Sustainable Aviation Fuel Workforce Development: Opportunities by Occupation

We assess the workforce development and occupation opportunities from building up the sustainable aviation fuels industry.

Aviation is one of the fastest-growing emissions sources in the US, as well as one of the hardest to abate. With air travel demands unlikely to slow down, decarbonizing aviation will be critical in achieving a net-zero economy by mid-century. A leading solution for decarbonizing aviation is the use of sustainable aviation fuels (SAF) as a drop-in replacement for conventional jet fuel. Doing so can dramatically reduce life-cycle carbon dioxide emissions compared to conventional jet fuel. In recent years, we have witnessed growing US policy support and private investment to help expedite SAF commercialization and scale-up. However, scaling up the industry will require a robust workforce comprised of skilled laborers across a variety of occupations.

In this note, we assess the employment benefits associated with a commercial-scale SAF production facility—focusing on the total number of jobs created as well as the types of jobs created. We find that constructing and operating a commercial facility results in an annual average of 2,210 plant investment jobs and 1,440 ongoing jobs. It also leads to the employment of a wide range of professions including construction workers, engineers, farm laborers, and other agricultural workers.

Getting the sustainable aviation fuel industry to scale

The US aviation sector is the third largest source of US transportation emissions, accounting for approximately 7% of total emissions from the sector. It is also one of the fastest-growing sectors. Emissions are expected to increase as air travel and air freight transport demands continue to rise. Decarbonizing aviation is particularly difficult in large part due to commercial aircrafts operating, on average, 20 to 30 years. Considering this, if the US relied only on improvements in aircraft design and efficiency and/or the electrification of aircrafts, it would take a considerable amount of time to decarbonize the sector, not to mention that it is unclear if electric-powered airplanes will ever be able to service long-haul markets like existing commercial airliners. Instead, the most viable option for mid-century decarbonization could be the use of sustainable aviation fuels (SAF). SAF is a type of “drop-in” fuel produced from either biological or non-biological feedstocks. Being a drop-in fuel means that it can easily and safely be dropped into existing jet engines and fueling infrastructure in place of jet fuel. Compared to conventional jet fuel, SAF can reduce total life-cycle carbon dioxide (CO2) emissions by up to 100%, with some technology options for net-negative jet fuel. Its drop-in status and lower life-cycle carbon footprint suggest that its use in place of jet fuel can produce significant reductions in aviation emissions.

