Closer to Home: Testing the Western Hemisphere’s Diversification Potential

Most countries in the Western Hemisphere are not competitive for ex-China diversification, and in the few that are, like Mexico, costs are rising. Reorienting supply chains to the region will therefore be a necessarily gradual effort.

The Trump administration is reenvisioning US economic ties in the Western Hemisphere, with an ambitious agenda to combat China’s influence, secure access to critical raw materials, and nearshore manufacturing supply chains in its neighborhood. These ambitions are bound to collide with a harsh reality: Most countries in the Western Hemisphere are not competitive for ex-China diversification, and in the few that are, like Mexico, costs are rising. Reorienting supply chains to the region will therefore be a necessarily gradual effort, requiring significant and more predictable policy support and realistic phase-in timelines to account for upstream China dependencies. An aggressive push to build ex-China supply chains in the Western Hemisphere also risks upsetting the fragile truce the US administration has with Beijing, short-circuiting its own re-industrialization plans, and inadvertently motivating China to assert stronger influence in the Indo-Pacific.

US economic influence in the Western Hemisphere

The US has strong, long-held economic ties with its neighbors in the Western Hemisphere.1 Preferential trade agreements—USMCA, CAFTA-DR, and US free trade agreements with Chile, Colombia, Panama, and Peru—geographic proximity, and decades of US investment have made the Western Hemisphere the source of nearly a third of US imports, while the US makes up over half of the Western Hemisphere’s exports (Figure 1).

These ties are strongest with Mexico and Canada, the largest US trade partners in the Americas. As a result of decades of trade integration through NAFTA and now the USMCA, Canada and Mexico account for 85% of US imports from the region, as well as 28% of total US imports and 33% of total US exports in 2024. This trade is underpinned by deep supply chain linkages, particularly in the automotive industry, where a component may cross the border with Mexico or Canada up to eight times before sale. Mexico’s share of US imports has also grown since Trump’s first term as companies looked to nearshore manufacturing of products subject to Section 301 tariffs on China as well as products used in critical infrastructure or other sensitive applications, with notable growth in medical devices, AI servers, and select electronic components (see October 9, Chain Reaction: US Tariffs and Global Supply Chains).

As the US looked beyond Mexico for cheaper manufacturing options, some Central American countries also emerged as specialized export hubs for various critical goods. Costa Rica has developed a small but thriving medical device manufacturing ecosystem, with production of increasingly complex devices for over 80 companies, mostly for the US market. Under the Biden administration, Costa Rica, along with Panama, also received support from the US to promote the development of near-shored semiconductor manufacturing capacity, especially assembly, testing, and packaging. These investments are bearing fruit, shown in recent export growth (Table 1).

Central America also picked up labor-intensive production for the US market, on the back of rising labor costs in Mexico, favorable logistics, and trade integration. CAFTA-DR’s yarn-forward rule, which requires most apparel inputs to come from the region to qualify for preferential treatment, supported the development of a vertically integrated regional supply chain offering lower lead times and freight costs than some Asian suppliers. More recently, Honduras emerged as a producer of wiring harnesses and other automotive components, thanks to its cost-effective workforce compared to Mexico.

The US imports significant amounts of commodities, including critical raw materials, from South America. Chile is the largest global producer of copper, followed at a distance by Peru. Along with Argentina, Chile is also a major supplier of lithium used in batteries, and an important source of rhenium for superalloys. Bolivia, Brazil, and Peru supply refined tin, for which the US is almost entirely dependent on imports. Brazil and Canada dominate global production of niobium, used in high-strength steel and aerospace applications. Trade in these raw materials comes in addition to energy and agricultural goods, which lead most South American countries’ exports to the US (Table 1).

Still, once Canada and Mexico are taken out, the Western Hemisphere plays a much more limited role in the US economy compared to other regions. This pattern is reflected in the US direct investment position in manufacturing. In fact, the Western Hemisphere shows $235 billion US direct investment position in manufacturing in 2024, compared to $537 billion in Europe, and $264 billion in Asia.

