Direct Air Capture Workforce Development: Opportunities by Occupation

Direct air capture has the potential to play a pivotal role in meeting long-term US decarbonization targets. To achieve scale, the emerging industry will require a large, well-trained workforce.

Direct air capture (DAC), a carbon dioxide removal solution that captures carbon dioxide directly from the atmosphere, has the potential to play a pivotal role in meeting the US goal of net-zero greenhouse gas emissions by 2050. Alongside the scale-up of clean electricity generation, electrification of end-uses, and other emissions abatement strategies, DAC could be a complementary technology that allows for emissions offsets from hard-to-abate sectors, and that can remove emissions that already exist in the atmosphere. Over the past few years, the Energy Act of 2020, the Infrastructure Investment and Jobs Act (IIJA), and the Inflation Reduction Act (IRA) have ushered in a wave of DAC policy support in the United States. Last month, the Department of Energy announced DAC hub funding (a program incentivized by IIJA) to support the development of two commercial-scale DAC facilities and 19 early-stage projects across the US.

Assuming this momentum continues and policy support is extended long-term, DAC deployment at scale will require a large, well-trained workforce to build and operate DAC facilities. In this note, we assess the job creation and workforce development benefits associated with a commercial-scale DAC facility. We find that the construction and engineering of a DAC plant creates 1,215 annual average jobs over the roughly five-year time period it takes to build the facility. After the plant is built, we estimate there are approximately 340 jobs needed to operate the facility over its lifetime. We also dig into the types of occupations that will benefit from DAC scale-up and find that the industry will support a diverse set of construction trades, maintenance workers, and business operators.

Scaling the direct air capture industry

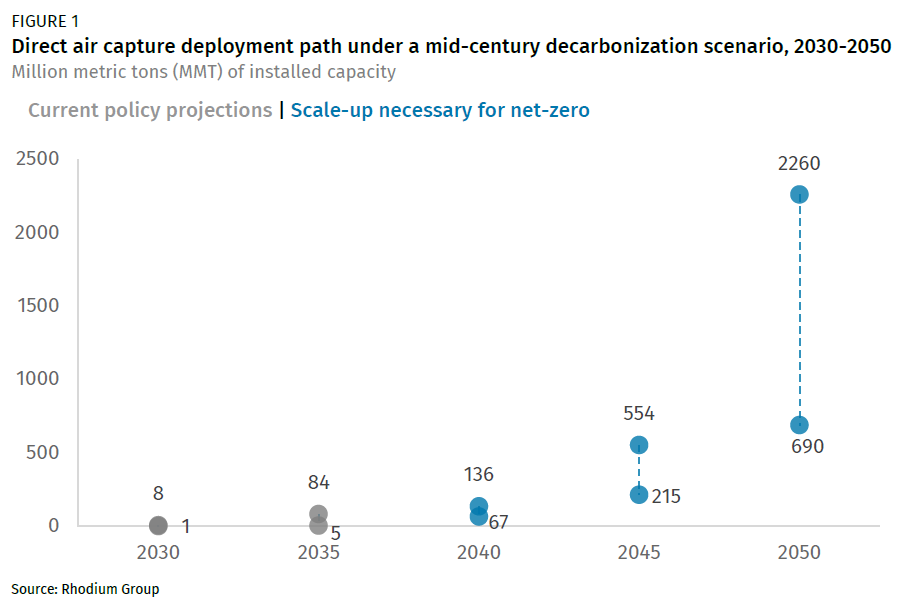

Direct air capture (DAC) is a technology similar to traditional carbon capture that captures carbon dioxide (CO2) from ambient air instead of an industrial or electric power flue gas stream. Because ambient air concentrations of CO2 are much more dilute than flue gas, the costs tend to be higher for DAC than traditional carbon capture. That said, unlike traditional carbon capture, the main utility of DAC is that it results in net-removal of CO2 from the atmosphere—not just abatement like traditional carbon capture. In a 2019 Rhodium report on advancing direct air capture, we estimate that the US needs to scale up to between 690 and 2,260 million metric tons (MMT) of annual DAC capacity in order to decarbonize the US by 2050 (Figure 1). The range of DAC capacity needed represents how quickly we can scale other decarbonization strategies such as energy efficiency, electrification, decarbonization of the electric power system, and the availability of other carbon dioxide removal (CDR) systems. The slower other decarbonization strategies are in scaling up, the more DAC the US will need to meet its goal of net-zero emissions by 2050.