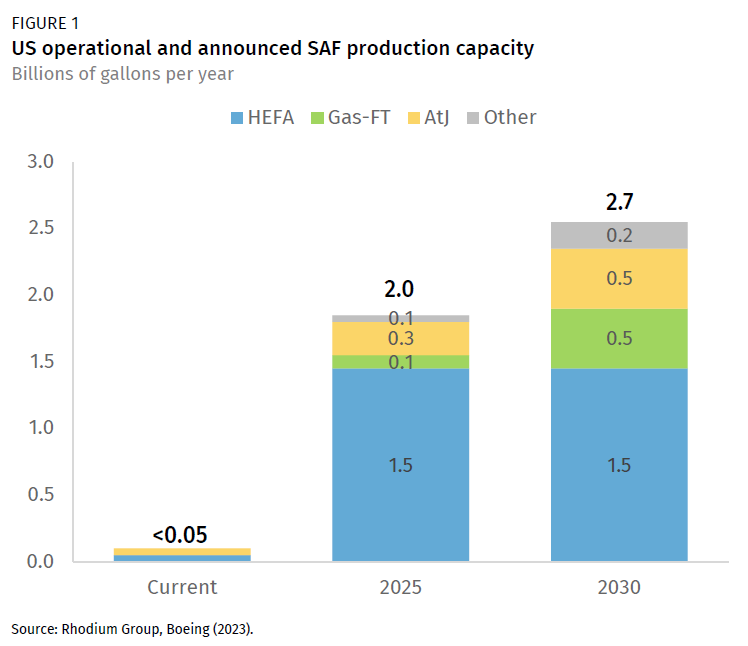

In recent years, several new SAF production facilities have been announced in the US. Total capacity is expected to reach 2.7 billion gallons per year (BGY) by 2030 (Figure 1). This would satisfy only about 7% of projected US 2030 jet fuel consumption. The hydroprocessed esters and fatty acids (HEFA) process is currently the only commercial SAF production pathway. However, the availability of sustainable feedstocks, and competition with other sectors for HEFA-based fuels, limit its use for aviation. Investment in other, less mature production pathways like bio-based synthesis gas Fischer-Tropsch (Gas-FT) and alcohol-to-jet (AtJ) will be needed if expanding SAF production capacity is to continue. We have chosen to focus on the AtJ pathway for this analysis given recent shifts in investment toward the commercialization of this technology.

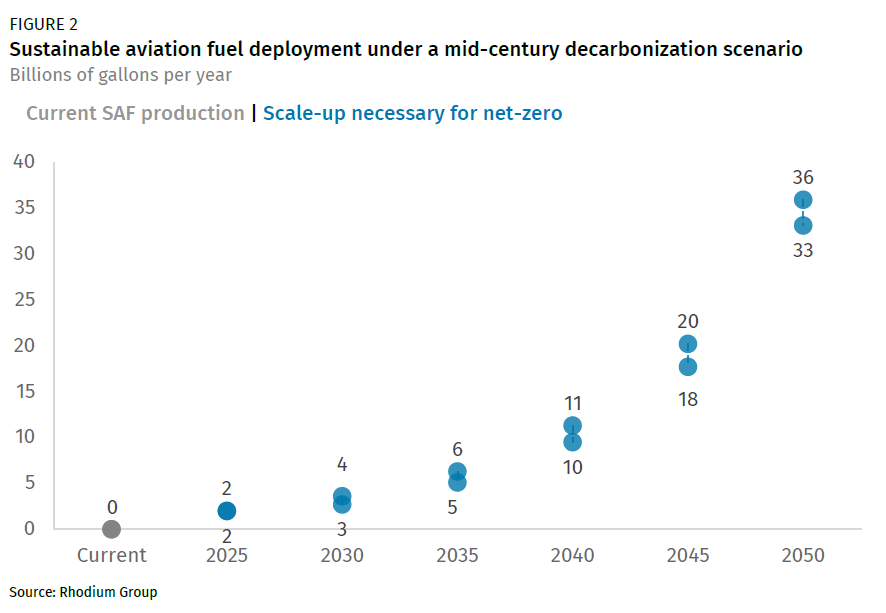

Production capacity levels in the US are far from being on track for what is needed to achieve mid-century decarbonization targets for aviation. If SAF is the predominant way to decarbonize, we estimate 33 to 36 billions of gallons per year will be needed to meet US aviation demand in a zero-emissions aviation sector (Figure 2). For SAF to scale exponentially, policy and private sector support needs to accelerate.

Here in the US, we are seeing more policy support and funding opportunities at both the federal and state levels to boost the nascent industry. Federal support includes: (1) new RD&D funding for SAF-related projects; (2) establishment of the SAF Grand Challenge; and (3) last year’s passage of the Inflation Reduction Act, which establishes SAF production tax credits through 2027. Other supporting federal policies include the Renewable Fuels Standard (RFS). The RFS allows SAF producers to “opt-in” and generate renewable identification numbers (RINs) that can then be sold to refiners to help offset their renewable blending requirements. The average price of a biomass-based diesel RIN (D4 RIN) in 2022 was $1.66. Unlike obligated parties, SAF producers do not face volume obligations under the RFS. State-level policies include California’s Low-Carbon Fuels Standard (LCFS). Like the RFS, it does not hold SAF producers to any volume obligations but allows them to generate and sell LCFS credits to obligated participants for revenue. Another state-level policy is the Invest in Illinois Act (“Invest Act”). The legislation offers a SAF purchase credit for airlines through 2033.