China and the “Donroe” Doctrine

China has also expanded its influence in the Americas in recent years. Over the past decade, exports to China from the Western Hemisphere, excluding the US, have grown by over 80%. Brazil and Peru are key beneficiaries, with outsized growth in soybean, copper, iron, precious metals, and petroleum oils exports to China. China has also made geopolitical inroads, with countries like Jamaica, Barbados, and Grenada participating in the Belt and Road Initiative, and Honduras severing diplomatic ties with Taiwan in 2023.

No wonder then that China is in the crosshairs as the Trump administration seeks to reassert its influence in the Western Hemisphere (see January 5, Man in the Arena: Trump’s Geopolitical Gambit for the Americas and Beyond). The National Security Strategy, National Defense Strategy, Department of State’s Strategic Plan for 2026, trade deals with several Latin American countries, and recent statements from top officials like Secretary of State Marco Rubio, highlight three objectives for US Western Hemisphere policy regarding China.

Combat Chinese influence, with a focus on critical infrastructure

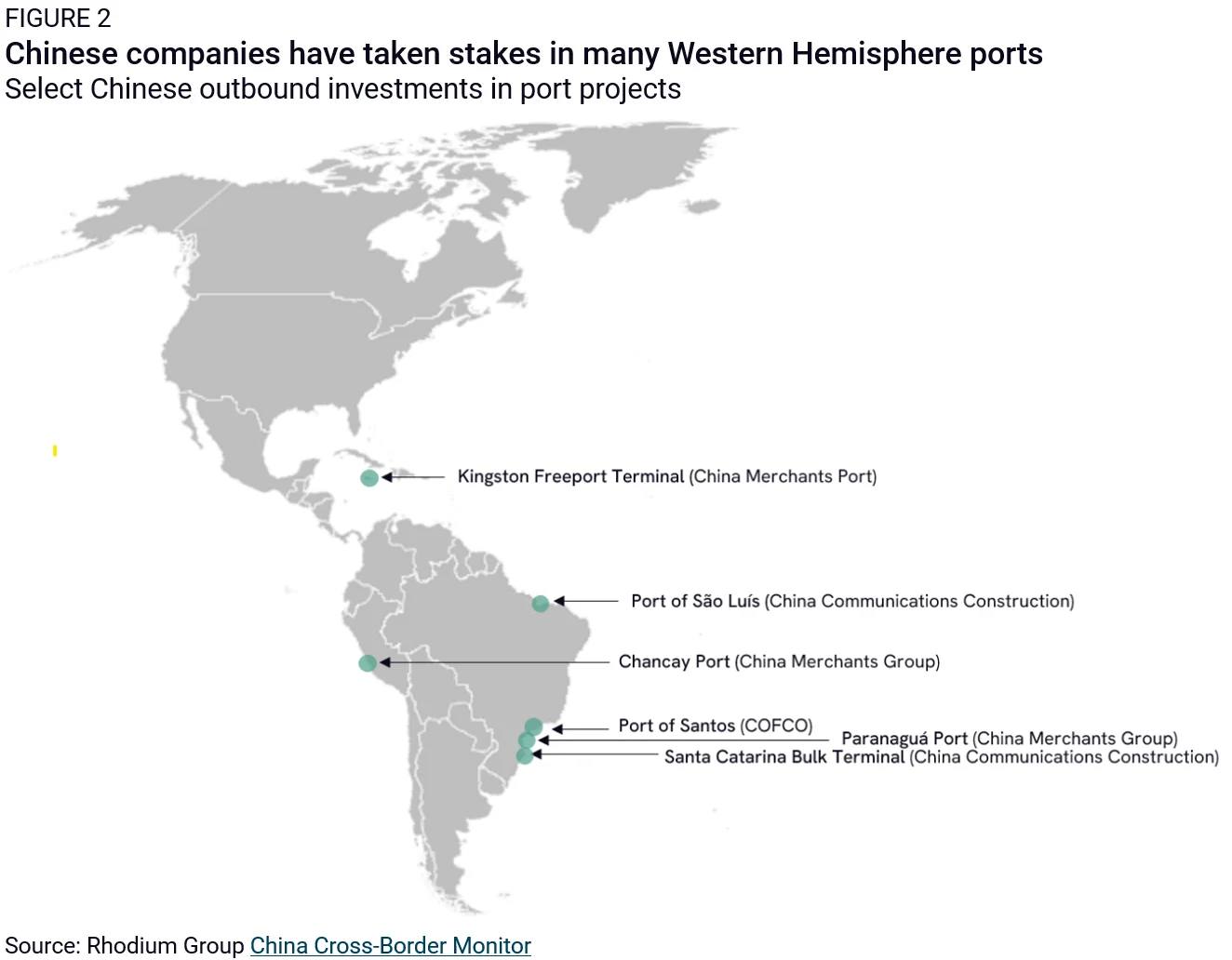

Limiting the influence of foreign powers has long been a core objective of US policy in the Western Hemisphere, dating back to the Monroe Doctrine. In recent years, the US government and military have raised concerns around Chinese investments in telecommunications networks, space facilities, deepwater ports, data centers, and other critical infrastructure systems (Figures 2 and 3). For example, last year, US Southern Command flagged Chinese space facilities and China’s COSCO’s 60% stake in Peru’s Chancay Port in its Posture Statement. China’s presence in Latin America has been mentioned as a threat in the past three National Security Strategies, starting with the first Trump administration. These concerns remain central in the second Trump administration’s National Security Strategy, in which the US pledged to “deny non-Hemispheric competitors the ability to position forces or other threatening capabilities, or to own or control strategically vital assets, in our Hemisphere.”

The first Trump administration sought to curb Chinese influence in the Western Hemisphere and other regions by highlighting the espionage, cybersecurity, “debt-trap,” and reliability risks of accepting lower-cost Chinese goods and foreign assistance. The second Trump administration is reiterating this message, with the US State Department explicitly warning, for example, that “cheap Chinese money costs sovereignty” with