Report

U.S. Perspectives on the Osaka APEC Summit

A proprietary report by Gary Hufbauer and Daniel H. Rosen. Prepared for the Harvard Institute for International Development (HIID), August 1995.

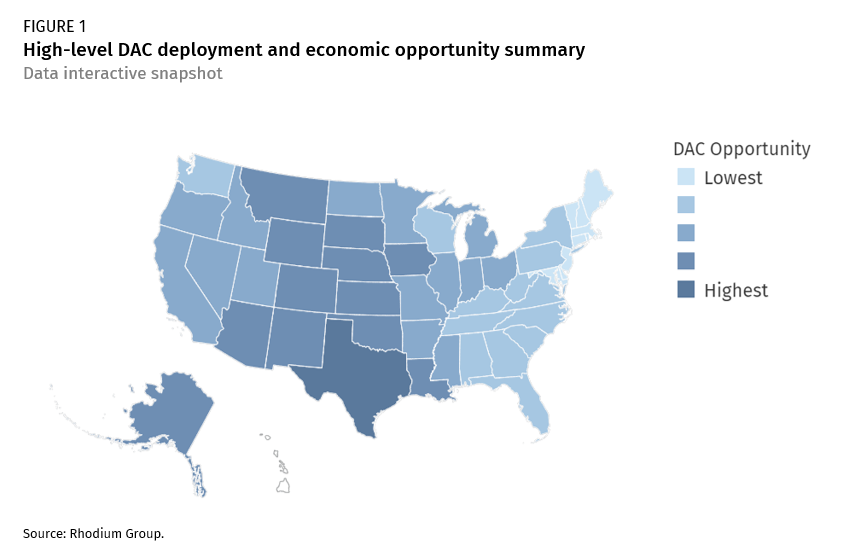

In a data dashboard, we take a look at what the potential for direct air capture industry scale-up means for individual states and how they might benefit.

In 2019, Rhodium Group released Capturing Leadership: Policies for the US to Advance Direct Air Capture Technologies which assessed national direct air capture (DAC) levels needed to achieve deep emissions reductions by mid-century in the US and the corresponding federal policies that could support a DAC industry scale-up. Since then, a wave of federal policy support has been enacted to support direct air capture (DAC), including a tax credit of up to $180 per ton of carbon dioxide removed and stored under section 45Q of the tax code and $3.5 billion in funding to support regional direct air capture hubs, a program designed to support companies that are ready to build large demonstration projects and move into early-commercialization. In our annual outlook on US emissions projections, Taking Stock, last year we projected current policy support could deploy up to 84 MMT/yr of direct air capture capacity in the US by 2035, and we anticipate a much larger deployment opportunity by mid-century.

In this analysis, we take a look at what the potential for DAC industry scale-up means for individual states and how they might benefit (Figure 1). We look at the potential to deploy direct air capture capacity at the state-level in the near-term, by 2035, by disaggregating the national-level deployment we find under current policy to the state-level. We also look at how that opportunity expands if the US fully decarbonizes by mid-century (2050), assuming national DAC deployment levels we projected in Capturing Leadership. In our detailed state-by-state data interactive, we show the capital investment in each state as well as the job development benefits from building and operating DAC facilities, including a breakdown by occupation type.

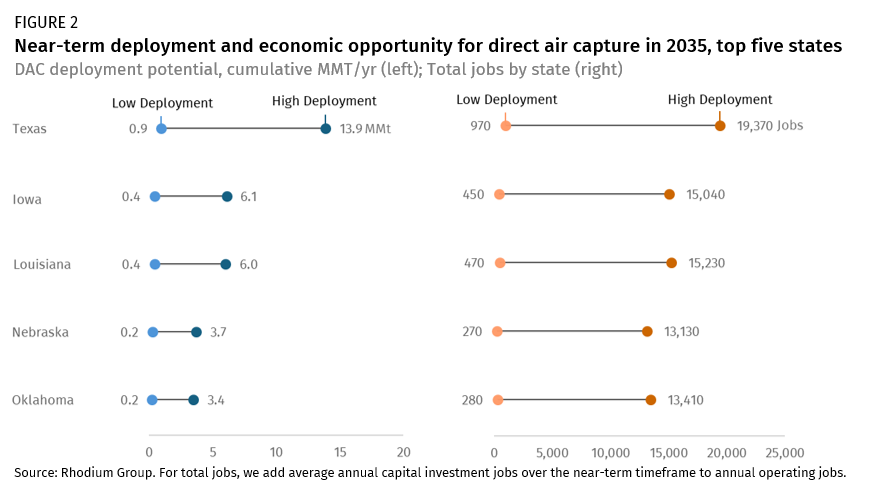

We find that in the near-term, nearly all states have potential to deploy at least one direct air capture facility, and we summarize the top five states with near-term deployment and job development opportunities for DAC in Figure 2.

