After the Fall: China’s Economy in 2025

By our estimates, China’s GDP growth in 2024 improved modestly to around 2.4% to 2.8%, well below target. If it stimulates domestic demand with some urgency and ramps up debt, we think China could get to 3-4.5% growth in 2025.

China’s 2024 claim that GDP growth was on track to meet high targets was impossible to reconcile with increasingly frantic efforts to prop up a flagging economy all year long. Collapsing property construction slowed growth to a crawl in 2022 and 2023, and in 2024 the spillover from real estate sidelined local government investment and consumption as well.

By our estimates, China’s GDP growth in 2024 improved modestly to around 2.4% to 2.8%, well below than official claims of nearly 5%. If it stimulates domestic demand with some urgency and ramps up debt, we think China could get to 3-4.5% growth in 2025, reaching the high end of that range only if everything falls in Beijing’s favor. But that is the very top of—or above—the potential growth ceiling until Beijing fixes long-festering structural problems.

Grappling with “authority bias”

The difference between analyzing China and any other economy in the world is the implicit “authority bias” in China’s official data. Beijing’s narrative of its own economic progress highlights certain economic data series (year-on-year real GDP growth, fixed asset investment, stable employment data) and excludes others (falling prices, slowing nominal GDP growth, falling fiscal spending relative to budget targets). How one sees China’s economic conditions depends on which aspects of Beijing’s narrative to credit and which to question.

Authority bias is now central to the global discussion of China’s slowdown. The most obvious disconnect is between China’s macroeconomic data and Beijing’s policy actions. Officially, China’s real GDP growth slowed only modestly from pre-pandemic levels in 2022, then rebounded to 5.2% growth in 2023—in line with the annual target. The public numbers show only a 0.4 percentage point (pp) slowdown coming into the end of 2024. But while reporting this good news, authorities have cut interest rates aggressively, conducted a mid-year budget adjustment unseen since the Asian financial crisis, unveiled a 10 trillion yuan ($1.4 trillion) refinancing program for local government debt, created new liquidity facilities for the central bank to directly support the stock market, changed the official monetary bias to “appropriately easing” for the first time since the global financial crisis, and called for “extraordinary” support for the economy in the December Politburo meeting. No government adjusts economic policy like that to counter a minor slowdown from 5.2% to 4.8% growth.

A judgment about statistical credibility is essential to any assessment of China’s economy. In a recent blog post, the IMF warned that the slowdown in China’s domestic demand is partly responsible for rising trade imbalances. But that drag on China’s real economy shows up nowhere in its macroeconomic data, which the IMF elsewhere accepts as reliable. And then, closing the ouroboric circle, Chinese officials regularly cite the IMF outlook to show that their economy is on track.

But the reality of a slowdown is clear, particularly in price data. China has fallen far short of its nominal GDP growth target in the past two years (4.6% versus a 6.9% target in 2023, 4.1% vs. a 7.4% target so far in 2024). Economists associated with China Finance 40 Forum, a think tank, recently argued that consumer price index (CPI) growth over the past three years was around –2%, well below official figures.