regard to Peru’s Chancay Port. It is also taking more forceful measures, like leveraging its treaty with Panama to push out CK Hutchison and insert a Western consortium to control the Panama Canal (see March 31, The Clawback: Reclaiming Strategic Assets from China). the US can also coerce alignment with threats of tariffs via Section 301 investigations or further asset clawbacks on national security grounds.

The US is also offering investment and preferential access to the US market and technologies in exchange for security and economic policy alignment. Recent trade deals with Latin American countries have conditioned low tariff rates on commitments to align with US export controls, investment security, and other restrictions, with China in focus. Guatemala and El Salvador agreed to only use communication technology suppliers “that do not compromise the security, safeguards, and intellectual property of ICT infrastructure, including 5G, 6G, communication satellites, and undersea cables.” While the Supreme Court struck down the IEEPA-based tariffs, the Trump administration has said it will reestablish tariffs with alternative legal statutes and can lean on other tools to ensure Western Hemisphere countries hold up their end of the bargain (see February 2020, Trade Tracker: IEEPA Tariffs Overruled).

Expand resource extraction, including of critical raw materials, to de-risk from China

President Trump has been blunt about his administration’s interest in the Western Hemisphere’s resources. The US Southern Command, in its 2025 posture statement, noted that “the region is home to abundant natural resources, including 20% of the world’s oil reserves, 25% of its strategic metals, 30% of its forest area, 31% of its fishing areas, and 32% of its renewable freshwater resources.”

Critical raw materials are especially in focus given China’s weaponization of critical inputs over the past year. Argentina, Bolivia, Brazil, Canada, the Dominican Republic, Ecuador, Mexico, Paraguay, and Peru all took part in a recent US-led Critical Minerals Ministerial. Access to critical minerals is also partially driving Trump’s interest in asserting stronger control over Greenland, given the island’s vast deposits.

In the aftermath of US Operation Resolve in Venezuela, Trump was explicit in declaring a US intent to control Venezuela’s oil. Secretary of State Marco Rubio has meanwhile focused attention on mining operations in the Orinoco belt for rare earths, bauxite, and gold. This region, however, is a militant hotbed and could become a proxy battleground to attack US-backed mining operations.

