Pathways to Build Back Better: Maximizing Clean Energy Tax Credits

Continuing to drive clean energy deployment via the US tax code is a key aspect of many ongoing policy discussions. We've identified five key design elements that are critical to maximizing the decarbonization impact of energy tax credits.

Policymakers in Washington, DC are continuing conversations on a host of policy proposals aimed at cutting the country’s greenhouse gas (GHG) emissions. President Biden and a bipartisan group of senators released a framework for an infrastructure deal, Democrats are discussing a reconciliation package, and a budget resolution is on the way. Continuing to drive clean energy deployment via the tax code is a key aspect of many of these conversations.

Our previous research demonstrates that clean energy tax credits can help the US get closer to a 100% clean electric grid, cut harmful pollution, and create or save hundreds of thousands of jobs. But the details of policy design matter. Tax credits can complement a clean electricity standard as well as potential future public health-focused power plant regulations. Simply extending the current clean energy tax credit framework will lead to less pollution reduction and fewer jobs than a revamp that modernizes tax incentives for the decade ahead.

In this note, we identify five key design elements that are critical to maximizing the decarbonization impact of tax credits: long-term availability, full credit value, flexibility, ability to receive direct payments, and extension to existing clean resources. These elements can all be folded into an update and enhancement of the existing investment (ITC) and production (PTC) tax credits, or they can inform the design of a new tax framework. Flexible tax credits that allow any technology to choose the ITC or PTC alongside a long-term, full value extension, direct pay, and incentives for retaining existing clean generators can cut US electric power sector CO2 emissions to 64-73% below 2005 levels in 2031—up to eight times more emission reductions than from a simple extension of the existing traditional tax credit regime at full credit values.

Building a long, flexible runway for clean energy takeoff

Two key tenets are the starting point for any discussion of tax credit design. To ensure maximum impact, lawmakers should push for long-term availability of tax credits, and the size of those credits should be restored to their full values. Under current policy, the ITC and PTC are set to wind down in the near future. [1] The current ITC value for solar is 26% of project costs, phasing down to 22% in 2023, to 10% for 2024-2025, and to 0% in 2026 and beyond. The PTC for wind is set at $15/MWH (60% of the full initial value adjusted for inflation), phasing down to zero in 2022.

