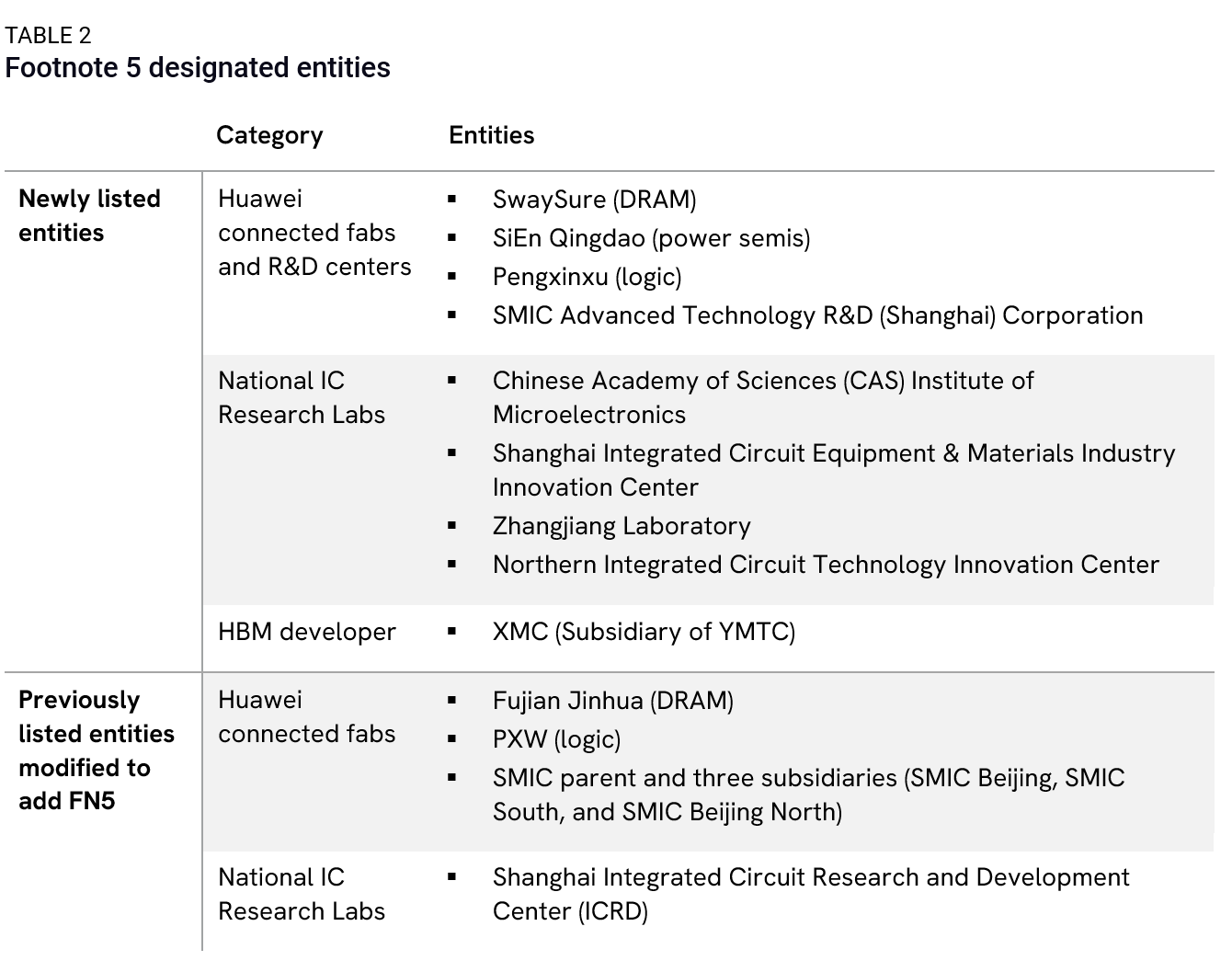

The rule establishes new Foreign Direct Product Rule Footnote 5 designations, or FN5 FDP entities, with the aim of disrupting Huawei’s emerging indigenous supplier network. FDP rules extend US extraterritorial reach by covering products that contain or were manufactured using US-origin technology. Think of the FN5 FDP as a tool to multiply the “Huawei effect,” where the US can impose heavy, long-arm restrictions on high-value targets on the grounds that their activities contribute to China’s military modernization. FN5 FDP entities become instant liabilities to multinational firms.

The sixteen entities (so far) designated under FN5 FDP designations are at the forefront of China’s tech indigenization charge: Huawei-connected fabs and R&D centers, SMIC subsidiaries, and YMTC’s high bandwidth memory (HBM)-developing subsidiary, Wuhan Xinxin Semiconductor Manufacturing (XMC). A broader SME product scope is assigned to FN5 FDP entities to cut off as much foreign tool supply as possible to these high-priority targets. In addition, BIS is also tightening up licensing standards, with multiple SMIC entities to be treated with the presumption of denial.