How the US ultimately plans to lay claim to the region’s resources remains unclear. The US International Development Finance Corporation, which, unlike many other US agencies, has seen its financing triple over the past year, has pledged to focus on critical minerals projects in Canada, and has been in talks on critical minerals with Argentina. Senators are also looking to raise the Export-Import Bank’s lending cap from $70 billion to $205 billion in support of critical minerals projects. And if positive inducements don’t work, the Trump administration has also demonstrated its willingness to threaten and use tariffs and military action through recent tariff threats on European partners, Greenland annexation threats, and recent events in Venezuela.

Deepen hemispheric supply chains

The US is also looking to expand its critical supply chains in the region. This effort serves several US objectives. First, as successive US administrations have articulated, a more prosperous Western Hemisphere could stem illegal migration, as fewer would make the treacherous journey to the US in search of economic opportunity. Second, further developing supply chains in strategic sectors in the hemisphere could reduce US dependence on Chinese manufacturing and inputs. The region’s geographic proximity, abundant supply of critical minerals, and comparatively low Chinese upstream dependencies make it especially attractive to DC strategists (Figure 4). Third, as the National Security Strategy notes, “an economically stronger and more sophisticated Western Hemisphere becomes an increasingly attractive market for American commerce and investment,” which, over the long run, could reduce Asia’s relative importance to the US economy.

A crucial part of this effort is preventing Chinese companies from gaining a foothold in Western Hemisphere markets and minimizing the use of Chinese inputs in hemispheric supply chains. Outside Mexico, there is limited Chinese value-added in exports from Western Hemisphere countries (Figure 4). But China is looking to alternative markets for its exports and to transship goods to the US. In response, the Trump administration is pressuring its neighbors to raise tariffs and non-tariff barriers on Chinese goods, as seen with Latin American countries’ commitments to impose “equivalent” or “similar” measures when the US imposes tariffs on third countries and to address unfair trade practices of third-country companies operating in their jurisdictions.

Mexico’s recently implemented tariffs on imports from countries with which it does not have an FTA, aimed at China, could serve as an example. The US could also unilaterally change rules of origin to ensure imports from Western Hemisphere countries do not contain Chinese content (December 8, Beyond Made in China: US Attempts to Rewrite Rules of Origin).

Reality check

Western Hemisphere’s low competitiveness as a diversification hub

The Trump administration’s vision to develop supply chains in the Western Hemisphere will run up against structural and institutional constraints. In recent decades, supply chains have relocated to countries with sufficiently skilled yet low-cost labor, supportive and predictable policies, trade and investment openness, high-performing logistics, existing manufacturing capacity, and a large, growing domestic market. Yet, most countries in the Western Hemisphere lag on many of these indicators. Our 2024 analysis showed that only Canada, Mexico, Chile, and Brazil ranked in the top 50 of US potential diversification partners (see Table 2 and August 7, A Diversification Framework for China).

Preferential access to the US market and low wages, combined with relatively strong basic education across much of the Western Hemisphere, could, in principle, support greater supply chain diversification. Literacy rates in Latin America and the Caribbean are comparable to those in Vietnam and Malaysia (around 96%) and exceed those in Thailand (91%), India (81%), and several other emerging economies. Wages in low-skill sectors are also broadly in line with those in Southeast Asia.

However, many countries on the continent fall far below the global average on key measures of political stability, government effectiveness, regulatory quality, rule of law, and corruption—raising costs and uncertainty for long-term investors in countries like Brazil, El Salvador, Guatemala, Honduras, and even Mexico. Beyond Mexico and Canada, the region ranks near the bottom on logistics, only beating Sub-Saharan Africa in the World Bank’s Logistics Performance Index. These factors, plus the relatively small working population and small domestic markets, make it difficult for many Western Hemisphere countries to offer the stability and scale that firms seek when relocating supply chains—and hence to offer an alternative to producing in Asia.