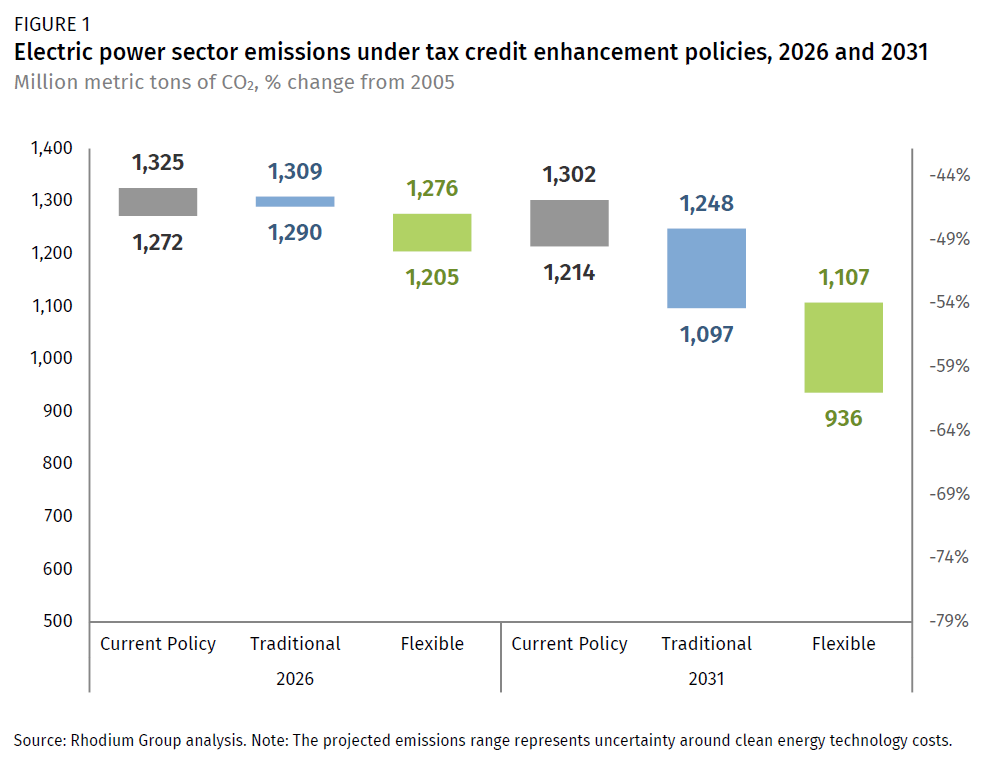

Long-term tax credit extensions give certainty to developers and investors, provide time for supply chains to scale up to meet increasing demand, and can complement potential future state and executive branch actions. Throughout this note, we model tax credits using RHG-NEMS at their full initial statutory value adjusted for inflation (i.e., $25/MWh for the PTC and 30% for the ITC) with a placed-in-service deadline of 2031. These enhancements alone, applied to the existing tax credit framework (essentially a long-term version of the congressional extensions of recent years) yield 54-117 million metric tons (MMt) in emission reductions over current policy in 2031 (Figure 1), and they’re critical to the success of other improvements to tax credits.

Credit flexibility doubles the emissions impact

The third design element that can maximize the impact of tax credits is flexibility. The current tax code is rigid: utility-scale solar can only claim the ITC, while land-based utility-scale wind can only claim the PTC. Expanding both credits so any zero-emitting resource qualifies for either more than doubles their effectiveness, resulting in power sector emissions that are 195-278 MMt lower than current policy in 2031 (Figure 1).

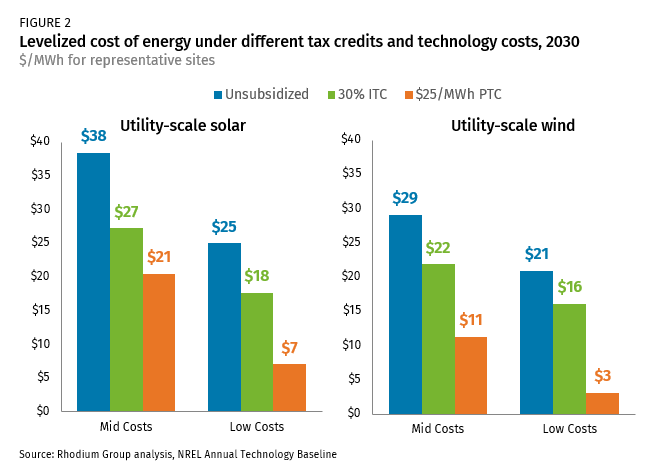

There are a few reasons why adding flexibility to clean energy tax credits leads to these deeper reductions. First, if solar costs continue their steady decline through the next decade, the ITC will provide less and less value to developers on an absolute dollar basis. Every 10% decline in the capital cost of solar reduces the absolute value of the ITC by 10%. Meanwhile, the PTC remains a flat payout of $25 per MWh throughout the decade. By 2030, the levelized cost of electricity (LCOE) for solar at a representative site[2] is 29-157% higher when factoring in the ITC versus the PTC (Figure 2).

Not all locations where wind and solar will be installed align with these representative characteristics—especially as annual deployment ramps up over the decade. In general, the ITC is more valuable in locations that have less plentiful renewable resource (i.e., have lower annual capacity factors), but the actual financial characteristics will vary on a project-by-project basis. This flexible approach is the same as what’s contained in Senate Finance Chair Ron Wyden’s Clean Energy for America Act. Flexibility levels the playing field between the investment and production credits, allowing developers to opt for whatever incentive makes the most sense in any given case.

Direct pay prevents financing bottlenecks

A fourth design element that can maximize the impact of clean energy tax credits is refundability and direct pay. Under current policy, renewable energy developers need to have tax liability or partner with an equity investor who has a tax liability to fully monetize tax credits. Most developers do not have tax liability and typically rely on a pool of relatively expensive and limited tax equity from large banks and other corporate players. Allowing renewable developers to receive the tax incentive for which they qualify either as a fully refundable tax credit or via a direct pay mechanism can decouple the renewables from tax equity and drive additional renewable deployment. This decoupling serves two important purposes.