Since we released our 2019 report, unprecedented policy support along with a surge in DAC investment has fundamentally changed the landscape for DAC. For example, as part of their pledge to invest one billion dollars in CDR, Microsoft has purchased carbon removal from three major DAC companies thus far—Climeworks, Heirloom, and CarbonCapture. Most recently, the Department of Energy (DOE) announced funding site selections for two major commercial-scale DAC hubs—one in Texas and the other in Louisiana—that will together have the capability to remove at least two million metric tons of CO2 once fully operational. In addition to these plants, 19 other potential DAC sites across the US were selected to receive DOE funding that assists with early-stage project development. In total, the Infrastructure Investment and Jobs Act (IIJA) passed in 2021 provides roughly $3.5 billion for four commercial-scale regional DAC hubs, $100 million for a commercial DAC prize, and another $4 million for a pre-commercial DAC prize. In addition, the 45Q tax credit enhancement in the Inflation Reduction Act (IRA), passed last year, allows DAC developers to receive $180 per ton of CO2 sequestered. Both pieces of legislation include elements that help to boost DAC deployment and build out supporting infrastructure like geologic storage and CO2 transportation pipelines. It’s also worth noting that the Energy Act of 2020 reorganized the Office of Fossil Energy at DOE to be inclusive of carbon management technologies and, subsequently, set up the first CDR research and development (R&D) program.

In the near term, this policy support creates the economic conditions necessary to establish a true market for DAC. We estimate that in total, these policies will drive 1 to 8 MMT of DAC capacity deployment in 2030 and 5 to 84 MMT of deployment by 2035 (Figure 1). These ranges represent the speed at which the supporting industries such as construction, engineering and manufacturing can scale to support the DAC industry as well as uncertainty surrounding regulatory and permitting reform. Though this is momentous for an industry that was hardly heard of five years ago, the direct air capture industry still has a long way to go to achieve gigaton scale by mid-century. Ultimately, longer-term policy support, private investment, and workforce development will be needed. As a starting point, we explore the opportunities for workforce development from scaling up the DAC industry.

Direct air capture workforce opportunities

Large-scale deployment of DAC has the potential to generate significant economic and employment opportunities in the communities where plants are sited and in the industries that support DAC construction and operation. For this analysis, we evaluated a range of DAC technological processes assuming they are at commercial scale. The results provided below reflect the median values across all DAC processes. Because no large-scale commercial DAC plants exist today, there is no empirical employment data to use in this analysis. We have developed a methodology that proxies DAC employment based on adjacent industries. To do this, we determine the capital and operating costs of each process based on expert interviews, literature, and public announcements. Next, we conduct in-depth research on how the distribution of costs varies by process and input those costs into the appropriate industry associated with the input-output model IMPLAN. We produce occupational results from IMPLAN and supplement these outputs with Bureau of Labor Statistics data.