This is not to say that diversification to the region is impossible. If US trade and investment policy creates the right incentives (see below), firms are likely to shift production, at least on the margins. Mexico—with deep trade ties to the US, existing manufacturing clusters, and sustained US pressure to build a “Fortress North America”—could capture supply chains across sectors, despite rising costs. A few smaller players could also pick up share of the US export market, even if their small workforces constrain the scale of production. Costa Rica could build on its success in the medical devices industry to expand export-oriented manufacturing in sectors that rely on higher-skill labor, rigorous quality control, and strict compliance with US regulatory standards, such as pharmaceuticals, electronics, and defense equipment. Panama, leveraging its strong port infrastructure and incentives for assembly and refurbishing, plus Colombia, with its growing manufacturing capacity, could step up production of low-complexity products sensitive to labor costs. With supportive domestic policies in place, Chile—already strong on most measures of diversification attractiveness and rich in raw materials—could also expand select industrial goods exports to the US.

Uncertainty in US tariff policy

Given the Western Hemisphere’s shortfalls, supply chain diversification to the region would, at a minimum, require significantly lower tariff rates than alternative manufacturing hubs (see October 9, Chain Reaction: US Tariffs and Global Supply Chains). Recent US trade deals, plus comments from Jamieson Greer, suggest the US is looking to establish this differential: Argentina, El Salvador, and Guatemala received reciprocal tariff rates of 10%—the lowest of US trade partners—and exemptions that brought their trade-weighted average tariff even lower than other countries. Although the Supreme Court struck down these reciprocal tariffs, exemptions for CAFTA-DR textile goods under the Section 122 tariffs suggest the Trump administration will preserve lower tariffs for Western Hemisphere countries as it rebuilds the tariff regime.

Mexico and Canada also continue to benefit from tariff rate exemptions under Section 122 for USMCA-compliant goods, which drastically lower their effective tariff rates for US-bound exports (Figure 5). Given the Trump administration’s focus on affordability, particularly ahead of the US midterm election, we expect the US will preserve these exemptions in the upcoming USMCA review. The main area to watch will be changes to rules of origin, such as increases to the regional value content requirement. This could reduce the number of goods that initially qualify for exemptions but will incentivize deepening regionalized supply chains.

The successful conclusion and implementation of these deals is not guaranteed, particularly amid the Supreme Court’s ruling on IEEPA-based tariffs. Trump has also privately asked advisors why he shouldn’t withdraw from the USMCA. Persistent tariff uncertainty, which is bound to continue as the Trump administration rolls out Section 301 investigations in lieu of reciprocal tariffs, could limit investment in manufacturing in the Western Hemisphere (see February 2020, Trade Tracker: IEEPA Tariffs Overruled).

US negotiations with other trade partners will matter too. The tariff differential that Western Hemisphere countries currently enjoy could decrease or disappear if other US trade partners also secure tariff exemptions or reductions, including for strategic goods subject to Section 232 tariffs. The US offer of a 0% tariff on a to-be-specified volume of select Bangladeshi, Indonesian, and Indian apparel and textile products is an example of this dynamic. Any further decreases in tariffs on US imports from China would also temper supply chain diversification to the Western Hemisphere.

Difficulties diversifying without Chinese companies or components

The US is pushing trade partners to align on economic security measures that aim to restrict Chinese goods and companies from their markets. Trade deals with Argentina, El Salvador, and Guatemala are no exception, with economic security provisions that could be used to restrict Chinese content in Western Hemisphere supply chains.

Ambassador Greer has outlined similar objectives for upcoming negotiations with Canada and Mexico. In testimony to Congress in December, he said the US will push for alignment on tariffs, export controls, and investment screening. He also said the US would seek to tighten USMCA rules of origin for non-automotive industrial goods and address Mexican policies that promote the use of third-country content and erode US supply chains, in an apparent bid to reduce Chinese content in US imports.

If implemented as the Trump administration envisions, Western Hemisphere countries would be expected to build supply chains with limited Chinese participation. But, where supply chain diversification has happened to date, it has almost always involved Chinese companies or inputs (see February 4, China and the Future of Global Supply Chains). If Western Hemisphere countries are required to expand production without China, the timeline will be significantly prolonged. A realistic US strategy for diversification in the Western Hemisphere would thus need to allow for some Chinese involvement in the interim and phased-in timelines for reducing Chinese content.

