Clean Investment Monitor: US Q3 2024 Update

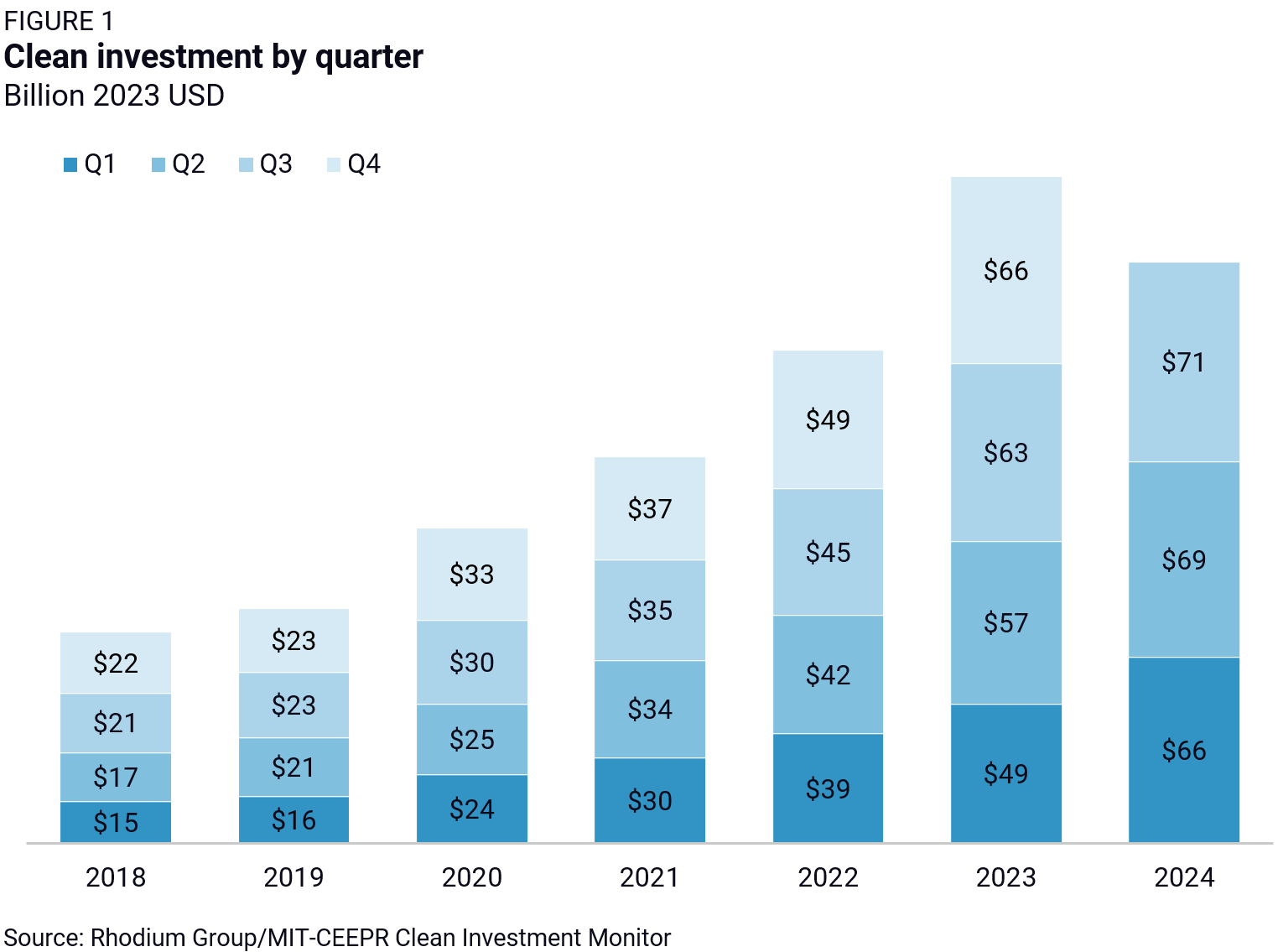

Clean energy and transportation investment in the United States continued its record-setting growth in Q3 of 2024, reaching a new high of $71 billion.

Clean energy and transportation investment in the United States continued its record-setting growth in Q3 of 2024, reaching a new high of $71 billion. This continues a nearly unbroken quarter-on-quarter growth trend over the past three years, and marks a 12% increase in Q3 of 2024 from the same period in 2023. Clean investment accounted for 5% of total US private investment in structures, equipment, and durable consumer goods in the United States, compared to 4.5% in Q3 2023.

Retail investment grew by 9% relative to the previous quarter, acting as the main driver of clean investment growth. This quarterly increase was due to a surge in zero-emission vehicle (ZEV) sales in Q3. Investment in clean technology manufacturing was flat quarter-on-quarter—declines in solar manufacturing investment offset small increases in battery and ZEV manufacturing investment—but up 57% from the same period last year. Investment in deploying technology to decarbonize energy and industrial production slipped 7% quarter-on-quarter, the third quarter of decline, and is now down 6% compared to Q3 2023. Investment in the deployment of emerging climate technologies (ECT) like clean hydrogen, carbon management, and sustainable aviation fuels increased by 4% from the previous quarter but slipped by 6% relative to the same period last year.

Using the Clean Investment Monitor database, we assessed the progress of the US clean electricity transition and found that the current pace of capacity expansion is falling short of what is needed to deliver a 40% reduction in net GHG emissions below 2005 levels by 2030—a target that the Inflation Reduction Act (IRA) was projected to achieve at the time of its enactment. Our latest analysis of projects in the pipeline shows that both solar and wind are underperforming, aligning more closely with a scenario that would yield only a 30% emissions reduction by 2030.

This quarter’s report includes several updates to our methodology that expand the scope of technologies covered and affect the magnitude of our findings. On the technology front, we have broadened our clean industry tracking to include approaches to decarbonizing the production of cement, iron and steel, and pulp and paper. This addition provides a more comprehensive view of advancements in industrial emissions reduction. We have also refined our inflation adjustment process, now tracking price changes with greater specificity to improve the accuracy of our cost assessments over time. Finally, we have dialed up our attention to the construction status and progress of tracked facilities, conservatively assuming a facility advances through construction stages only when we can identify evidence of a groundbreaking. Facility timelines are adjusted accordingly, with start dates pushed back if groundbreaking evidence is lacking. These updates have lowered our actual investment estimates for this quarter and previous quarters.