Layer 2: Lock in extraterritorial measures for SME

The update introduces a second FDP rule for advanced semiconductor manufacturing equipment (SME FDP). Advanced SME is already largely covered by export controls, including a range of extraterritorial measures like US persons restrictions and 0% de minimis US content rules for advanced photolithography machines. This rule introduces yet another layer of exterritorial controls on advanced SME via the FDP rule. The rule enables the US to periodically expand the scope of FDP-covered SME products over time and assert a long-arm standard for compliance to hold partners accountable.

Most of the SME items under the new SME FDP rule have already been harmonized with the Netherlands and Japan, though the US may be reinforcing alignment on licensing stringency, to include coverage of servicing and repair on spare parts and components of covered SME. Foreign subsidiaries of US SME producers that may have been trying to circumvent the US persons rule will now be caught by the SME FDP. BIS has also added a handful of newly controlled SME tools under the SME FDP product scope, including machinery critical to the production of advanced high bandwidth memory, as well as unproven emerging technologies like nanoimprint lithography that could eventually offer Chinese firms a workaround to broad US and partner-allied restrictions on DUV lithography systems.

The SME FDP rule’s product scope focuses narrowly on advanced tools, while the restricted product scope for FN5 FDP entities covers a broad range of SME, components, and accessories (see Table 1), including certain “node-agnostic” equipment and tools that can be used to optimize DUV lithography-based production processes (ECCN 3B993 technologies).

With FDP leverage now attached to SME controls via both the SME FDP and FN5 FDP rules, the US is imposing SME controls universally. For Japanese, Dutch, and German suppliers, this means the US is laying down an expectation that harmonized controls will follow if they want to keep their carveout status. Meanwhile, Korean and Singaporean suppliers, whose host governments have not yet signed onto harmonized controls, are now subject to US licensing for covered products unless, and until, their governments impose equivalent controls to regain licensing sovereignty. SME companies headquartered in Malaysia, Taiwan, or Israel (SME-relevant countries not on either of the US partner lists referenced in the rule for carveouts), will come under US long-arm licensing restrictions regardless, unless the US adjusts licensing exemptions over time to reward partner cooperation.

Layer 3: Amp up extraterritoriality with revised “single chip” de minimis standard

Close observers of US chip rules will remember well the “0% de minimis” standard for advanced lithography, which BIS introduced in the October 17, 2023 update to force the Netherlands to align on expanded controls on DUV machines. The new rule adds another de minimis provision, this time to a broader product scope for SME beyond advanced lithography. The new provision, which we call “single chip de minimis,” says if a foreign-produced item is made in a plant anywhere in the world, and if that plant or “a major component” of a plant where that tool was made contains a single US chip, then the US can assert extraterritorial jurisdiction to restrict controlled items.

In attaching this expansive de minimis provision to the Foreign Direct Product rules for FN5 entities and SME described in layers 1 and 2, the US is going out of its way to assert extraterritorial jurisdiction. As the rule states, the FDP rules “simply recognize that certain SME items—already subject to comprehensive restrictions […] when they originate from the United States—should also be subject to controls” when those SME items are made abroad and could not have been produced without US technology in the first place. In other words, the US is bolstering the de minimis provision to prevent foreign suppliers from filling the gap left by US companies forced to cede their market share in China.

Layer 4: Create the hook

US blacklisting is designed to create a broader chilling effect on transactions with Chinese entities. The FN5 FDP entities described in Layer 1 are already subject to US long-arm restrictions since they form the core of the Huawei-SMIC nexus. The BIS rule adds to its Entity List 140 companies engaged in China’s indigenous semiconductor supply chain, subjecting these firms to US licensing restrictions on the presumption of denial. The Entity List covers most of the key players in China’s emerging advanced semiconductor ecosystem (with a few notable omissions like CXMT, China’s leading DRAM developer). It even includes firms like Wingtech (the Chinese owner of Netherlands-based semiconductor firm Nexperia) and the investment firms that enabled that acquisition, JAC Capital and Wise Road Capital, arguing that these firms have promoted China’s advanced chip development via strategic investments and acquisitions. We expect this list to expand over time to identify companies in the orbit of FN5 FDP entities. Companies on the Entity List could also be a step away from getting an FN5 FDP designation themselves, assuming most roads in China’s indigenous chip supply network lead to the Huawei-SMIC nexus.

Layer 5: Expand SME coverage with extraterritorial push

BIS creates a new export control classification number (ECCN 3B993) to cover various “node-agnostic” tools that can be used for both legacy and advanced chip production, as well as certain tools used to optimize production using deep ultraviolet lithography and multi-patterning techniques. China has been relying heavily on such tools to develop leading-edge AI chips with older technology. If partners issue equivalent controls, then they will be exempt. This is the same approach the US used to pursue the first wave of SME control harmonization with the Netherlands and Japan.