Moves to “de-risk” from the US and manage relations with China

Many countries in the Western Hemisphere may simply be unable to push back against US coercion, given their economic ties to the US, vulnerability to US security threats, and general power asymmetries. However, a growing middle power push to “de-risk” from the US could still stifle the Trump administration’s plans.

Canada’s decision to ease tariffs on Chinese electric vehicles in exchange for greater canola exports is a case in point: Allowing BYD or other China-made vehicles into the North American trade bloc directly undermines the US ambition to create a “Fortress North America” and block out foreign adversary influence. With USMCA in review, the US can ratchet up economic pressure on Ottawa to realign with the US-led tariff strategy on China. But the geopolitical climate for such alignment is now much more fraught.

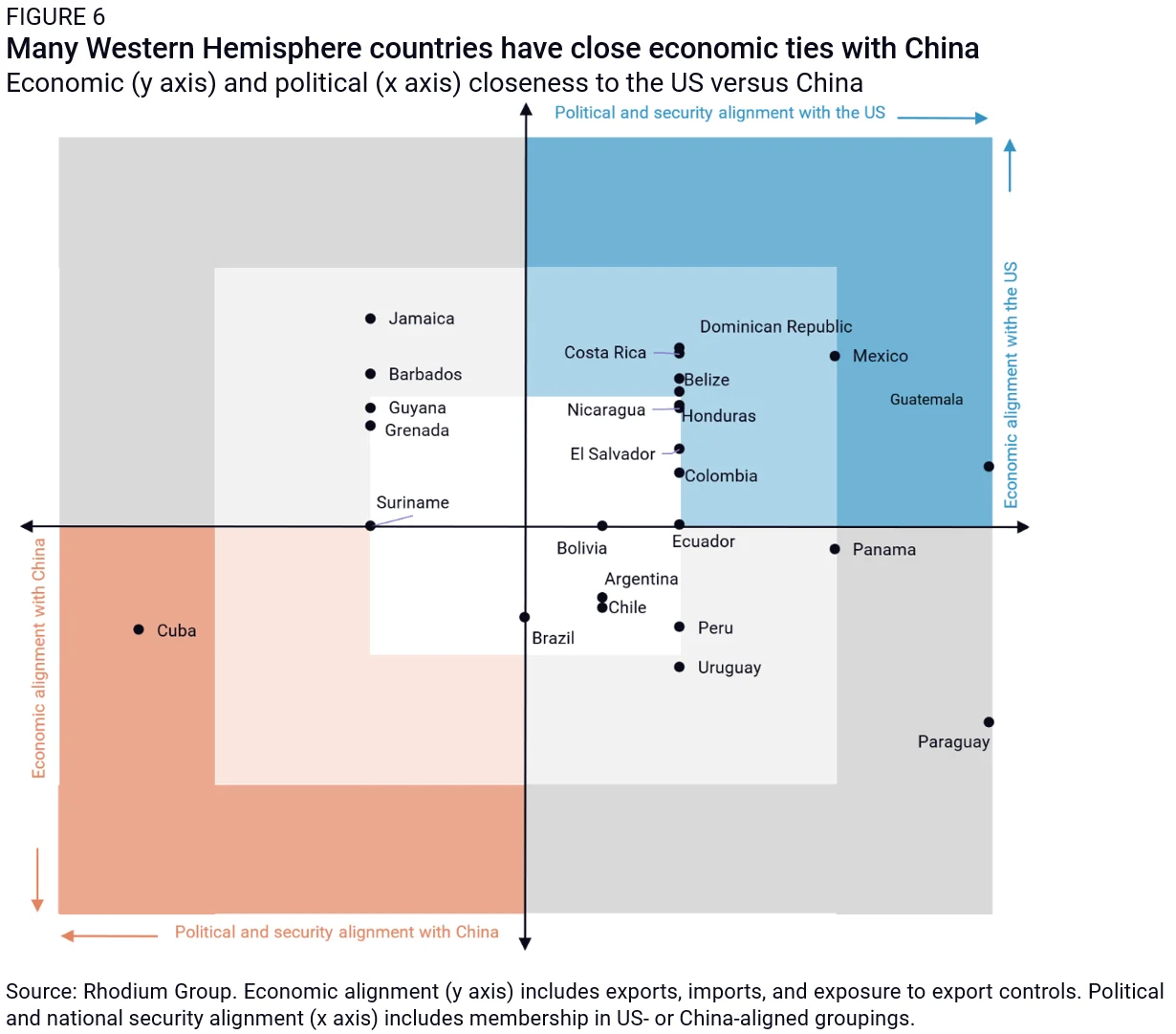

Moreover, while most countries in the region remain geopolitically aligned with the US, China has become a more important partner, which Western Hemisphere countries may be wary of crossing (Figure 6). Western Hemisphere countries that raise trade barriers against China would likely be targeted by retaliatory measures, including tariffs on key exports, even if China continues to import commodities—such as Brazilian soybeans—from the region.

China could also seek to offset US pressure through more positive diplomacy. While Chinese FDI in the region has fallen over the past decade amid the broader decline in Chinese outward investment, Chinese companies have announced major transactions in the automotive and basic metals, materials, and minerals sectors recently (see February 4, China’s Global Investment Grew in 2025, But Exports Outpaced Offshoring). The promise of jobs from investments like these, the allure of Chinese infrastructure, or fresh development financing could deter some Western Hemisphere countries from aligning too closely with the US.

China’s response

China, in this context, will play both spoiler and emulator. During the Trump years, Beijing’s primary objective is to undermine US trade frameworks laden with restrictions on Chinese trade and investment because China, which is ever more reliant on exports for growth, needs overseas markets to remain open. This explains why, as Canada became fed up with US disruptions to cross-border trade and Trump’s territorial threats to acquire Canada as the 51st state, Beijing was quick to roll out the red carpet for Prime Minister Mark Carney.