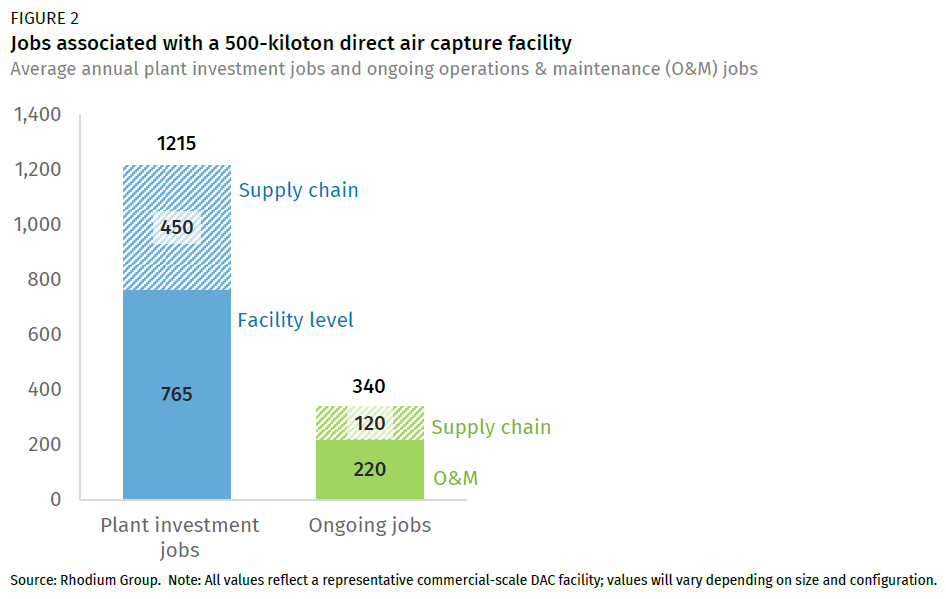

We estimate the total number of jobs created from the construction and operation of a single commercial DAC facility with an annual capture capacity of 500 kilotons (kt) because that will be the size of the first large-scale commercial DAC facility in the US. For reference, this is a plant size that captures emissions equivalent to about half those produced annually by an average-sized natural gas combined-cycle power plant.

We find that a commercial 500 kt DAC facility generates, on average, 1,215 plant investment jobs each year over the course of the facility’s five-year construction period (Figure 2). Plant investment refers to the jobs associated with construction, engineering, materials, and any equipment needed to build the DAC facility. 63% (765 jobs) of these jobs are considered facility-level jobs in that they are directly related to the construction of the DAC facility. All remaining plant investment jobs support supply chain activities like freight transport and equipment manufacturing.

Ongoing operations and maintenance (O&M) over the lifetime of the facility generates an additional 340 jobs, with roughly 65% (220 jobs) being on-site primarily maintaining the DAC equipment over the facility’s lifetime.

Direct air capture plant construction occupations

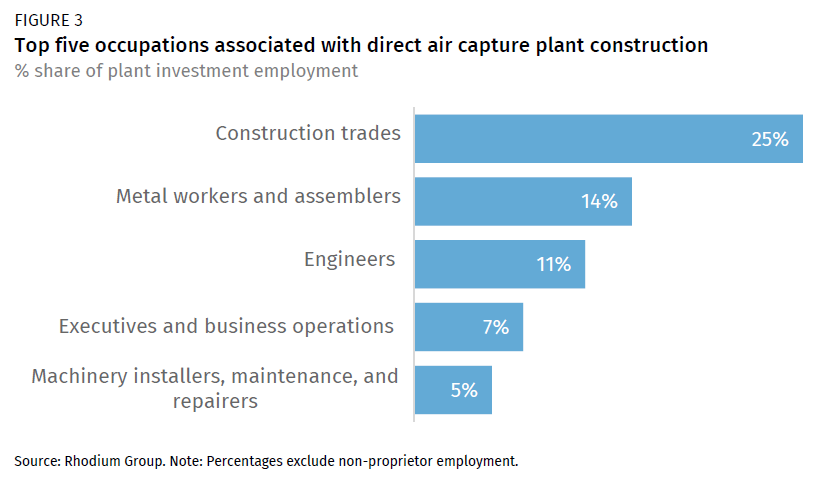

For the first time, we take a deeper dive into the types of jobs associated with the construction and operation of a commercial-scale DAC facility. We exclude occupational detail on supply chain jobs from this analysis. The top five occupational categories associated with the construction of a typical DAC facility are: (1) construction trades; (2) metal workers and assemblers; (3) engineers; (4) executives and business operations; and (5) machinery installers, maintenance, and repairers (Figure 3). Collectively, they account for roughly 63% of all non-proprietor employment associated with the facility’s construction. Non-proprietor employment refers to wage and salary workers—in other words, employees who are not owners.

Construction trades are the largest occupational category, followed by metal workers and assemblers, and engineers. Metal workers include welders, solderers, and machinists. Civil, mechanical, industrial, and electrical engineers, along with engineering technicians, make up the third largest group of occupations associated with building a DAC plant.