Layer 6: Raise costs of doing business in China with the “knowledge” standard

BIS throws a bone to the industry by creating the Entity List of Chinese semiconductor companies subject to US licensing restrictions. This is in response to industry appeals for a list that compliance officers can use to screen transactions. BIS also established a new License Exception, Restricted Fabrication Facility (RFF)—effectively a license for companies to sell equipment for non-advanced node production to China. At the same time, BIS imposes stringent reporting on companies to prevent covered products from being diverted to listed entities or advanced node production lines. This includes new reporting requirements on fab equipment for legacy chip production going into China and notifications “within one business day” when a company “gains knowledge” that equipment is being used for advanced node production. It also includes a red flag test that assumes covered equipment can be diverted to advanced node production in physically connected facilities. Given the barriers companies face to on-site inspections of such facilities in China, providing legal assurance that no diversion is happening will be an uphill battle. This may result in foreign suppliers reducing transactions with certain Chinese entities out of caution.

Layer 7: Stay on top of emerging chokepoints like high bandwidth memory

BIS covers a new chokepoint in the rule aimed at slowing China’s indigenous development of AI hardware: high-bandwidth memory (HBM) chips. HBM chips are distinct from consumer-grade DRAM and are integral components in high-end AI accelerators. As with previous controls on advanced AI chips, the new rules set technical thresholds that will effectively ban the sale of advanced high bandwidth memory chips at level HBM2E and above to China.1 For context, Huawei uses HBM2E produced by Samsung in its current Ascend 910B AI processor.

None of China’s memory producers is currently capable of producing HBM2E. This means that if the rule is enforced effectively, this restriction will compel Huawei to rely on stockpiled HBM to continue producing AI accelerators domestically unless it can make breakthroughs in indigenous production. Huawei, Alibaba, and other leading Chinese AI chip designers have reportedly been stockpiling HBM since early 2024 in anticipation of tighter controls, and with BIS granting HBM suppliers a one-month grace period before the new rules take effect, there will be a furious rush to buy up as much stock as they can over the next few weeks.

However, stockpiling can only serve as a short-term fix. NVIDIA’s new Blackwell processors incorporate up to eight stacks of HBM3E, while SK Hynix and TSMC are partnering to push forward mass production of next-generation HBM4 by early 2025. With access to foreign HBM now restricted, China will need to establish a viable domestic HBM producer quickly to keep pace.

Multiple Chinese firms are currently working on HBM development, including newly entity-listed Huawei partner and YMTC subsidiary XMC. However, the list notably excludes China’s DRAM champion, ChangXin Memory Technologies (CXMT), which is widely viewed as the country’s leading HBM player and is rumored to have already begun volume production of HBM2. CXMT’s omission from the latest round of entity listings raises legitimate questions, particularly given its status as a major customer for Western SME producers. In lieu of an entity listing, BIS is betting that the new SME FDP rule will be sufficient to limit CXMT’s access to high-end foreign equipment required for HBM production, most notably through the addition of new ECCNs covering high aspect-ratio etch tools.

Self-reliance on steroids

When these layers stack together, the controls are potentially far-reaching and hard-hitting. BIS has created substantial long-arm mechanisms to further patch up loopholes that have allowed Chinese fabs to stockpile foreign SME and degrade the effectiveness of stockpiled equipment that is already contributing to China’s advanced chip production. If partner alignment comes through in the coming weeks, the China sales bonanza enjoyed by foreign SME suppliers will quickly dissipate.

Foreign SME makers have enjoyed historic sales numbers in China over the past two years (Figure 1). In general, these companies have referred to China’s massive investments in legacy capacity to explain the surge. China is set to add more legacy node capacity than the rest of the world combined over the next few years (see our notes, Thin Ice: US Pathways to Regulation China-Sourced Legacy Chips and Running on Ice: China’s Chipmakers in a Post October 7 World.)

But China’s legacy capacity buildout is only part of the story. Chinese fabs with leading-edge aspirations have also exploited various loopholes in the rules to stockpile the most advanced tools they can get their hands on. Chinese customs data offers valuable insight into this trend. As reflected in Figure 2, the average prices of China’s SME imports in several key chokepoint technology segments have risen sharply since the US chip controls were first implemented in October 2022. While unit price inflation has played a role in this trend, it can only account for a small portion of the overall increase. For example, the global average price of non-EUV ASML lithography systems increased by roughly 20% between Q1 2022 and Q1 2024.2 However, the average price of lithography systems imported to China rose by more than 200% during the same period.

The predominant factor behind the explosive rise of average prices in chokepoint SME categories in China over the past two years has been a shift in product mix toward higher-value—and hence more advanced—systems rather than general price increases. This trend hit an apex in the second half of 2023 before leveling off over the course of 2024, indicating that new, harmonized restrictions on high-end SME announced by the US, Netherlands, and Japan in late 2023 may have at least partially disrupted Chinese access to covered tools.