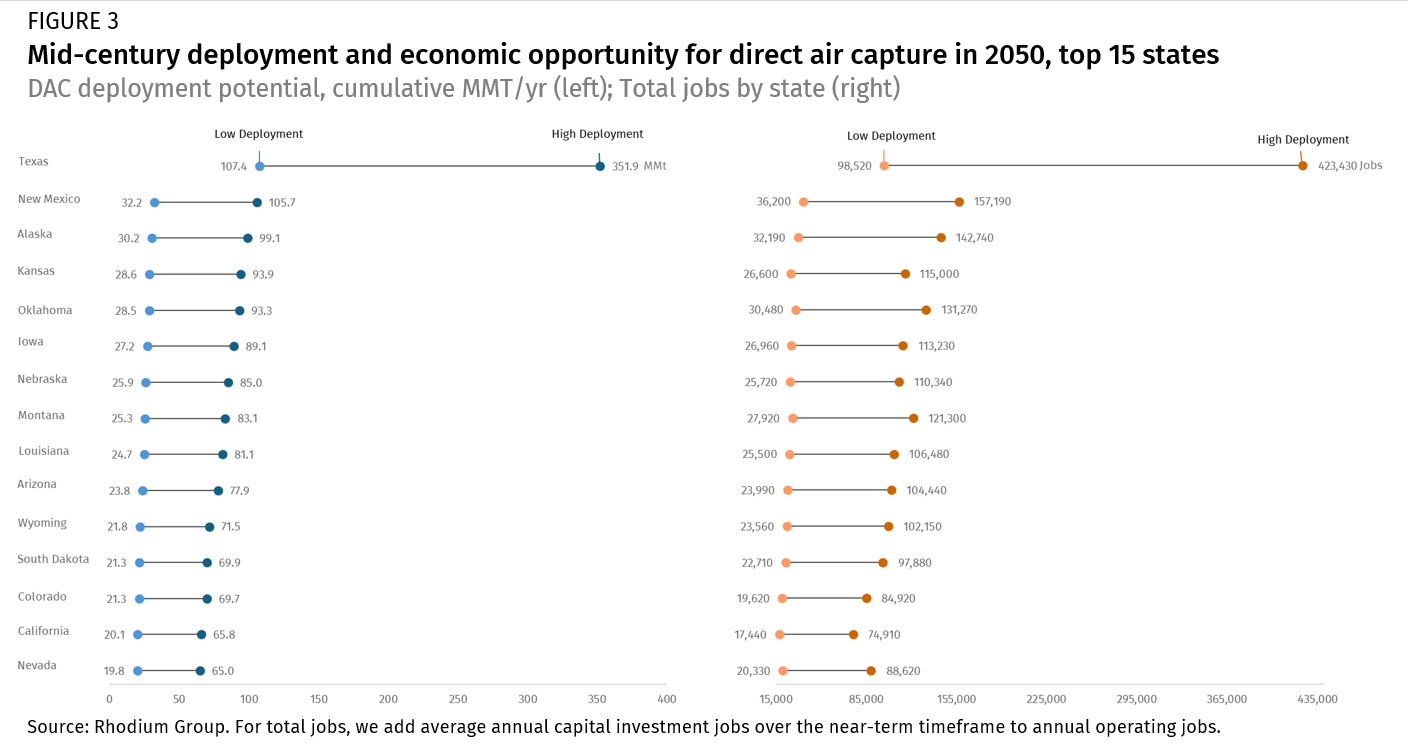

By mid-century, we find substantial opportunity for DAC deployment and the associated economic opportunity across almost all states. Figure 3 summarizes this opportunity for the top 15 states. Notably, Texas has a very large direct air capture industry and economic opportunity because of its large land area and substantial low-carbon energy and storage resource potential.

Report

A proprietary report by Gary Hufbauer and Daniel H. Rosen. Prepared for the Harvard Institute for International Development (HIID), August 1995.

Report

Daniel Rosen is a co-author of this working paper on China's economic reforms along with Gautam Jaggi, Mary Rundle, and Yuichi Takahashi.

Report

A proprietary report by Edward M. Graham and Daniel H. Rosen. Prepared for the Board of Foreign Trade, Taipei, July 1997.

Report

A proprietary report by Daniel H. Rosen, Catherine L. Mann and Sue Eckert. Prepared for the Board of Foreign Trade, Taipei, January 2000.