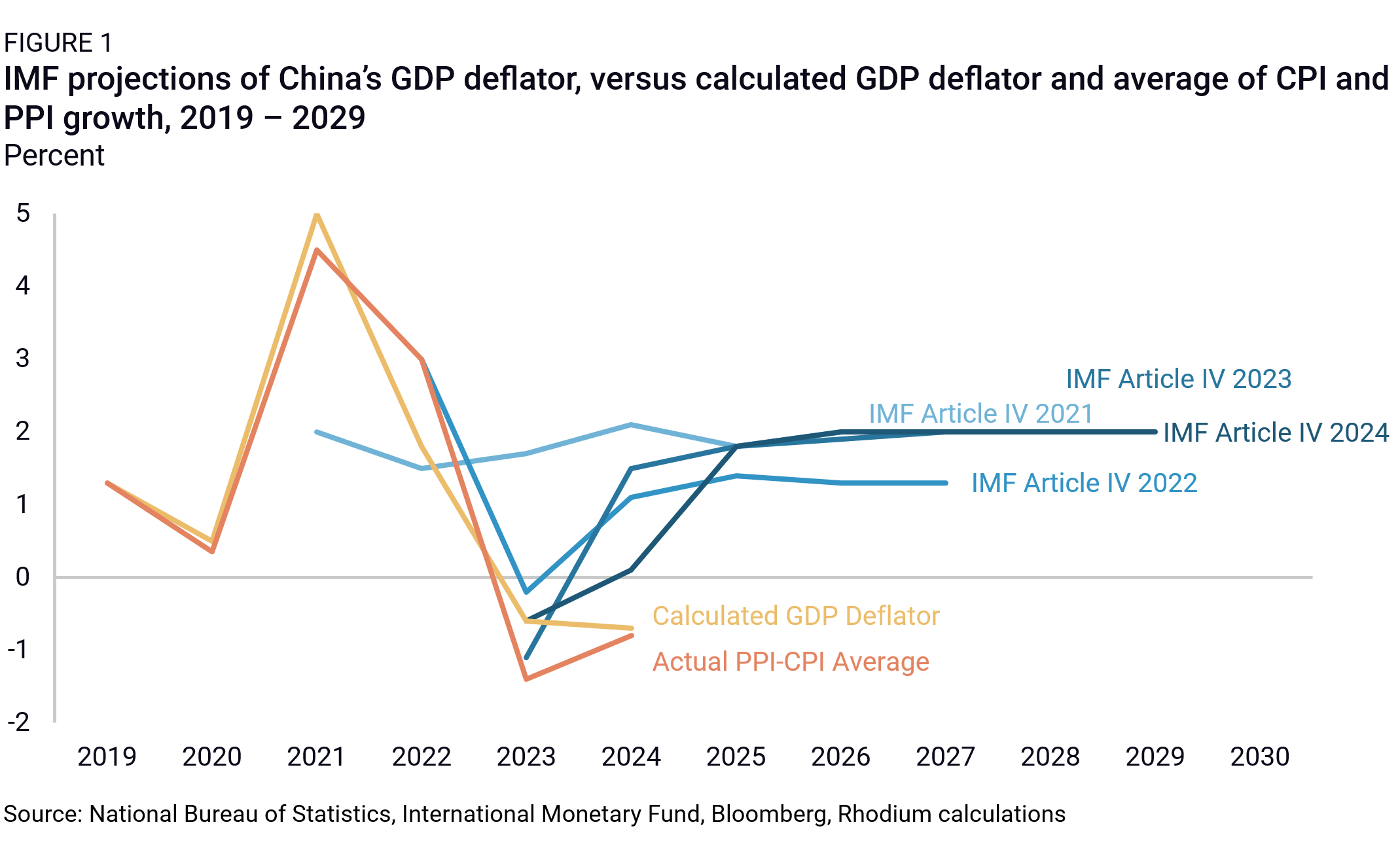

By contrast, the IMF’s macroeconomic projections do not suggest any deflationary concerns, with price growth forecast to return in 2025 and rebound to around 2% through 2029. That would suggest no domestic demand policy support is necessary. The chart below highlights the evolution of the IMF’s projections of the GDP deflator—a measure of how headline growth is affected by inflation—in China within the last four Article IV reports, compared with the actual calculated GDP deflator and the average of consumer and producer price growth. Even after price growth has disappointed in 2023 and 2024 following the slow rebound in activity after COVID restrictions were lifted, the Fund has continued to upgrade its outlook for China’s prices.

We doubt that we are saying anything that the Fund and its staff do not already know. We highlight these issues with the Fund’s presentation of China’s economic data because their assessments are closely followed by policymakers and business leaders around the world. The Fund would likely argue that focusing on the quality of Chinese data would divert attention away from their efforts to shape policy decisions to make growth more sustainable, and China may throw up obstacles to them doing so, as they did in 2007 with the debate over exchange rate surveillance policies.

The key question for the rest of us is: when does the authority bias of China’s official data distort our perception of how China’s growth affects the global economy? We think we passed that point long ago. As we argued in 2022, 2023, and earlier this year, China’s property and local government-driven slowdown has been far more severe than implied in official data, and this is harming global interests. Chinese economists we’ve spoken to agree with virtually all the facts in this critique, if not the implications of them. Some argue that GDP growth has been overstated by 3 pp for each of the past three years, which suggests that the overall size of China’s economy is around 10% smaller (or $1.7 trillion) than official data imply.