Notably, this trend has been particularly pronounced in the major hubs of Huawei’s advanced chip development effort—and consequently, the targets of the new BIS FN5 FDP designations: Shanghai, which is home to SMIC’s advanced 7nm logic production lines, and Shenzhen, Guangdong, where Huawei is working to establish a complete supply chain for advanced logic and memory chips via a network of fab partners, including PenXinWei Semiconductor (PXW, logic), Pengxingxu Technology (PXX, logic), and SwaySure Technology (DRAM).

BIS targets this emerging network of advanced chip suppliers with particularly stringent restrictions in the new entity list regulations. Each of the sixteen entities designated with FN5 is working in close cooperation with Huawei to propel Beijing’s advanced chip indigenization objectives. Those additions include several SMIC subsidiaries and other Huawei-connected fab partners, as well as national IC research centers like the Shanghai Integrated Circuit Research and Development Center (ICRD), a leading-edge research lab that is working closely with Huawei to promote China’s advanced chip capabilities across a range of areas, including EUV and other next-generation lithography technologies.

With these FN5 designations, BIS is attempting to throttle these firms’ access to foreign SME, and related components and spare parts, for advanced node chipmaking. The new SME FDP provision also addresses concerns that US SME suppliers have managed to evade BIS jurisdiction by establishing foreign-based subsidiaries led by non-US person decision-makers in Southeast Asian countries like Singapore and Malaysia to continue selling covered equipment to Chinese fabs engaged in advanced node production. Specifically, the SME FDP extends BIS jurisdiction over the export of certain high-end equipment, components, and related software and technology to all foreign jurisdictions that do not currently have equivalent export controls on the books.

BIS also included a provision aimed at closing loopholes that have allowed Huawei-SMIC and other advanced chip developers in China to stockpile SME for advanced node capacity by placing fab facilities nominally focused on legacy node production in immediate proximity to advanced node production facilities and connecting them via a so-called “wafer bridge.” Red Flag 27 in the new rules explicitly addresses this problem by imposing a new end-user verification requirement to ensure that companies do not conduct any covered transactions with a facility that is “physically connected to a ‘facility’ where ‘production’ of ‘advanced-node ICs’ occurs.” If foreign suppliers cannot meet the due diligence requirements to verify tools are not going to restricted end users, this can have a chilling effect on their transactions with Chinese entities.

The new regulations also send a shot across the bow of China’s emerging upstream semiconductor ecosystem with a raft of new entity listings covering nearly every major Chinese supplier of SME, components, and materials, as well as its most prominent electronic design automated (EDA) software developer outside of Huawei, Empyrean Technology.

These entity listings only apply licensing requirements to the sale of any items listed in the EAR to covered entities from US suppliers. Upstream suppliers in China have been diligently working to minimize their supply chain exposure to the US while stockpiling necessary components for years now, so losing access to US suppliers is unlikely to significantly constrain their development trajectory. It remains to be seen to what extent non-US suppliers will continue selling to US entity-listed SME companies in China when there is lingering concern that those companies could fall under an FN5 FDP designation if they are caught in the Huawei-SMIC nexus.