These policies in conjunction with increasing US airline offtake agreements and private sector investment are driving the US SAF capacity expansion. In 2022, there were 42 announced offtake agreements, the highest of any year in the last decade. This includes an agreement between the major US carrier Delta Airlines and SAF producer GEVO. Starting in 2026 Delta will receive 75 million gallons of SAF annually over the next seven years from GEVO. US carrier United Airlines also announced a joint agreement with Dimension Energy in which they agreed to purchase at least 300 million gallons of SAF over the next couple of decades. But even more support across the public, private, and market dimensions is needed if a net-zero aviation sector is ever to exist.

Another major requirement for scaling up SAF will be the availability of a capable workforce. In our recent 2022 report, Sustainable Aviation Fuels: The Key to Decarbonizing Aviation, we investigated the job creation potential in the US for a range of SAF production pathways. Although our prior work shed light on potential workforce levels associated with commercial SAF deployment, it lacked details on the types of jobs employed. In this note, we provide additional analysis of workforce development in the SAF industry, including the types of jobs created.

SAF workforce opportunities

To successfully scale up SAF by mid-century, we need a capable workforce with skilled laborers in a variety of occupations. For this analysis, we estimated the total number of jobs created by the construction and operation of a 50 million gallon per year SAF facility utilizing the AtJ production process. The selected production capacity falls within the range of capacities for announced SAF projects. As of today, there are no commercial AtJ facilities in operation. However, new commercial-scale projects have been announced in the last few years. The world’s first commercial AtJ facility will be LanzaJet’s Freedom Pines Fuels facility located in Soperton, GA. The ethanol-based production facility is on track for commissioning later this year.

Because there are currently no active commercial facilities, there is no empirical data we can utilize to conduct our analysis. Therefore, we developed a methodology that estimates SAF employment based on adjacent industries. We begin by determining the capital and operating costs for each production process based on expert interviews, literature reviews, and Rhodium analysis. Next, we conduct in-depth research on how the distribution of cost varies by production method and link these costs to the appropriate industries reflected in the input-output economic model IMPLAN. We estimate employment numbers by inputting our cost data into IMPLAN using its national-level dataset. Occupational results are also extracted from the model and supplemented with Bureau of Labor Statistics data. Our employment numbers capture both the on- and off-site jobs associated with the construction and operation of a commercial SAF facility. They also capture jobs associated with upstream supply chain activities.