To justify our position in the China GDP debate, we focus on the expenditure-side components of growth: investment, household consumption, government consumption, and net exports. This note analyzes each of these components in the 2024 growth picture, and how we see them evolving in 2025.

2024 in review

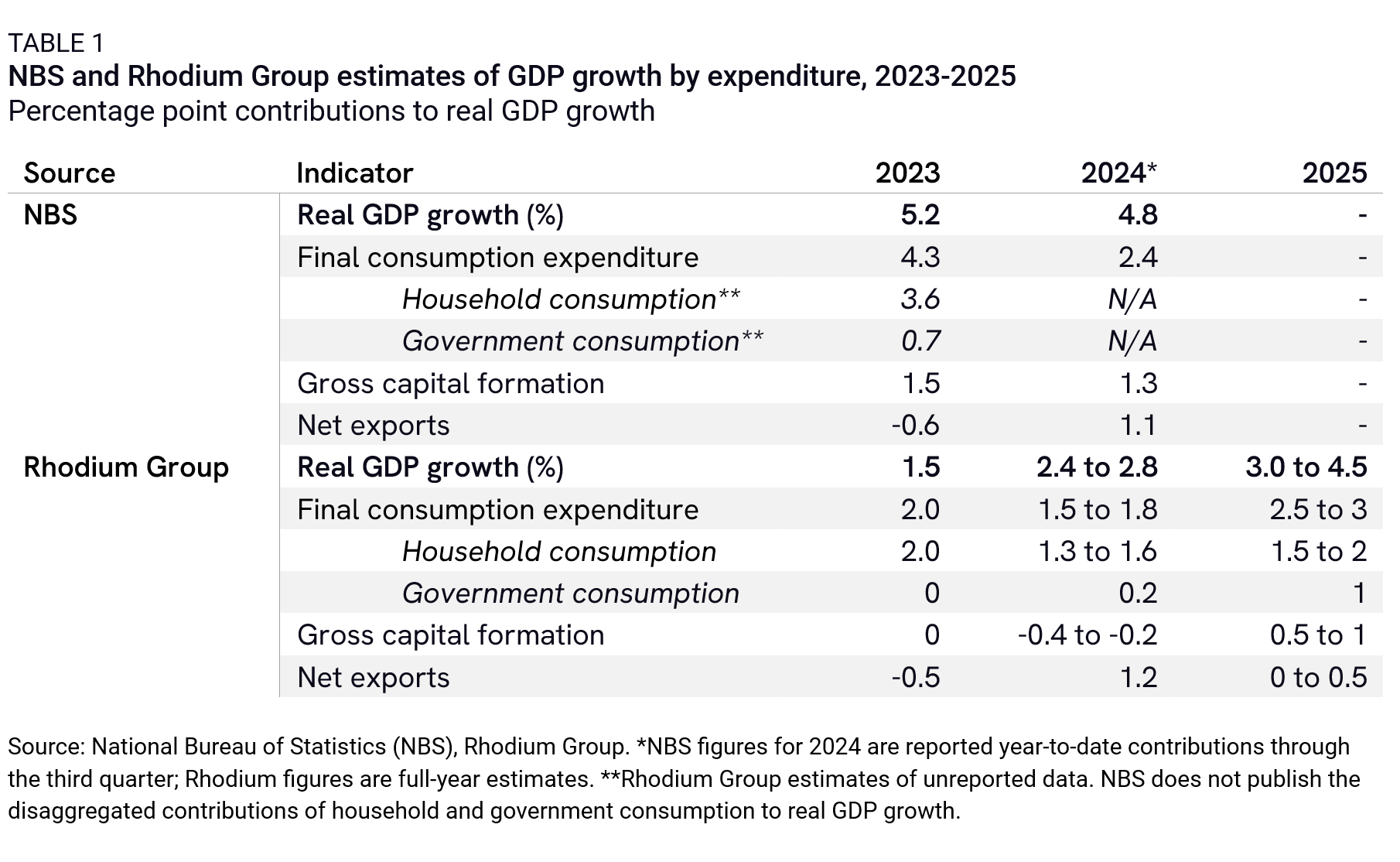

In 2024, we estimate that China’s GDP grew 2.4 to 2.8%, well below the 4.8% annualized year-to-date growth through Q3 reported by NBS. The largest area of divergence between official numbers and ours was in gross fixed capital formation (investment), with differences in household consumption also important.

