Rhodium Climate Outlook: Probabilistic Projections of Energy, Emissions, and Global Temperature Rise

We provide probabilistic projections of the likely evolution of global emissions and temperature rise through the end of the century.

Eight years after the adoption of the Paris Agreement, the international community will gather at COP28 in Dubai and conclude the first Global Stocktake to gauge progress in limiting global temperature increases to well below 2°C above pre-industrial levels. The need to understand what kind of climate future the world is on track for has become increasingly important not just for diplomats and policymakers, but to almost every actor of the global economy. These policy-takers need access to an outlook that incorporates uncertainty in factors over which they have no control—variables like policy, fuel prices, and economic growth. The newly launched Rhodium Climate Outlook strives to provide this kind of information, with detailed data on how the global energy transition, greenhouse gas (GHG) emissions, and temperatures are likely to evolve given current policy and technology trends, but absent a major acceleration in climate policy and clean technology innovation.

The Rhodium Climate Outlook (RCO) seeks to address some of the shortcomings of existing modeling with probabilistic energy, emissions, and temperature projections of use to a wide range of global stakeholders, including policy-takers. We’ve done this by incorporating the following innovations, which to our knowledge have never been combined in a single modeling platform:

- Probabilistic global emissions projections that capture uncertainty in economic and population growth, oil and gas prices, and clean energy technology costs.

- An econometrically-based policy projection module that uses evidence of the determinants of climate policy around the world over the past two decades to provide probabilistic projections for how policy is likely to evolve going forward.

- Projections for all GHG emissions, not just CO2.

- Probabilistic temperature projections derived directly from our emissions projections but including climate system uncertainty as well.

In this inaugural RCO, we find that:

1. The world is very likely on track to exceed 2°C above pre-industrial levels, but we’ve avoided the most catastrophic projections.

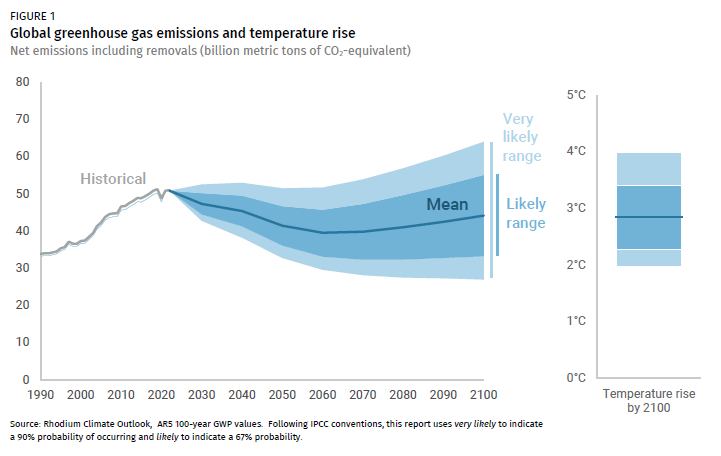

Shortly before the Paris Agreement was adopted in 2015, the Intergovernmental Panel on Climate Change (IPCC) estimated that without additional efforts to reduce emissions, global temperatures would increase between 2.5 and 7.8°C (very likely range, i.e. 90% confidence interval) by the end of the century. Policy and technological progress over the past eight years has significantly reduced the global temperature outlook. We now project very likely temperature increases of 2.0 to 4.0°C by century’s end, with a 2.3 to 3.4°C likely range and a mean of 2.8°C. While this is progress from just eight years ago, it still represents a dire climate future—falling significantly short of the Paris Agreement goal of limiting warming to well below 2°C.

2. The world has made progress in decarbonizing electricity and vehicles, but current technology has its limits.

Thanks to several decades of policy and innovation, the world has made considerable progress in decarbonizing power generation and transitioning from internal combustion to electric vehicles. As a result, emissions from power and transportation likely fall and peak in the coming decade, respectively, with both declining through mid-century. But momentum in power and transport bottoms out after mid-century as variable renewable energy (like wind and solar) and electric vehicle deployment plateau, and as demand for more power and transportation continues to increase. Without ongoing support for variable renewable technologies, along with significant policy acceleration and innovation in zero-emission dispatchablegeneration (e.g., storage, advanced geothermal and advanced nuclear), fossil generation hangs on and even expands in the second half of the century. In transportation, as policy and innovation drive decarbonization for passenger and freight vehicles, emissions from air and marine transport remain stubbornly high and increase (with more than 50% probability) absent an acceleration of policy and innovation in zero-emission fuels and technologies for aviation and shipping.

3. As electricity and transport decarbonize, industry becomes the largest challenge.

We see a greater than 50% chance that emissions from the industrial sector—including production of iron, steel, cement, oil and gas, and chemicals—rise over the coming decades as demand for industrial products grows without widely available, cheap decarbonization solutions, offsetting the progress achieved in power and road transportation. By 2050, industry consumes more fossil fuel than power generation, and emits more GHGs than power, transport, and buildings combined in our projection mean. By century’s end, industrial emissions grow to three times the level of emissions from either electricity generation or transportation (projection mean). It took decades of policy and investment in innovation to scale decarbonization technologies in power and transport. Solutions for decarbonizing industry are still in their very early stages of development and will require a significant acceleration in both innovation and policy to achieve the same liftoff velocity as renewables and EVs.

4. Fossil fuel use likely peaks this decade, but not for long.

Global fossil fuel consumption—including coal, natural gas, and oil—is likely to peak this decade thanks to progress in decarbonizing power and passenger vehicles. We find a greater than 83% chance that this decline in fossil fuel consumption plateaus after 2060, remaining stubbornly high at more than 60% of today’s levels. Without a significant acceleration in policy and clean energy innovation, there is a greater than 50% chance that fossil fuel consumption begins to rise again after mid-century, driven largely by a rise in natural gas demand, a slowing reduction of coal use in industry, and a rebound in oil consumption to meet global aviation, shipping, and plastic demand.

5. Getting below 2°C will require making clean energy cheap beyond the OECD and China.

Emissions from OECD countries and China—today’s highest emitters—are very likely to decline significantly through mid-century, thanks in part to decades of policy and investments that have brought down the costs of renewable electricity and electric vehicle batteries, positioning these technologies to scale rapidly in the years ahead. The bulk of emissions growth in the future, however, will come from other emerging markets—particularly India and other non-OECD countries in Asia, the Middle East, and Africa—driven by economic growth and rising industrial production. Keeping the increase in global temperatures below 2°C will require investing in the deployment of mature clean energy technologies in these regions, and a significant acceleration of policy and innovation to drive down the cost of emerging clean technologies required to decarbonize hard-to-abate sectors—like industry, shipping, and aviation—to make those solutions affordable for all regions to adopt at scale.

In the first chapter of our inaugural Rhodium Climate Outlook report, we introduce the RCO approach and how it addresses gaps left by other existing global emissions and energy outlooks. In the following chapters, we present our results, first globally, then by sector, and last by region. We end with an overview of key drivers of global emissions and sources of uncertainty in possible climate futures.