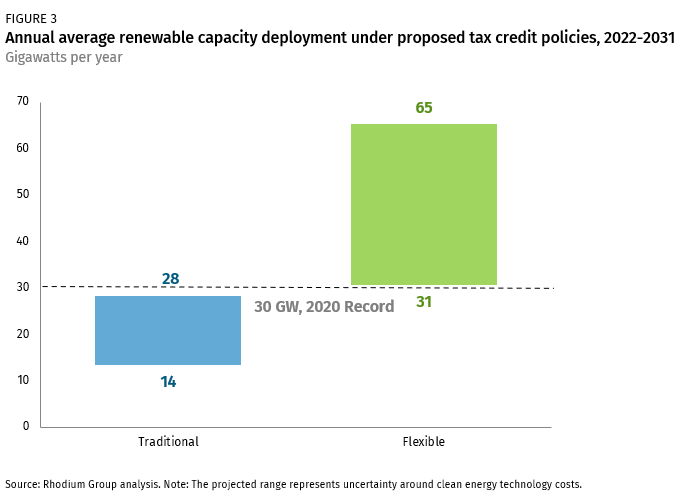

First, there are increasing concerns about the ability of tax equity markets to absorb the credits associated with increasing levels of renewable deployment. In 2020, tax equity markets were stretched thin as developers deployed a record level of renewables—nearly 30 GW of utility-scale facilities in all. Under our modeling, 30 GW represents the lower bound of annual average renewable deployment from 2022-2031 if tax credits shift to a long-term, flexible framework (Figure 3). If renewables meet the most aggressive expectations for cost reductions, this annual figure more than doubles to an annual average of 65 GW. That puts developers and investors in uncharted territory, and it’s not at all clear that there is sufficient appetite among tax equity investors to absorb the associated level of tax credits. If the limits of tax equity are reached, there is a real risk that clean energy deployment will not reach its full potential. Direct pay can help prevent any potential bottlenecks caused by a lack of tax appetite.

Second, tax equity investors often require a higher return than other sources of equity. Allowing developers to seek out cheaper equity reduces the overall cost of capital for renewable developers, thus reducing the cost of electricity from these projects. We estimate that this shift to cheaper equity could amplify the emission reductions associated with a long-term, full-value, flexible tax credit extension by as much as another 5% in 2031. However, some proposals require a 15% reduction in the incentive payout if a developer opts for direct pay. While such requirements would still prevent financing bottlenecks, they likely negate any additional emission reductions associated with a shift to direct pay.

Retaining existing clean resources doubles the impact

The final key aspect of tax credits design is an expansion of their reach so that they can benefit existing clean resources that are at risk of early retirement. Under current policy, existing clean resources such as nuclear, hydropower, and other renewables receive no federal tax credits recognizing their contribution to decarbonizing the electric system, or keeping them from retiring early due to economic challenges. Absent policy action, as much as 64% of the current nuclear fleet could retire by 2030, owing to competitive pressures from cheap natural gas as well as low electric demand growth.

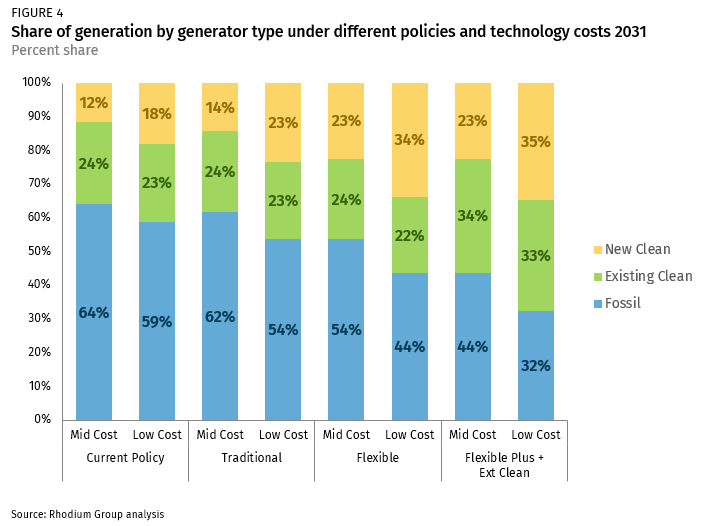

Retaining this large chunk of today’s zero-emitting generating capacity reduces emissions in two ways. When those nuclear plants retire, the electricity they were previously supplying needs to come from somewhere else. Under current policy, natural gas replaces 55% of generation from retiring nuclear plants, while wind and solar only replace 45% of nuclear generation. This dynamic increases the carbon intensity of the grid and makes the task of decarbonization that much harder. Second, supporting these nuclear plants means that new renewable capacity that comes online in the 2020s only displaces fossil plants and does not push yet more nuclear out of the market. Under current policy, fossil fuels provide 58-64% of total generation in 2031. Long-term, full-value, flexible tax credits with direct pay cut that range to 44-54%. When existing clean resources are retained, the range drops to 32-44% of total generation (Figure 4).