Because our estimates of China’s growth in 2022 and 2023 differ substantially from official statistics, we base our annual growth estimates for 2024 on our own estimates for growth in those years.

Investment

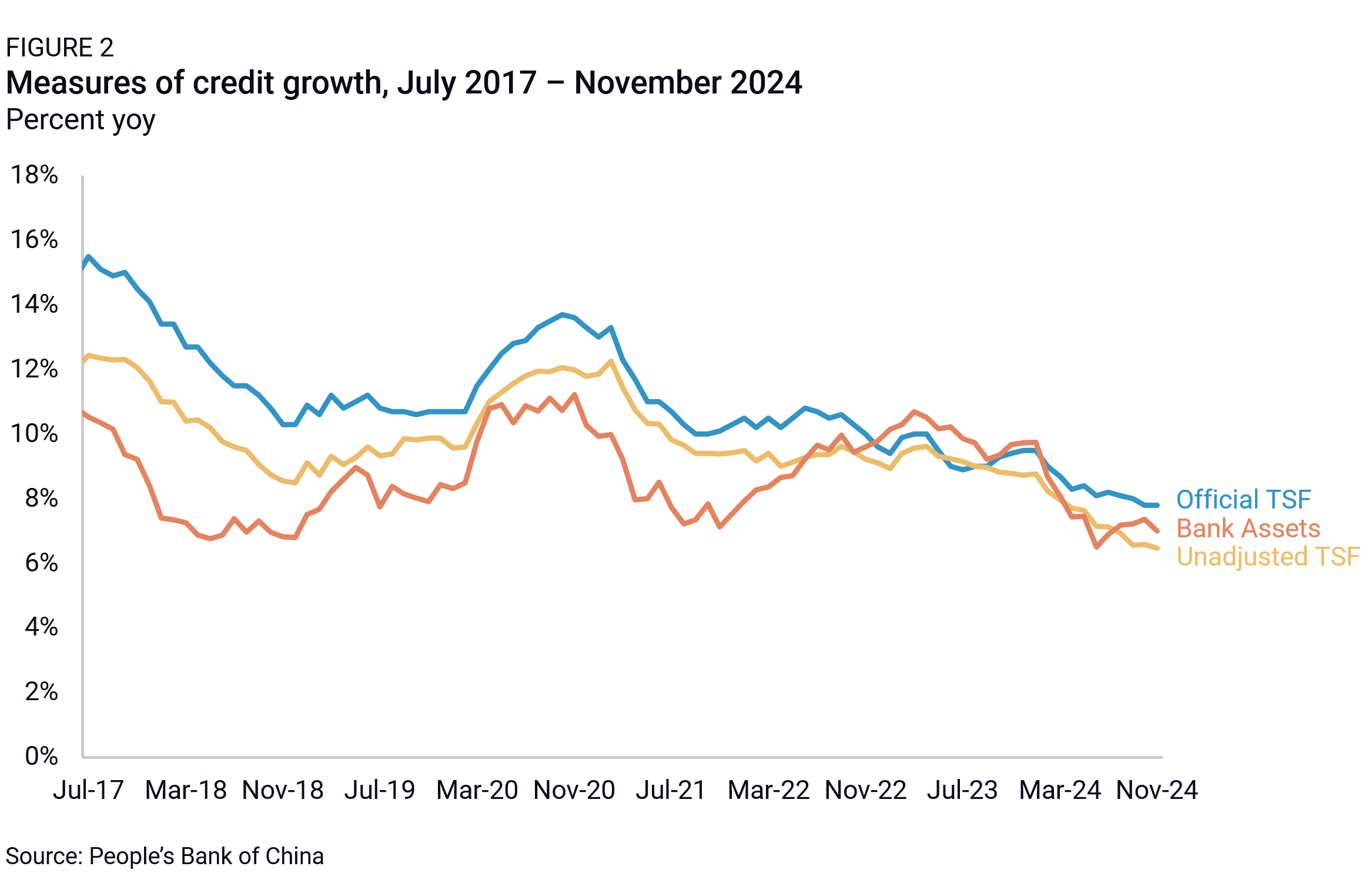

Official data will likely show stable investment growth in 2024, adding around 1.3 to 1.5 pp to GDP growth. We argued that investment activity was almost certainly negative in 2023, led by contraction in the property sector. In 2024, investment growth is likely flat at best, and probably declining again, led by the slowdown in local government investment, particularly in infrastructure. This has been reflected in a significant slowdown in overall credit growth, with TSF growth hitting new lows at 7.8% y/y, and bank asset growth ex-government bonds trending below 6% (Figure 2). Most of the decline in borrowing has occurred among local government financing vehicles (LGFVs) from “risky” provinces as designated in the still unpublished Circular 35 from October 2023.