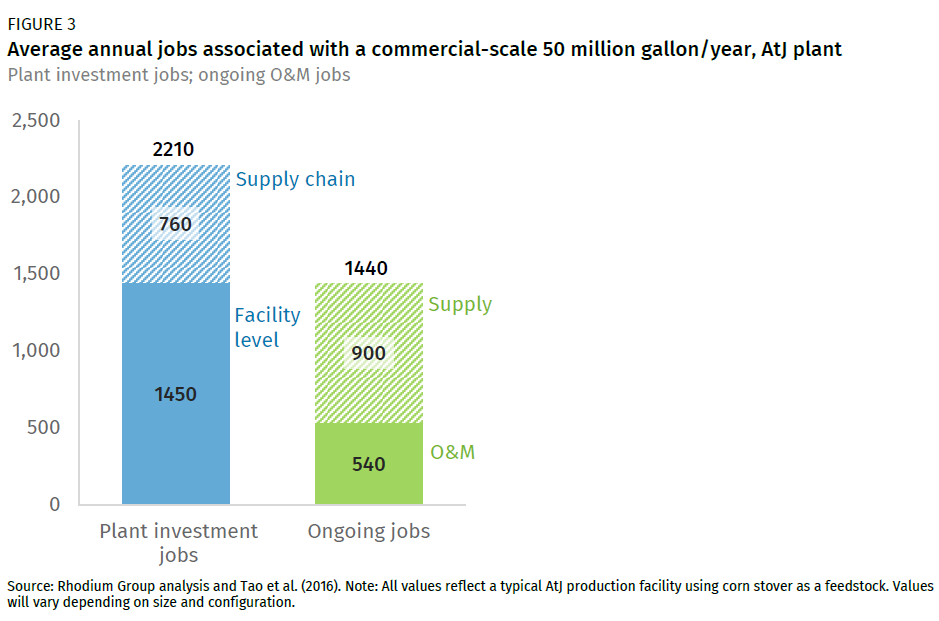

We find that the facility generates, on average, 2,210 plant investment jobs each year over a three-year construction period (Figure 3). Plant investment refers to the construction, engineering, materials, and any equipment needed to build the SAF facility. About two-thirds of these are facility-level jobs as they are directly related to the on-site construction of the facility and its many systems. All remaining jobs support related supply chain activities (e.g., business support services). A total of 1,440 jobs are associated with ongoing facility operations and maintenance (O&M). 38% (540 jobs) of those jobs occur on-site. Most of the O&M jobs occur off-site and support related supply chain activities. A further drill down reveals that a significant portion of the supplier jobs are associated with the production and transport of the corn stover feedstock.

Job breakdown by occupation

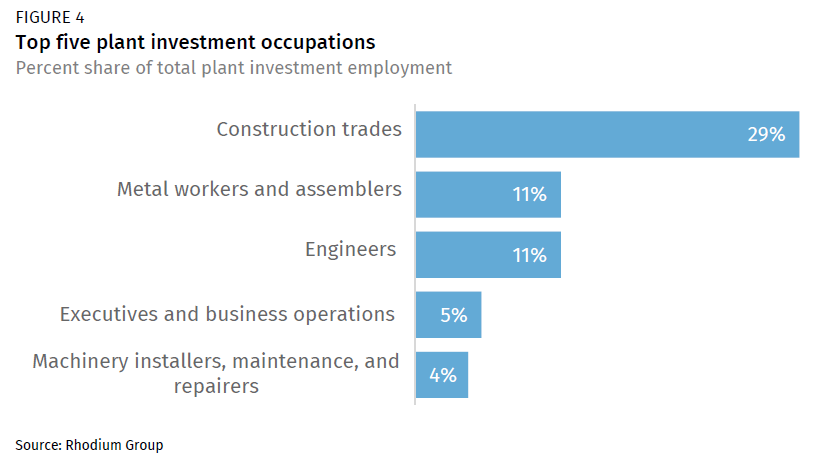

The purpose of our occupational analysis is to show the types of jobs stemming from the building and operation of a commercial AtJ SAF facility, with the focus being on plant investment and ongoing O&M employment.[1] Figure 4 shows the top five occupational categories associated with plant investment. They are: (1) construction trades; (2) metal workers and assemblers; (3) engineers; (4) executives and business operations; and (5) machinery installers, maintenance, and repairers. Together, these occupations account for about 61% of all non-proprietor plant investment employment. Non-proprietor employment refers to wage and salary workers—in other words employees that are not owners.