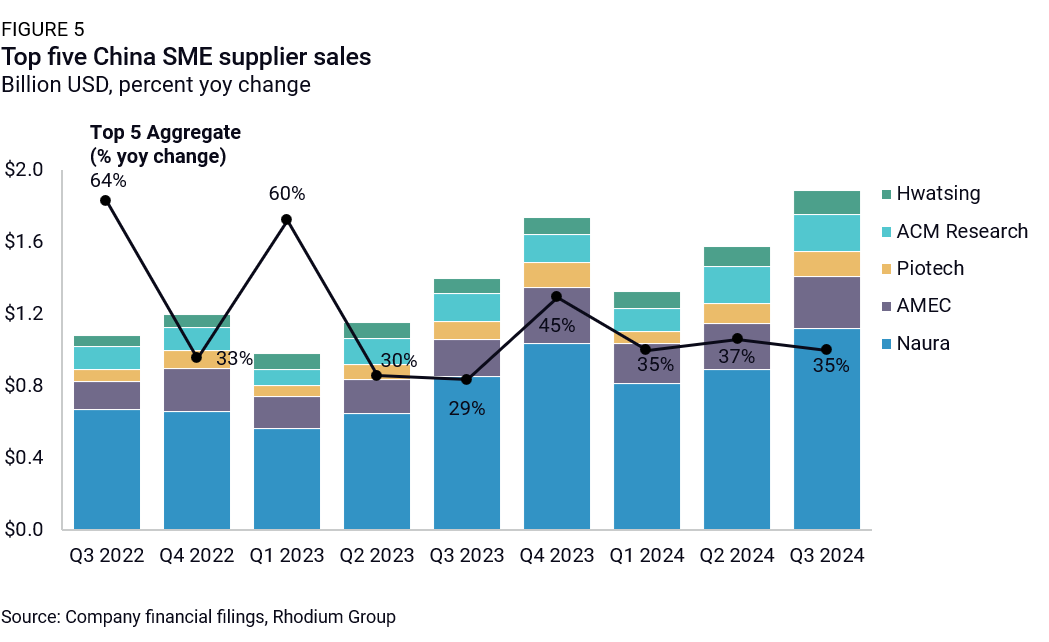

The near comprehensive entity listing of China’s emerging upstream semiconductor supply chain reflects a growing concern within BIS regarding the recent progress of China’s upstream supply chain development. While Western suppliers have reaped the lion’s share of the revenue from China’s chip capacity expansion over the past two years, China’s domestic suppliers have also enjoyed unprecedented growth. The aggregate sales growth of China’s five largest public front-end SME producers has risen at an annualized rate of 30% or greater in each of the past nine quarters (Figure 5).

Nearly every prominent front-end SME supplier in China is now on the US Entity List, with the exception of AMEC, which was removed from the Verified End-User list at its own request but has not (yet) been added to the Entity List. Naura Technology is the most noteworthy name on the list. The Beijing-based company has surpassed one billion dollars in revenue in two of the past four quarters and is developing a diversified product portfolio that covers a range of critical SME categories, from physical and chemical vapor deposition to etch and wafer cleaning.

While Naura and AMEC have made notable strides in certain categories of deposition and etching tools, even these relatively advanced companies remain significantly behind the cutting edge in their covered product segments. Meanwhile, China’s leading players in segments critical for advanced node fabrication, like inspection and metrology (Skyverse, Jingce Electron, Raintree Scientific Instruments) and ion implantation (Shanghai Wanye), are only in the very early stages of development. As a result, the US SME FDP rule, which applies US extraterritorial reach to cover components, software, and other technology required for the production of certain advanced SME, will have little direct impact on these firms in the near term. However, their association with the entity list may have a chilling effect on the willingness of foreign suppliers to transact with them more broadly. The US also routinely ratchets the intensity of entity listing restrictions retroactively, so addition to the list carries longer-term risks of a harsher crackdown in the future.

China raises the retaliatory stakes

Beijing’s retaliatory strikes to the escalation in chip controls have been swift. Less than 24 hours after BIS issued the December 2 chip rules, China’s Ministry of Commerce issued a wave of export controls harnessing its leverage in critical minerals used in production for semiconductors and the defense industrial base. Within a week of the BIS controls, China’s anti-monopoly arm announced a probe into a four-year old NVIDIA acquisition.

The biggest constraint to Beijing’s retaliatory calculation is its continued reliance on foreign investment and exports for economic growth and the potential for serious backlash to economic coercion. However, MNCs are going to be pulled between tightening US controls aimed at China’s tech self-reliance campaign and Beijing’s offers of incentives to companies in some tech segments willing to double down on their Made in China strategy.