Officially, infrastructure-related fixed asset investment is growing at 4.2% through November, down from 5.9% last year. But fixed asset investment data have never fully captured the changes in China’s credit and investment cycles. Other evidence speaks to much weaker infrastructure growth: so far this year, cement output is down 10.1%, asphalt plant utilization rates have been declining throughout 2024, and the drop in diesel demand has been severe, even amid an overall 1.8% decline in refinery runs in China. Even if one does take the fixed asset investment data at face value, private fixed asset investment has declined by 0.4% so far this year.

The property sector continued to decline in 2024, with new starts down by 23% through November and completions down 26.2%. These headline numbers probably overstate the decline in property construction, as the NBS data does not capture projects that are subcontracted from LGFVs to property developers. These projects have become more common as local governments have had little alternative to incentivizing their own LGFVs to buy land. High-frequency indicators of construction activity, such as the average hours worked by Komatsu construction equipment, reveal a stabilization in activity in the last few months. Nonetheless, it would be difficult to argue that the property sector grew in 2024: the question is the extent of the decline. If property and local government infrastructure investment both declined, while even official data recognizes that private sector investment fell, it is hard to understand what could have produced investment growth.

Furthermore, local government fiscal weakness was the trigger of the policy pivot from September 2024. The 10 trillion yuan in announced new bond issuance to swap for local government debt over the next five years is meant to help localities struggling to pay for civil servants and social services. Under these conditions, how should we expect growth in infrastructure investment?

It is more probable that investment shrank in 2024 (or stayed flat at best) rather than contributing to GDP growth. The decline in real growth was likely in the same range or slightly deeper than in 2023, given the additional pressure on local government infrastructure investment, resulting in a -0.4 to -0.2 pp drag on GDP growth.