China can pressure governments in the Western Hemisphere that are aligning with US trade and security objectives by offering competing investments. It can also leverage its market prowess to undercut competitors on price. China can step up economic coercion on target countries by quietly raising trade barriers, intensifying phytosanitary inspections on perishable exports, encouraging consumer boycotts, pausing pending investments, restricting critical inputs for manufacturing, or even withholding critical medical supplies. During the COVID-19 pandemic, China conditioned access to vaccines on Paraguay, Guatemala, and Honduras dropping recognition of Taiwan. In response to the Panamanian government’s invalidation of CK Hutchison’s port concessions, Beijing has already delivered guidance to state-owned enterprises to freeze pending projects in Panama and has threatened to reroute ships to avoid the canal.

Beijing could also create an opportunity out of the so-called Donroe Doctrine. China has made a practice of imitating US national and economic security measures, as evidenced by its burgeoning export control regime. Similarly, Chinese President Xi Jinping can imitate Trump’s attempt to boot out foreign adversary influence in the Western Hemisphere by asserting a comparable Xi doctrine for the Asia-Pacific. In his negotiations with Trump, Xi could demand an end to US freedom of navigation patrols in China’s backyard and a reversal of US economic security conditions with Asian trading partners. Above all, China would demand US non-interference in Taiwan, including a halt to arms sales.

In surveying the map, the Trump administration sees the Western Hemisphere as an “easy” target to apply military pressure and make geopolitical gains for resource extraction, nearshoring production, eradicating foreign adversary influence, and even territorial expansion. But ambition and geographic proximity do not make a strategy, and some Trumpian tactics have already shown the risk of backfiring and playing into Beijing’s hands.

Perhaps the ultimate test of Trump’s legacy for the Western Hemisphere rests not on redrawing the map or tacking on corollaries to historic documents, but on the less flashy goal of building up regionalized trade in the Americas. This would entail a tariff design that maintains high and coordinated tariffs on China across key markets while tempering the impulse toward punitive tariffs on neighbors and keeping low trade barriers within the region. It would entail credible enforcement of measures like the ICTS rule with reasonable timelines for phasing out Chinese content and credible investments to build out manufacturing capacity in the most promising diversification candidates. A successful USMCA renegotiation, inclusive of China-specific measures, could even create the conditions for expansion of the agreement to qualifying countries like Costa Rica.

Footnotes

We define the Western Hemisphere as North America, Central America, South America, and the Caribbean.