Critical mineral curbs

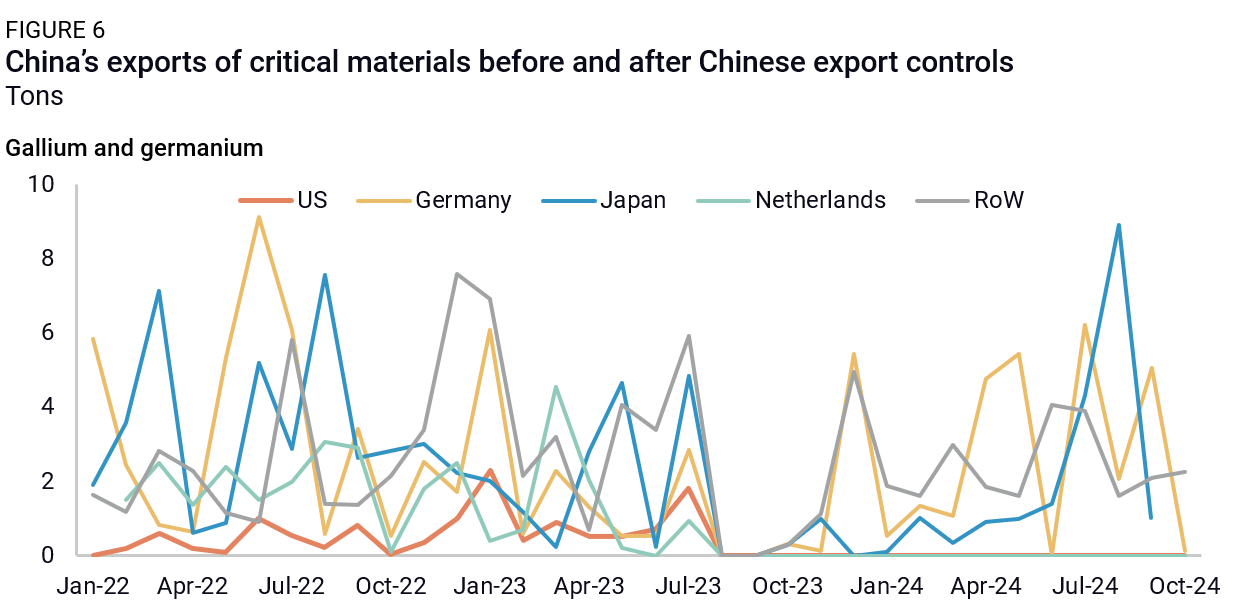

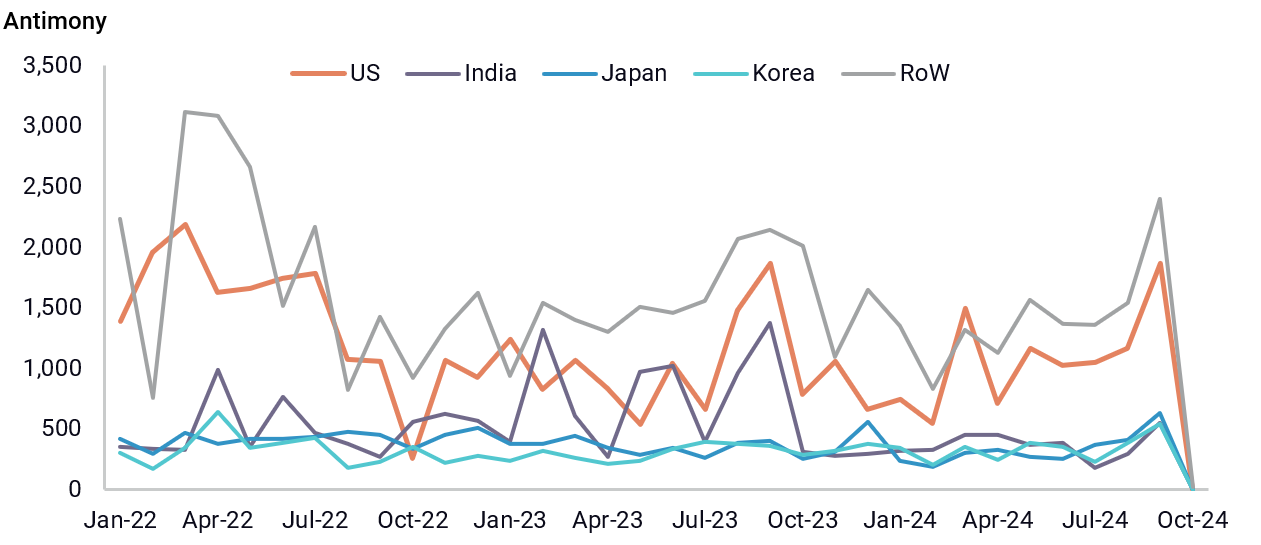

Targeting the US exclusively, MOFCOM prohibited the export of gallium, germanium, antimony, and superhard materials and subjected graphite to stricter reviews of end-uses. China had already been selectively restricting gallium and germanium exports to the US (and the Netherlands) since controls went into effect in August 2023. Antimony exports from China cratered when controls came into effect on September 15. Beijing stopped short of an outright ban on graphite (critical for EV battery production), but it announced stricter end-user reviews for graphite exports to the US. This may be meant to signal to the US that China can dial up the restrictions if pushed harder on tech and trade controls.

The critical mineral curbs follow a series of recent steps by MOFCOM preparing for this very moment: consolidating existing controls into a single Dual-Use List, assigning export control classification numbers, and, most notably, introducing provisions that mirror US extraterritorial provisions. For example, MOFCOM has introduced de minimis and FDP-like authorities that stretch Chinese export control jurisdiction over foreign-made items containing “specific amounts” of Chinese-origin content or “produced with China-origin technologies.” It created a Watch List, similar to the US Unverified List, which would imply MOFCOM officials getting access to on-site inspections of US and partner firms (a high bar). China’s export control law also enables special “country” or region groupings based on risk levels (akin to the US Country Group A:5 for trustworthy versus D:5 for untrustworthy countries in the US Export Administration Regulations).

The measures are also meant to telegraph three things to US partners (i.e., Japan, the Netherlands, and other foreign equipment suppliers now caught in US long-arm measures). First, alignment with the US on tech controls could result in similar restrictions. Second, attempts to circumvent China’s export controls on the US by re-routing trade could mean that circumvention countries could be added to a list of untrustworthy countries subject to tighter restrictions. Third, Beijing will assert its jurisdiction over final goods produced in third countries that contain controlled materials imported from China.

This sounds potent in theory, but in practice, there is a giant question mark confronting Beijing’s ability and willingness to assert this kind of long-arm jurisdiction. MOFCOM officials simply don’t have the same sway outside China as BIS regulators do with partner countries around the world. Attempts to conduct on-site inspections of US and partner firms abroad would lead to confrontation with host governments who could simply reject the visas of Chinese regulators on the grounds that such moves amount to economic coercion and retaliation.