Government consumption

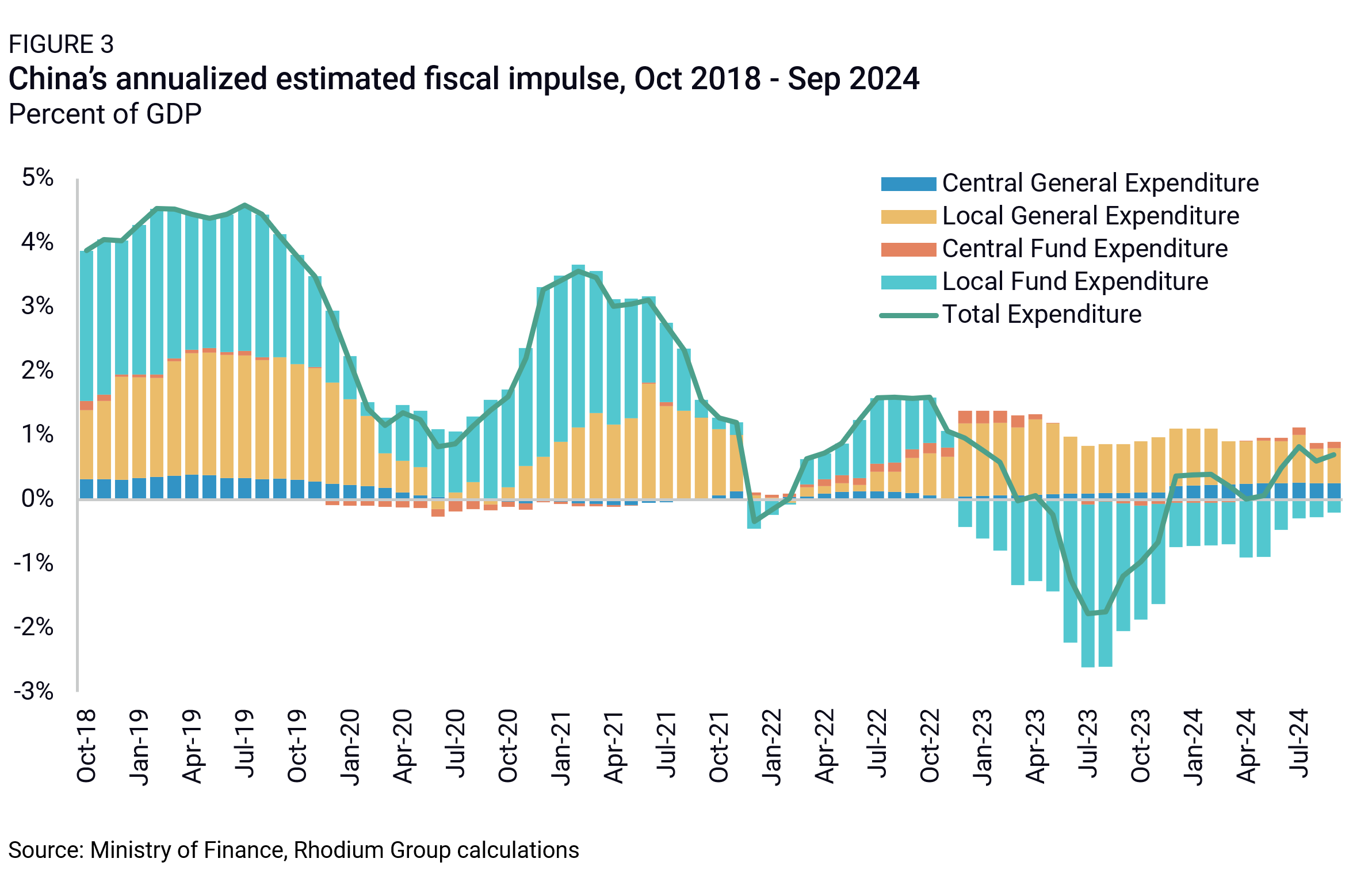

NBS does not publish the government contribution to real GDP growth in quarterly data, instead consolidating household and government consumption. The Ministry of Finance’s fiscal expenditure statistics are the best proxy available, even though they do not precisely correspond to government consumption in the national GDP accounts. Official monthly government expenditure data through October 2024 show meager spending growth this year. Total spending across central and local governments is up just 1% year to date (see Figure 3), including general and fund expenditures.1 December spending is always higher than in other months, but even an upside surprise will not significantly alter the full-year picture.

Given widespread deflationary pressures, government prices were likely flat in 2024, meaning that government consumption in real terms was probably weakly positive, contributing around 0.2 pp to growth.2 As in recent years, the biggest source of drag has been local government fund expenditure, which is contracting for the fourth consecutive year. This, in part, follows from incentives facing local government officials, whose priorities have shifted from growth to debt management. Meanwhile, the productivity of infrastructure investment projects continues to decline, and land sale revenues remain weak.

The stimulus package announced in November will not have much effect on 2024 government consumption. It focuses on refinancing local government debt at lower interest rates, which is necessary from a debt sustainability perspective, but will have a limited impact on government consumption. And any impacts from a package announced so late in the year will be felt mainly in future years.

Household consumption

Official data will likely imply slightly above 2 pp of household consumption contribution to 2024 GDP growth.3 According to NBS household survey data, from which official consumption GDP data are derived, real per capita household expenditure is expanding at 5.3% this year.4

This figure is hard to square with other indicators of household consumption. NBS’s own nominal retail sales growth figures are less than half of what they were last year, and official estimates of online retail sales are essentially flat. The NBS consumer confidence index remains at an all-time low. The CPI increased just 0.2% y/y in November, with services inflation slowing to near zero. Core price growth, which strips out food and energy price fluctuations, is only marginally higher at 0.3%. High-frequency and alternative consumption measures also paint a bearish picture, with e-commerce sales on Jingdong and Alibaba’s Taobao and Tmall platforms contracting 3%.

Real household consumption growth is probably closer to CPI-adjusted retail sales, somewhere between 3.5% and 4%, resulting in a contribution to real GDP growth of 1.3 to 1.6 pp.