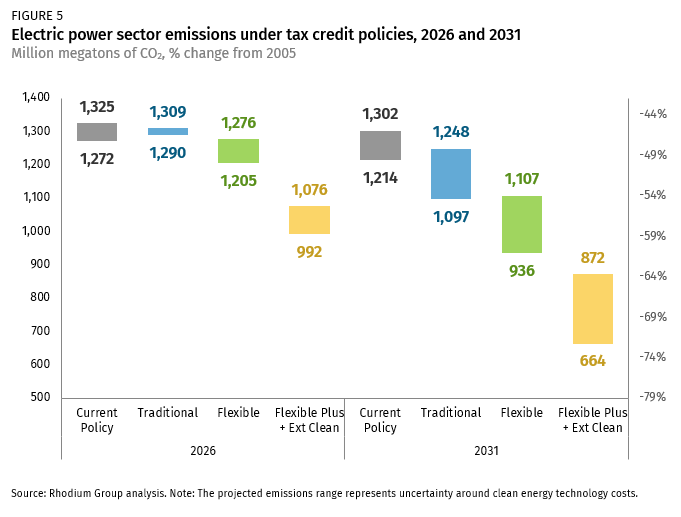

Adding at-risk existing clean generators to the set of resources that can benefit from tax incentives has a meaningful impact on emissions. In 2031, retaining these generators can reduce power sector CO2 by another 235-272 MMt above and beyond what the flexible tax approach does on its own, pushing emissions down to 64-73% below 2005 levels (Figure 5). There are multiple pathways to accomplish this goal, and they can be structured in a technology-neutral manner so that any potentially at-risk resources can take advantage of the credit. Proposals on the table include the Zero-Emission Nuclear Power Production Credit Act, introduced by Rep. Bill Pascrell and Senator Ben Cardin, as well as the civil nuclear credit program in Senate Energy and Natural Resource Chair Joe Manchin’s infrastructure proposal.

Tax credits can meet other recovery goals

In addition to maximizing the emission reduction potential of these tax credits, policymakers can also design tax credits to meet other recovery goals, be they addressing environmental justice and transition issues, developing domestic supply chains and ensuring well-paying jobs, or stimulating the next generation of new clean technologies.

For instance, Senator Wyden’s Clean Energy for America Act includes provisions that increase the size of the tax incentive if the deployment takes place in disadvantaged communities. The bill establishes an inclusive definition of the communities it seeks to target, including areas with high levels of poverty, large industrial or power sector emitters, or a local economy reliant on fossil fuel production. This bonus crediting can help reduce local pollution issues and provide local jobs—while potentially driving even further clean energy deployment.

Similarly, both Wyden’s bill and the House Ways and Means Growing Renewable Energy and Efficiency Now (GREEN) Act include provisions aimed at ensuring workers receive a fair wage when installing projects that receive incentives. The GREEN Act offers a 10% plus-up of the ITC for projects that meet Davis-Bacon wage requirements, while the Wyden bill makes receipt of the ITC and PTC contingent on payment of locally prevailing wages. The Wyden bill also requires projects to meet certain domestic content requirements to be eligible for direct pay.

Finally, tax credit provisions can be designed to drive investment in critical clean energy technologies beyond wind and solar. Nearly every single study shows that technologies beyond wind and solar can lower the cost and accelerate the achievement of decarbonizing the electric sector.[3] The Energy Sector Innovation Credit provides a technology-neutral framework to incent early-stage deployment of new clean generating technologies, and the Wyden bill increases payouts for nascent technologies. The Wyden bill also makes an ITC available for energy storage and new transmission investments. Increased deployment of these emerging and enabling technologies will be critical to achieving full decarbonization of the power sector. Extension and increased credit values under the section 45Q carbon capture tax credit can provide long-term support for retrofitting existing coal and natural gas plants as well as deploying next generation power plants with near-zero combustion CO2 emissions.

What will Congress and the White House do?

Congress and the White House have a rare opportunity to make meaningful changes to the way the US tax code helps to drive power sector decarbonization. Understanding the trade-offs in key design elements of tax policy is critical to ensuring their goals are met. As concrete tax reform proposals emerge and infrastructure proposals move forward, we plan to assess the extent to which policymakers are maximizing the impact of these powerful policies.

[1] Throughout this note “current policy” refers to current laws on the books with no assumed modifications or extensions.

[2] NREL defines the representative value as the plant characteristics “that most closely align with recently installed or anticipated near-term installations of electricity generation plants.”

[3] See for example: Harvey et al 2021, Larson et al. 2020, Haley et al. 2019, Larsen et al. 2019 and IPCC 2018.

This nonpartisan, independent research was conducted with support from Bloomberg Philanthropies, the ClimateWorks Foundation, and the Heising-Simons Foundation. The results presented in this report reflect the views of the authors and not necessarily those of supporting organizations.