While China cannot match the US on high-tech IP, which is difficult to displace, it does have significant leverage in critical mineral production. Critical raw material production is not as capital- and IP-intensive as high-end technological development, but the US and its partners face the tyranny of time in trying to rapidly diversify to non-China production. Beijing is signaling that it is willing to put the US and partner countries in a critical supply chain lurch if pushed too far.

Western firms operating in China are the most exposed in this new phase of Chinese retaliation. They face an elevated risk of on-site inspections, investigations, fines, and product bans as Beijing tries to assert its export control authority. They also face the potential of cybersecurity, data security, and other national security measures that could be selectively employed to punish targeted firms. Companies that face credible Chinese competition—or whose sales to China are increasingly restricted by US measures anyway—are the most vulnerable, with China trying to make room for indigenous firms to grow market share.

To this end, on December 5, China’s Ministry of Finance announced new draft standards for government procurement, with the dual purpose of boosting the competitiveness of indigenously made products like chips and incentivizing MNCs to deepen their footprint in China. They are doing this by offering preferential treatment in government procurement for both domestic and foreign players on the condition that a (still-unspecified) amount of key components of final products are also made in China.

Making an example of NVIDIA?

The Chinese government is also brandishing sticks. On December 9, China’s anti-monopoly agency, the State Administration for Market Regulation (SAMR), announced an investigation into NVIDIA for a deal it initially approved four years ago. At issue is NVIDIA’s possible violation of China’s Anti-Monopoly Law and the remedy commitments it entered into as part of its acquisition of Israel-based Mellanox Technologies Ltd. (a manufacturer of network interconnection products) in 2020. The move can be viewed as another step in China’s retaliation to chip controls, sending a striking message to companies in China: Comply with US export controls and you will be punished in China. According to China’s Anti-Monopoly Law, “particularly heinous violations” can result in fines of up to 50% of firms’ revenue from the previous year—which would amount to as much as $13.5 billion for NVIDIA. SAMR could also attempt to impose new conditions on NVIDIA-Mellanox in a retroactive review. But again, we question China’s political will to credibly enforce these threats.

First, China is still dependent on NVIDIA chips. NVIDIA’s exposure to China is concentrated in the sale of graphics processing units (GPUs) that fall below the threshold of BIS controls. Though Huawei is trying to displace NVIDIA’s market share in China as the “trustworthy” domestic source of Ascend AI processors, it is still in the early stages of this endeavor. Although NVIDIA is prohibited from selling its most advanced GPUs in China, the market accounts for 15% of its revenue through large volumes of BIS threshold-compliant H20 chips. NVIDIA was the largest supplier of AI chips to China in 2024, with most estimates pegging its total sales volume at around one million units. Meanwhile, despite notable breakthroughs, Huawei is rumored to be struggling to fulfill its contracts for high-profile customers like Baidu and faces the prospect of tighter BIS controls constraining SMIC’s production of high-end chips. If Beijing wants to keep pace with the US in AI competition, it does not have the luxury of self-restricting NVIDIA chip sales at this stage.

Second, making an example of NVIDIA with a punitive fine in a bid to strengthen industry lobbying and restrain US tech controls could backfire significantly. In fact, such a move could drive US policy to use more unconventional tactics to challenge China’s enforcement credibility. For example, if NVIDIA does not pay a fine handed down by SAMR and the US challenges the legality of such a fine by simply not recognizing the claim, would Beijing find other ways to retaliate? Lighter fines could be coupled with restrictive measures related to China’s self-reliance targets or cybersecurity law, but substantive retaliation against a US AI tech champion will likely only further animate the US tech controls agenda under the Trump administration.

On our watch list

The December 2 chip rules represent another high-stakes bet by the Biden administration with less than seven weeks to go until the transition to Trump. From a US mission statement more than two years ago to build as wide a lead as possible over China in force-multiplying technologies, to the series of punchy chip controls that followed, and the mixed results of that policy now nagging at the current US administration, the urgency to patch controls with partners is palpable.

The following questions will be vital to interrogate in the wake of these rules:

- Will key SME-producing partners follow through with harmonized controls? We are watching for the Netherlands and Japan to tighten up licensing and expand the scope of their controls, but this may be done quietly to try and manage the escalation with China. Germany is our biggest question mark. German firms Trumpf (a critical supplier of laser systems for advanced lithography machines) and Zeiss (high precision optics for advanced lithography) are highly relevant SME players. Germany falls on the partner carveout list, but the rule assumes that Germany, like Japan and the Netherlands, will impose equivalent controls. However, the German government is in flux, with elections slated for Feb. 23, and there is no guarantee Berlin will play ball—Beijing is ratcheting up retaliatory threats and Germany expects to be a prime trade target for Trump. If Germany does not comply, BIS could update the rule with a revised carveout list, subjecting Germany to FDP restrictions. Meanwhile, the governments of South Korea (also in political flux) and Singapore are already under FDP restrictions unless they, too, impose equivalent controls. They can either quietly comply with the US rules or adjust their export controls to regain licensing sovereignty.