Net exports

Net exports made a large positive contribution to China’s growth in 2024. Exports rose 6.7% in value terms year-to-date through November, up from 0.6% in the same period last year. Falling prices mean that real exports have been even stronger. Export quantity growth was 11.6% year-on-year in November and was double digits throughout all but two months of the year. Rising volumes and falling prices are two sides of the same coin: China’s industrial overcapacity incentivizes its producers to both cut prices and export more (see Figure 4).

Meanwhile, imports have been weak, with imports in value terms up only 2.4% year-on-year through November. Subdued household consumption is a factor, but the larger impact is from weak property and infrastructure investment, which lowers demand for raw materials and intermediate construction inputs.

The net effect of rising exports and flat imports is a large net positive contribution to GDP growth. NBS data show a 1.1 pp contribution for Q1-Q3, but monthly trade data for October and November suggest that Q4 will push the full-year figure slightly higher, perhaps to 1.2 pp. If that figure holds, taking the official data at face value, 2024 would see the third-highest net export contribution to China’s growth this century. It was higher only in 2021, when China restarted its factories while other major economies were struggling to contain the COVID-19 pandemic, and in 2006, when export growth was surging in the years following China’s WTO entry.

Looking ahead to 2025

Investment

After a steep decline in property investment since 2021, there is a strong case that construction activity will stabilize in 2025. New starts are now down 68% from their peak levels, below our estimates for long-term equilibrium demand in the sector. Local government infrastructure investment is likely to stabilize as well, given more aggressive fiscal spending and a reported expansion of special treasury bond issuance. It remains unclear how much the Ministry of Finance may relax requirements on qualifying investment projects, but the volume of fiscal spending is still likely to reverse the current decline in infrastructure investment. Private investment is likely to remain weak, given the overall constraints on credit growth and continued deflationary pressures in producer prices, which are expected to persist. Trade tensions and rising protectionism are likely to limit new investment in manufacturing in China itself, although Chinese firms may be more active in investing abroad. Overall, we would argue that investment is likely to stabilize and contribute positively to growth in 2025, expanding 2-3% in real terms, thus contributing around 0.5 to 1.0 pp to GDP growth.

Government consumption

Government spending should contribute more to growth in 2025. The government has promised a stronger fiscal impulse, and there are reports of a fiscal deficit target of 4% in 2025, up from the initial 2024 target of 3%. Three trillion RMB in reported special treasury bond issuance should also increase government spending. Lower interest rates as part of China’s debt refinancing push should also reduce the cost of local government debt service, freeing up money to spend elsewhere. However, the actual volume of government spending and resulting investment activity will probably fall short of these targets, as most government-led investment is still executed and implemented by LGFVs, and they will continue prioritizing managing their existing debt burdens.

China’s fiscal system will remain constrained by weak revenue growth. China’s tax system is heavily tilted toward industrial production, with the general budget deriving approximately 60% of revenues from corporate income and VAT taxes. During the past 12 months, total tax revenue declined by 3.3% (or 592 billion RMB) as deflationary pressure and weaker industrial output have eroded tax income. Land sales revenues, which have been the largest constraint on local government finances over the past two and half years, are likely to stabilize but cannot return to past levels of growth.

Put together, government spending will be supported by the larger fiscal deficit, a substantial increase in special treasury bonds, stabilizing land sales, and a reduction in interest rates, but this contribution will be capped by continued weakness in tax revenues. Cumulatively these changes in government finances will result in around a 0.5 to 1 pp contribution to GDP.

Household consumption

After years of disregard, boosting household consumption was the top message at the December 2024 Central Economic Work Conference. Beijing plans to scale up the late-2024 trade-in subsidy programs used to boost auto and household appliance sales. Yet despite this focus, consumption faces headwinds. Household consumption fundamentals will remain about the same as long as disposable income and wage growth continue to slow. No substantial policy measures have been announced that will substantially change the employment or wage outlook.

Instead, policy support programs are mostly focused on expanding trade-in subsidy programs for consumer durables. Programs this year stimulated spending in targeted product categories (sales of household appliances and autos grew at 27% and 10% year-on-year in November), but it is unclear whether they added to aggregate consumption. Though the expansion of these programs will modestly support short-term consumption growth in 2025, the primary impact of these programs is to pull demand forward in time.