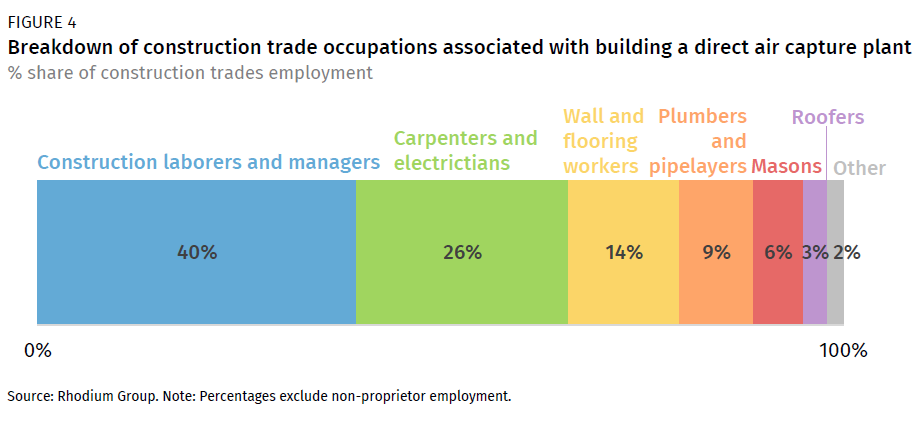

Since the construction trades represent such a diverse set of skills and they are responsible for a large subset of the DAC plant construction workforce, we’ve provided more detail for this particular occupation group (Figure 4). 40% of construction trade jobs required to build a DAC plant are either general laborers or managers. Carpenters and electricians account for 26% of construction trade jobs, and wall and flooring workers account for 14%. Plumbers, pipelayers, masons, and roofers account for the remaining construction trade labor associated with building a DAC plant.

Direct air capture plant operation occupations

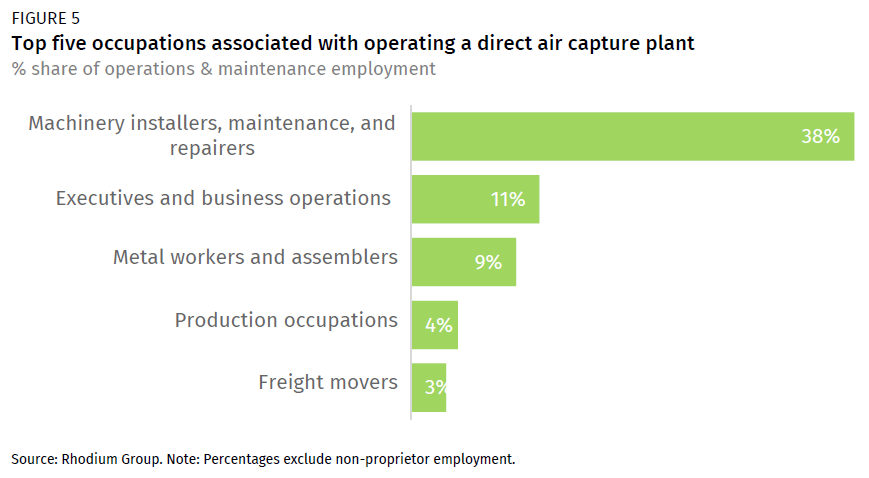

In the case of ongoing jobs associated with operations and maintenance of a DAC plant, the top occupations are machinery installers, maintenance and repairers, which includes industrial mechanics and industrial line supervisors. The next largest categories of occupations include executive and business operations occupations, metal workers and assemblers, production occupations and freight movers (Figure 5).

This first-of-its-kind occupational analysis provides insight into not only the total number of jobs but also the types of jobs created from the construction and operation of a commercial DAC facility. Given the current state of the industry, our occupational analysis should be seen as a first-order estimate, but we expect the overall takeaways to be the same as we continue to improve our analysis. As the DAC industry scales, we know that there will be a huge demand for a workforce to build and operate the plants. That workforce represents a diverse set of occupations that exist today. Even so, many of these occupations will require technical and extensive on-the-job training. To prepare for a scale-up of these emerging technologies, occupational training programs will be crucial. Planning will be key to make sure that the DAC workforce is abundantly available and trained in the locations where developers are looking to build DAC plants.

Forthcoming analysis

This analysis is in a three-part series assessing the workforce development opportunities from scaling up emerging climate technologies in the US. The first part, looking at the clean hydrogen industry, is available here, and our third part on the sustainable aviation fuel industry is forthcoming.

In addition, we plan to refine our approach and understanding of the DAC workforce as facilities get built and more experience and innovation on DAC technology occurs with scale-up. We will also continue to expand upon our employment analysis to investigate important factors including wages, union labor, and required skills. Additionally, later this year we will be releasing an analysis assessing opportunities for building up the DAC industry within individual states, including the associated economic and employment benefits. Finally, we are planning on a full employment analysis for the selected DAC hubs that we’ve discussed in this note.

This nonpartisan, independent research was conducted with support from Breakthrough Energy. The results presented reflect the views of the authors and not necessarily those of supporting organizations.