- How hard will China punch back? China retaliated swiftly in an effort to dissuade partners from harmonizing with US controls. If China’s gambit pays off, it could portend a bigger confrontation ahead between the US (under Trump) and trading partners like Germany already under the Trump microscope. Alternatively, partners may be willing to stomach some degree of Chinese retaliation if they assume China lacks the political will to enforce export controls, especially when Beijing wants to leverage Trump tensions to fracture US partners and when China still needs export markets and investment for growth. Moreover, Beijing may lack the capability to enforce long-arm export controls outside China. As the stakes rise, we will be watching whether China’s regulations, including country-wide controls and discrimination against foreign MNCs, increasingly delineate between friendly and unfriendly trading partners linked to the US.

- Trump has a loaded weapon on tech controls. Will he use it? We still do not know the full makeup of the BIS and NSC teams under Trump, but we question whether Trump’s team will put the same resources into Commerce BIS to devise such intricate and technically complex rules. If not, will the US fall behind in keeping on top of China’s evolving SME ecosystem to identify new targets? With FDP and de minimis rules loaded, the Trump team has inherited immense extraterritorial leverage to ratchet up FN5 entity listings and revoke carveouts for partners if their controls do not meet US demands on stringency. We expect the Trump administration will be less willing to cede licensing sovereignty to partners via negotiations over equivalent controls, as the Biden administration has done more recently.

- Will the rules slow China’s tech indigenization or accelerate it further? The BIS rules, in concert with partner harmonization, aim to cut off foreign SME suppliers from selling into the Chinese market. This will infuse even more urgency and resources into China’s self-reliance campaign. We will specifically be watching for Huawei’s ability (or lack thereof) to maintain its current pace of production for high-end Ascend chips now that it has been cut off from foreign HBM supply. Notably, Chinese SME firm AMEC requested to be removed from the US Verified End User list, which implies it may be confident enough in its indigenous capabilities to avoid subjecting itself to US inspections. We are also monitoring the pace of AI development in China, where innovative foundation model developers like DeepSeekAI, Alibaba, and others have thus far managed to scrape together enough high-end compute power to stay within striking distance of their GPU-rich Western rivals. BIS is betting that this is just a temporary state of affairs—as the West continues to push state-of-the-art AI accelerators forward, the gap between US and Chinese AI developers will inevitably expand. Will China’s AI development community manage to continue climbing the innovation curve just a couple steps behind the US? Or will the impact of US-partner export controls combined with the substantial increase in compute power enabled by NVIDIA’s Blackwell platform begin to widen the US lead over China in AI development by an appreciable degree?

- Will China try to scale in AI compute? Struggling under tighter export controls, Beijing could lead a state-led emergency push to centralize and scale its AI compute resources in an effort to keep pace with the US. The big problem with this centralized approach is that it only makes the Chinese entities bigger targets, and the company leading China’s AI chip development—Huawei—is already the most heavily sanctioned Chinese firm. Any linkage to the Huawei-SMIC nexus will create a wider target set for the US to deploy FN5 FDP.

- Will SME companies rebalance toward US-driven AI demand? Foreign SME suppliers riding the China stockpiling wave will face a reckoning. Will their revenues return to their pre-stockpiling baseline, and will these companies be able to compensate for lost China growth with increasing demand for high-value cutting-edge chipmaking tools to power AI expansion in the US and partner countries?

- Other chip controls still pending? We will be watching for potential eleventh-hour tech controls by the Biden administration. For example, the rule mentions an additional forthcoming rule to address industry comments on SME measures. This could range from mild technical clarifications to beefed-up due diligence requirements on foreign fabs, additional entity listings (CXMT, AMEC, and Huahong in focus), or even adjustments to licensing carveouts if partners don’t follow through with commitments to harmonize controls. Further out, we need to watch for potential measures on China’s legacy chip production under the Trump administration. If Chinese chipmakers face bigger hurdles in maintaining advanced node production in the wake of these rules, will we see more state resources, including Big Fund allocations, flood toward trailing edge production where Chinese chipmakers can operate under relatively fewer constraints? And will that be the trigger for US-led cybersecurity/ICT controls and component tariffs for China-sourced chips under Trump?

Footnotes

BIS restricts the export of any HBM that has a ‘memory bandwidth density’ greater than 2 GB per second per mm2

China accounted for roughly 90% of ASML’s non-EUV lithography system sales in Q1 2024, so even if the supply constraints imposed by export controls caused prices to rise disproportionately in China relative to other jurisdictions, that price premium could only account for a relatively small share of the overall price increase for lithography imports to China.