Policymakers are also framing local government debt programs as promoting household consumption, the logic being that by increasing social services spending and thus reducing the need for precautionary savings, households will spend more. However, the scope of these programs is so limited that the impact on social services spending is likely to be small.

The multi-year process of household deleveraging is also not yet finished. Households are likely to continue paying down mortgage and credit card balances, reducing the potential for more real economy spending. While we expect property price stabilization, households have endured profound negative wealth effects from the real estate crisis. And fragile labor market conditions weigh on consumer confidence.

On balance, we project household consumption growth of between 3.5-4.5% in 2025, similar to our estimates for recent years, corresponding to a growth contribution of around 1.5-2.0 pp to GDP.

Net exports

China’s trade outlook in 2025 is deeply uncertain. First is US tariffs: though Trump has talked about 60% tariffs on all Chinese goods, the scope, timing, and enforcement capacity are unclear. Second is China’s response: Beijing’s most likely response to US tariffs will be to allow the yuan to depreciate, partially though not completely offsetting the impact of tariffs. China may also retaliate with its own tariffs on US imports and export restrictions on critical inputs like graphite. At the macroeconomic level, these moves will not move the needle much: Any agricultural imports China doesn’t buy from the US will come from other trading partners, and critical inputs like gallium and germanium account for a tiny fraction of China’s overall exports.

The biggest source of uncertainty is how the rest of the world responds. US tariffs on China’s exports will cause Chinese exporters to seek markets elsewhere. If China’s trading partners do nothing, China’s volume of exports will be mostly unchanged, with the US importing less, and other countries importing more.

If global markets remain open to China, growth in China’s record-high trade surplus—which determines whether net exports is a driver or a drag on GDP growth—is likely to be small but positive, contributing perhaps around 0.5 pp. The spike in China’s trade surplus in 2024 was largely the result of weak domestic demand. Government efforts to promote consumption and infrastructure investment, and the bottoming out of the property sector, will likely slow the pace of export growth and somewhat boost imports.

However, China’s trading partners are unlikely to stand by as sustained Chinese industrial overcapacity and a weaker RMB threaten their own industries, especially if US tariffs push Chinese exports their way instead.

Tempering expectations

2024 was a turning point in the narrative around China’s economy. Faced with collapsing credibility even among Chinese economists and increasingly unviable talking points claiming that everything was on track, Beijing conceded late in the year that it needed to use all the tools available to support domestic consumption. This was too late to salvage results for 2024, though once again Beijing will claim to have hit its targets, and the IMF and other organizations will flinch from questioning that. Still, China’s policy stance is clearly changing. The action pledged so far involves short-term counter-cyclical support, and is likely to boost growth from the 2-3% range in 2024 to the 3-4% range in 2025, perhaps even as high as 4.5% if everything goes Beijing’s way. But a cyclical 2025 improvement should not be mistaken for a long-term recovery. Overinvestment in manufacturing remains a serious challenge—one that will make China’s trading relationships more fraught in 2025—and rebalancing toward a consumption-led economy will require much deeper economic liberalization.

Footnotes

China’s fiscal accounts are divided into four separate budgets: the general budget, the government funds budget, the state capital operations budget, and the social security funds budget. The official budget deficit considers only the general budget, which covers day-to-day government operations, but a complete picture of China’s fiscal policy should ideally account for all four. The Ministry of Finance releases statistics for the general and government funds budgets on a monthly basis, but figures for the other two are released only annually. The general and government funds budgets accounted for a combined 79% of China’s total government expenditure in 2023.

The price deflator for government consumption is not provided by NBS and must be estimated. We follow Holz (2014) in estimating the government consumption deflator as a weighted average of CPI and PPI, yielding -0.1% government price growth for 2024 based on monthly price indices reported through November. See Carsten A. Holz, “The Quality of China’s GDP Statistics,” China Economic Review 30 (September 2014): 309–38, https://doi.org/10.1016/j.chieco.2014.06.009.

Final consumption expenditure, of which around 70% is household consumption, has contributed 2.4 pp to growth year-to-date through Q3, according to NBS figures.

NBS does not report the levels of the demand-side GDP components in real (price-adjusted) terms. Rhodium Group constructed estimates of these unreported data using reported nominal levels of GDP components, the reported percentage point contributions of major GDP components to real GDP growth, and price deflators.