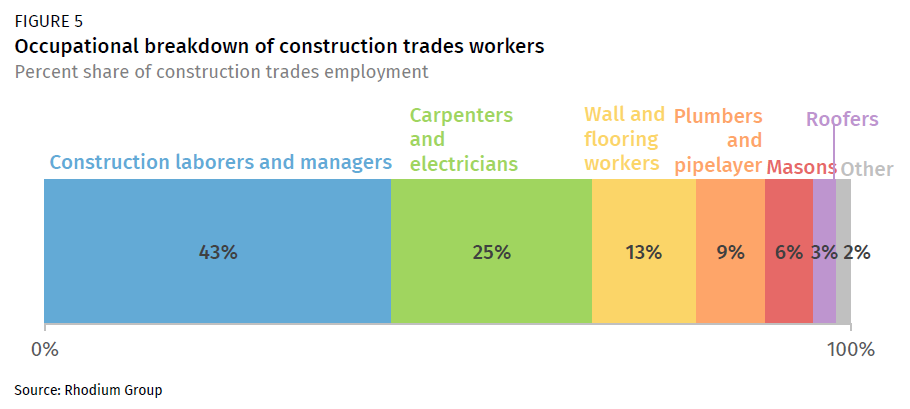

Construction is the largest occupation category, which is not surprising given that it captures all physical labor types involved in the construction of the facility’s exterior shell, building envelope, and many of its complex systems. Roughly 43% of all construction trade workers are either construction laborers or site managers/supervisors (Figure 5). Other prominent occupations include carpenters, electricians, and wall and flooring workers.

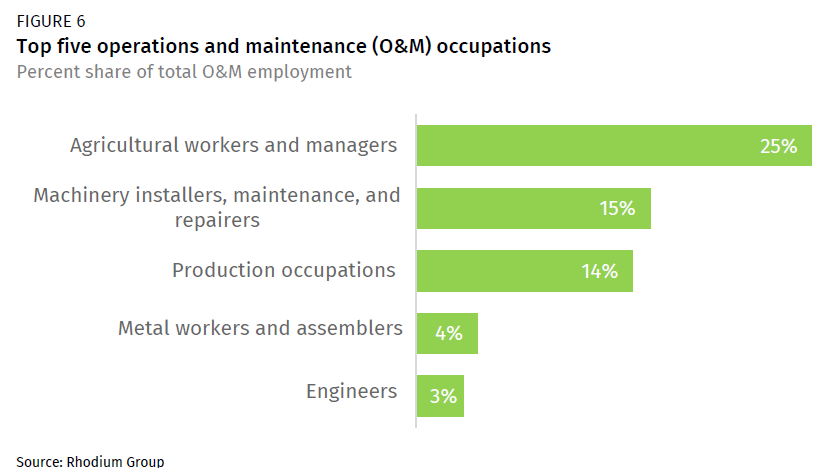

The largest ongoing O&M occupational category is agricultural workers and managers (Figure 6). The AtJ process converts alcohol feedstocks from biomass (i.e., sugars, starches, hydrolyzed cellulose) into SAF. Therefore, the majority of the O&M activities are associated with the processing and handling of biomass feedstock inputs. The next largest category is machinery installers, maintenance, and repairers, which includes industrial machinery mechanics and mobile equipment mechanics.[2]

Overall, our findings suggest that large-scale SAF deployment has the potential to generate thousands of jobs while establishing a workforce that is characterized by a wide range of occupations. Many of these occupations will require both technical and extensive training. As the industry continues to expand, it is imperative that a wide range of resources be directed towards the development and support of new on-the-job training assistance programs. This will ensure that the SAF workforce is well equipped with the skills and knowledge necessary to perform any essential duties.

Forthcoming analysis

So far, there has been limited work exploring the types of occupations associated with the construction and operation of a commercial SAF facility. Our estimates are based on the most up-to-date data in a dynamic and fast-moving technology space. As the SAF industry develops we will refine and expand our analysis. We will also continue to expand upon our employment analysis to investigate important factors including wages, union labor, and required skills.

This note serves as the last in a three-part series on the employment and occupational impacts of selecting emerging clean technologies. The other two notes assess workforce development associated with clean hydrogen and direct air capture facilities.

[1] Supplier jobs are not considered in our occupational analysis.

[2] For additional information on any of the occupations discussed in this note, such as general job duties, wages, or working conditions, refer to the latest edition of the US Bureau of Labor Statistics’ Occupational Outlook Handbook

This nonpartisan, independent research was conducted with support from Breakthrough Energy. The results presented reflect the views of the authors and not necessarily those of supporting organizations.